Thanks Brute! A bit hard to explain without doxing myself, as there are only 3–4 companies in the world offering a similar product. It is a specific service that helps companies solve a specific problem.

My company only offers two standardized products which combine my experience with two, three external suppliers into the final product. A lot of it is automated, so I do not have to do much operational work.

Yearly profit could be anywhere from –3000 to 120,000 EUR, I would consider it a success if it could be over EUR 1,000 a month. Launch is now planned for October 1, if all works out with the bureaucracy.

Singvestor's awakening

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #38: August 2018

It is embarassing, but...

- 20 days no alcohol: failed: 18 days

- 12 times sports: failed: 7 times

September is not looking to good either, oh man.

October will be better.

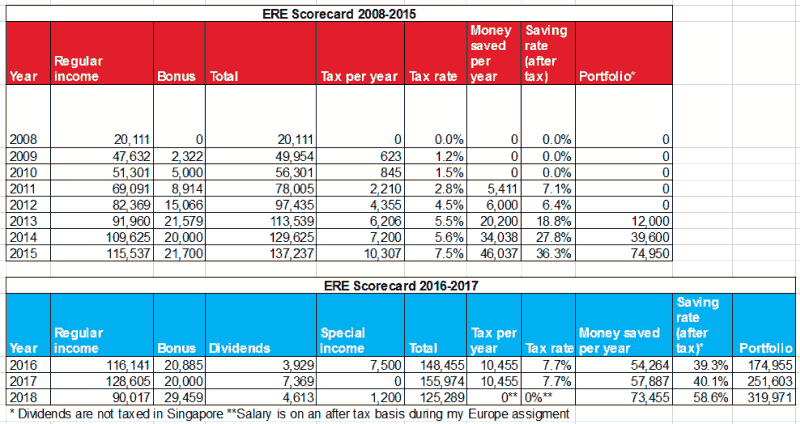

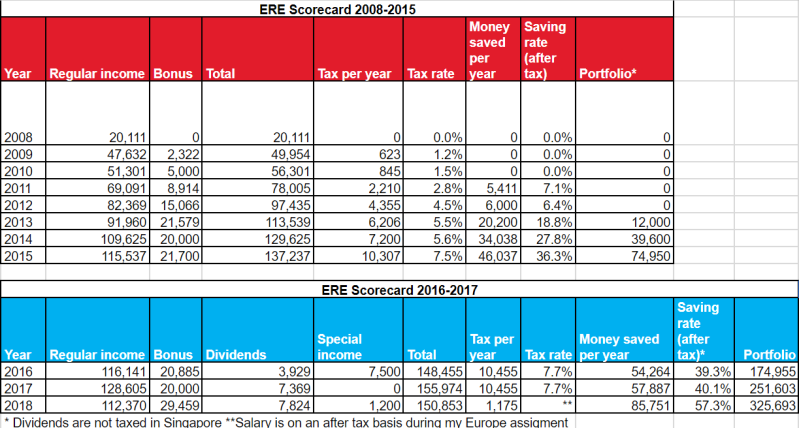

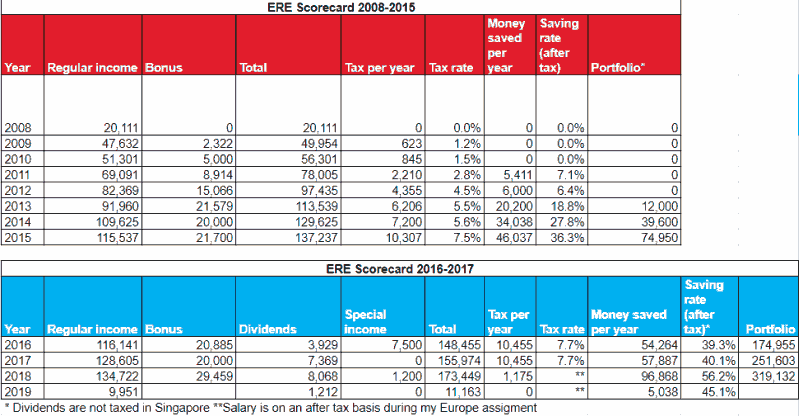

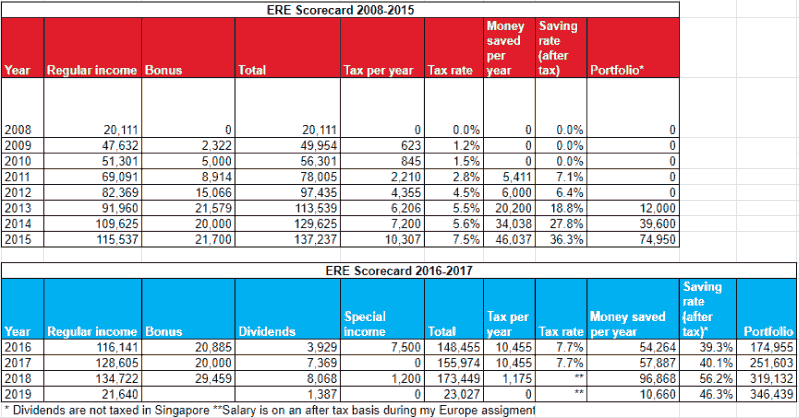

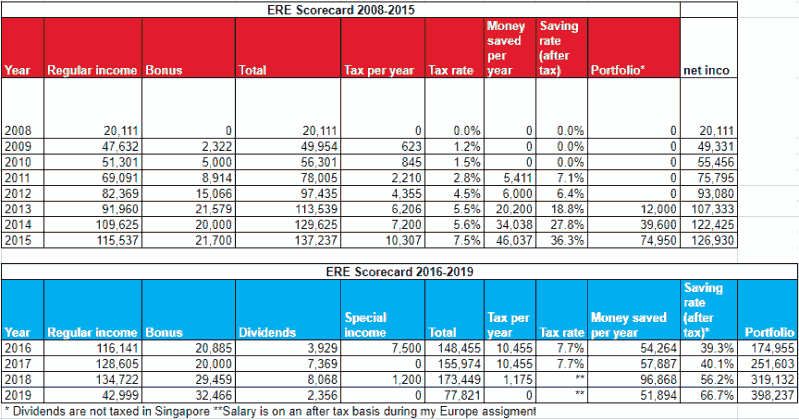

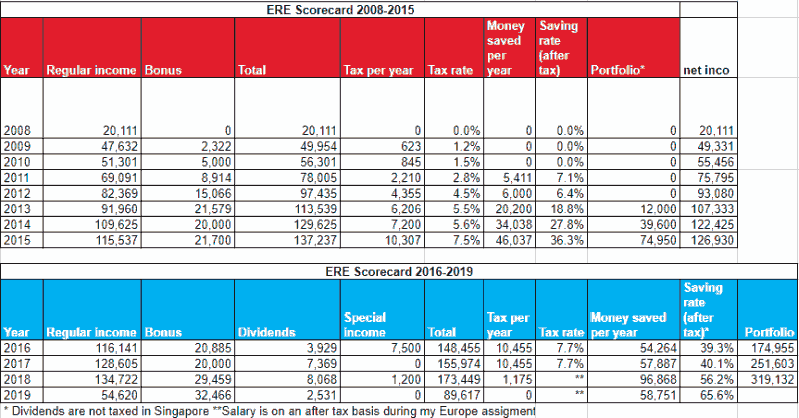

ERE Scorecard August

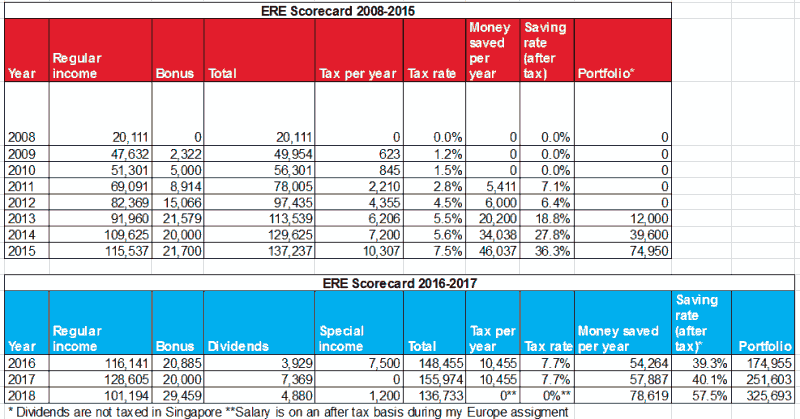

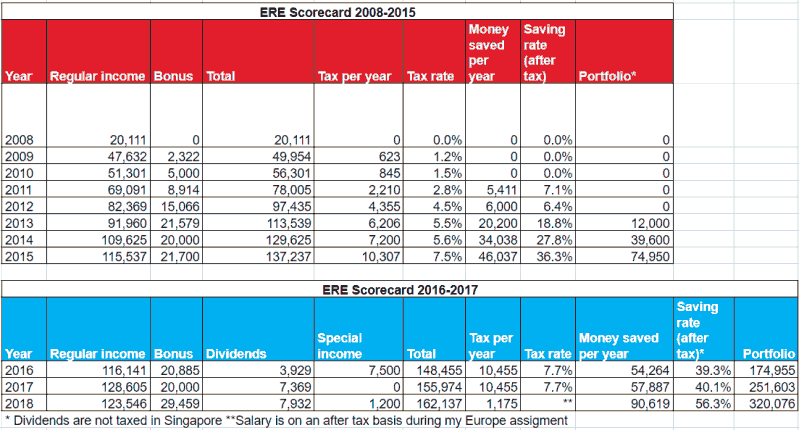

Saving rate was 50% for August, year-to-date saving rate is 59%.

File gone ☹

I managed to lose my Excel file with all my charts and data. Only had a six-month-old backup. Now I migrated everything to Google sheets, but the charts are not as good. Google Sheets is quite limited in this regard. On the other hand being able to access the file from multiple devices is great.

