Re: C40's Journal

Posted: Thu Nov 14, 2013 10:27 pm

double post...

---post-consumerist resilience for the 21st century

https://forum.earlyretirementextreme.com/

https://forum.earlyretirementextreme.com/viewtopic.php?t=1344

Interesting thoughts. I hadn't really been thinking this way. I replied in the thread below. (it's more directly relevant there and will get more views/discussion)ebast wrote: I wonder if there aren't surrogates that feel like you're going out for dinner but don't cost 90 bucks along the way.. like you mentioned museums -- you go to the a museum or gallery for an opening, everybody's dressed up, maybe there'll be wine and cheese, music.. does that feel more like a date? If you see something live instead of a movie, is that somehow date-ier? (asking a girl out for a Spotify date - good luck with that) I dunno.. more things to figure out..

It's scary how often this gets mentioned on this forum. I'm starting to get this too, as people are beginning to realise it's not just a phase:)The only thing that really causes friction is some cases of people close to me expecting me to spend more.

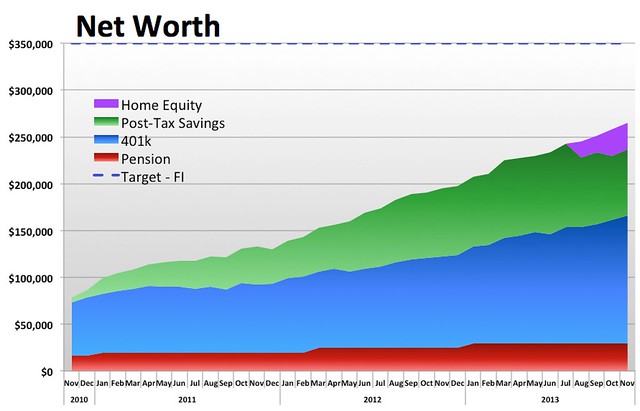

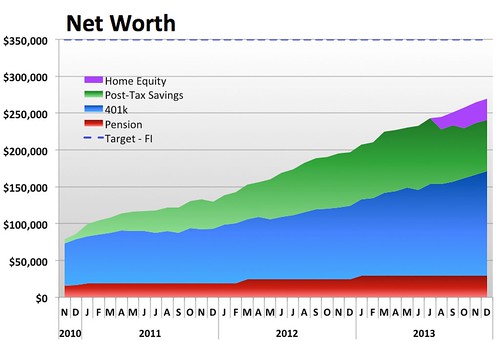

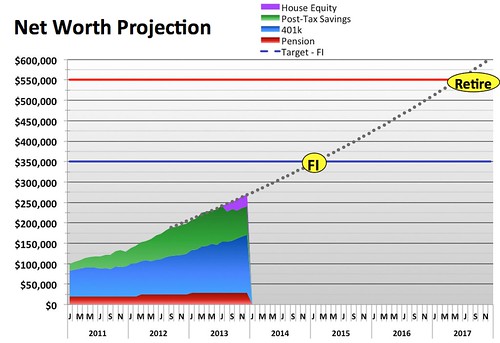

