a planter's garden

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:23 pm, edited 2 times in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:23 pm, edited 2 times in total.

-

jacob

- Site Admin

- Posts: 15995

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: a planter's garden

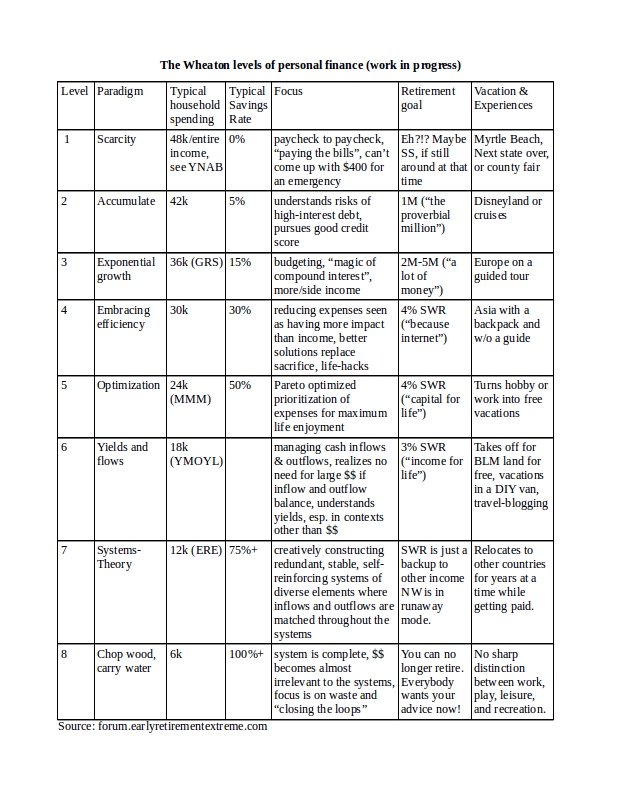

You're confusing ERE with E-ER from standard one-dimensional FIRE. The problem of retiring in 2020 with a consumerist mindset under the 4% rule does exist---indeed it's hard to swing a dead cat in the FIRE movement w/o hitting one of those optimists---but I believe it's rare here.

I believe the danger-zone is found at level 4, that is, people who have learned enough to know about the 4% rule but not enough to know about its limitations. Ditto life in general, that is, enough to life-hack and geo-arbitrage a consumer lifestyle, but again not enough to realize the limits of that as they get older/life happens.

Reminder:

I believe the danger-zone is found at level 4, that is, people who have learned enough to know about the 4% rule but not enough to know about its limitations. Ditto life in general, that is, enough to life-hack and geo-arbitrage a consumer lifestyle, but again not enough to realize the limits of that as they get older/life happens.

Reminder:

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:23 pm, edited 1 time in total.

-

RockyMtnLiving

- Posts: 47

- Joined: Fri May 08, 2020 8:49 am

Re: a planter's garden

For an interesting analysis of SS for early retirees, see https://thefinancebuff.com/early-retire ... efits.html. Apologies if the same or similar analysis is posted here somewhere.plantingtheseed wrote: ↑Sat Jun 27, 2020 2:17 pm

-Continue to maximize social security credits.

This is a rather imporant point. The way social security is calculated, it takes the highest 35 years in income to calculate the benefits. In any missing years, '0' is entered. Not necessarily advocating working 35 years, but this is a relevant information.

https://www.ssa.gov/pubs/EN-05-10070-1956.pdf

The bend points are interesting. This is too flippant of a generalization, but at some point -- actually, when you reach the second bend point -- exiting the work force doesn't have a significant impact on future benefits.

I think the greater risk for younger folks -- e.g., those 30 or younger, say -- is that the SS rules may change in the decades ahead, given the financial situation of the trust fund and recent societal financial stresses (2008/9 and the ongoing pandemic). I expect (read: "hope") that older folks -- e.g., those 50 and older when the changes are made -- will be grandfathered in such a scenario. I could be wrong, of course. And depending too much on programs such as SS is always risky, I suppose.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:24 pm, edited 1 time in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:24 pm, edited 1 time in total.

-

jacob

- Site Admin

- Posts: 15995

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: a planter's garden

SS is one of those systems where massive outflows are finely balanced with massive inflows so a small change on the dial has big consequences to the behavior of the system. A small percentage in taxing will change it but a significant fraction of politicians will howl about that as they actively working to get rid of SS entirely.plantingtheseed wrote: ↑Sat Jun 27, 2020 9:55 pmPBS documentary "When I'm 65" talks about the SS problem (See: 35m12s - 40m30s) https://www.pbs.org/video/dptv-document ... m-65-full/ and shows SS could easily be fixed, for example by raising FICA from 7.5% to 9%, it can go for another 75 years.

Other countries have mostly taken the road of slowly increasing the retirement age so as to make less people collect/people collect less before they die. For example, my Danish nephew will not be able to collect before he is 72. In the US this would probably be considered highly unfair given the wide span in life expectancy between different counties with some of the richest pushing ~86 years and some of the poorest at ~66 years.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:24 pm, edited 1 time in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:24 pm, edited 1 time in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:25 pm, edited 1 time in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 10:52 am, edited 1 time in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:24 pm, edited 2 times in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:24 pm, edited 2 times in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:24 pm, edited 2 times in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:25 pm, edited 2 times in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:25 pm, edited 2 times in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 10:57 am, edited 1 time in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

..

Last edited by plantingtheseed on Thu Feb 18, 2021 4:25 pm, edited 1 time in total.

-

plantingtheseed

- Posts: 202

- Joined: Sat Mar 28, 2020 7:23 pm

Re: a planter's garden

A good reminder - Just looking at the price is not investing (0:00 to 10:10)

https://www.youtube.com/watch?v=Qm0jktMIYlk

https://www.youtube.com/watch?v=Qm0jktMIYlk