Fortunately, this one was a slam dunk. But yeah, I know the feeling of not wanting to be proven wrong.

Strong work on the net worth increase this month. You have reached the point where monthly market fluctuations are larger than most household's annual incomes.

MedSaver's Journal

Re: MedSaver's Journal

Apologies to anyone who waits for updates with bated breath, but tardy post due to illness and travel.

Oct 2024 Update

Assets:

IRA/Brokerage/403b/457/cash: $4,141,413

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $653,938 @ 2.75% fixed

Net: $4,687,475

Oct 2024 Update

Assets:

IRA/Brokerage/403b/457/cash: $4,141,413

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $653,938 @ 2.75% fixed

Net: $4,687,475

Re: MedSaver's Journal

Quoting part of your first journal post to youMedSaver wrote: ↑Fri Jan 15, 2016 1:42 amSo the purpose of this journal is to keep me honest and on track with early retirement. Our goal is liquid assets of $3-4 million. This would let us comfortably withdraw about $100,000/year indefinitely. When my fiancee and I reach our goal we will probably continue to work in some capacity. She enjoys her work and would continue at 60-80%, while I would probably do an occasional locums shift to keep my skill set up to par so our earned income wouldn't drop to zero initially. We are both in the medical field and in our early 30's. No kids (yet).

Now this was in 2016, so if you just assume you experienced the average US inflation since then, your goal now would be $4.0-5.3 million. (33% inflation total in this period, oof!). So would this still be the goal? And any plans already for the both of you on how to potentially change your jobs? It seems like your wife could easily drop down to 60-80% already, as you're getting so close to your goal that doing so would at most slow you guys down a month or two in reaching it. Coasting to the goal...

Re: MedSaver's Journal

Very astute. I was going to post this in my end of year review, but as far as the original goal stands (with inflationary correction), yes, I have accepted a part time position starting early 2025. These slots do not arise often and we had just hit our liquid asset target of right above $4MM so it seemed almost like this was preordained. I had no choice! I will be working about 2 weeks a month at ~70-ish% salary so I think this is a good deal and plan to do this for maybe 6 more years.DutchGirl wrote: ↑Mon Nov 11, 2024 2:06 amQuoting part of your first journal post to you

Now this was in 2016, so if you just assume you experienced the average US inflation since then, your goal now would be $4.0-5.3 million. (33% inflation total in this period, oof!). So would this still be the goal? And any plans already for the both of you on how to potentially change your jobs? It seems like your wife could easily drop down to 60-80% already, as you're getting so close to your goal that doing so would at most slow you guys down a month or two in reaching it. Coasting to the goal...

Mrs. MedSaver continues to enjoy her job and will remain 100% for around 4 more years at which point her succession plan is in place to move to about 50-60%, but from a site much closer to home.

Time to start coasting.

Re: MedSaver's Journal

Oh, that sounds very nice! I'm sure you're looking forward to that.

And what is it that they say? Luck favors the prepared... (Apparently Louis Pasteur said something like that, which seems appropriate).

I hope that you'll love it and I hope you'll keep us posted about how it feels and what you're doing with your extra non-work time...

And what is it that they say? Luck favors the prepared... (Apparently Louis Pasteur said something like that, which seems appropriate).

I hope that you'll love it and I hope you'll keep us posted about how it feels and what you're doing with your extra non-work time...

Re: MedSaver's Journal

Nov 2024 Update

Assets:

IRA/Brokerage/403b/457/cash: $4,216,585

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $652,638 @ 2.75% fixed

Net: $4,763,947

Assets:

IRA/Brokerage/403b/457/cash: $4,216,585

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $652,638 @ 2.75% fixed

Net: $4,763,947

Re: MedSaver's Journal

Strong work. I feel decamillionaire status is in your future (5-10 years max).

Re: MedSaver's Journal

Annual Update

INCOME:

MedSaver gross W2 income 2024: $676,000 (2023: $686,000 ), down <2%.

Net income 2024: $366,667 (2023: $350,485), up 5%. Not sure why net income rose when gross income fell.

Monthly net: $30,555

Mrs. MedSaver gross W2 income 2024: $205,028 (2023: $196,665), up 8%.

Net income 2024: $30,005 (2023: $28,514), up 5%.

Monthly net: $2,500

Deferred comp/income not otherwise specified: ~$237,000.