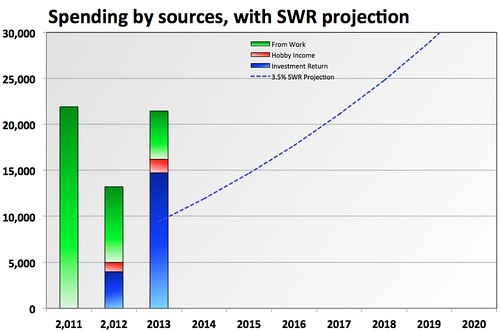

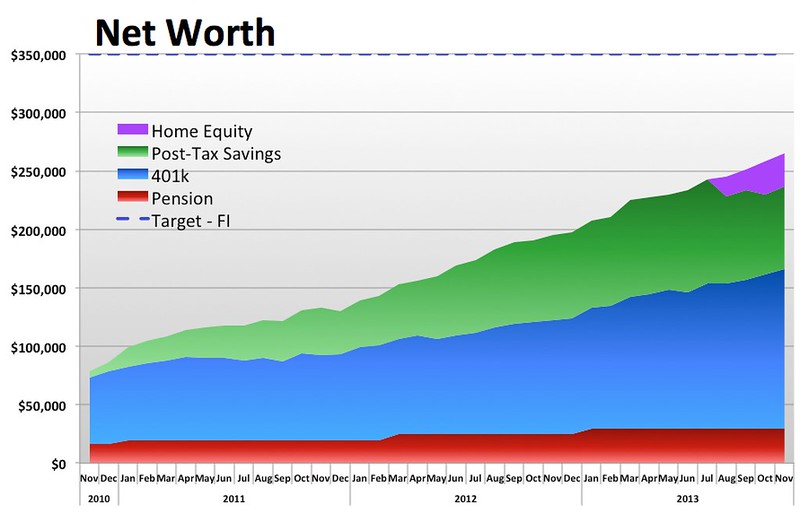

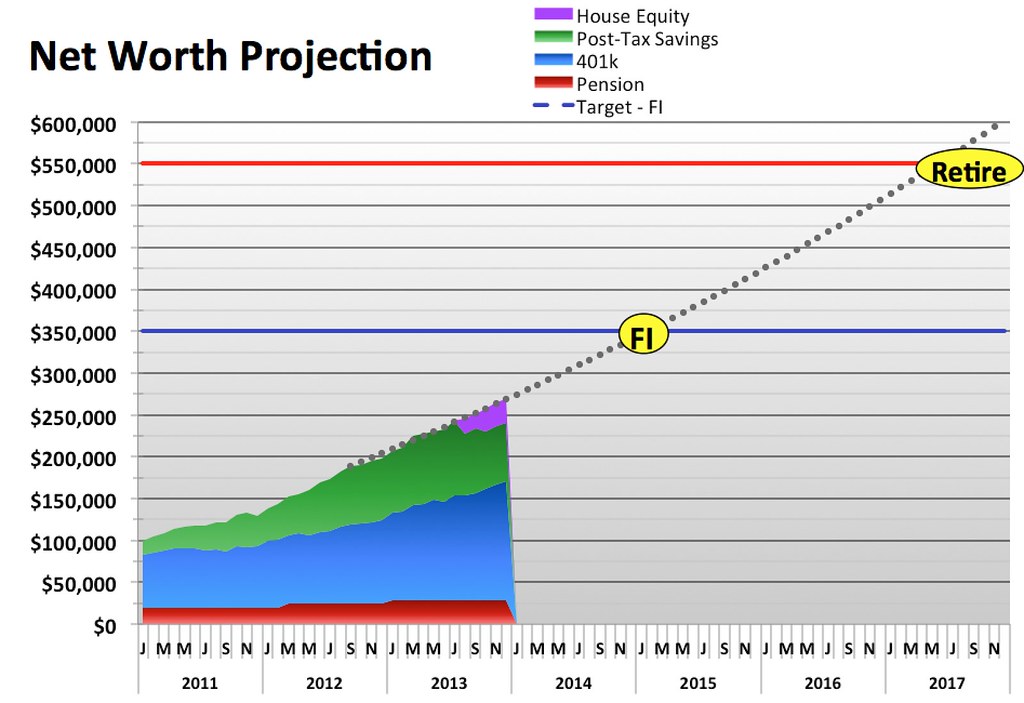

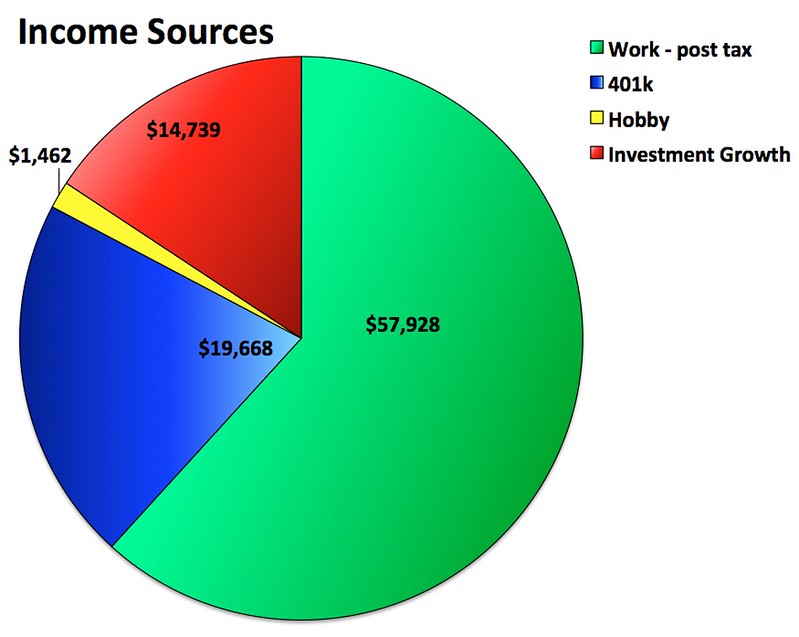

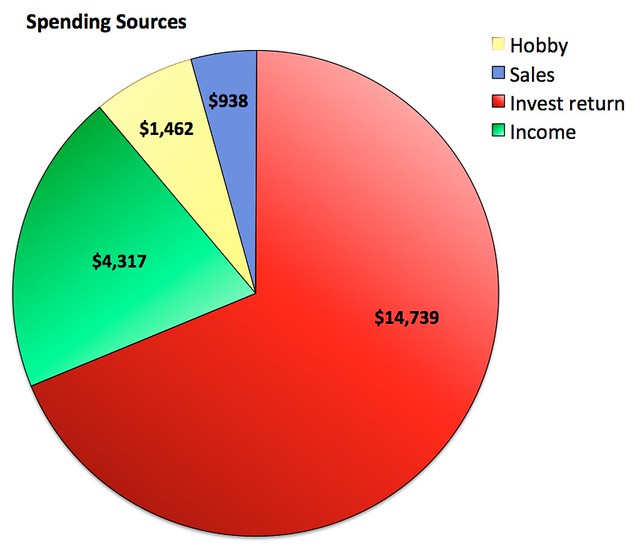

Also, got some good ideas for my own tracking, thanks:)Also note in the Net Worth graph that I added in my work pension value. I never had this on before. I was looking at work retirement stuff and reviewed some Pension information. It seems like they changed how it works within the last couple years. Before, you would use a formula to calculate how much money you can get when you retire. You just do this math with how many years you work and your age and your highest salary, and it spits out a monthly figure. But now when I go look at it, they show a specific value, $19,300, that is supposedly mine. The pension is fully vested, and from the short explanations I've read, that means that they owe me the money, and my employment ends tomorrow, they have to give me that $19,300. So I added that to my net worth total. I was surprised how much they are putting in there - over $5,000 this year, which comes to 7% of my salary. I estimated how much the value would've been for all the months before July, so it shows up on the net worth graph like it was always in there.