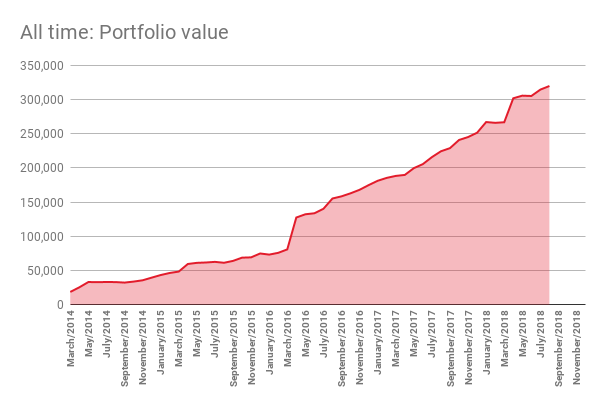

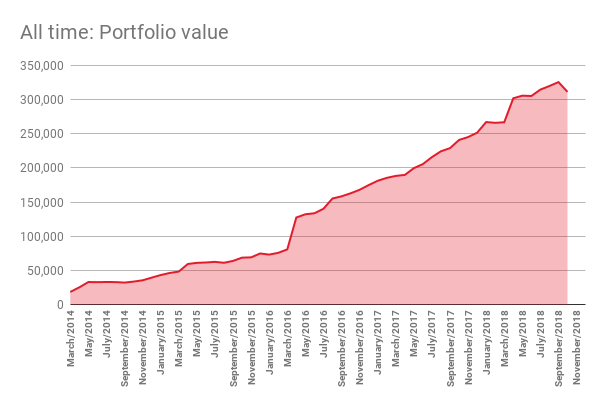

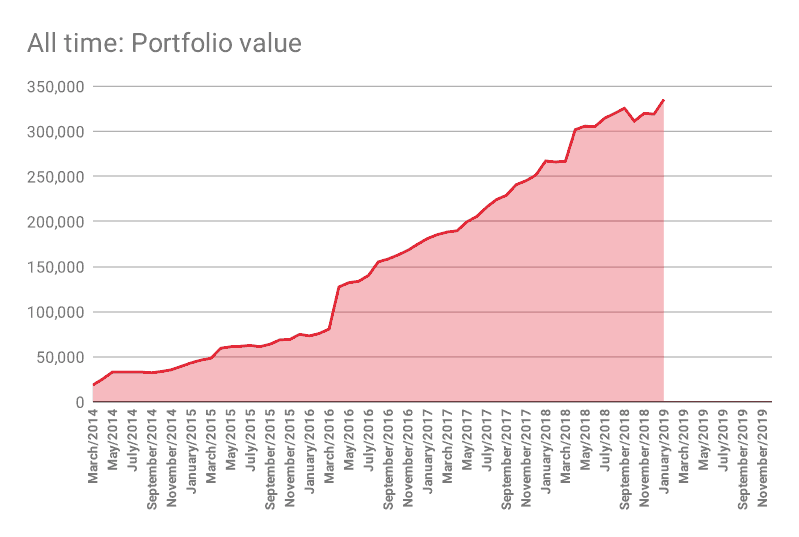

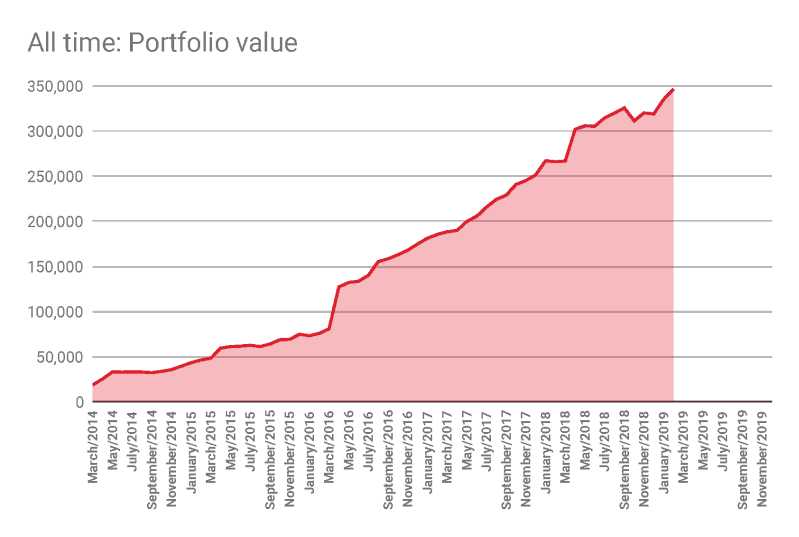

Portfolio update

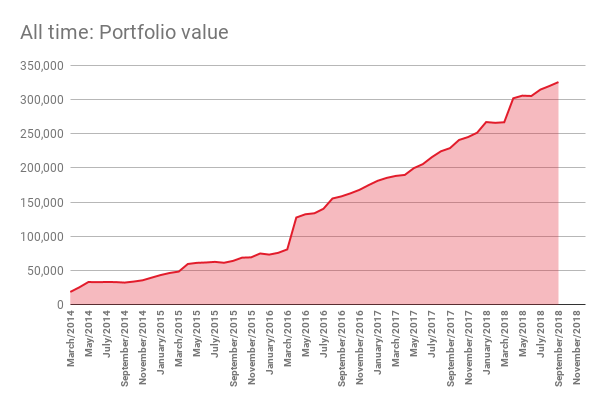

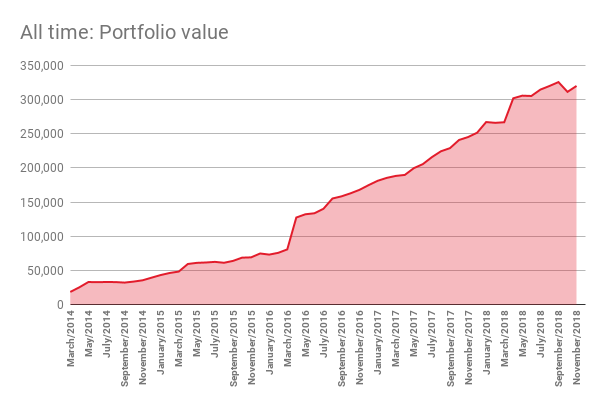

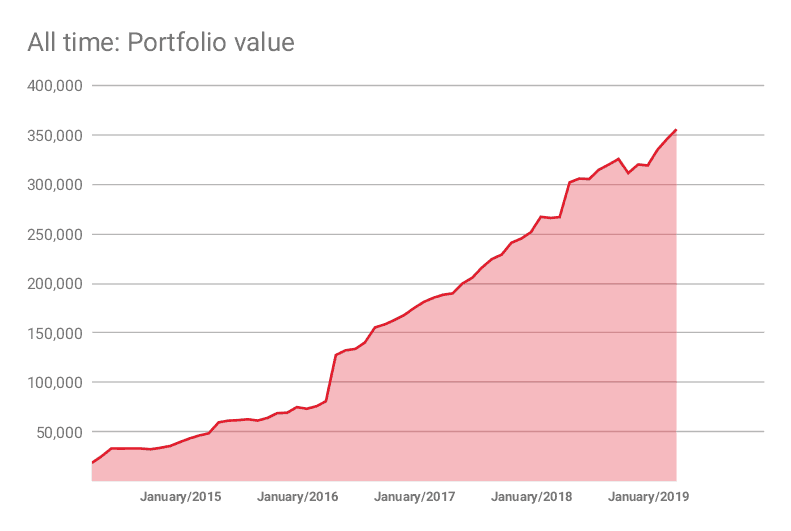

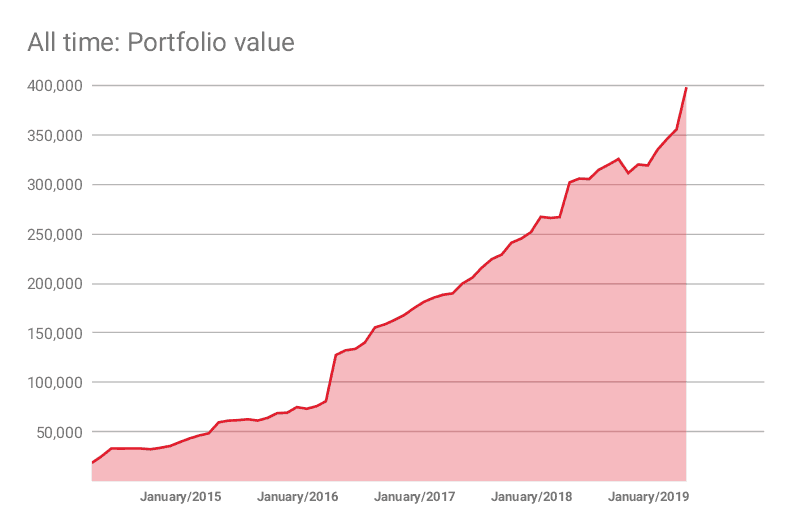

In August my portfolio increased by SGD 5,265 or 1.7% to SGD 319,971 (USD 232,841). Fresh investments of SGD 6,023 and decline of SGD 758 contributed.

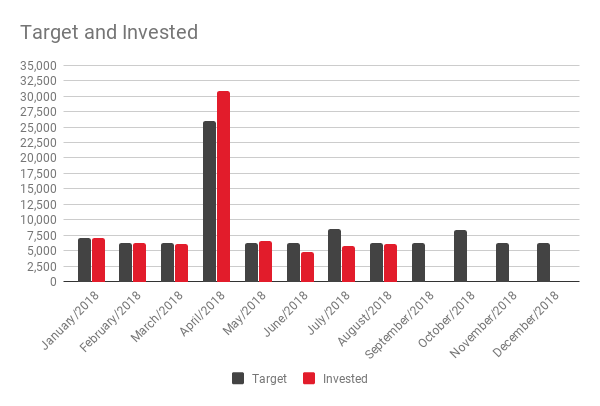

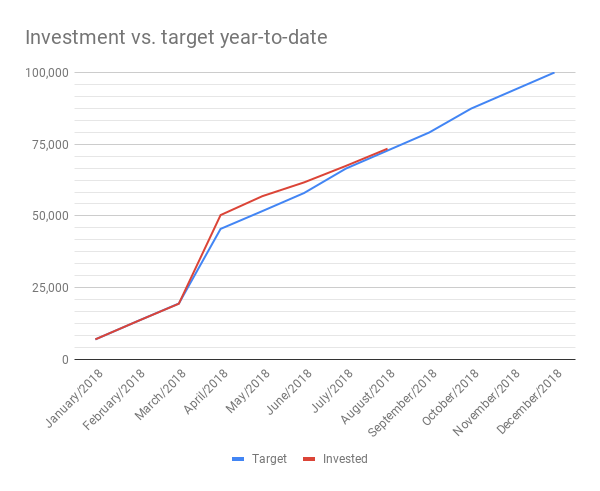

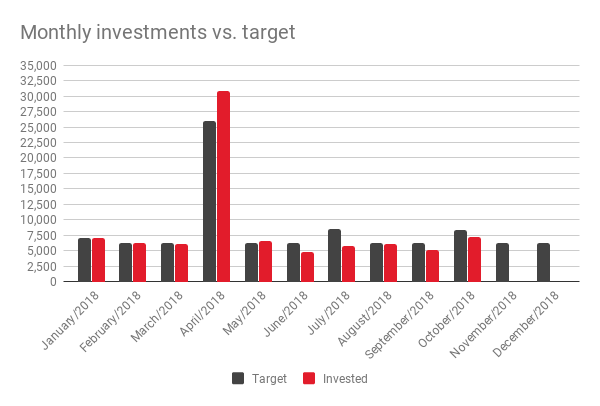

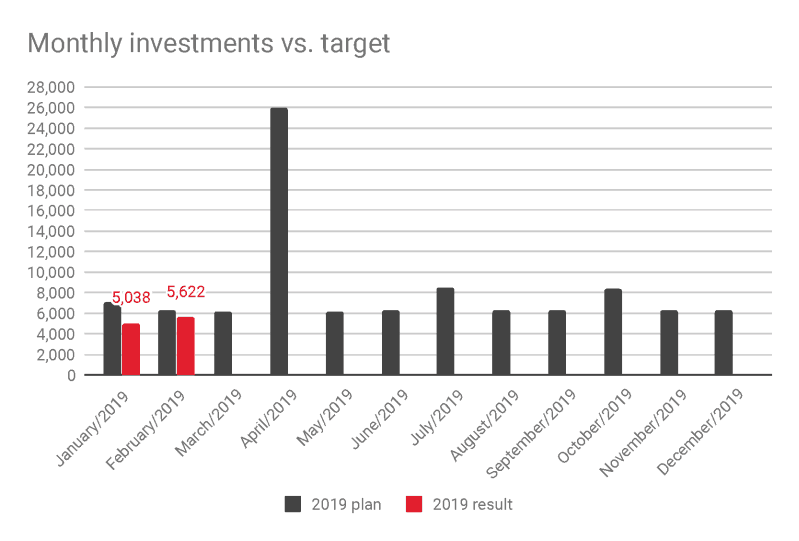

Investments vs. plan

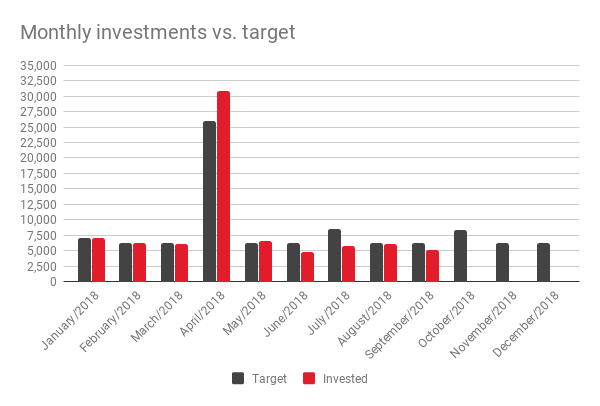

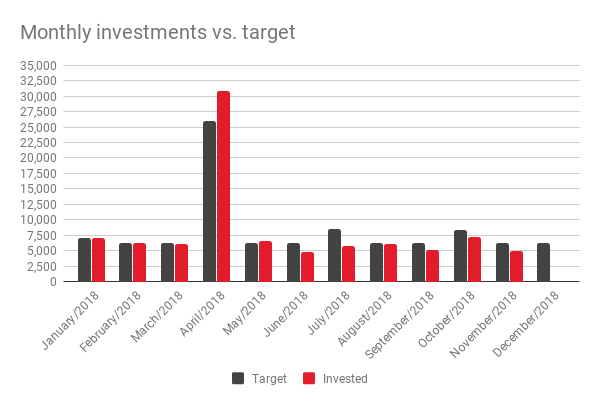

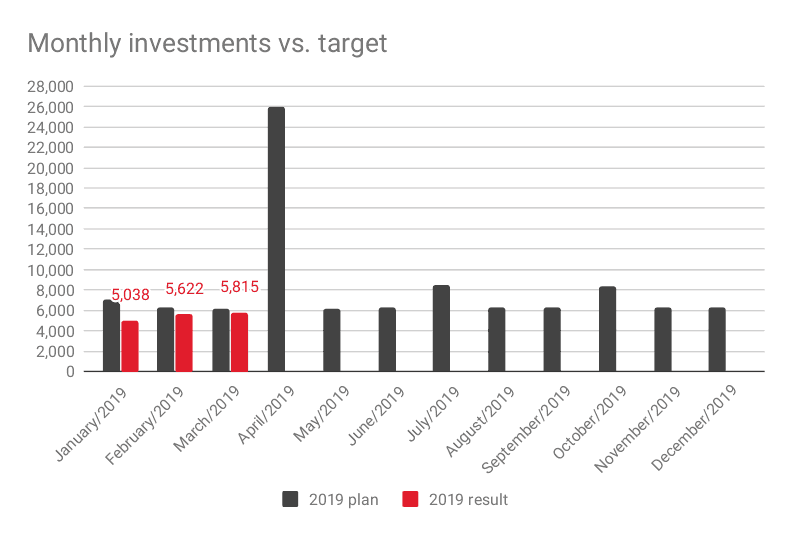

I invested SGD 6,023 into my portfolio which was less than planned (SGD 6,300).

Fortunately, I am still ahead of the plan, thanks to a good performance in previous months.