Total gross annual earned income: $881,000

EXPENDITURES:

Spending breakdown (monthly):

Food (groceries+restaurants): $1900 (Up from $1800)

Mortgage (principal/interest/insurance): $4600 (up from $4400 due to change in taxes and homeowners insurance)

Other Insurance: $1100 (Up from $950)

Utilities: $300 up from $270)

Gas: $150 (no change)

Internet: $85 (no change)

Cleaning service: $360 (no change)

Cell phone: $125 (No change)

Travel: $4450 (previously $3000) - starting to take “bucket list” type trips

Other: $7500 (previously $6800)

Total monthly recurring expenses 2024: $20,750 (previously $17,870)

Total annual expenses: $249,000. More than last year. Large rise in travel expenses. We took our first 2 week long vacation in almost a decade.

ASSETS:

IRA/Brokerage/403b/457/cash: $4,145,067 (Jan 2024 $3,124,863)

Estimated Home Worth: $1,150,000

Mortgage: $652,021 (2023: $682,370) @ 2.75% fixed

Total Net Worth: $4,643,046 (Jan 2024 $3,592,493), which is +$87,549 (previously +99,117/month)

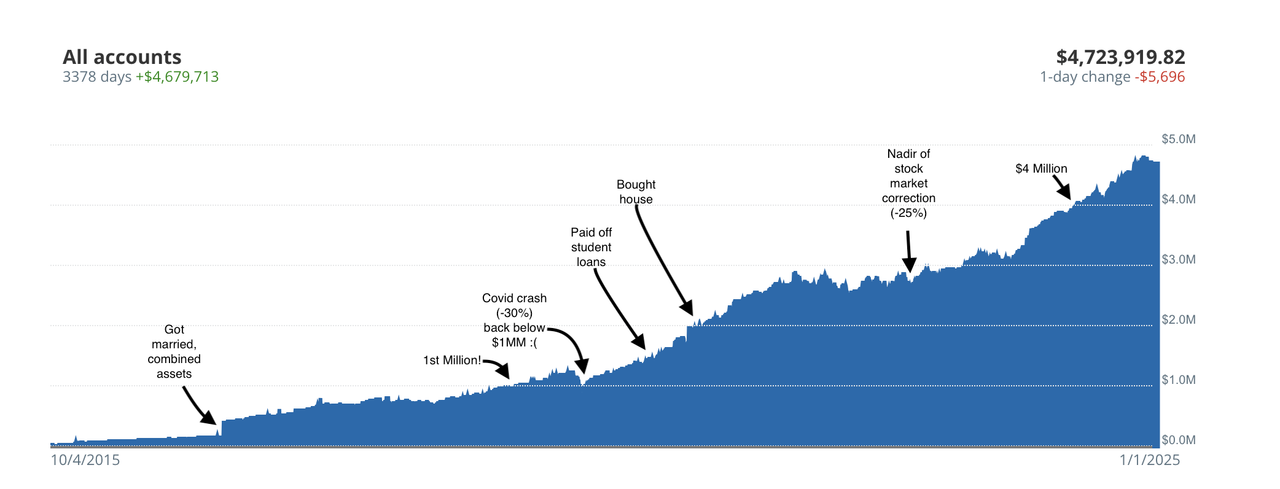

Sometimes a picture (or graph) is better at showing the forest for the trees.

INCOME:

MedSaver gross W2 income 2024: $676,000 (2023: $686,000 ), down <2%.

Net income 2024: $366,667 (2023: $350,485), up 5%. Not sure why net income rose when gross income fell.

Monthly net: $30,555

Mrs. MedSaver gross W2 income 2024: $205,028 (2023: $196,665), up 8%.

Net income 2024: $30,005 (2023: $28,514), up 5%.

Monthly net: $2,500

Deferred comp/income not otherwise specified: ~$237,000.

Total gross annual earned income: $881,000

EXPENDITURES:

Spending breakdown (monthly):

Food (groceries+restaurants): $1900 (Up from $1800)

Mortgage (principal/interest/insurance): $4600 (up from $4400 due to change in taxes and homeowners insurance)

Other Insurance: $1100 (Up from $950)

Utilities: $300 up from $270)

Gas: $150 (no change)

Internet: $85 (no change)

Cleaning service: $360 (no change)

Cell phone: $125 (No change)

Travel: $4450 (previously $3000) - starting to take “bucket list” type trips

Other: $7500 (previously $6800)

Total monthly recurring expenses 2024: $20,750 (previously $17,870)

Total annual expenses: $249,000. More than last year. Large rise in travel expenses. We took our first 2 week long vacation in almost a decade.

