Median annual household income where the head of household has a college degree is more like $90k+. Note that this would include many households with only one or even zero earners. Married filing jointly households have similarly high earnings on average. I couldn't easily find data on two income earners, both with college degrees, but the median must be over $100k. With a typical taxes and a healthy 401k contribution, the couple might net $85k. With these high incomes, half of all of these people/couples which are the typical FIRE audience could still spend around $30k+ and achieve FI in a decade or less.

Imagine if half of all married couples and/or college educated people FIREd within 10 years or less! I'm sure we're far from "critical mass" but we may be near the limits of culture/popularity.

The $40k average number is still accurate for all people under age 35, however that includes all young people earning hardly anything in summer / minimum wage jobs who will be earning a lot more in the future.

FIRE reaching Critical Mass

Re: FIRE reaching Critical Mass

In my experience the rent/own math works dramatically different depending on location.

There was no logical way I could make the purchase of a condo unit in Manhattan work, unless I started banking on huge appreciation, for example.

I believe we are now in a similar situation in other big cities I looked into (Milan, HK), with cost of purchase being often well above 30 years of rent minus expenses.

But IIRC in Chicago buying makes much more sense than renting (assuming one plans to stay there).

So I would guess it depends?

-

jacob

- Site Admin

- Posts: 17143

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: FIRE reaching Critical Mass

Your numbers are a bit low wrt the averages and median but fair enough. It's not that many years ago (great recession) when they were representative.

Also, we certainly can not always assume that anyone can do better than the median

If we look at percentiles .. https://dqydj.com/united-states-househo ... rcentiles/ then 35% of households made less than $40,000 in 2017. Unless we are willing to leave 1/3 of the population behind, I don't want to just ignore their concerns or suggest that they just need to try harder and take a programming class.

Example: A couple where one is an adjunct professor in English teaching 3-4 different classes making $25k/year and the other non-academic is holding two part time jobs at $8k each (no benefits)---a fairly common job situation in this booming economy of ours.

First, there are taxes (they should not be ignored when talking median and average incomes). I used https://smartasset.com/taxes/income-taxes for a married couple earning 40k in my county(*). They now have 33.5k left. Rent around here is in the $800-900 but there are many places in the country (farther away from the big city) where you can find a 1bd/1ba apartment (or even a dilapidated house if you prefer) for $500-600/month. A couple with a small child (or a very well-trained teenager) can certainly squeeze into that. Lets split the difference so 12 months of rent costs 6.5k.

(*) The majority here are FICA and state taxes. Federal can be reduced by a few hundred bucks (we're in the 15% bracket) by opening an IRA. If you're only making 40k for the family, chances are reasonably high that you ARE NOT going to have access to a 401k or similar, but anyone with earned income can open and max out an IRA.

You now have 27k left per year to spend or save on the rest with your housing and taxes taken care of.

If you spend 27k, you'll save nothing. FIRE will never happen. You can look at fig 7.3 (IIRC, the last figure) in the ERE book or you can use this

https://networthify.com/calculator/earl ... awalRate=4

To compare budgets, I would need to rip everything out of my budget that is currently spent on housing in order to bring me into the same position as someone whose rent is already paid. Those rent prices would typically also include free heat, waste, and water, but you would probably pay for gas and electric. If I do that to my/our budget, we spend $9000/year on everything else (food, car, clothes, dog, meds, internet, stuff).

ERE could thus FIRE in 10.2 years because our savings rate is then 66%

https://networthify.com/calculator/earl ... awalRate=4

All I could find was MMM's 2016 budget http://www.mrmoneymustache.com/2017/05/ ... -spending/ ... Like my current situation he has a fully owned house and therefore does not pay rent or mortgage which is consequently not included it the budget! I'll rip all the housing costs out and put some frugal gas and electric back in as well to get the MMM HQ spending ex housing "as if they were living in the 1bd/1ba apartment above". I get about $5000 in house-related costs. (MMM spends 60% less on RE tax than we do.) I'll also subtract the broken arm ($3807) and use the 2015 number for health insurance ... which gives MMM a running budget of $17500/year, roughly twice that of ERE.

MMM would therefore have a savings rate of 36% and could thus FIRE in 24 years

https://networthify.com/calculator/earl ... awalRate=4

Obviously there's a difference in years but both 10 years and 24 years would qualify for FIREing in ones 30s or 40s if either budget plan was adopted.

