Ok, so the planned update to be posted a few days after end of November turned into about 5 weeks...that makes it a quarterly update.

UPDATE October, November and December

It was October that this journal entered the 2 year mark and, although I still keep track of all finances, we’re moving towards (e)re more or less on auto-pilot. Of course we take certain decisions on purpose and we consider some ideas carefully, but the day to day stuff just goes automatically. Most likely because we simply always have been frugal and it always has felt as a waste to me to spend money on certain things as most people do. We just spend what, in our view, is needed and what we think is worth it. With the (E)RE in mind, we have just optimized it further and gotten more understanding of our goal(s) and how/when we might be able to reach them. As mentioned before, it is like a marathon. Slowly but steady it goes.

January non-financial

I'll leave in a few days for the annual company trip to Hong Kong and planned to meet a ERE forum member in the weekend.

When work is finished, I will spend a few holidays in SE-Asia. Since the company paid the ticket to Hong Kong my cost for these holidays will be very limited. All in all I will be 2 weeks away from home.

I look forward to this, but I also know that at the end of the trip I look forward to go home. Not so much to be "home", but be back with the family and stop traveling.

FINANCIAL HIGHLIGHTS

Calculations

Previously I deducted “kids expenses” with a tax benefit we received for a couple of years. But because that that tax benefit will end now, I decided to change the calculations and treat it as additional income. That way we’re able to compare and check details better. It doesn’t change the amounts we saved, but it did decrease our ttm savings rate with 2%. DW will start working 15% more as of January, so the end of the tax benefit will likely be offset with the higher income and it will likely not affect our future savings rate.

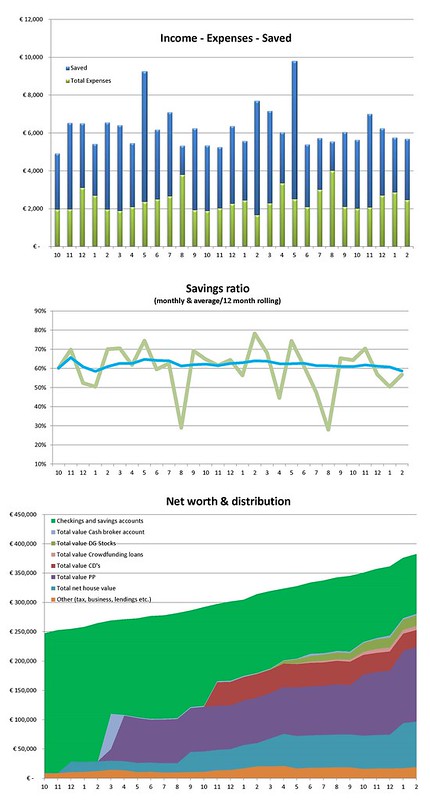

Mortgage

We have paid off another 10% of our mortgage January 1st, yeah! I also checked what the penalty would be if we would pay off the remaining mortgage all at once, but it was way too much to make it worthwhile. So we just will pay 10% each year for now.

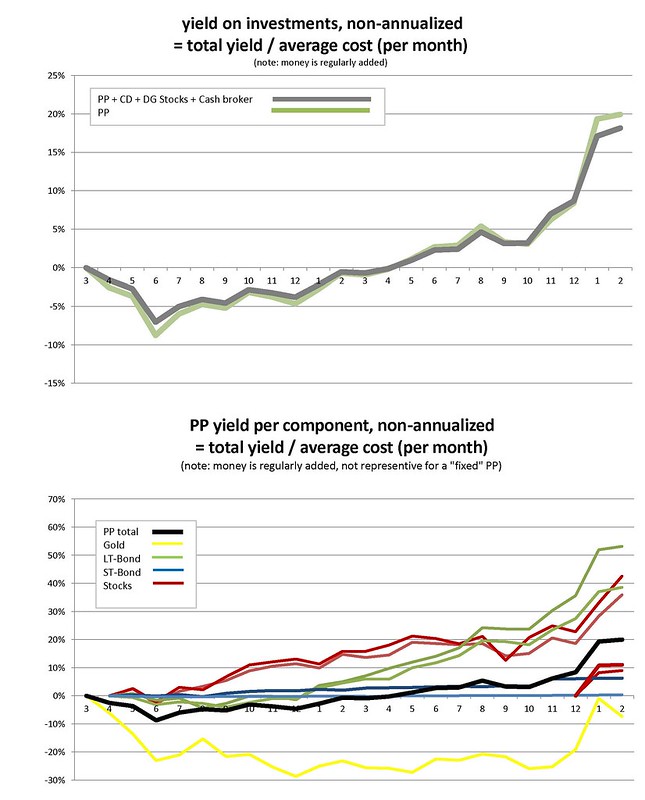

Permanent Portfolio and other investments

I moved 20K from some savings to the Permanent Portfolio and also bought for about 5K individual stocks as part of a separate (small) Dividend Growth Portfolio. Not sure if I will continue with that though, too complex for me and I do not think that (at this moment) I do have enough knowledge (and time) to beat a broad index fund.