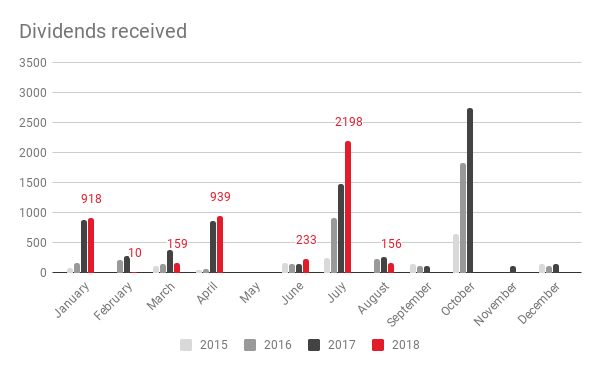

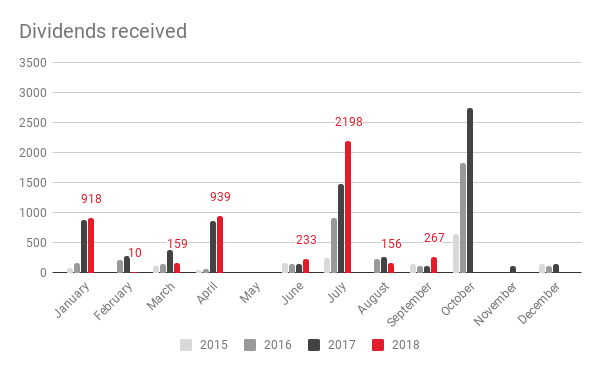

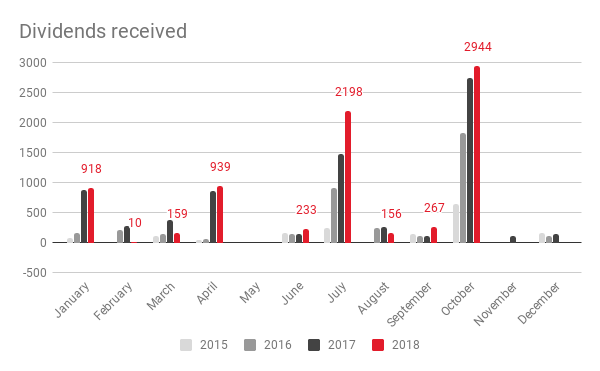

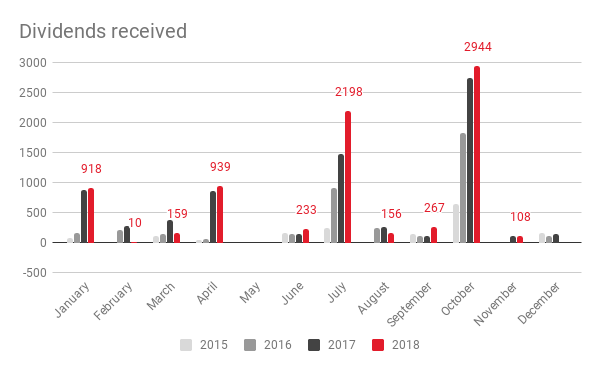

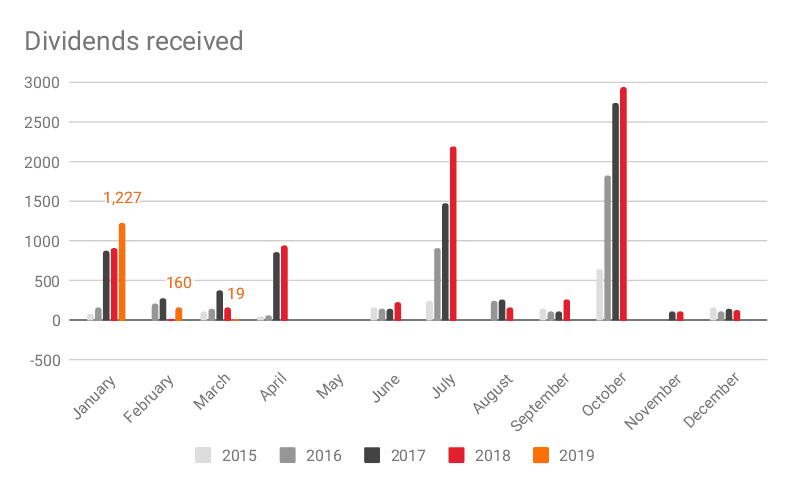

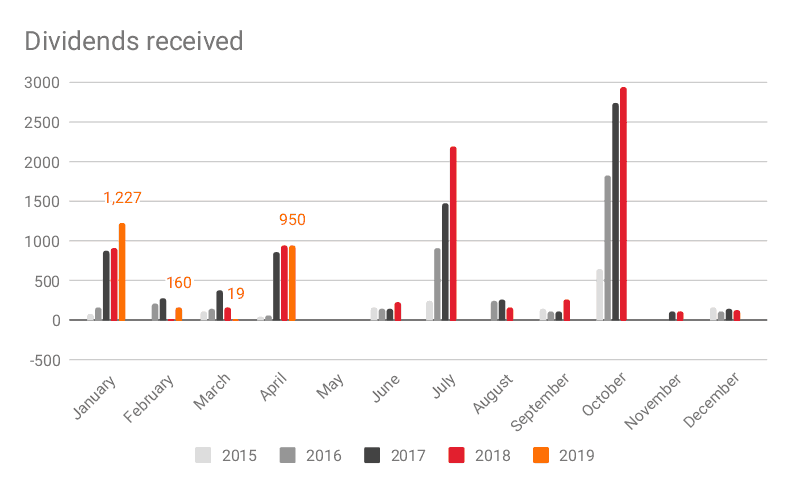

Dividends received

SGD 156

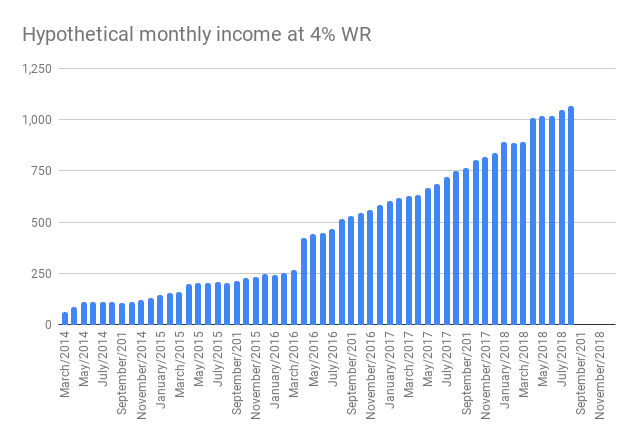

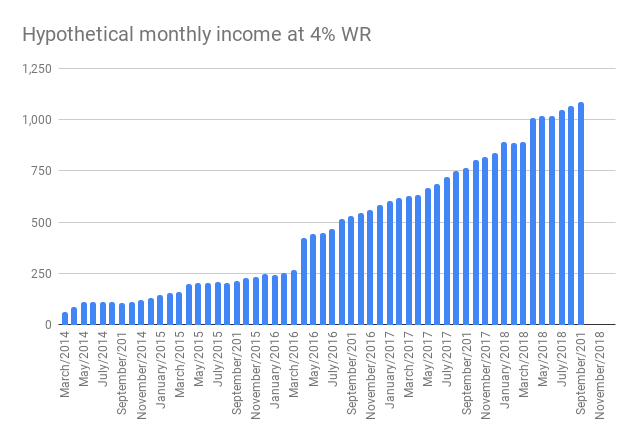

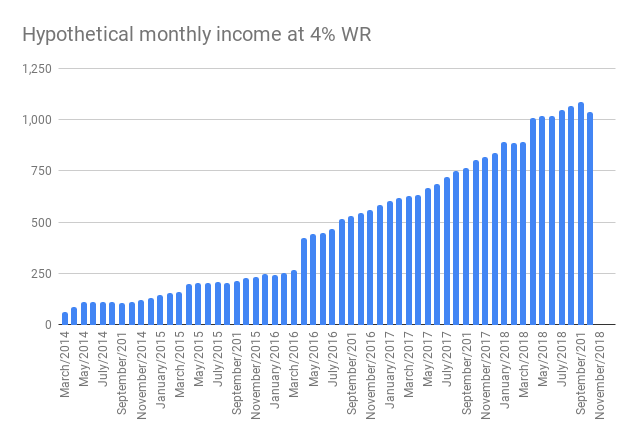

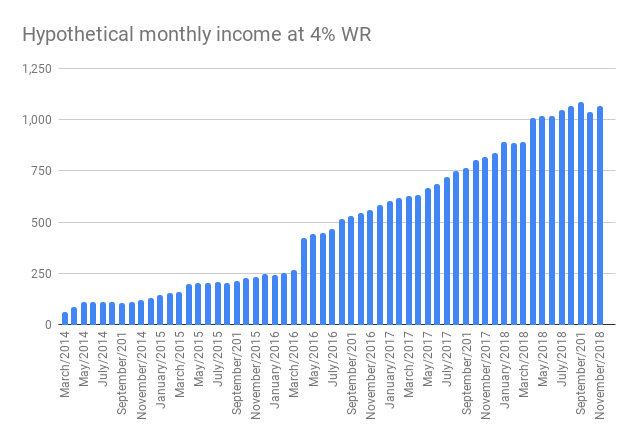

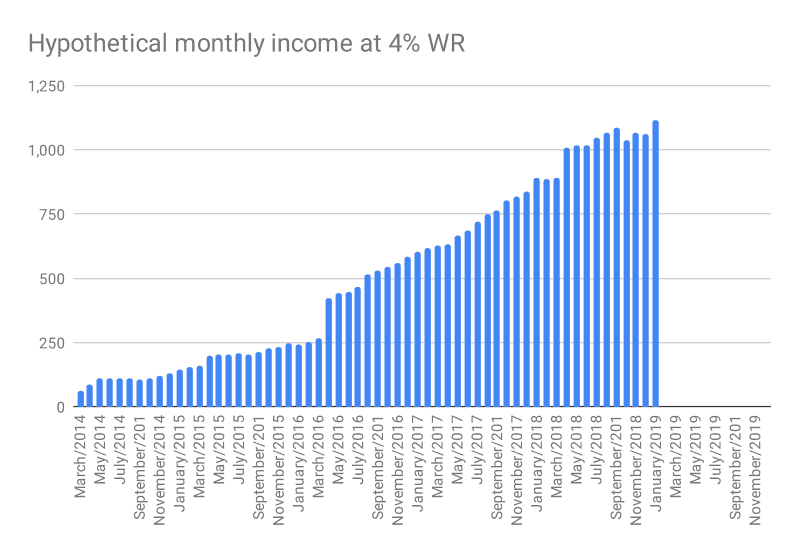

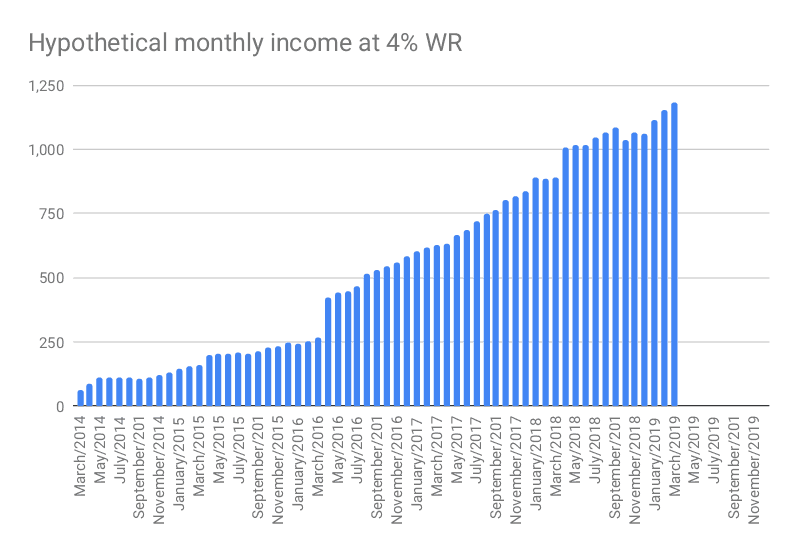

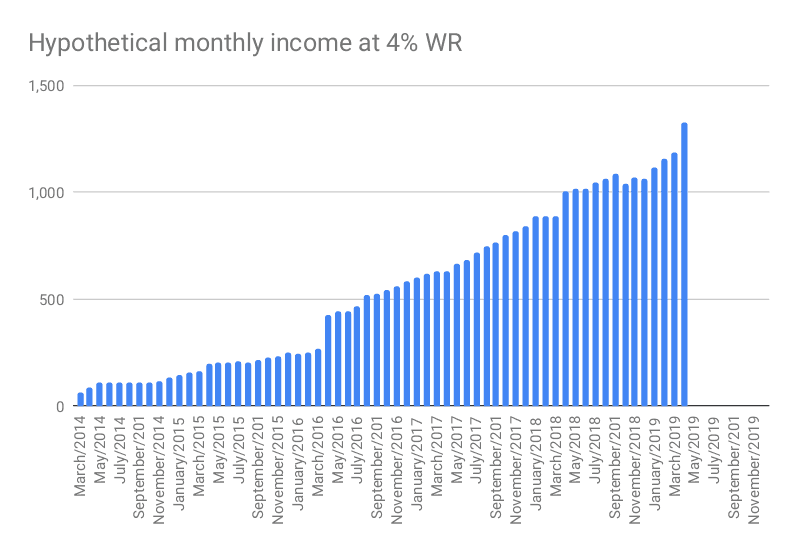

Hypothetical monthly income (4% WR)

SGD 1,067 – crawling up a hill.