The average family has a savings rate of maybe 6% (lets say they follow the standard advice of "meeting the match") so they would FIRE in 62 years at which point they would likely be dead. For this budget, retirement would only happen because their FICA taxes provide social security. Indeed for many Americans, retirement savings are not intended for FIRE but as a supplement to social security.

https://networthify.com/calculator/earl ... awalRate=4

-

jacob

- Site Admin

- Posts: 17143

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: FIRE reaching Critical Mass

ARGH, doh! I just realized the calculations above are wrong. I need to add the 6.5k net housing cost back to both spending and income (after tax) to get the proper savings and FIRE numbers.

Here's the recalculation supposing a married couple makes 40k gross => 33.5k net and lives in housing that costs 6.5k/year:

ERE HQ adjusted budget: spending 9+6.5=15.5k => savings rate is 54%, FIRE in 14.9 years.

MMM HQ adjusted budget: spending 17.5+6.5=24k => savings rate is 28%, FIRE in 29.5 years.

I'd also add http://earlyretirementextreme.com/how-t ... -wage.html

Here's the recalculation supposing a married couple makes 40k gross => 33.5k net and lives in housing that costs 6.5k/year:

ERE HQ adjusted budget: spending 9+6.5=15.5k => savings rate is 54%, FIRE in 14.9 years.

MMM HQ adjusted budget: spending 17.5+6.5=24k => savings rate is 28%, FIRE in 29.5 years.

I'd also add http://earlyretirementextreme.com/how-t ... -wage.html

-

jennypenny

- Posts: 6910

- Joined: Sun Jul 03, 2011 2:20 pm

Re: FIRE reaching Critical Mass

So an MMM-type budget is the same as the standard 30yr work-then-pension/retirement model (or what the standard used to be)?

huh

huh

Re: FIRE reaching Critical Mass

Right, but if you make this choice, you then have to factor in higher commute transportation costs/time. Because much more unlikely to find reasonably otherwise rewarding job such as adjunct faculty member in, for instance, Cement City, MI. This is almost the exact trade-off my ex and I made over 30 years ago.jacob wrote:Rent around here is in the $800-900 but there are many places in the country (farther away from the big city) where you can find a 1bd/1ba apartment (or even a dilapidated house if you prefer) for $500-600/month. A couple with a small child (or a very well-trained teenager) can certainly squeeze into that. Lets split the difference so 12 months of rent costs 6.5k.

Re: FIRE reaching Critical Mass

I wanted to post it before, but my 'Stop Arguing in the Internet"-cat helped me not to do so, but situation got even worse so...

Yep, there is.

This is why I'm behaving like cat in the heat lately on the forum.

<short coughing sound>Obviously there's a difference in years but both 10 years and 24 years

Yep, there is.

So "20 years" as my anwer to my last question wasn't that far fetchedERE HQ adjusted budget: savings rate is 54%, FIRE in 14.9 years.

MMM HQ adjusted budget:savings rate is 28%, FIRE in 29.5 years.

This is why I'm behaving like cat in the heat lately on the forum.

-

jacob

- Site Admin

- Posts: 17143

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: FIRE reaching Critical Mass

@Stahlman - However, it's also important to realize that neither I nor Mr MM would choose our current spending-mix if our gross 2+ person household income was 40k. We're smart enough to know better---however, not all of our readers are and I'll get back to that. The spending-mix (or budget) you see here in both cases are for people who are already FIREd. When my income was 25k (after tax) in grad school, my spending was around/under ~6k leading to a savings rate of 75%+.

Young jacob (approximate numbers): savings rate is 78%, FIRE in 6.2 years

It can certainly be done.

If you have to drag a non-income performing spouse along, which is not unusual---this is why the median household income is not 2x the median single income, then it's typically longer. You're somewhat helped by the fact that some expenses scale. The marginal cost of each extra person in a household drops logarithmically (not linearly => whether you get to divide by the number of humans under your roof is a nontrivial decision and very much and apples and oranges issue).

However at that time I was living in a dorm room, ate my famous lentil soup, and walked everywhere. Read http://earlyretirementextreme.com/how-i ... art-i.html etc. to see how I lived during the early years.

Note that 25k at the time was still near the median so 50% were earning less than me. They would have had to go more hardcore and/or work somewhat longer, like 10 years, to get to FIRE. This is still less than 20 years though. This is why I wrote and posted the minimum wage post. You should really read it!

However, there would be no way to FIRE in 5-10 years while supporting 2+ people (apparently my damn dog(*) costs more than MMM's son in ongoing expenses) while owning a car, eating fancy multi-ingredient meals, or buying stuff; IOW naively copying down our lifestyle while making a sub-median income!

(*) Wait what?! Yeah, you see, we also pay taxes for the school district even if we don't get to enjoy the benefits directly. Our dog eats food made out of the same ingredients we do. A pug actually burns some 800kcal/day so similar to a small child. Crazy as that sounds, dogs are heat engines and caloric burn does not scale linearly with bodymass. And being old he's on a couple of prescription meds for arthritis.