As of January I am planning to put investments for the Permanent Portfolio more on semi-autopilot, every month the same amount at the same time. This should help me to prevent the monthly savings pile up and actually to decrease the amount in savings and checking accounts.

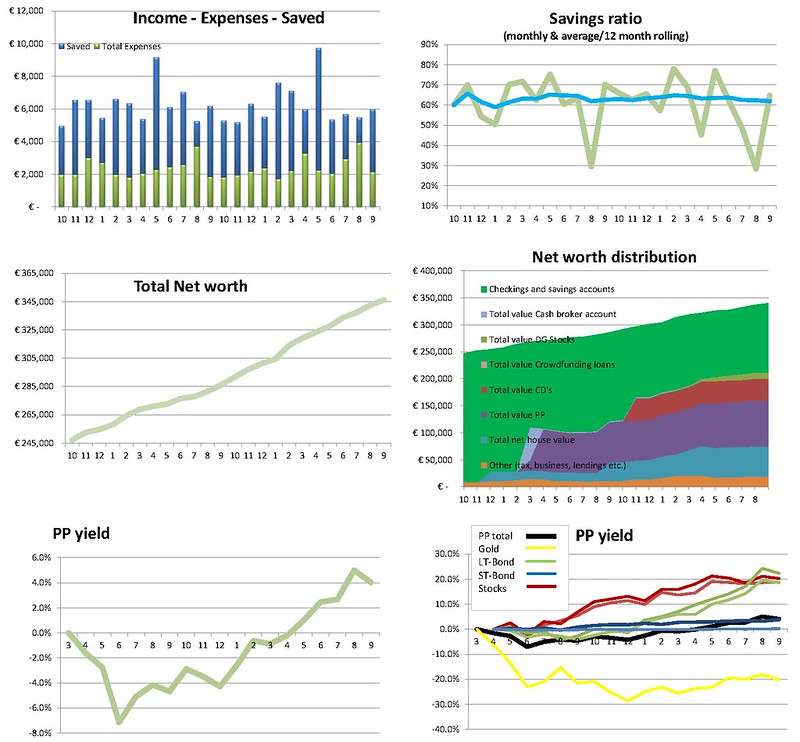

Expenses – income – savings ratio

Expenses October 2094

Expenses November 1949

Expenses December 2708

Income October 5659 (5518 regular income, 141 dividends)

Income November 7024 (5516 regular income, 1240 interest, 205 dividends, 63 sales)

Income December 6264 (5694 regular income, 418 interest, 87 dividends, 65 sales)

Savings ratio 63%, 72% and 57% (ttm 61%)

Special expenses

Per previous post, we bought plane tickets for the next summer holiday. Costs was almost 2700, more than our average month expenditure….I have included 10% of this in the November and December expenses and will do this for the next 8 months coming.

Furthermore we bought a tablet and some clothing in December and had some more expenses then usual on gifts. Also we donated some charity and had a once a year insurance costs. Expenses seems to be creeping up now and then, but I am still satisfied and just keep an eye on it.

Income

Income from regular work is very steady. Annually Interest in November was from our CD’s, these will run for another 4 years.

Net worth

Net worth went from 345K in September to 357K in November, despite having paid almost 3K for the plane tickets. The market “gave” us almost 5K extra compared to the normal month on month increase. And in December our net worth rose another 4K despite spending more then usual.

We ended the year at 361K. We're happy with that.

Coming months financial

From January on our income will change a bit (wife works a bit more, changes in tax/pension, benefit) and a little in expenses (paid off 10% of the mortgage). But it will probably take a few months before the exact changes are clear.

I Expect around February a (for me) considerable bonus due to a good result of the company. And I hope also to get a small annual raise around then.

If there are no major changes in the Market I expect we should go over 370K in Feb. From that point I might be focusing more on our Net Worth excluding our house which should be then around 200K.

Graphics

Graphics follow soon (I will really try...

)