Outlook

My own company is making progress, but European bureaucracy is a battle. Hopefully everything is ready in October so I can hunt some customers. Chance of success: 20%.

- 20 days no alcohol: failed: 18 days

- 12 times sports: failed: 7 times

September is not looking to good either, oh man.

October will be better.

ERE Scorecard August

Saving rate was 50% for August, year-to-date saving rate is 59%.

File gone ☹

I managed to lose my Excel file with all my charts and data. Only had a six-month-old backup. Now I migrated everything to Google sheets, but the charts are not as good. Google Sheets is quite limited in this regard. On the other hand being able to access the file from multiple devices is great.

Portfolio update

In August my portfolio increased by SGD 5,265 or 1.7% to SGD 319,971 (USD 232,841). Fresh investments of SGD 6,023 and decline of SGD 758 contributed.

Investments vs. plan

I invested SGD 6,023 into my portfolio which was less than planned (SGD 6,300).

Fortunately, I am still ahead of the plan, thanks to a good performance in previous months.

Dividends received

SGD 156

Hypothetical monthly income (4% WR)

SGD 1,067 – crawling up a hill.

Outlook

My own company is making progress, but European bureaucracy is a battle. Hopefully everything is ready in October so I can hunt some customers. Chance of success: 20%.

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #39: September 2018

What a disaster, monthly goal review:

- 20 days no alcohol: failed: 14 days

- 12 times sports: failed: 8 times

I will fix this in October. Calories in > calories out. 2 kgs of weight to reduce in October. Same program like in July.

Morroco

Traveled through Morocco and Southern Spain with DW and a group of close friends that I have known since childhood. Amazing experience that provided a lot of clarity and outside perspective. Felt holiday afterglow that urged me to quit job and drive off into the sunset trusting that things will be fine. Existential crisis when returning to day job polishing political PowerPoints.

Own company

Spent some more money on establishing own company. Guess about SGD 700 or so. Will do the detailed accounting of company costs at the end of the year and just count it as spending for now.

ERE Scorecard

Saving rate for September was 45%. Ouch. Did not buy unneccessary stuff, but had a long vacation and attended a wedding of a very close friend whom I gave EUR 500 as a wedding gift. Rest of the year will be more frugal with all trips and weddings completed.

Portfolio update

In September my portfolio increased by SGD 5,722 or 1.8% to SGD 325,693 (=USD 237,500). Fresh investments of SGD 5,164 and gains of SGD 558 contributed.

Investments vs. plan

I invested SGD 5,164 into my portfolio which was less than planned (SGD 6,300). This means that I am now SGD 481 behind the plan for the year. I need to be a bit more frugal, especially since I need to spend some money for the new company.

Dividends received

SGD 267 - not bad.

Hypothetical monthly income

SGD 1,086. Looking forward to the SGD 1,600/month milestone at SGD 480k at which I will get EUR 1,000 monthly for life

Outlook

Rest of the year will feature stress at work, but I have no more big travels planned. Key focus is to get the own company off the ground as fast as possible.

- 20 days no alcohol: failed: 14 days

- 12 times sports: failed: 8 times

I will fix this in October. Calories in > calories out. 2 kgs of weight to reduce in October. Same program like in July.

Morroco

Traveled through Morocco and Southern Spain with DW and a group of close friends that I have known since childhood. Amazing experience that provided a lot of clarity and outside perspective. Felt holiday afterglow that urged me to quit job and drive off into the sunset trusting that things will be fine. Existential crisis when returning to day job polishing political PowerPoints.

Own company

Spent some more money on establishing own company. Guess about SGD 700 or so. Will do the detailed accounting of company costs at the end of the year and just count it as spending for now.

ERE Scorecard

Saving rate for September was 45%. Ouch. Did not buy unneccessary stuff, but had a long vacation and attended a wedding of a very close friend whom I gave EUR 500 as a wedding gift. Rest of the year will be more frugal with all trips and weddings completed.

Portfolio update

In September my portfolio increased by SGD 5,722 or 1.8% to SGD 325,693 (=USD 237,500). Fresh investments of SGD 5,164 and gains of SGD 558 contributed.

Investments vs. plan

I invested SGD 5,164 into my portfolio which was less than planned (SGD 6,300). This means that I am now SGD 481 behind the plan for the year. I need to be a bit more frugal, especially since I need to spend some money for the new company.

Dividends received

SGD 267 - not bad.

Hypothetical monthly income

SGD 1,086. Looking forward to the SGD 1,600/month milestone at SGD 480k at which I will get EUR 1,000 monthly for life

Outlook

Rest of the year will feature stress at work, but I have no more big travels planned. Key focus is to get the own company off the ground as fast as possible.

Re: Singvestor's awakening

What’s your alcohol spending month to month? Thoughts on a spending target vs. a days without alcohol target?

Also what’s the motivation? Health? Weight? Negative aspects of intoxicated singvestor? Hangovers?

Also what’s the motivation? Health? Weight? Negative aspects of intoxicated singvestor? Hangovers?

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Re: Singvestor's awakening

Interesting ideas!

Alcohol spending is overall very small in the big theme of things. Health and maintaining my weight are the primary drivers for reducing alcohol. I figured out that 12 days sports and 20 days no alcohol are the ideal balance to keep weight and fitnesslevel constant for me.

Life without any alcohol would be the best from a health perspective, but I love drinking beer to much to accomplish that. Terrible but true

Alcohol spending is overall very small in the big theme of things. Health and maintaining my weight are the primary drivers for reducing alcohol. I figured out that 12 days sports and 20 days no alcohol are the ideal balance to keep weight and fitnesslevel constant for me.

Life without any alcohol would be the best from a health perspective, but I love drinking beer to much to accomplish that. Terrible but true

Re: Singvestor's awakening

What about limiting alco to Fridays & Saturdays (8 days a month) plus 2 'wild cards' per month (for a total of 10d/m)?

You could then workout every Mon, Wed & Fri (before having a beer on Fri evening) for a total of 12d/m.

Alternatively, the cycle of 2 days of work out, a day of drinking, 1 day of workout, a day of drinking & repeat. This way you would always work out at least 1.5x as many days as you'd be drinking, or at least not drink if you've not exercised. Although a con of this approach is associating alco with reward (for working out).

You could then workout every Mon, Wed & Fri (before having a beer on Fri evening) for a total of 12d/m.

Alternatively, the cycle of 2 days of work out, a day of drinking, 1 day of workout, a day of drinking & repeat. This way you would always work out at least 1.5x as many days as you'd be drinking, or at least not drink if you've not exercised. Although a con of this approach is associating alco with reward (for working out).

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #40: October 2018

Back on track, monthly goal review:

- 20 days no alcohol: achieved: 20 days

- 12 times sports: achieved: 12 times

Thanks, guys, for your encouragement! Now that I have stabilized the alcohol and sport it is time to increase the sport effort.

October

Work was tiring, so was the setup of the own company which is still ongoing. Still working on it with full steam, so far it has only cost money but have not found a single customer. Was focusing very much on the logistics of the company, but did not look for customers actively. The plan is to stay in soft launch mode until January and then kick off the active promotion.

ERE Scorecard

Saving rate for October was 51%. Would have been better, but got a surprising tax bill for SGD 1,175 (about USD 850). Strange way of calculating, but did not want to fight HR, since the company tax equalizes me in Europe which costs them a ton.

Portfolio update

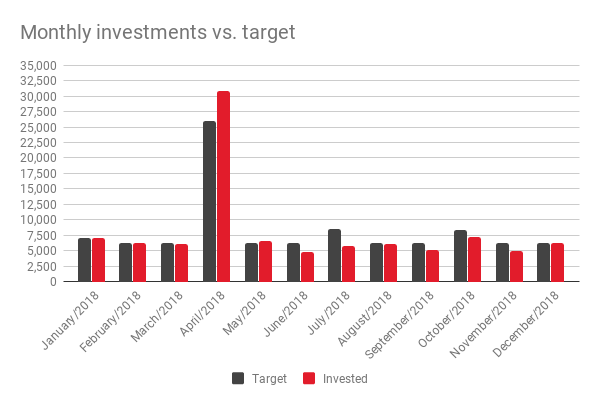

October was the worst month since I started tracking my portfolio. Portfolio declined by SGD 14,299 to SGD 311,394 (USD 226,200). Fresh investments of SGD 7,132 were offset by a decline of SGD 21,431

Investments vs. plan

I invested SGD 7,132 into my portfolio which was less than planned (SGD 8,300). This means that I am now SGD 1,649 behind the plan for the year.

Own company has cost over SGD 3,000 so far and will probably cost another SGD 2,000 or so until it is fully operational.

Dividends received

SGD 2,944 – new record.

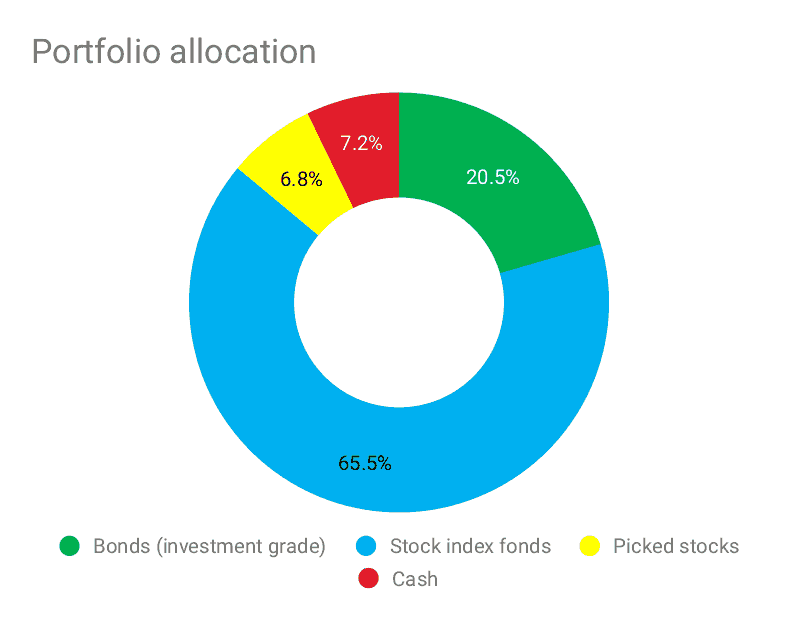

Portfolio allocation

When Asian stocks were taking a beating in October, I used the chance to buy some Bank of China stock which was quite cheap in my opinion and comes with a nice dividend yield. This reduced the cash portion of the portfolio a bit.

Hypothetical monthly income

SGD 1,038. Things are going backward a bit, but I will keep on with the program.

Outlook

Own company is still in focus.

Heavy allocation towards Asian stock is making this year difficult – SGD 26,000 in unrealized losses so far. It does not overly concern me as I am still in the middle of the accumulation phase.

Life in Europe is more interesting than in Singapore somehow. I have stopped obsessing over the portfolio and personal finances. Not yet sure if this is good or not!

- 20 days no alcohol: achieved: 20 days

- 12 times sports: achieved: 12 times

Thanks, guys, for your encouragement! Now that I have stabilized the alcohol and sport it is time to increase the sport effort.

October

Work was tiring, so was the setup of the own company which is still ongoing. Still working on it with full steam, so far it has only cost money but have not found a single customer. Was focusing very much on the logistics of the company, but did not look for customers actively. The plan is to stay in soft launch mode until January and then kick off the active promotion.

ERE Scorecard

Saving rate for October was 51%. Would have been better, but got a surprising tax bill for SGD 1,175 (about USD 850). Strange way of calculating, but did not want to fight HR, since the company tax equalizes me in Europe which costs them a ton.

Portfolio update

October was the worst month since I started tracking my portfolio. Portfolio declined by SGD 14,299 to SGD 311,394 (USD 226,200). Fresh investments of SGD 7,132 were offset by a decline of SGD 21,431

Investments vs. plan

I invested SGD 7,132 into my portfolio which was less than planned (SGD 8,300). This means that I am now SGD 1,649 behind the plan for the year.

Own company has cost over SGD 3,000 so far and will probably cost another SGD 2,000 or so until it is fully operational.

Dividends received

SGD 2,944 – new record.

Portfolio allocation

When Asian stocks were taking a beating in October, I used the chance to buy some Bank of China stock which was quite cheap in my opinion and comes with a nice dividend yield. This reduced the cash portion of the portfolio a bit.

Hypothetical monthly income

SGD 1,038. Things are going backward a bit, but I will keep on with the program.

Outlook

Own company is still in focus.

Heavy allocation towards Asian stock is making this year difficult – SGD 26,000 in unrealized losses so far. It does not overly concern me as I am still in the middle of the accumulation phase.

Life in Europe is more interesting than in Singapore somehow. I have stopped obsessing over the portfolio and personal finances. Not yet sure if this is good or not!

-

prognastat

- Posts: 991

- Joined: Fri May 04, 2018 8:30 pm

- Location: Texas

- Contact:

Re: Singvestor's awakening

Good work on sticking to your goals.

What's your eventual goal you're working towards with both exercise and alcohol?

What's your eventual goal you're working towards with both exercise and alcohol?

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Re: Singvestor's awakening

Hi prognatsat, the overall goal is to be healthy, non-fat and stable. More or less on track

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #41: November 2018

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 12 times

Not great, but then it is November...