Yeah, you see, we also pay taxes for the school district even if we don't get to enjoy the benefits directly. Our dog eats food made out of the same ingredients we do. A pug actually burns some 800kcal/day so similar to a small child. Crazy as that sounds, dogs are heat engines and caloric burn does not scale linearly with bodymass. And being old he's on a couple of prescription meds for arthritis.

To believe this, one would have to be pretty naive. However, as FIRE has grown it attracts people who are literally that naive figuring that they can just copy the lifestyle of their favorite blogger/author and they too shall be FIRE'd. That's some cargo cult thinking right there which I suppose makes it human and forgivable. Yeah, it's not unusual for people to persist in the belief that as long as they ride a bicycle, eat lentils, switch their cell phone plan, and open an investment account with vanguard (the one that always goes up in the long run) that they too can retire in their thirties... it does not occur to them to do the actual math and figure out their own personal savings rate. And us---authors and bloggers---presume that doing the math is so obvious that we shouldn't have to mention it.

There's a mismatch there. When/if we [bloggers] say that "everybody can do it" there are certain unstated presumptions there. For some, like me, it's the ability to do long division in your head---actually not just the ability to do it but the compulsion to do as you read along. For others, it's the belief that it's easy to preserve a middle-class lifestyle under $10k or break into the supermedian income club.

Readers HAVE TO MAKE AN EFFORT to UNDERSTAND THE PRINCIPLES whenever they want to pursue something that's different from the mainstream. Unfortunately, that's actually asking for quite a high Dreyfus learning level and many can't be bothered.

Young jacob (approximate numbers): savings rate is 78%, FIRE in 6.2 years

It can certainly be done.

If you have to drag a non-income performing spouse along, which is not unusual---this is why the median household income is not 2x the median single income, then it's typically longer. You're somewhat helped by the fact that some expenses scale. The marginal cost of each extra person in a household drops logarithmically (not linearly => whether you get to divide by the number of humans under your roof is a nontrivial decision and very much and apples and oranges issue).

However at that time I was living in a dorm room, ate my famous lentil soup, and walked everywhere. Read http://earlyretirementextreme.com/how-i ... art-i.html etc. to see how I lived during the early years.

Note that 25k at the time was still near the median so 50% were earning less than me. They would have had to go more hardcore and/or work somewhat longer, like 10 years, to get to FIRE. This is still less than 20 years though. This is why I wrote and posted the minimum wage post. You should really read it!

However, there would be no way to FIRE in 5-10 years while supporting 2+ people (apparently my damn dog(*) costs more than MMM's son in ongoing expenses) while owning a car, eating fancy multi-ingredient meals, or buying stuff; IOW naively copying down our lifestyle while making a sub-median income!

(*) Wait what?!

To believe this, one would have to be pretty naive. However, as FIRE has grown it attracts people who are literally that naive figuring that they can just copy the lifestyle of their favorite blogger/author and they too shall be FIRE'd. That's some cargo cult thinking right there which I suppose makes it human and forgivable. Yeah, it's not unusual for people to persist in the belief that as long as they ride a bicycle, eat lentils, switch their cell phone plan, and open an investment account with vanguard (the one that always goes up in the long run) that they too can retire in their thirties... it does not occur to them to do the actual math and figure out their own personal savings rate. And us---authors and bloggers---presume that doing the math is so obvious that we shouldn't have to mention it.

There's a mismatch there. When/if we [bloggers] say that "everybody can do it" there are certain unstated presumptions there. For some, like me, it's the ability to do long division in your head---actually not just the ability to do it but the compulsion to do as you read along. For others, it's the belief that it's easy to preserve a middle-class lifestyle under $10k or break into the supermedian income club.

Readers HAVE TO MAKE AN EFFORT to UNDERSTAND THE PRINCIPLES whenever they want to pursue something that's different from the mainstream. Unfortunately, that's actually asking for quite a high Dreyfus learning level and many can't be bothered.

Re: FIRE reaching Critical Mass

Thanks for elaborated answers.

-

jacob

- Site Admin

- Posts: 17143

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: FIRE reaching Critical Mass

As an example of considering the spending mix, in 2004, after having graduated and upgraded my domicile from a dorm room (sharing kitchen and toilets with 18 other smelly students) to a studio(*) about 15 minutes of walking from my work office ... and then six months later to a "cute house" with DW (GF back then) renting for $600/month(**) while being about 25 minutes of walking away; ...

(*) Because now I was making $40k/year as a postdoc and therefore clearly deserved having my own kitchen and bathroom

(**) Cheaper than a studio + grad school residences.