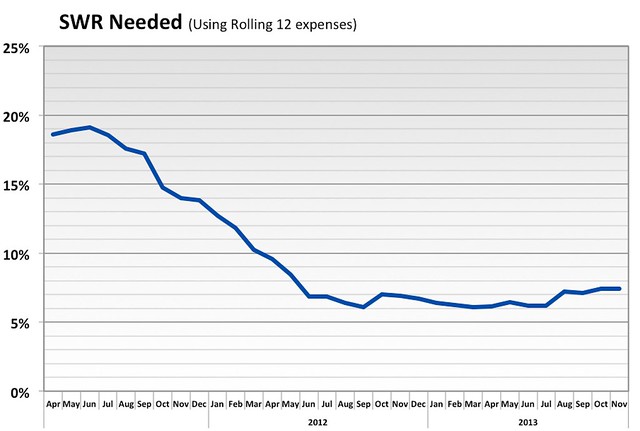

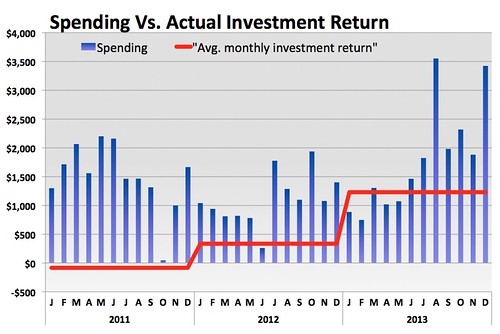

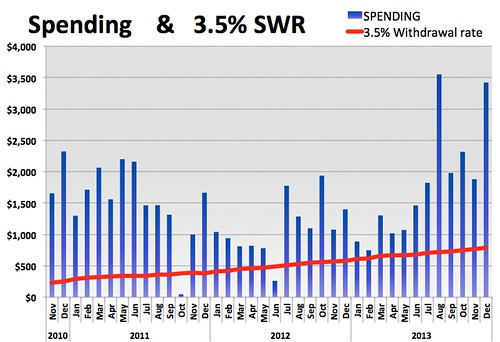

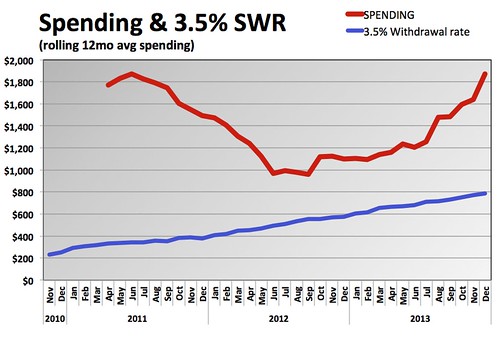

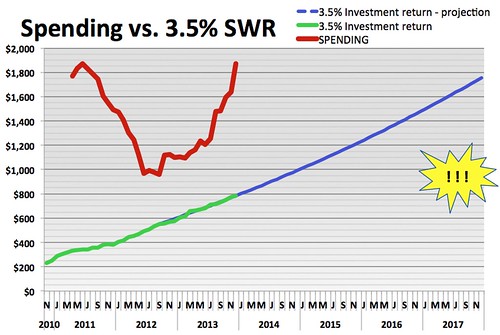

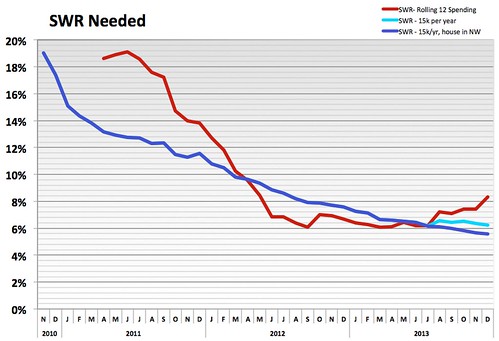

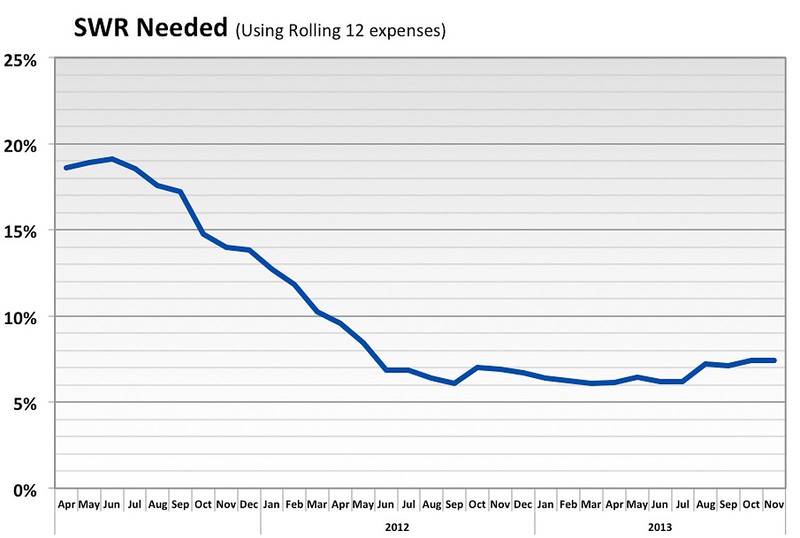