November

Overall quite a terrible month, because of work. It is really not fun. On the other hand I am being overpaid for the work that I do.

Had a small health scare and needed extensive health checkup, but all seems to be ok so far. Gave me a lot to think about priorities in life and mortality.

Outrageous predictions

I feel like there is a recession around the corner in Europe, especially in Germany. While I know I cannot predict the market or the economy, I have a very strong feeling that it is going to happen soon. Already there were profit warnings in some of the big German companies and the mood in my company is so much worse than usual.

ERE Scorecard

Saving rate was a paltry 43% - not good at all. I buffered a bit of cash since I had a lot of doctor bills to pay (which I can claim back from insurance) and also want to buy a nice Christmas gift for my parents (a joint vacation).

Portfolio update

Portfolio increased by SGD 8,682 to SGD 320,076 (USD 233,500). Fresh investments of SGD 4,868 and gains of SGD 3,814 contributed.

Investments vs. plan

I invested SGD 4,868 into my portfolio which was less than planned (SGD 6,300). This means that I am now SGD 3,081 behind the plan for the year. Seems like I cannot make my six figure investment goal, bummer.

Dividends received

SGD 108.

Hypothetical monthly income

SGD 1,067

Outlook

The year is nearly over already and I am quite exhausted. There are 15 more months in my assignment to Europe and I am glad it has an expiration date. So much fun to live here, but the job is a bit of a disappointment.

- 12 times sports: achieved: 12 times

Not great, but then it is November...

November

Overall quite a terrible month, because of work. It is really not fun. On the other hand I am being overpaid for the work that I do.

Had a small health scare and needed extensive health checkup, but all seems to be ok so far. Gave me a lot to think about priorities in life and mortality.

Outrageous predictions

I feel like there is a recession around the corner in Europe, especially in Germany. While I know I cannot predict the market or the economy, I have a very strong feeling that it is going to happen soon. Already there were profit warnings in some of the big German companies and the mood in my company is so much worse than usual.

ERE Scorecard

Saving rate was a paltry 43% - not good at all. I buffered a bit of cash since I had a lot of doctor bills to pay (which I can claim back from insurance) and also want to buy a nice Christmas gift for my parents (a joint vacation).

Portfolio update

Portfolio increased by SGD 8,682 to SGD 320,076 (USD 233,500). Fresh investments of SGD 4,868 and gains of SGD 3,814 contributed.

Investments vs. plan

I invested SGD 4,868 into my portfolio which was less than planned (SGD 6,300). This means that I am now SGD 3,081 behind the plan for the year. Seems like I cannot make my six figure investment goal, bummer.

Dividends received

SGD 108.

Hypothetical monthly income

SGD 1,067

Outlook

The year is nearly over already and I am quite exhausted. There are 15 more months in my assignment to Europe and I am glad it has an expiration date. So much fun to live here, but the job is a bit of a disappointment.

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #42: December 2018 + Full year 2018

Worst things first:

December monthly goal review:

20 days without alcohol: failed: 14 days

12 times sport: achieved: 12 times

What a disaster. I immediately gained 2kgs in the process and now have to do the healthy January routine.

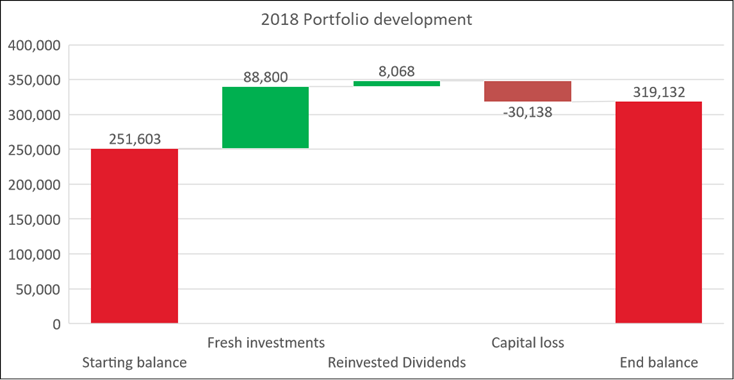

Portfolio update

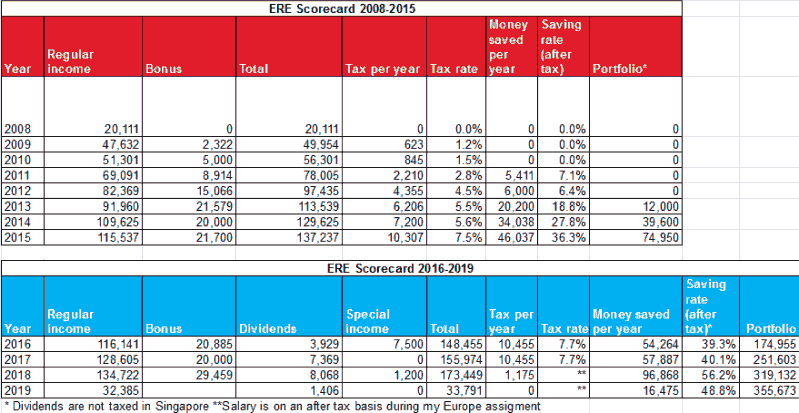

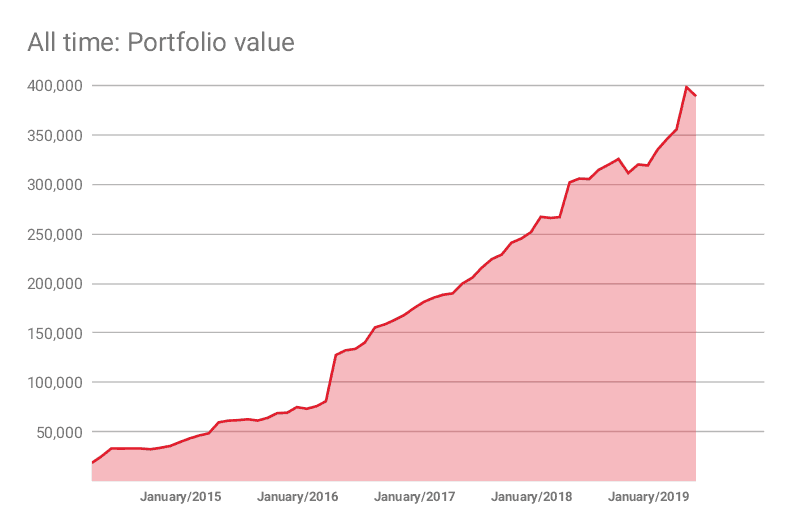

To celebrate the end of the year, I created a waterfall chart. In 2018 my portfolio grew from SGD 251,603 by SGD 67,529 to SGD 319,132. As you can see, the markets were not kind to my portfolio in 2018 and before dividends my portfolio depreciated by SGD 30,138.

Investment vs. goal

At the beginning of 2018 I had decided to save up SGD 100,000 during the year. Sad to say: I failed. I only managed to save SGD 96,868.

As you can see, I had a great start to the year, but then things deteriorated at the second half. Reasons were my own company which I have been busy setting up. Unfortunately, I spent quite a bit of money on it, but I has been worth the learning and experience.

Dividends receivedIn total I received SGD 8,068 in dividends. Not bad! It is surprising how quickly the dividends have been growing. I expect this figure to slow down quite a bit – since I am now investing in accumulating ETFs to optimize taxes.

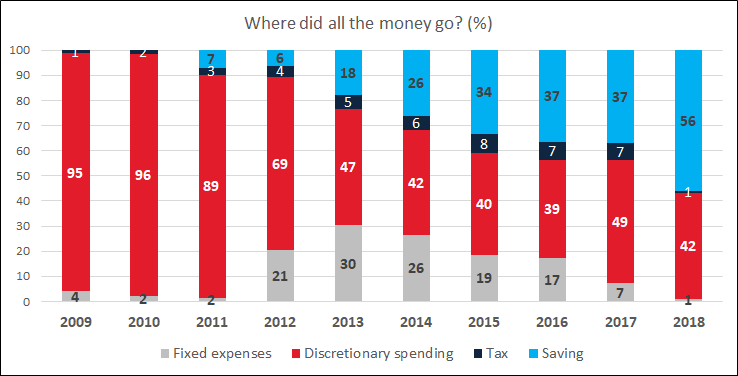

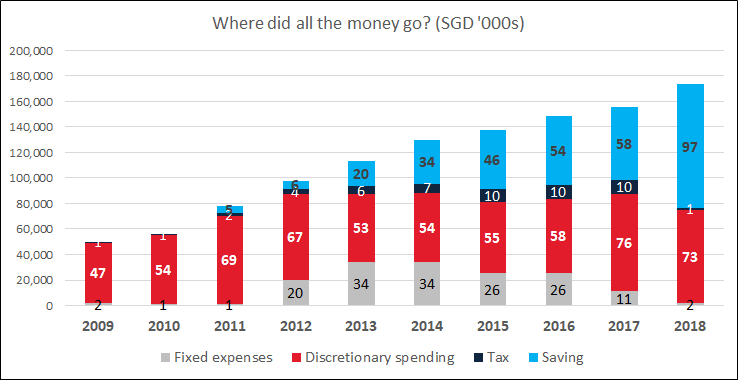

Where did all the money go?

At the beginning of every year I like to take stock of where my money is going. This is the result for 2018:

At first glance the picture looks quite positive: saving rate increased to 56% before tax, which is a nice increase. When zooming in, things do not look as rosy though:

In absolute terms it becomes obvious that I spent a massive SGD 73,203 on discretionary categories, such as food, travel, restaurants, shopping, my car, presents…

This kind of spending is absolutely too high. How could I spend USD 54,000 when I have free housing. I focused on the increasing income side for too long, this year I have to track all expenses.

Plan for 2019

- Invest SGD 100,000 – same plan as this year, but with more discipline

- Regular cardio exercise

- Track all expenses

December monthly goal review:

20 days without alcohol: failed: 14 days

12 times sport: achieved: 12 times

What a disaster. I immediately gained 2kgs in the process and now have to do the healthy January routine.

Portfolio update

To celebrate the end of the year, I created a waterfall chart. In 2018 my portfolio grew from SGD 251,603 by SGD 67,529 to SGD 319,132. As you can see, the markets were not kind to my portfolio in 2018 and before dividends my portfolio depreciated by SGD 30,138.

Investment vs. goal

At the beginning of 2018 I had decided to save up SGD 100,000 during the year. Sad to say: I failed. I only managed to save SGD 96,868.

As you can see, I had a great start to the year, but then things deteriorated at the second half. Reasons were my own company which I have been busy setting up. Unfortunately, I spent quite a bit of money on it, but I has been worth the learning and experience.

Dividends receivedIn total I received SGD 8,068 in dividends. Not bad! It is surprising how quickly the dividends have been growing. I expect this figure to slow down quite a bit – since I am now investing in accumulating ETFs to optimize taxes.

Where did all the money go?

At the beginning of every year I like to take stock of where my money is going. This is the result for 2018:

At first glance the picture looks quite positive: saving rate increased to 56% before tax, which is a nice increase. When zooming in, things do not look as rosy though:

In absolute terms it becomes obvious that I spent a massive SGD 73,203 on discretionary categories, such as food, travel, restaurants, shopping, my car, presents…

This kind of spending is absolutely too high. How could I spend USD 54,000 when I have free housing. I focused on the increasing income side for too long, this year I have to track all expenses.

Plan for 2019

- Invest SGD 100,000 – same plan as this year, but with more discipline

- Regular cardio exercise

- Track all expenses

Re: Singvestor's awakening

brute would call it a 96% success

100k is truly a massive savings goal. (about 75k USD, right?)

brute forgets, what's the endgame for Singvestor? staying in the fine city? slow travel? moving to Europe for good? something else?

100k is truly a massive savings goal. (about 75k USD, right?)

brute forgets, what's the endgame for Singvestor? staying in the fine city? slow travel? moving to Europe for good? something else?

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Re: Singvestor's awakening

Thanks Brute! About USD 75k is correct depending on the exchange rate.

End game is working freelance, in my own company or part time in some flexible arrangement to enjoy more Renaissance man leisure activities.

The dream case would be another international assignment on Singapore contract after this one and then ere-ing after.

End game is working freelance, in my own company or part time in some flexible arrangement to enjoy more Renaissance man leisure activities.

The dream case would be another international assignment on Singapore contract after this one and then ere-ing after.

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #43: January 2019

Back on track, monthly goal review:

- 20 days no alcohol: achieved: 24 days

- 12 times sports: achieved: 17 times

It felt good to exercise a lot. Not all of December’s weight gain has been reversed, but I feel fitter already. Keeping it up in February despite a 15-day vacation will be the challenging, but important.

January

Am a bit stuck with the new company I set up in Q4 last year. The product is solid, but I am having troubles finding customers. At first many potential clients are interested, but I am quite bad at selling. Something I have to learn!