I spent a long time trying to decide whether to spend $35 for a used bicycle to shave off 10 minutes from my commute. Was it worth it? I figured I would need to buy a bicycle pump too. Actually, I think DW/GF bought one but I forget why. I don't recall her having a bicycle?!? Maybe I'm wrong. In any case, a lot of considerations went into that $35 purchase.

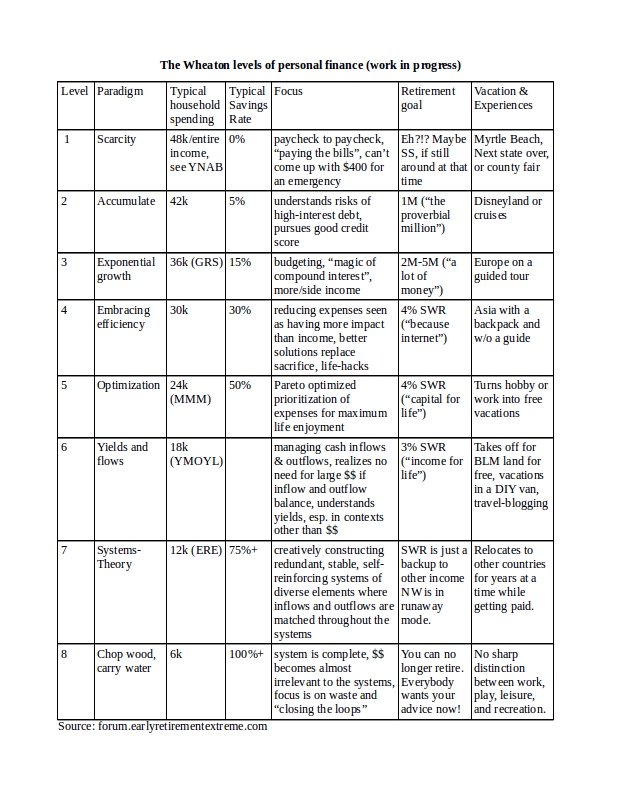

At that point in time I was at ERE Wheaton level 4.

Today I wouldn't think twice about it.

However, ERE neophytes who want to walk in my [improved] footsteps should definitely still be thinking about such things. I can afford not to because I've internalized the decision. Someone who buys a bicycle simply because I own 2 (and I never ride them) is not "getting it".

(*) Because now I was making $40k/year as a postdoc and therefore clearly deserved having my own kitchen and bathroom

(**) Cheaper than a studio + grad school residences.

I spent a long time trying to decide whether to spend $35 for a used bicycle to shave off 10 minutes from my commute. Was it worth it? I figured I would need to buy a bicycle pump too. Actually, I think DW/GF bought one but I forget why. I don't recall her having a bicycle?!? Maybe I'm wrong. In any case, a lot of considerations went into that $35 purchase.

At that point in time I was at ERE Wheaton level 4.

{kind=link}

Today I wouldn't think twice about it.

However, ERE neophytes who want to walk in my [improved] footsteps should definitely still be thinking about such things. I can afford not to because I've internalized the decision. Someone who buys a bicycle simply because I own 2 (and I never ride them) is not "getting it".

-

ThisDinosaur

- Posts: 997

- Joined: Fri Jul 17, 2015 9:31 am

Re: FIRE reaching Critical Mass

So, the expanding FIRE movement is really about wealth inequality. One segment of the population is making 3-5× more than they 'need' and bragging about how easy it is to be Frugal. While a larger fraction have no career prospects and may live with their parents indefinitely.

The standard FIRE blog message will read like salt in the wounds for Boomerang kids. Just like ERE will look like self flagellation to anyone who can afford an indefinite suburban lifestyle after "only" 10 years of work.

All advice should be context specific. The solutions for MMM's audience of engineers is necessarily different than advice to minimum wage Boomerangers. Your concern here only makes sense because I know you use "early retirement" as a fake out to push anti consumerism. Whereas the larger FIRE movement uses anticonsumerism as a means to escape alarm clocks and middle management.jacob wrote: ↑Sun Oct 07, 2018 8:35 amIf we look at percentiles .. https://dqydj.com/united-states-househo ... rcentiles/ then 35% of households made less than $40,000 in 2017. Unless we are willing to leave 1/3 of the population behind, I don't want to just ignore their concerns or suggest that they just need to try harder and take a programming class.

-

jacob

- Site Admin

- Posts: 17143

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: FIRE reaching Critical Mass

Just for fun, I reran the calculations for someone earning at the 66% percentile. (See links above for numbers). That's $85,100 gross and $67.5k net.

ERE HQ adjusted budget: earning 67.5knet and spending 9+6.5=15.5k => savings rate is 78%, FIRE in 6.8 years.