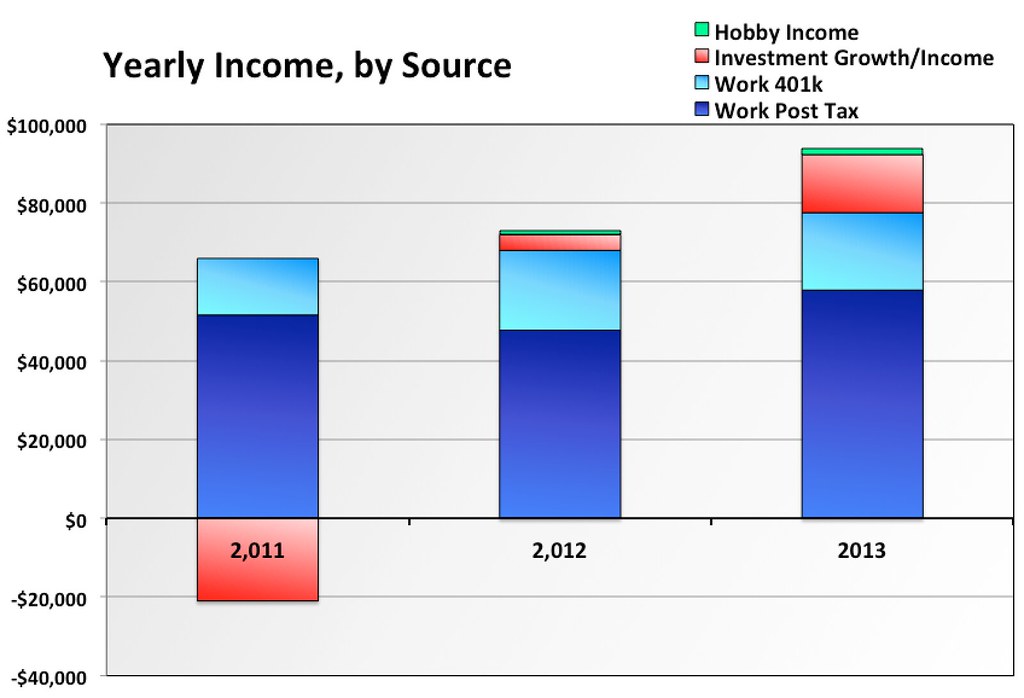

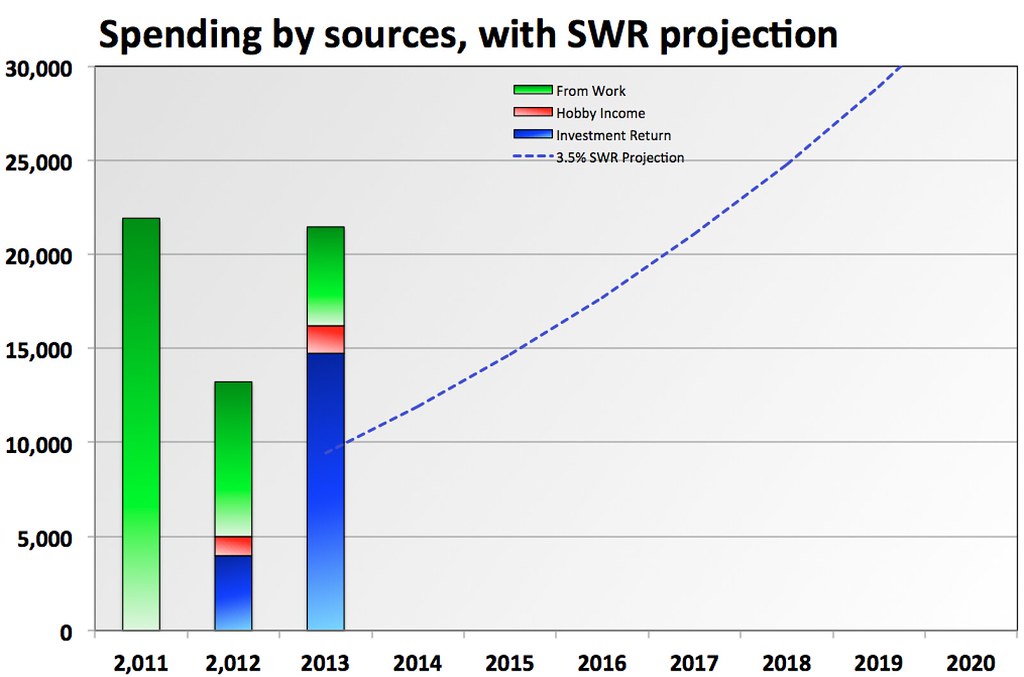

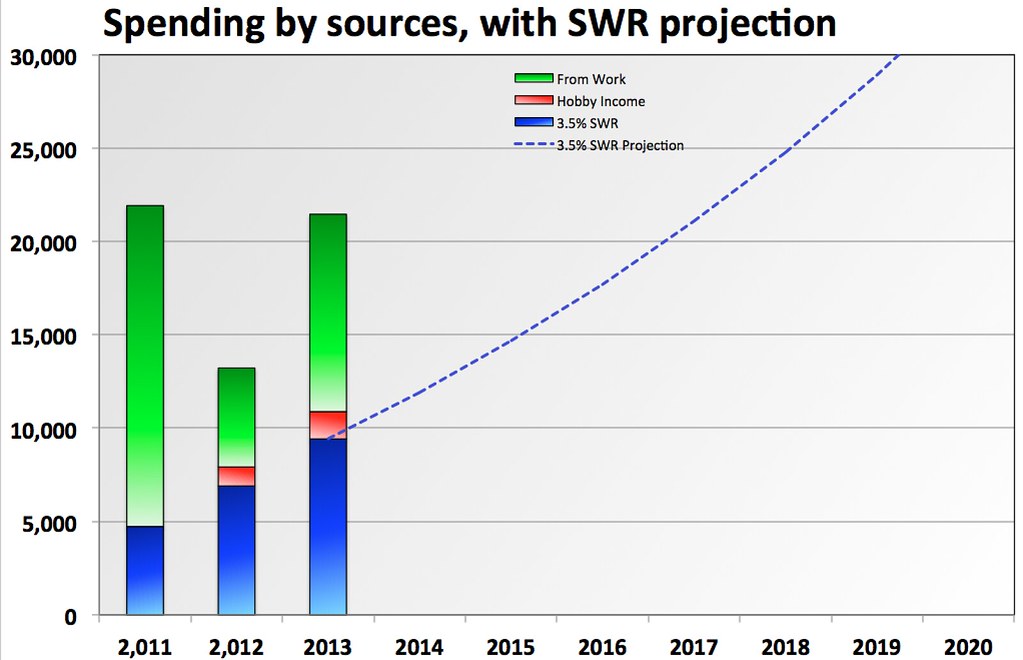

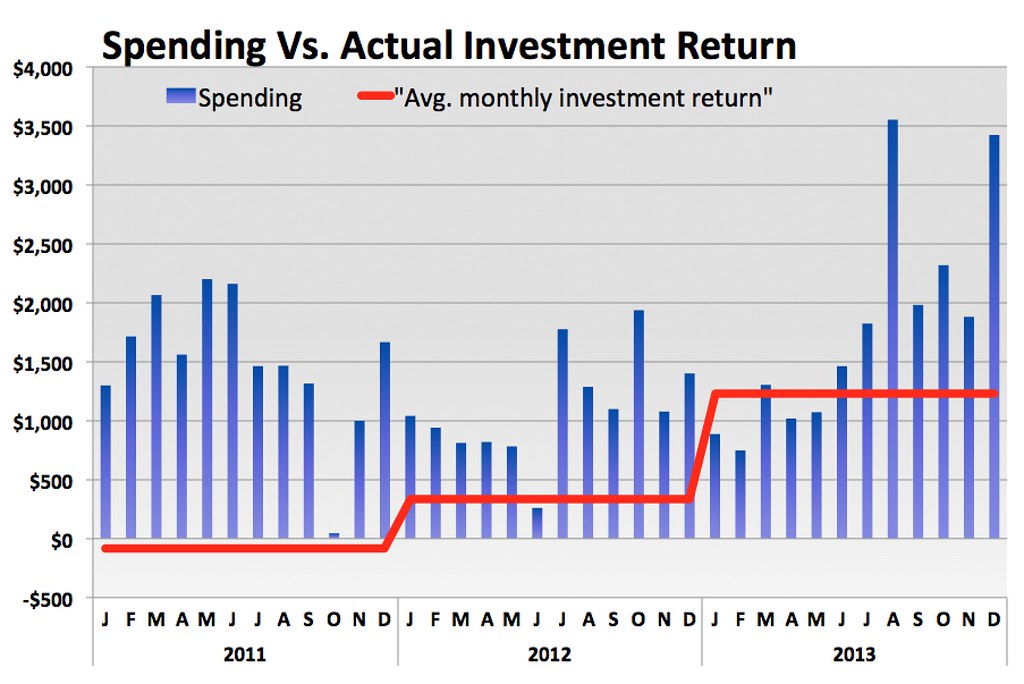

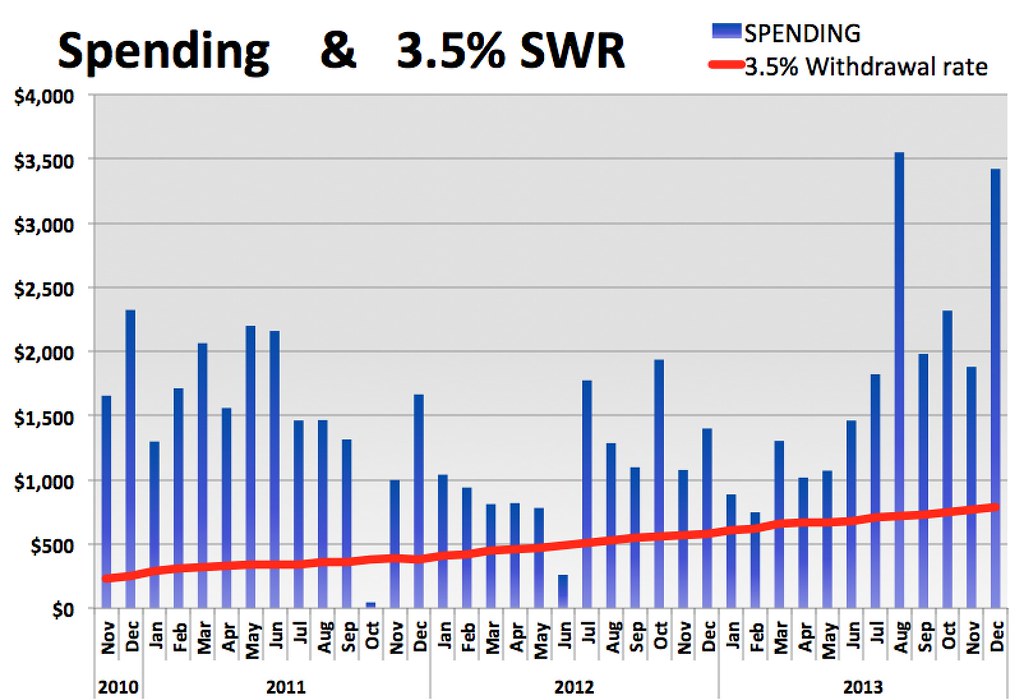

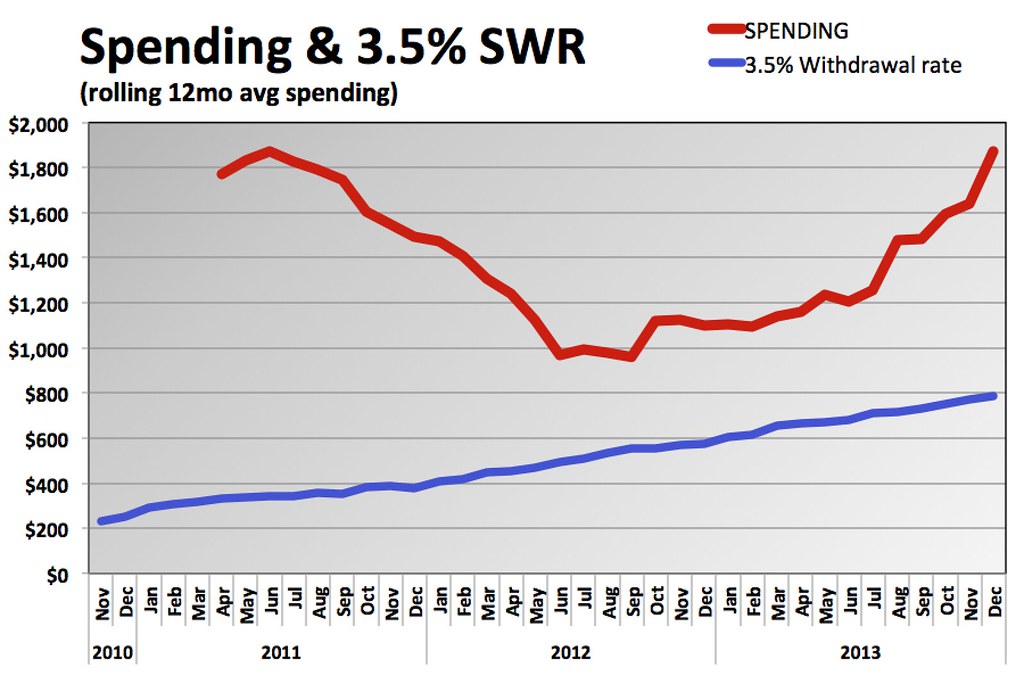

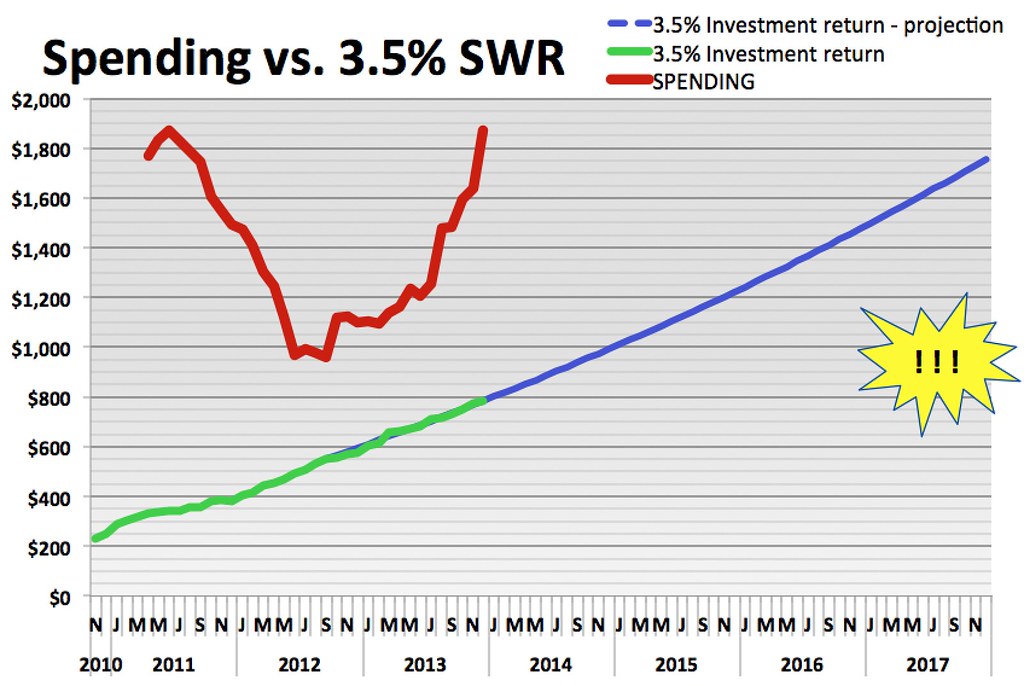

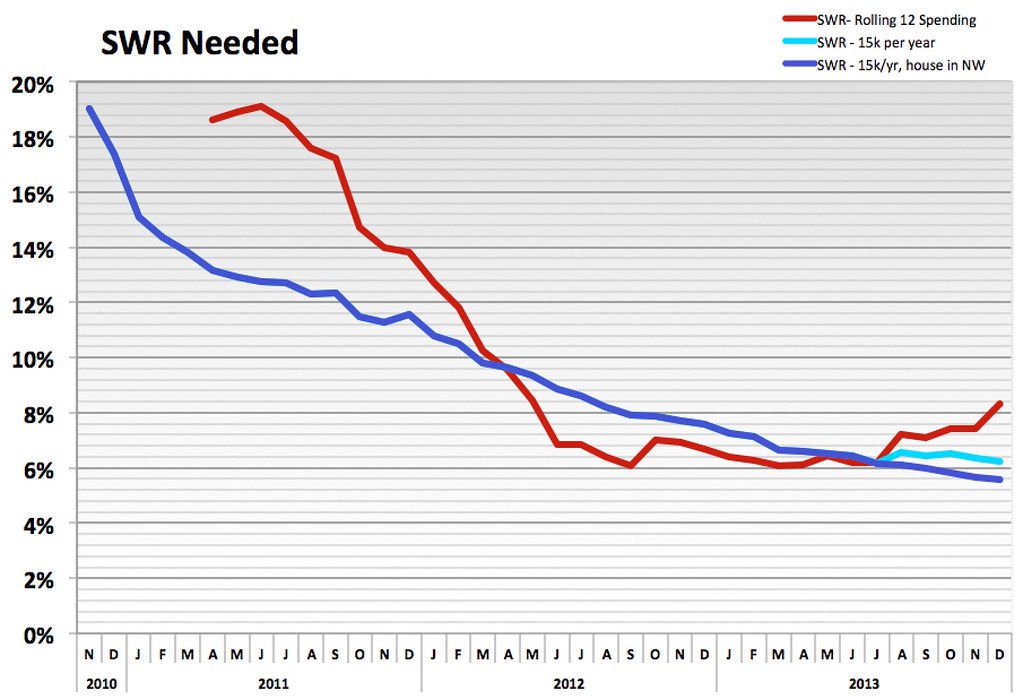

Yes, for now I'm counting 3.5% of everything (except, at times, for the money tied up in the house). There are some potential pitfalls, including:IwantLess wrote: Question for you.. when the day comes when you say you are FI and retire, are you planning on that 3.5% withdraw to be calculated from all of your combined assets even including your pension? That is the area where I'm constantly battling my approach. My current stretch goal is to be retired off my taxable account only but that means having to work a bit longer to achieve. Just curious what your plan for that is at the moment.