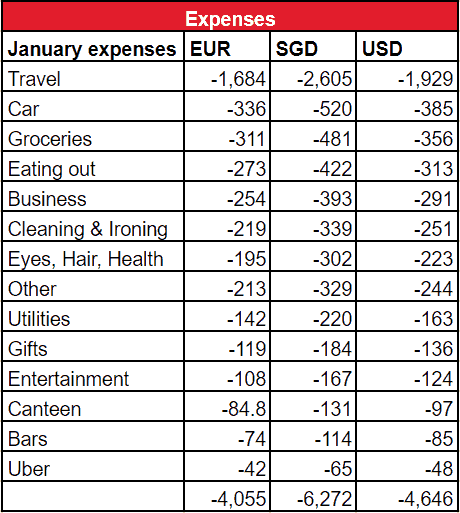

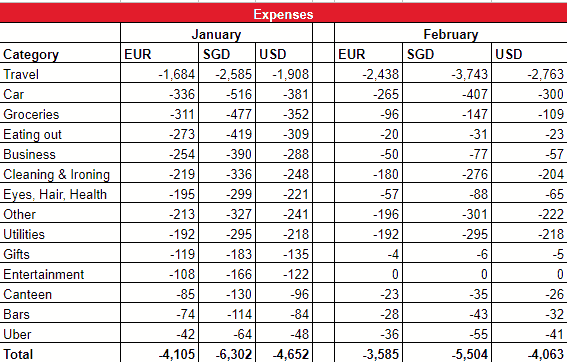

As planned, I tracked my expenses. Without further ado, here is my table of shame:

These are only my expenses; my wife and I keep separate accounts.

Travel: by far the biggest expense, as I booked a lot of holidays for the next six months and prepaid some of the hotels for a big trip to South Africa in February.

I have focused on the income and investing aspect so long in ERE and neglected the cost reduction aspect. Terrible. Between my wife and me we receive EUR 25 per working day in meal vouchers from our companies which we can use for supermarket purchases. Otherwise the grocery spending would be much higher.

Looking at this table I see tremendous opportunity for saving.

ERE Scorecard

Saving rate in January was only 45%. Not good at all.

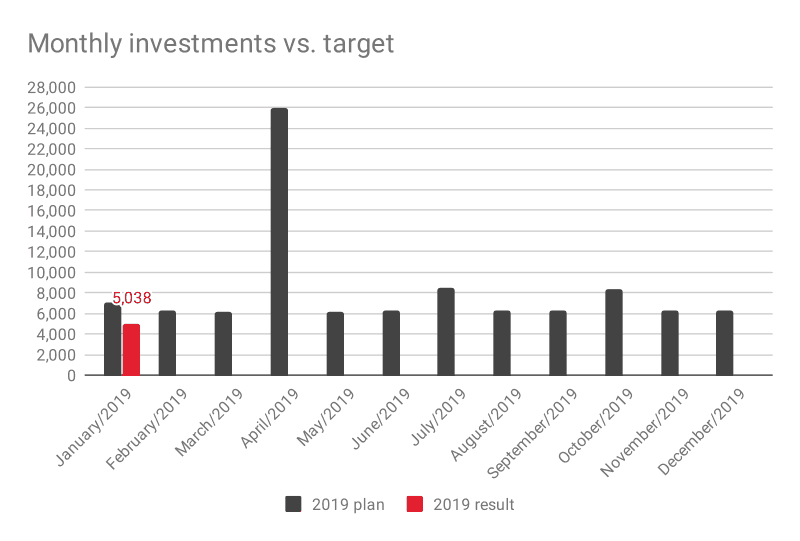

Portfolio update

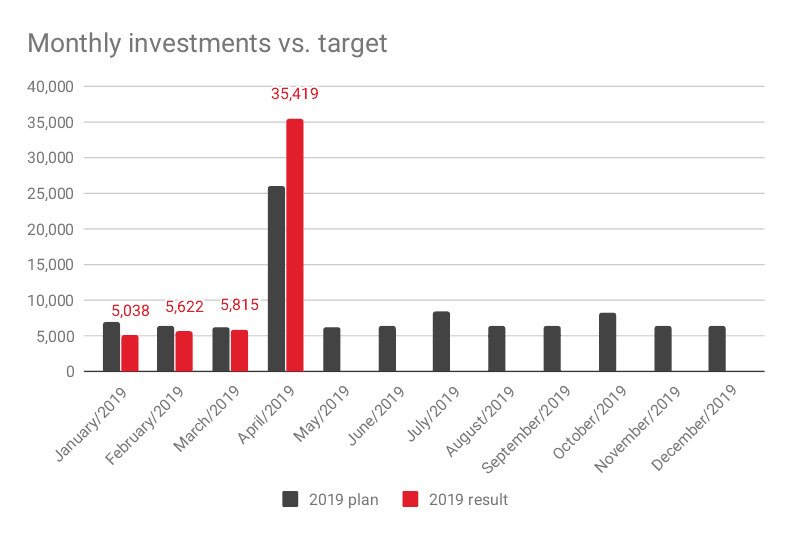

Portfolio increased by SGD 16,122 to SGD 335,254 (USD 248,300). Fresh investments of SGD 5,038 and gains of SGD 11,084 contributed. At the beginning of the month I would have bet on a big market decline in January, luckily I am not trying to time the market.

Investments vs. plan

I invested SGD 5,038 into my portfolio which was less than planned (SGD 7,000). This puts me in catch-up mode already in the first month of the year. Clearly all the expenses copied above are to blame.

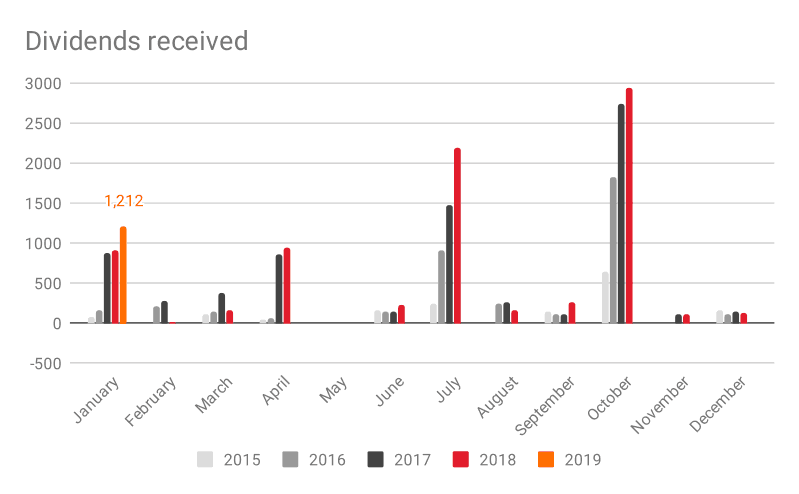

Dividends received

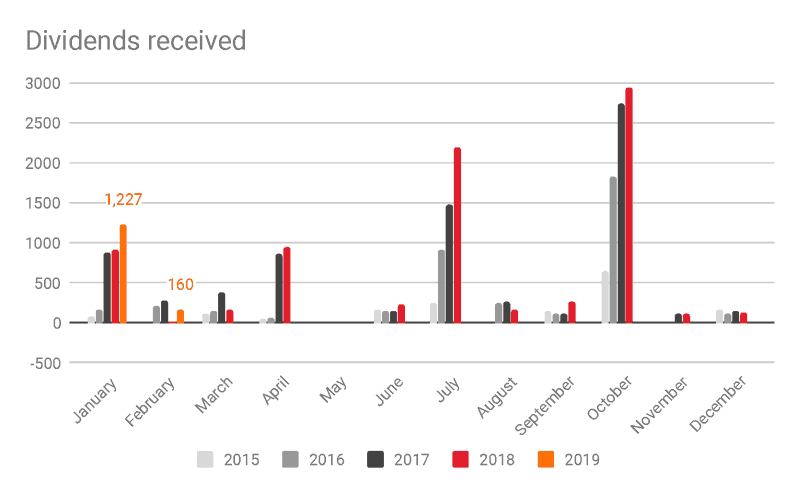

SGD 1,212 – nice.

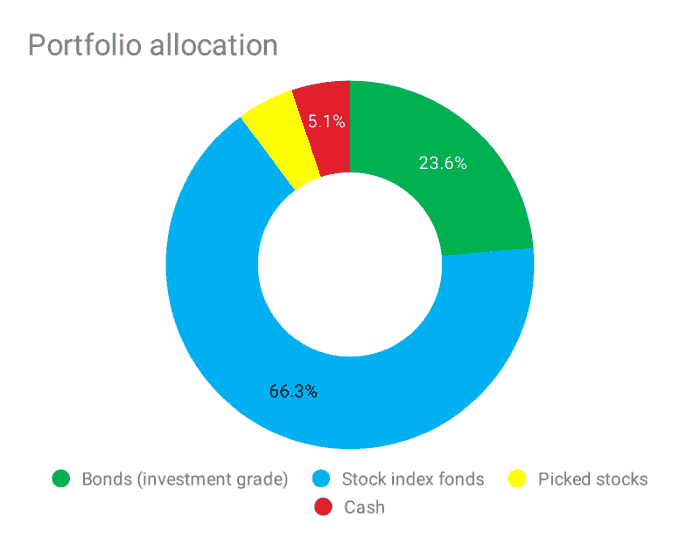

Portfolio allocation

Getting a bit light on the bonds, as my Singaporean broker does not allow me to buy bond ETFs while living in Europe and I have not figured out how to buy individual bonds, or if this is a bad idea.

Hypothetical monthly income

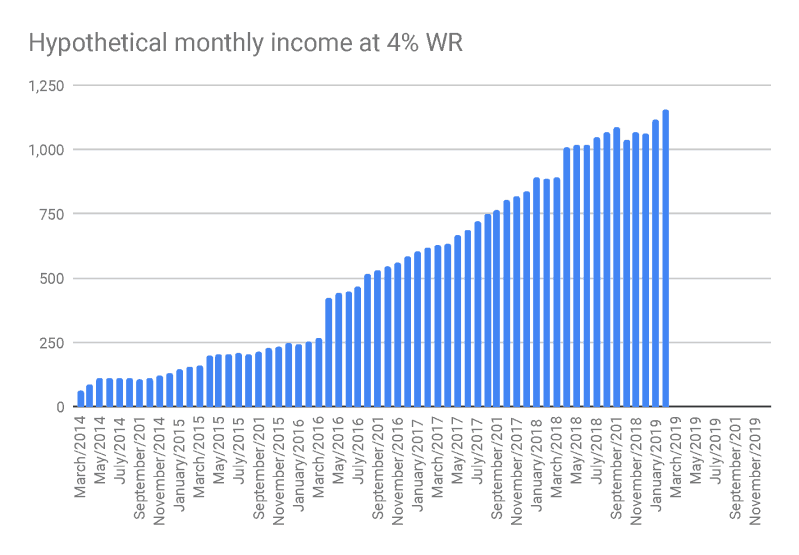

SGD 1,118. Things are going up again!

Outlook

Huge holiday planned in February, hope I will stay disciplined

- 20 days no alcohol: achieved: 24 days

- 12 times sports: achieved: 17 times

It felt good to exercise a lot. Not all of December’s weight gain has been reversed, but I feel fitter already. Keeping it up in February despite a 15-day vacation will be the challenging, but important.

January

Am a bit stuck with the new company I set up in Q4 last year. The product is solid, but I am having troubles finding customers. At first many potential clients are interested, but I am quite bad at selling. Something I have to learn!

As planned, I tracked my expenses. Without further ado, here is my table of shame:

These are only my expenses; my wife and I keep separate accounts.

Travel: by far the biggest expense, as I booked a lot of holidays for the next six months and prepaid some of the hotels for a big trip to South Africa in February.

I have focused on the income and investing aspect so long in ERE and neglected the cost reduction aspect. Terrible. Between my wife and me we receive EUR 25 per working day in meal vouchers from our companies which we can use for supermarket purchases. Otherwise the grocery spending would be much higher.

Looking at this table I see tremendous opportunity for saving.

ERE Scorecard

Saving rate in January was only 45%. Not good at all.

Portfolio update

Portfolio increased by SGD 16,122 to SGD 335,254 (USD 248,300). Fresh investments of SGD 5,038 and gains of SGD 11,084 contributed. At the beginning of the month I would have bet on a big market decline in January, luckily I am not trying to time the market.

Investments vs. plan

I invested SGD 5,038 into my portfolio which was less than planned (SGD 7,000). This puts me in catch-up mode already in the first month of the year. Clearly all the expenses copied above are to blame.

Dividends received

SGD 1,212 – nice.

Portfolio allocation

Getting a bit light on the bonds, as my Singaporean broker does not allow me to buy bond ETFs while living in Europe and I have not figured out how to buy individual bonds, or if this is a bad idea.

Hypothetical monthly income

SGD 1,118. Things are going up again!

Outlook

Huge holiday planned in February, hope I will stay disciplined

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #44: February 2019

monthly goal review:

- 20 days no alcohol: failed: 15 days

- 12 times sports: achieved: 13 times

I went on a big vacation and it was too tempting to sometimes have wine and beer. Not good!

February

Another brutal month in terms of expenses. I spent two weeks in South Africa which was probably one of the best experiences I ever had. All spending during this time (rental car, meals, restaurants) was combined into the “travel” category. My wife also paid for some things, but this table only shows my expenses, as we keep separate accounts.

Already now the expense tracking is proving eye opening. I am looking at this table and can’t believe these amounts. Now that a lot of the trips for the first half of 2019 are booked and paid I hope for some lower travel spending. I need to come up with a strategy to get the costs down.