MMM HQ adjusted budget: earning 67.5knet and spending 17.5+6.5=24k => savings rate is 64%, FIRE in 10.9 years.

It's clear that insofar one naively clones the frameworks, then there's a significant difference between between in the top 1/3 of household incomes and the bottom 1/3. And whereas the difference between ERE and MMM is relatively small in absolute years at the high income levels, it's materially different at low income levels.

The top---guesstimating---70-75% income percentile or better is actually quite representative of the numbers (5 years, 10 years, before you're 40) usually used by the FIRE community.

One can plot this on a graph, which @Fish actually did. Check out the 5 year and 10 year lines.

If you pick the 5 year line, you're following the ERE sales pitch: "You can retire in 5 years". Now, if you're going about it naively (not understanding the principles), then you start on the y-axis and look at your spending level. Let's say it's $15000/year (like it is at ERE HQ with a fully owned house, a car, a dog,... Several of you have seen it in person by now). If you try to replicate my current lifestyle, then you need to be roughly around the 75% income percentile for the math to work (that's $105k gross). If you are willing to work 10 years, then making more than 45% of the people will do ($51k gross). And if you're willing to work 20 years, then you only have to do better than 25% of the population ($29k gross).

Recall these are the gross income for a two-person household.

Note the solid line in the graph. That's what normal consumers actually spend given their income. Note how spending is so high in the US that people will not FIRE in under 50 years until they're in the 55% income percentile. IOW, FIRE is unpossible for more than half of the standard consumer units!!! The 40 years working life line (at which time people can begin to collect SS anyway) is crossed around the 65% income percentile. This means that only 1/3 of Americans can even begin to consider ANY kind of pre-age 67.5 kind of retirement as long as they're typical consumers.

Let's look at MMM in which case you follow the 10 year line since MMM worked for 10 years. Enter on the y-axis at $24000 and you need to be at the 66% percentile income for the math to work (so $85k gross). If you want the MMM spending and FIRE in 5 years, you need to be at the 90% percentile income level. Converting that around, you need to make $170k gross.

PS: If @Fish is reading this and the data is there, it would be interesting to see a graph for singles instead of households.

ERE HQ adjusted budget: earning 67.5knet and spending 9+6.5=15.5k => savings rate is 78%, FIRE in 6.8 years.

MMM HQ adjusted budget: earning 67.5knet and spending 17.5+6.5=24k => savings rate is 64%, FIRE in 10.9 years.

It's clear that insofar one naively clones the frameworks, then there's a significant difference between between in the top 1/3 of household incomes and the bottom 1/3. And whereas the difference between ERE and MMM is relatively small in absolute years at the high income levels, it's materially different at low income levels.

The top---guesstimating---70-75% income percentile or better is actually quite representative of the numbers (5 years, 10 years, before you're 40) usually used by the FIRE community.

One can plot this on a graph, which @Fish actually did. Check out the 5 year and 10 year lines.

If you pick the 5 year line, you're following the ERE sales pitch: "You can retire in 5 years". Now, if you're going about it naively (not understanding the principles), then you start on the y-axis and look at your spending level. Let's say it's $15000/year (like it is at ERE HQ with a fully owned house, a car, a dog,... Several of you have seen it in person by now). If you try to replicate my current lifestyle, then you need to be roughly around the 75% income percentile for the math to work (that's $105k gross). If you are willing to work 10 years, then making more than 45% of the people will do ($51k gross). And if you're willing to work 20 years, then you only have to do better than 25% of the population ($29k gross).

Recall these are the gross income for a two-person household.

Note the solid line in the graph. That's what normal consumers actually spend given their income. Note how spending is so high in the US that people will not FIRE in under 50 years until they're in the 55% income percentile. IOW, FIRE is unpossible for more than half of the standard consumer units!!! The 40 years working life line (at which time people can begin to collect SS anyway) is crossed around the 65% income percentile. This means that only 1/3 of Americans can even begin to consider ANY kind of pre-age 67.5 kind of retirement as long as they're typical consumers.

Let's look at MMM in which case you follow the 10 year line since MMM worked for 10 years. Enter on the y-axis at $24000 and you need to be at the 66% percentile income for the math to work (so $85k gross). If you want the MMM spending and FIRE in 5 years, you need to be at the 90% percentile income level. Converting that around, you need to make $170k gross.

PS: If @Fish is reading this and the data is there, it would be interesting to see a graph for singles instead of households.

-

jacob

- Site Admin

- Posts: 17143

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: FIRE reaching Critical Mass

@ThisDinosaur - Exactly!