LOL... nice.akratic wrote: I had girlfriend as a line-item in a former wall chart, and one day my girlfriend saw it and was pretty sore about it.

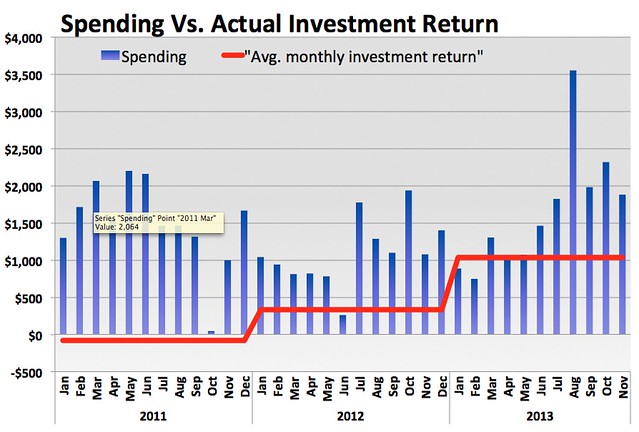

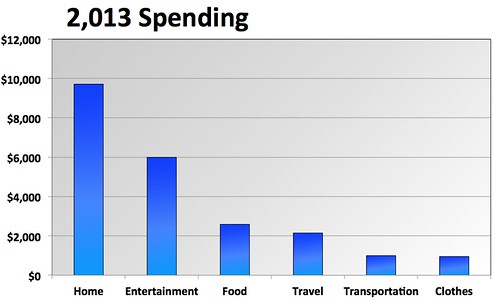

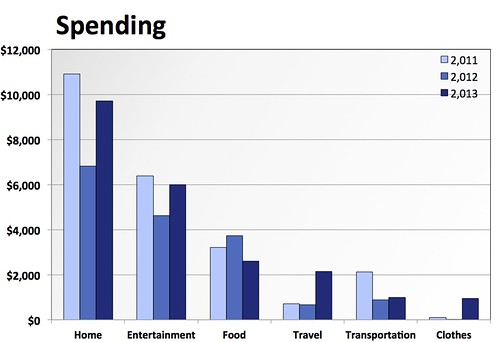

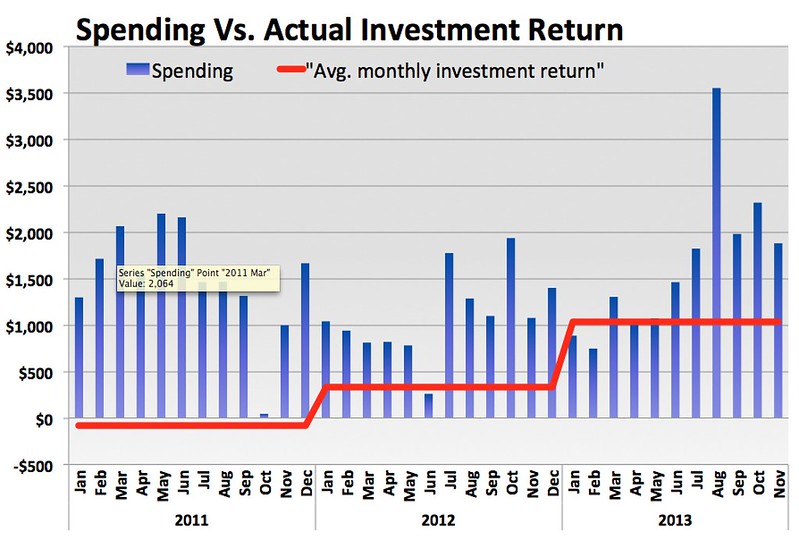

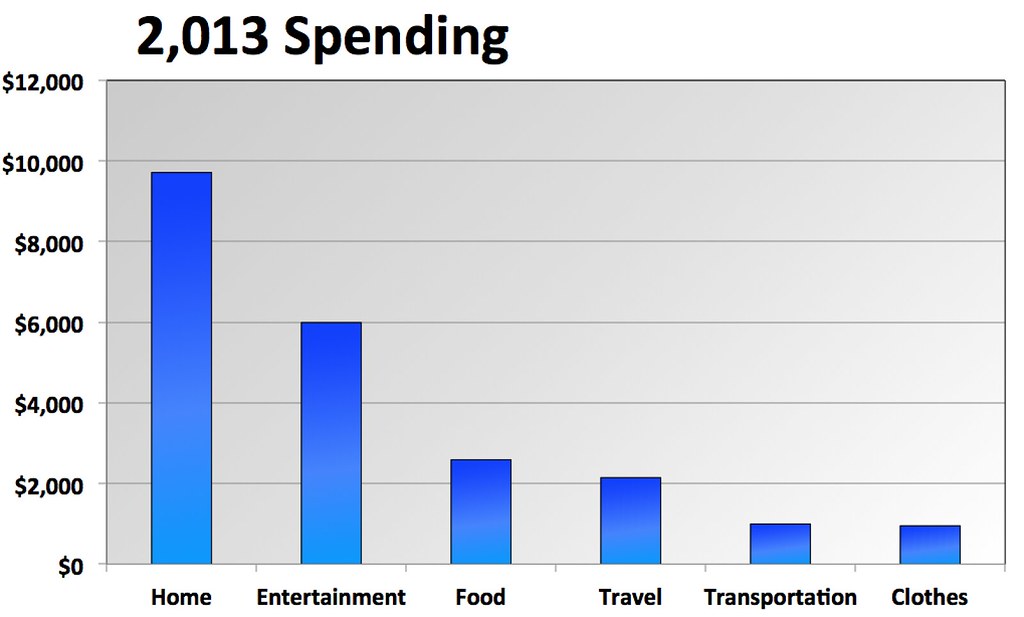

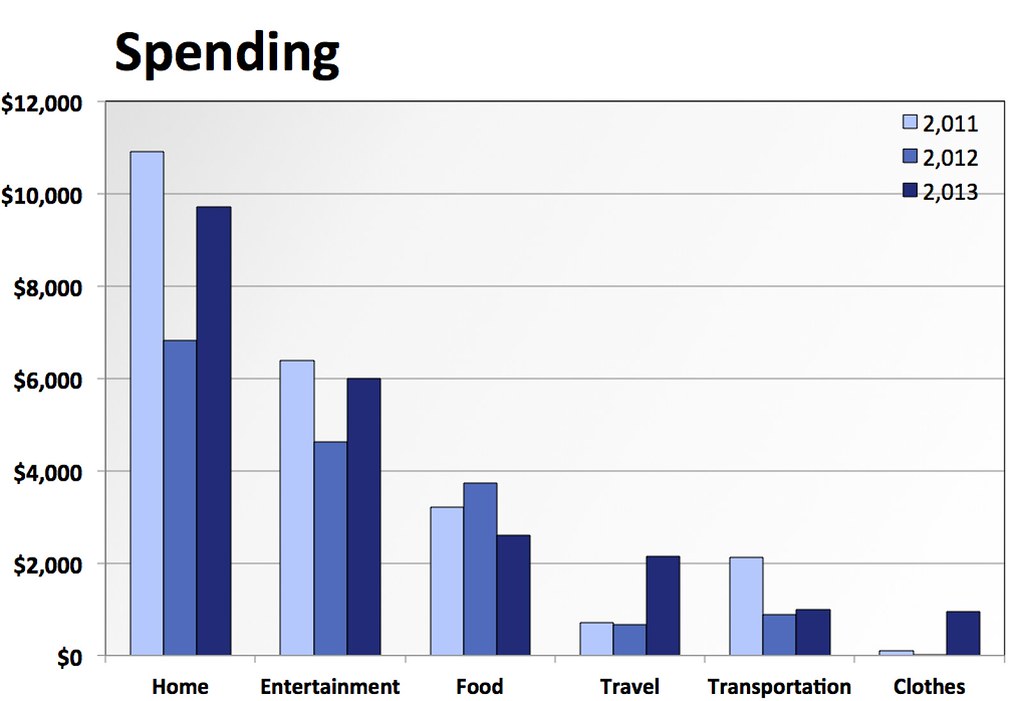

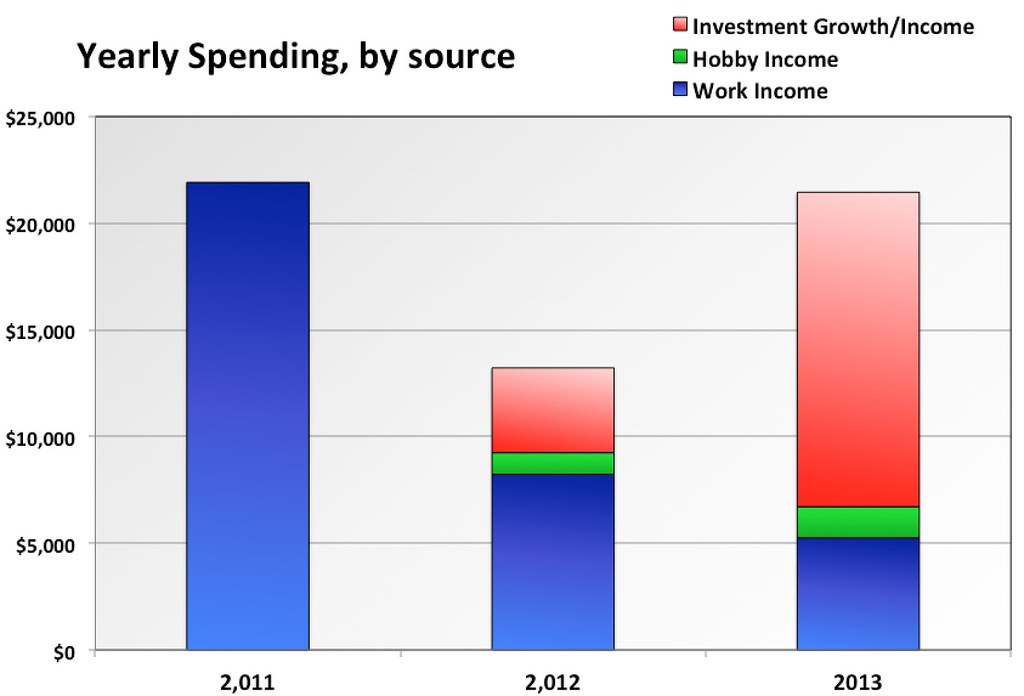

Yeah, a lot of the time that I was living in my previous apartment, a big portion of my expenses were entertainment and hobbies.. maybe 40% many months. I kind of liked it this way. I'd prefer my spending be on that instead of high rent, gas for commuting, etc.. One problem was that sometimes I just kept spending on hobbies up until I broke $1,000 for the month.akratic wrote: The entertainment number from 2013 jumps out to me as pretty high. I guess it has some pretty useful stuff in there like a computer though. I wonder if you could split that category apart so that things like a computer would'nt be grouped with things like a $10 movie ticket.

My girlfriend knows that I track all my spending and make my charts and such. She did ask me if I keep track of how much money I spend with/on her, and she didn't like that I do. She suggested/told me that I should not track it... She wasn't too surprised about her suggestion not going anywhere.akratic wrote:

I had girlfriend as a line-item in a former wall chart, and one day my girlfriend saw it and was pretty sore about it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}