I am doing ERE on easy mode with rent being paid for by the company - it is embarrassing to see this table.

ERE Scorecard

Saving rate in February was 51%. Better than in January, but still not good. The reason for this was the exorbitant travel spending during my trip in South Africa. I am basically on ERE easy mode with housing paid for by the company, yet I am spending too much money.

Portfolio update

Portfolio increased by SGD 11,185 to SGD 346,439 (USD 256,000). Fresh investments of SGD 5,622 and gains of SGD 5,563 contributed. The market is so optimistics this year - no idea what is going on!

Investments vs. plan

I invested SGD 5,622 into my portfolio which was less than planned (SGD 6,300). So far I am already SGD 2,640 behind the plan for this year. Things are bound to improve though, especially the outlook for bonus in April seems better than expected, as my boss submitted me for an extra bonus for high performance. Needless to say this is welcome, but highly undeserved.

Dividends received

SGD 160.

Hypothetical monthly income

SGD 1,155. Trending upward after a lacklustre Q4 2018.

At what age could I retire if I stopped investing today?

Assuming an annual growth of current portfolio of 6% and inflation at 2% per year I could retire at the age of 69. Huge improvement from the last time I calculated it. German official retirement age is 67 so in a few months I should have officially “front loaded” my German retirement

Outlook

I have to spend less money in March. Expenses have to go down, saving rate has to go up!

- 20 days no alcohol: failed: 15 days

- 12 times sports: achieved: 13 times

I went on a big vacation and it was too tempting to sometimes have wine and beer. Not good!

February

Another brutal month in terms of expenses. I spent two weeks in South Africa which was probably one of the best experiences I ever had. All spending during this time (rental car, meals, restaurants) was combined into the “travel” category. My wife also paid for some things, but this table only shows my expenses, as we keep separate accounts.

Already now the expense tracking is proving eye opening. I am looking at this table and can’t believe these amounts. Now that a lot of the trips for the first half of 2019 are booked and paid I hope for some lower travel spending. I need to come up with a strategy to get the costs down.

I am doing ERE on easy mode with rent being paid for by the company - it is embarrassing to see this table.

ERE Scorecard

Saving rate in February was 51%. Better than in January, but still not good. The reason for this was the exorbitant travel spending during my trip in South Africa. I am basically on ERE easy mode with housing paid for by the company, yet I am spending too much money.

Portfolio update

Portfolio increased by SGD 11,185 to SGD 346,439 (USD 256,000). Fresh investments of SGD 5,622 and gains of SGD 5,563 contributed. The market is so optimistics this year - no idea what is going on!

Investments vs. plan

I invested SGD 5,622 into my portfolio which was less than planned (SGD 6,300). So far I am already SGD 2,640 behind the plan for this year. Things are bound to improve though, especially the outlook for bonus in April seems better than expected, as my boss submitted me for an extra bonus for high performance. Needless to say this is welcome, but highly undeserved.

Dividends received

SGD 160.

Hypothetical monthly income

SGD 1,155. Trending upward after a lacklustre Q4 2018.

At what age could I retire if I stopped investing today?

Assuming an annual growth of current portfolio of 6% and inflation at 2% per year I could retire at the age of 69. Huge improvement from the last time I calculated it. German official retirement age is 67 so in a few months I should have officially “front loaded” my German retirement

Outlook

I have to spend less money in March. Expenses have to go down, saving rate has to go up!

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #45: March 2019

monthly goal review:

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 13 times

The figures improved. I went on a snowboarding trip with friends which was expensive - lift passes and snowboard courses cost a ton, but DW loved it. Could stay for free at my friend's place which eliminated a lot of potential costs.

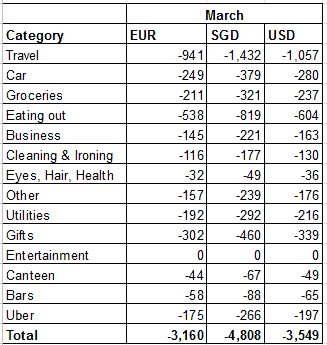

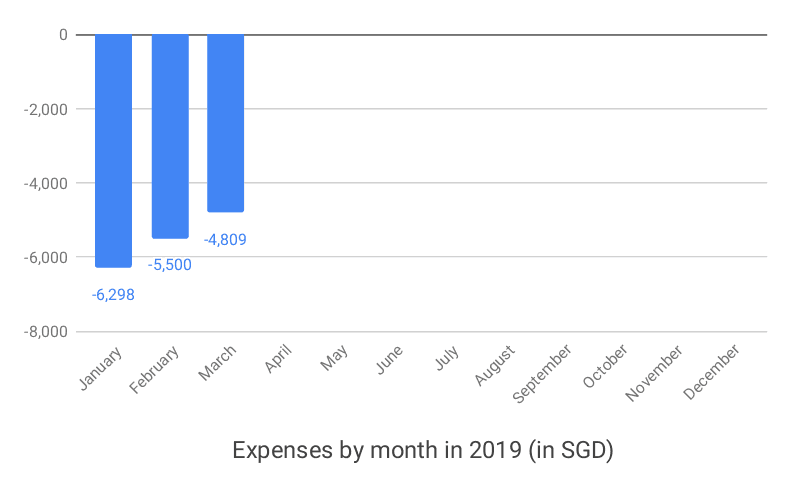

March expenses

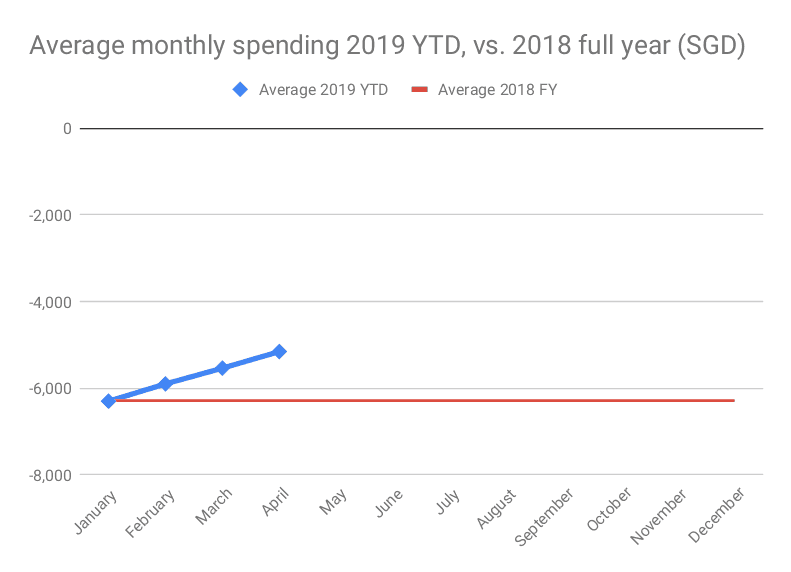

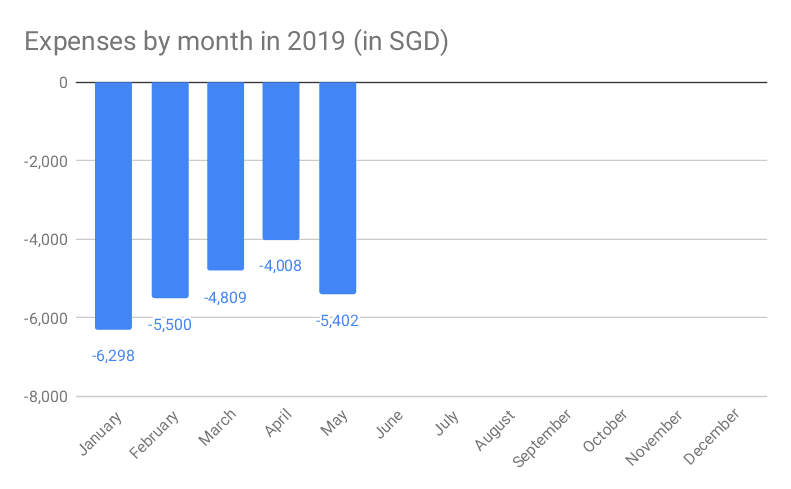

Still spending too much money. Last year's average spending was SGD 6,284 per month, so I am making improvements - but too few and too slowly.

This year's average monthly spending for the first quarter: SGD 5,536.

ERE Scorecard

Saving rate in March: 54%. Things will be better in April, as I will invest my complete bonus.

Portfolio update

Portfolio increased by SGD 9,234 to SGD 355,673 (USD 262,500). Fresh investments of SGD 5,815 and gains of SGD 3,419 contributed.

Investments vs. plan

I invested SGD 5,815 into my portfolio which was less than planned (SGD 6,200). Things will improve in April, but right now I am having a hard time because of exchange rate and uncontrolled spending..

Dividends received

SGD 19.

Hypothetical monthly income

SGD 1,186. Slowly increasing.

Outlook

April will mark the last holiday then I will be on a travel hiatus, doing only short weekend trips by car. I will save my vacation days for the depressive and cold days of November and December. My European home country is so beautiful from May-October that we will focus on exploring the great spots in our backyard during this time.

Own company had a sudden boost of activity in March with a lot of enquiries from potential customers. Hopefully soon I can close the first customer, that would be nice So far the company has been only cost.

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 13 times

The figures improved. I went on a snowboarding trip with friends which was expensive - lift passes and snowboard courses cost a ton, but DW loved it. Could stay for free at my friend's place which eliminated a lot of potential costs.

March expenses

Still spending too much money. Last year's average spending was SGD 6,284 per month, so I am making improvements - but too few and too slowly.

This year's average monthly spending for the first quarter: SGD 5,536.

ERE Scorecard

Saving rate in March: 54%. Things will be better in April, as I will invest my complete bonus.

Portfolio update

Portfolio increased by SGD 9,234 to SGD 355,673 (USD 262,500). Fresh investments of SGD 5,815 and gains of SGD 3,419 contributed.

Investments vs. plan

I invested SGD 5,815 into my portfolio which was less than planned (SGD 6,200). Things will improve in April, but right now I am having a hard time because of exchange rate and uncontrolled spending..

Dividends received

SGD 19.

Hypothetical monthly income

SGD 1,186. Slowly increasing.

Outlook

April will mark the last holiday then I will be on a travel hiatus, doing only short weekend trips by car. I will save my vacation days for the depressive and cold days of November and December. My European home country is so beautiful from May-October that we will focus on exploring the great spots in our backyard during this time.

Own company had a sudden boost of activity in March with a lot of enquiries from potential customers. Hopefully soon I can close the first customer, that would be nice

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Re: Singvestor's awakening

Hi Bigato, do you mean the apartment that the company is paying or the meal vouchers? Not easy to account for these. The apartment is quite luxurious for my standards and I would never rent it myself. It is not really income, but some type of benefit in kind.

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #46: April 2019

monthly goal review:

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 15 times

Had visitors, was in Southern France, drank copious amounts of wine… not ideal.

April expense report

I spent SGD 4,008. Way too much of course. These were the categories for April:

Notable points:

Utilities spending is rather high, as I had to pay the yearly water bill. DW showers recreationally and has childhood trauma of her aunt banging the bathroom door asking her for shorter showers. I could try switching to a more efficient shower head, I guess?

Groceries spending is high, since I forgot my company vouchers and realized at the cashier once.

Bought some unnecessary things, including a limited art print for EUR 129, a laser distance meter to measure a house and so on

I contemplated Bigato’s point to include the company meal vouchers in the calculation, but decided to leave them out because of laziness. They make up <2% of compensation and are complicated to account for, since they cannot be converted to cash and are used mainly by my wife who works near the supermarket (we still keep separate accounts). I also will not count my “free” flat which is paid for by the company.

Overall: Quite embarrassed at the spending level.

I fear that Jacob will ban me at some point for my ERE-unworthy behavior

Only sign of hope:

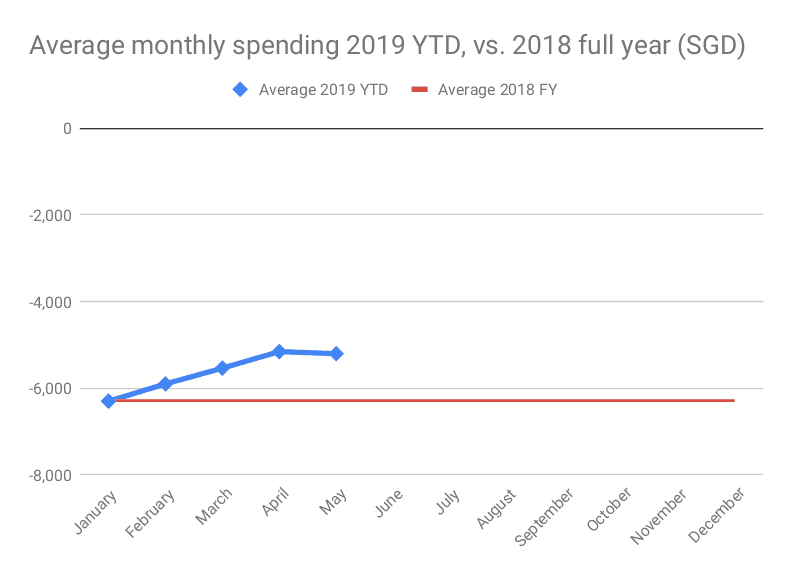

Expense trend is going down slowly:

I hope to maintain this trend and reduce spending of vs. last year:

Why did I not focus on expenses the first 5 years of my ERE journey?!