PS: Nice observation wrt anticonsumerism. To me (and I think to MMM too) it's an end(*). But for many in the FIRE community it's a means. One can tell the difference between the two sentiments by whether not buying something is thought of as a sacrifice or an achievement.

(*) That whole "save the world" drive which we have in common although we go about it from two very different directions which can aptly be summarized as optimism vs pessimism.

PS: Nice observation wrt anticonsumerism. To me (and I think to MMM too) it's an end(*). But for many in the FIRE community it's a means. One can tell the difference between the two sentiments by whether not buying something is thought of as a sacrifice or an achievement.

(*) That whole "save the world" drive which we have in common although we go about it from two very different directions which can aptly be summarized as optimism vs pessimism.

Re: FIRE reaching Critical Mass

As I practise my assertiveness skills :

1. If we speak about simple math like: 1 [month unit] / (percent of salary I've survived on last month or somekind average of longer period)= months I don't need work, well... it comes pretty naturally, pretty fast for somebody with 2 digits IQ (I hope I'm there ).

).

2. As with everything, matchings such equations with surrouding reality - this is the most difficult part.

Didn't you have an idea to buy 100x chewing gum in primary school canteen with your parent's allowance if only 1 gum costed 1 cent? 8)

3. In my orginal post (viewtopic.php?p=175561#p175561)

I simply tried to mock the possibilty that FIRE will become much more popular, because... for most people it will be difficult to save enough (or in "early" fashion) based on their mix of social pressure, earnings, skills or other stuff mentioned in different topics.

1. If we speak about simple math like: 1 [month unit] / (percent of salary I've survived on last month or somekind average of longer period)= months I don't need work, well... it comes pretty naturally, pretty fast for somebody with 2 digits IQ (I hope I'm there

2. As with everything, matchings such equations with surrouding reality - this is the most difficult part.

Didn't you have an idea to buy 100x chewing gum in primary school canteen with your parent's allowance if only 1 gum costed 1 cent? 8)

3. In my orginal post (viewtopic.php?p=175561#p175561)

I simply tried to mock the possibilty that FIRE will become much more popular, because... for most people it will be difficult to save enough (or in "early" fashion) based on their mix of social pressure, earnings, skills or other stuff mentioned in different topics.

-

jacob

- Site Admin

- Posts: 17143

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: FIRE reaching Critical Mass

@Stahlmann - Poe's Law suggests one must exercise care when mocking.

My concern is that the FIRE community can easily come to be seen as overpromising and underdelivering when seen outside its own subculture, vis-a-vis what @ThisDinosaur said

... which is unfortunately a real phenomenon and some don't even know it. When it comes to income and lifestyle (<= how one spends money) humans live in bubbles. There's certainly a material segment of the FIRE community which can be described as "having a high income while having proudly discovered how to spend and live like regular people". A certain modesty/humility/gratefulness might be optimal in those cases, but that is not what is observed.

Some of the optics are positively bad even if it's quite unintentional and isn't at all mean-spirited. Therein lies the problem of going wide or getting popular.

I do understand that such insight/self-awareness easily gets lost in all the excitement of discovering a new thing. I'm guilty of the same thing. I was occasionally accused of being a poverty tourist back in the days when I talked about how easy it was to live well below the poverty level. That was before I realized how many non-monetary resources/capital I had at my disposal which do not exist among the poor.

Same thing now with some of the high-income crowd who think they're kings of frugality because they've discovered shopping at Costco, painting their own walls, buying stuff at Goodwill, and driving older cars instead of new ones while not realizing that this is normality in the US middle class.

My concern is that the FIRE community can easily come to be seen as overpromising and underdelivering when seen outside its own subculture, vis-a-vis what @ThisDinosaur said

($) The complete definition of a savings rate between 75% and 83%ThisDinosaur wrote: ↑Sun Oct 07, 2018 1:37 pmOne segment of the population is making 3-5× more than they 'need'($) and bragging about how easy it is to be Frugal.

... which is unfortunately a real phenomenon and some don't even know it. When it comes to income and lifestyle (<= how one spends money) humans live in bubbles. There's certainly a material segment of the FIRE community which can be described as "having a high income while having proudly discovered how to spend and live like regular people". A certain modesty/humility/gratefulness might be optimal in those cases, but that is not what is observed.

Some of the optics are positively bad even if it's quite unintentional and isn't at all mean-spirited. Therein lies the problem of going wide or getting popular.

I do understand that such insight/self-awareness easily gets lost in all the excitement of discovering a new thing. I'm guilty of the same thing. I was occasionally accused of being a poverty tourist back in the days when I talked about how easy it was to live well below the poverty level. That was before I realized how many non-monetary resources/capital I had at my disposal which do not exist among the poor.