ERE Scorecard

Saving rate in April was 80%. I did not spend all the rest, but buffered some for future months.

April month is bonus month, where many colleagues just spend a lot of money. In Europe this is far less pronounced than in Singapore - I did not hear any discussions on how to spend the bonus as fast as possible. As always I just invested the whole bonus. I received a 30% on top of the normal bonus, because of so called “outstanding performance”. My performance was average in my opinion, but I appreciate the money. It helped, because the company did poorly and normal bonus was lower than last year.

Portfolio update

Portfolio increased by SGD 42,564 to SGD 398,237 (USD 292,500). Fresh investments of SGD

35,419 and gains of SGD 7,145 contributed.

Investments vs. plan

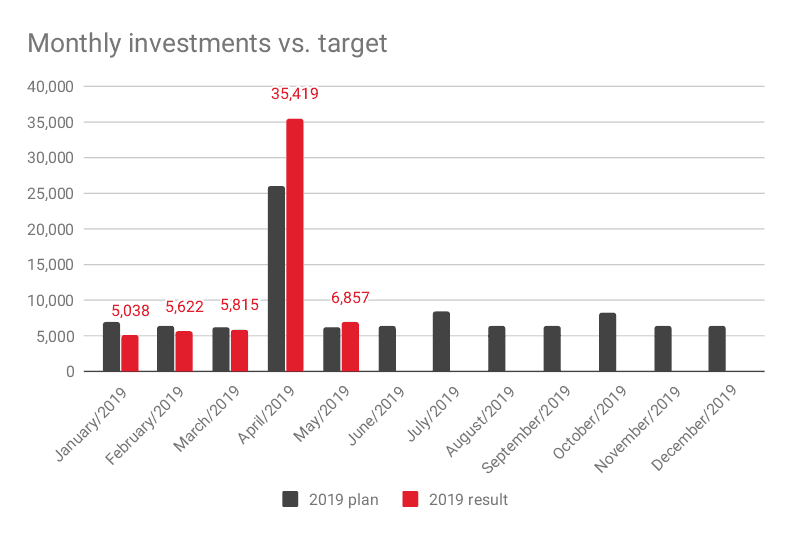

I invested SGD 35,419 into my portfolio which was quite a bit more than planned (SGD 26,000). This helped me catch up with the weak first three months and I am now ahead of my savings plan again.

I am a bit worried about the market valuation and optimism in the last few months. Thus I kept some of my new inflows in cash. Asset allocation is currently as follows:

I am also getting light on bonds, which I cannot tax efficiently buy here, because of the EU regulation on PRIIPs. My Singaporean broker does not allow me to buy ETFs anymore, only single stocks and REITs.

Dividends received

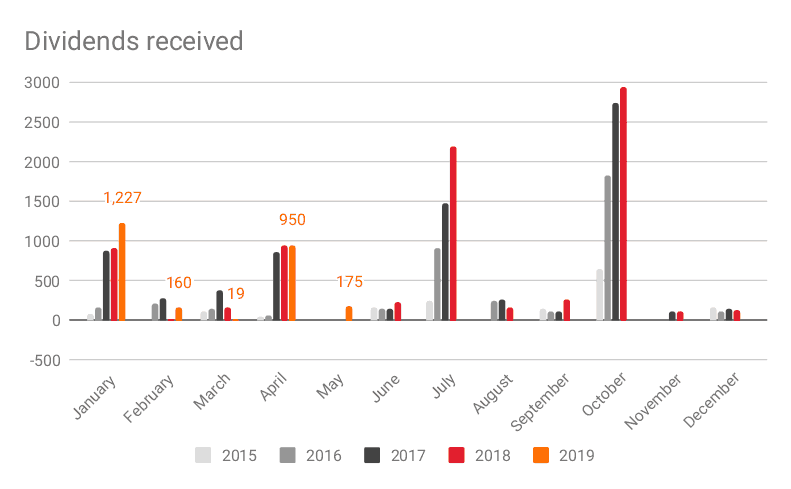

SGD 950.

Hypothetical monthly income

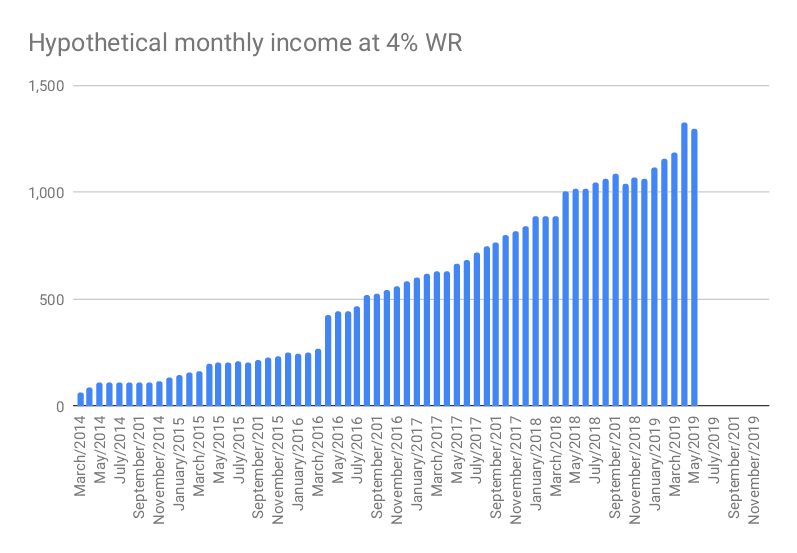

SGD 1,372. Getting closer and closer to the magical EUR 1,000 mark (SGD 1,530)

Early retirement: funding secured!

Assuming an annual growth of current portfolio of 6% and inflation at 2% per year I could retire at the age of 66. German official retirement age is 67 so I have officially paid for my somewhat early retirement Feels like quite a big deal!

Moreover my portfolio would support monthly income of EUR 2,500 in today’s Euros. Someone who always paid into the German state-run retirement scheme while working non-stop for 45 years would only receive EUR 1,400 before tax. So my early retirement would be quite cushy.

Outlook

It seems like I got a bit of salary increase - not sure how much, but it seems like about EUR 300 / month or so. Will see in May. Needless to say, lifestyle inflation will be avoided!

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 15 times

Had visitors, was in Southern France, drank copious amounts of wine… not ideal.

April expense report

I spent SGD 4,008. Way too much of course. These were the categories for April:

Notable points:

Utilities spending is rather high, as I had to pay the yearly water bill. DW showers recreationally and has childhood trauma of her aunt banging the bathroom door asking her for shorter showers. I could try switching to a more efficient shower head, I guess?

Groceries spending is high, since I forgot my company vouchers and realized at the cashier once.

Bought some unnecessary things, including a limited art print for EUR 129, a laser distance meter to measure a house and so on

I contemplated Bigato’s point to include the company meal vouchers in the calculation, but decided to leave them out because of laziness. They make up <2% of compensation and are complicated to account for, since they cannot be converted to cash and are used mainly by my wife who works near the supermarket (we still keep separate accounts). I also will not count my “free” flat which is paid for by the company.

Overall: Quite embarrassed at the spending level.

I fear that Jacob will ban me at some point for my ERE-unworthy behavior

Only sign of hope:

Expense trend is going down slowly:

I hope to maintain this trend and reduce spending of vs. last year:

Why did I not focus on expenses the first 5 years of my ERE journey?!

ERE Scorecard

Saving rate in April was 80%. I did not spend all the rest, but buffered some for future months.

April month is bonus month, where many colleagues just spend a lot of money. In Europe this is far less pronounced than in Singapore - I did not hear any discussions on how to spend the bonus as fast as possible. As always I just invested the whole bonus. I received a 30% on top of the normal bonus, because of so called “outstanding performance”. My performance was average in my opinion, but I appreciate the money. It helped, because the company did poorly and normal bonus was lower than last year.

Portfolio update

Portfolio increased by SGD 42,564 to SGD 398,237 (USD 292,500). Fresh investments of SGD

35,419 and gains of SGD 7,145 contributed.

Investments vs. plan

I invested SGD 35,419 into my portfolio which was quite a bit more than planned (SGD 26,000). This helped me catch up with the weak first three months and I am now ahead of my savings plan again.

I am a bit worried about the market valuation and optimism in the last few months. Thus I kept some of my new inflows in cash. Asset allocation is currently as follows:

I am also getting light on bonds, which I cannot tax efficiently buy here, because of the EU regulation on PRIIPs. My Singaporean broker does not allow me to buy ETFs anymore, only single stocks and REITs.

Dividends received

SGD 950.

Hypothetical monthly income

SGD 1,372. Getting closer and closer to the magical EUR 1,000 mark (SGD 1,530)

Early retirement: funding secured!

Assuming an annual growth of current portfolio of 6% and inflation at 2% per year I could retire at the age of 66. German official retirement age is 67 so I have officially paid for my somewhat early retirement

Moreover my portfolio would support monthly income of EUR 2,500 in today’s Euros. Someone who always paid into the German state-run retirement scheme while working non-stop for 45 years would only receive EUR 1,400 before tax. So my early retirement would be quite cushy.

Outlook

It seems like I got a bit of salary increase - not sure how much, but it seems like about EUR 300 / month or so. Will see in May. Needless to say, lifestyle inflation will be avoided!

-

singvestor

- Posts: 207

- Joined: Tue Jul 21, 2015 12:48 am

Monthly update #47: May 2019

monthly goal review:

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 12 times

Would have been easier, but had a bad cold so skipped a week of sports. Was on track to make the alcohol challenge, but spontaneous company event got in the way. Need to budget buffer days.

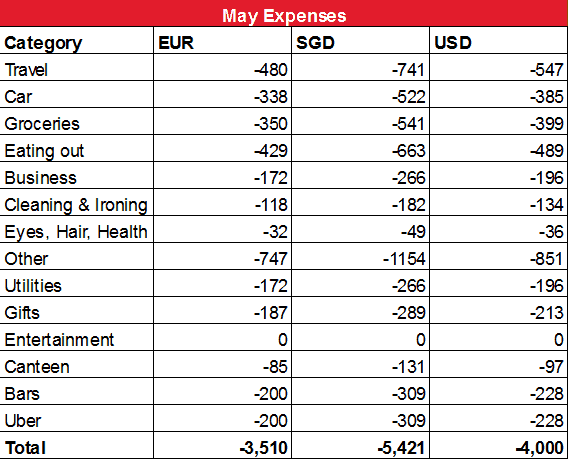

May expense report

Expenses were way too high. I travelled with friends to Spain and Romania, bought unnecessary things, went to expensive restaurants and so on.

I thought about how to implement Bigato’s feedback to count the non-monetary benefits I have been receiving every month:

Lunch vouchers (~EUR 160 / month)

Free apartment (~EUR 1500 / month)

Car loss compensation (part of loss of value due to early selling when I leave

Free language classes for DW and me

Free health insurance

In the end it was too complicated. I get all these from work, but would live in a cheaper apartment or house hack when retired and would get rid of the car. I would also not need to pay for cleaning and ironing.

ERE Scorecard

Saving rate in May was 58%.

Portfolio update

Portfolio decreased by SGD 9,159 to SGD 389,078 (~USD 284,000). Fresh investments of SGD

6,857 were offset by a large paper loss of SGD 16,016.

Investments vs. plan

I invested SGD 6,857 into my portfolio which was quite a lot more than planned (SGD 6,200).

Dividends received

SGD 175.

Hypothetical monthly income

SGD 1,297.

Outlook

June is proving to be very challenging, as I have some really tough situation to sort out in my private life. 99 Problems, but retirement ain’t one at the moment. Also my new job in the company is being negotiated. I turned down a very good offer in another country for a chance at an even better job which might not materialize - tricky situation.

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 12 times

Would have been easier, but had a bad cold so skipped a week of sports. Was on track to make the alcohol challenge, but spontaneous company event got in the way. Need to budget buffer days.

May expense report

Expenses were way too high. I travelled with friends to Spain and Romania, bought unnecessary things, went to expensive restaurants and so on.

I thought about how to implement Bigato’s feedback to count the non-monetary benefits I have been receiving every month:

Lunch vouchers (~EUR 160 / month)

Free apartment (~EUR 1500 / month)

Car loss compensation (part of loss of value due to early selling when I leave

Free language classes for DW and me

Free health insurance

In the end it was too complicated. I get all these from work, but would live in a cheaper apartment or house hack when retired and would get rid of the car. I would also not need to pay for cleaning and ironing.

ERE Scorecard

Saving rate in May was 58%.

Portfolio update

Portfolio decreased by SGD 9,159 to SGD 389,078 (~USD 284,000). Fresh investments of SGD

6,857 were offset by a large paper loss of SGD 16,016.

Investments vs. plan

I invested SGD 6,857 into my portfolio which was quite a lot more than planned (SGD 6,200).

Dividends received

SGD 175.

Hypothetical monthly income

SGD 1,297.

Outlook

June is proving to be very challenging, as I have some really tough situation to sort out in my private life. 99 Problems, but retirement ain’t one at the moment. Also my new job in the company is being negotiated. I turned down a very good offer in another country for a chance at an even better job which might not materialize - tricky situation.