Same thing now with some of the high-income crowd who think they're kings of frugality because they've discovered shopping at Costco, painting their own walls, buying stuff at Goodwill, and driving older cars instead of new ones while not realizing that this is normality in the US middle class.

Re: FIRE reaching Critical Mass

@jacob:

Rich people shitting on poor people is how I think FIRE would ultimately be received if it actually got big enough to receive major media attention. I remember reading an article about how minimalism is bullshit because it's only for rich people. I don't really think this is avoidable though, which is why I don't think this movement is going mainstream. I do wish this movement would go mainstream, in it's sincerest form. I also wish there was a prominent FIRE blogger who made significantly under the median income, because this is the demographic who would benefit most from it's message.

I don't blame MMM for being a good salesman. I think he's really trying to promote something he seriously believes in as best he can. Most of his article are about why consumerism is lame and how to escape from the normal way of doing things. I still think this is still the core message of FIRE and ERE. Other people misinterpreting the message by going wide is almost an inevitability, but is it better to just not try?

If you're trying to escape a conventional lifestyle and your plan is to copy what someone else does exactly, do you really deserve to escape?

Rich people shitting on poor people is how I think FIRE would ultimately be received if it actually got big enough to receive major media attention. I remember reading an article about how minimalism is bullshit because it's only for rich people. I don't really think this is avoidable though, which is why I don't think this movement is going mainstream. I do wish this movement would go mainstream, in it's sincerest form. I also wish there was a prominent FIRE blogger who made significantly under the median income, because this is the demographic who would benefit most from it's message.

I don't blame MMM for being a good salesman. I think he's really trying to promote something he seriously believes in as best he can. Most of his article are about why consumerism is lame and how to escape from the normal way of doing things. I still think this is still the core message of FIRE and ERE. Other people misinterpreting the message by going wide is almost an inevitability, but is it better to just not try?

If you're trying to escape a conventional lifestyle and your plan is to copy what someone else does exactly, do you really deserve to escape?

Re: FIRE reaching Critical Mass

If I may attempt to summarize using round numbers with an X multiplier:

- Typical household expenses are X to 2X.

- Average income for young people is 2X. Household income or income for higher skilled people is more like 3-4X.

- (Early) ERE spending is 0.25X and he got there making X.

- MMM spending is X and they got there making 4X.

In terms of income levels, and thoughts one might have when encountering FIRE:

1X (ERE): I don't make enough to pay my bills, let alone FI. I hope Social Security still exists when I'm old.

2X: I make enough to get by, but could only see myself saving 0.1X. I'll be lucky to retire at age 70.

3X: Maybe if I made some major changes I could save X, but I'd really have to downsize everything and it would still take me 25 years to retire. Why bother just to retire in my 50s instead of 60s?

4X (MMM): I landed this boring but high-paying job and have all this extra cashflow automatically from just living reasonably. I guess I can quit the office job in a few years and do something else!

And in terms of (perceived) difficulty in spending habits and career skills:

1X (ERE): You can FIRE at any salary (easy) if you live as optimally as possible (very hard).

2X: Land an average job (average) and optimize spending half of the low end of typical spending (hard).

3X: Get a good solid job requiring a college degree or trade skills (hard), and spend an average amount (average).

4X (MMM): Get a job in one of the most in-demand fields (very hard) and then just live unlike a spendthrift (easy).

Anyone making the average income or below will consider FIRE too difficult. Typical people making more than average may agree it's doable, but will not see the short-term "hardship" being worth the long-term benefit, especially if they think they are only capable of shaving a few years off their career.

- Typical household expenses are X to 2X.

- Average income for young people is 2X. Household income or income for higher skilled people is more like 3-4X.

- (Early) ERE spending is 0.25X and he got there making X.

- MMM spending is X and they got there making 4X.

In terms of income levels, and thoughts one might have when encountering FIRE:

1X (ERE): I don't make enough to pay my bills, let alone FI. I hope Social Security still exists when I'm old.

2X: I make enough to get by, but could only see myself saving 0.1X. I'll be lucky to retire at age 70.

3X: Maybe if I made some major changes I could save X, but I'd really have to downsize everything and it would still take me 25 years to retire. Why bother just to retire in my 50s instead of 60s?

4X (MMM): I landed this boring but high-paying job and have all this extra cashflow automatically from just living reasonably. I guess I can quit the office job in a few years and do something else!

And in terms of (perceived) difficulty in spending habits and career skills:

1X (ERE): You can FIRE at any salary (easy) if you live as optimally as possible (very hard).

2X: Land an average job (average) and optimize spending half of the low end of typical spending (hard).

3X: Get a good solid job requiring a college degree or trade skills (hard), and spend an average amount (average).

4X (MMM): Get a job in one of the most in-demand fields (very hard) and then just live unlike a spendthrift (easy).

Anyone making the average income or below will consider FIRE too difficult. Typical people making more than average may agree it's doable, but will not see the short-term "hardship" being worth the long-term benefit, especially if they think they are only capable of shaving a few years off their career.

-

jennypenny

- Posts: 6910

- Joined: Sun Jul 03, 2011 2:20 pm

Re: FIRE reaching Critical Mass

I hope FIRE bloggers don't discourage people here who don't fall into the super-salary category. I can see where if you don't make that kind of money, and maybe don't have a partner to split the bills with, FI might seem like an unattainable goal.

Looking at FIRE lifestyles built on high incomes is no different than watching professional athletes with exceptional skills or successful musicians with great singing voices. I'm sure they put in a lot of hard work, but they also have a level of talent and training most people don't have -- and even with that they still needed a lot of luck to capitalize on it.

It's ok to admire people like that and learn what you can from them, but try to avoid comparing yourself or your results to theirs. That would be my FI advice -- do your own math, set your own goals, dig deep ... then dig a little deeper ... and avoid patterning your life (before or after FI) on anyone else.

Looking at FIRE lifestyles built on high incomes is no different than watching professional athletes with exceptional skills or successful musicians with great singing voices. I'm sure they put in a lot of hard work, but they also have a level of talent and training most people don't have -- and even with that they still needed a lot of luck to capitalize on it.

It's ok to admire people like that and learn what you can from them, but try to avoid comparing yourself or your results to theirs. That would be my FI advice -- do your own math, set your own goals, dig deep ... then dig a little deeper ... and avoid patterning your life (before or after FI) on anyone else.

-

Laura Ingalls

- Posts: 788

- Joined: Mon Jun 25, 2012 3:13 am

Re: FIRE reaching Critical Mass

@Jacob

Your dog probably does cost more than a human child since at the $25k level a human child would get Medicaid and the refundable portion of the Child Tax Credit. On the other hand teenage boys consider 800 calories a light snack and a pug will never make a compelling case for you buying him an iPhone.

@7w5 thought Cement City was a joke til I looked it up. Do you think it is more prosperous than Oil City?

Your dog probably does cost more than a human child since at the $25k level a human child would get Medicaid and the refundable portion of the Child Tax Credit. On the other hand teenage boys consider 800 calories a light snack and a pug will never make a compelling case for you buying him an iPhone.

@7w5 thought Cement City was a joke til I looked it up. Do you think it is more prosperous than Oil City?

-

SustainableHappiness

- Posts: 266

- Joined: Tue Jun 28, 2016 6:39 pm

Re: FIRE reaching Critical Mass

Ditto on the reason why FIRE won’t go mainstream is because breaking free of modeling your behaviour off of a role model is friggin’ hard. It took me 4 years of reading blogs and trying things out before realizing I’m not MMM, I’m not ERE, and more importantly, I don’t actually want MMM’s or a ERE (modeled by Jacob) life. But they are (were?) my damn role models and there is inherently some envy that goes along with that.

Assuming moving from Copying through Creating (to reference ERE learning steps) takes a number of years in a relatively stress-free environment where an individual (me in this case) is both willing and able to devote time and mental energy to it, is it a reasonable expectation that the Copying->Creating cycle will even happen for a 2 person household making $40k a year? Toss a kid in there and even with higher income, the deep learning would be difficult/impossible without significant amounts of time and effort.

It’s weird, but the way that makes sense to me to break into those minds and push anti-consumerism would be mind-numbing amounts of advertising, like moving from pull marketing tactics (a la blogs) to push marketing tactics (a la “Playing With FIRE” the movie) so people are more likely to follow the tactical aspects and fall into the strategic aspects. And that just sounds f’ed up. I mean, a billboard about the latest FIRE superstar...WTF?

Assuming moving from Copying through Creating (to reference ERE learning steps) takes a number of years in a relatively stress-free environment where an individual (me in this case) is both willing and able to devote time and mental energy to it, is it a reasonable expectation that the Copying->Creating cycle will even happen for a 2 person household making $40k a year? Toss a kid in there and even with higher income, the deep learning would be difficult/impossible without significant amounts of time and effort.

It’s weird, but the way that makes sense to me to break into those minds and push anti-consumerism would be mind-numbing amounts of advertising, like moving from pull marketing tactics (a la blogs) to push marketing tactics (a la “Playing With FIRE” the movie) so people are more likely to follow the tactical aspects and fall into the strategic aspects. And that just sounds f’ed up. I mean, a billboard about the latest FIRE superstar...WTF?