ASSETS:

IRA/Brokerage/403b/457/cash: $4,145,067 (Jan 2024 $3,124,863)

Estimated Home Worth: $1,150,000

Mortgage: $652,021 (2023: $682,370) @ 2.75% fixed

Total Net Worth: $4,643,046 (Jan 2024 $3,592,493), which is +$87,549 (previously +99,117/month)

Sometimes a picture (or graph) is better at showing the forest for the trees.

Re: MedSaver's Journal

Jan 2025 Update

Assets:

IRA/Brokerage/403b/457/cash: $4,247,281

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $652,638 @ 2.75% fixed

Net: $4,794,643

Assets:

IRA/Brokerage/403b/457/cash: $4,247,281

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $652,638 @ 2.75% fixed

Net: $4,794,643

-

2Birds1Stone

- Posts: 1779

- Joined: Thu Nov 19, 2015 11:20 am

- Location: Earth

Re: MedSaver's Journal

Your income is insanely high, but spending is too. What is "Other" @ $7,500/month or $90k a year.

At first glance I thought these were annual numbers and as I nodded I realized that they were monthly =D

At first glance I thought these were annual numbers and as I nodded I realized that they were monthly =D

Re: MedSaver's Journal

Feb 2025 Update

Assets:

IRA/Brokerage/403b/457/cash: $4,245,827

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $651,338 @ 2.75% fixed

Net: $4,794,489

Assets:

IRA/Brokerage/403b/457/cash: $4,245,827

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $651,338 @ 2.75% fixed

Net: $4,794,489

Re: MedSaver's Journal

Hi. The "other" is goods/merchandise, subscriptions, home maintenance/upkeep, HOA fee, gifts, charitable giving, clothes, political contributions, automotive upkeep, gym membership, pet food/supplies, vet visits, work parking fees, and healthcare amongst other things.2Birds1Stone wrote: ↑Sat Feb 01, 2025 4:32 amYour income is insanely high, but spending is too. What is "Other" @ $7,500/month or $90k a year.

At first glance I thought these were annual numbers and as I nodded I realized that they were monthly =D

-

2Birds1Stone

- Posts: 1779

- Joined: Thu Nov 19, 2015 11:20 am

- Location: Earth

Re: MedSaver's Journal

Those sound like some of the bigger ticket items when broken down, no? You're tracking $150/month in gas and and $85/month on internet separately but lumping $7,500 worth of stuff together? I guess that's why it didn't make sense to me -_-

Re: MedSaver's Journal

Your expenses are high compared to others here on the forum (including me). If you want to keep spending $250k per year, you'd have to reach a net worth of $6.3 million to likely be able to continue to cover your expenses from your investments.

...but you will easily reach that amount in a couple of years, even with now slightly reduced income (you did go for that new part time role, right?). And your expenses are probably low compared to other people in your direct vicinity - so keep them in check.

Maybe it's a good thing to know that with your current net worth a good lifestyle can also be had. You would have to make some adjustments if all income streams suddenly dried up and you would have to "make do" - ahem - with $4.8 million, but you would definitely still be comfortable, and be able to have a lot of fun.

How is the new role?

And are you donating to charities in a tax-efficient way? Have you looked into donor-advised funds?

...but you will easily reach that amount in a couple of years, even with now slightly reduced income (you did go for that new part time role, right?). And your expenses are probably low compared to other people in your direct vicinity - so keep them in check.

Maybe it's a good thing to know that with your current net worth a good lifestyle can also be had. You would have to make some adjustments if all income streams suddenly dried up and you would have to "make do" - ahem - with $4.8 million, but you would definitely still be comfortable, and be able to have a lot of fun.

How is the new role?

And are you donating to charities in a tax-efficient way? Have you looked into donor-advised funds?

Re: MedSaver's Journal

March 2025 Update

Assets:

IRA/Brokerage/403b/457/cash: $3,946,903

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $650,038 @ 2.75% fixed

Net: $4,496,865

Assets:

IRA/Brokerage/403b/457/cash: $3,946,903

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $650,038 @ 2.75% fixed

Net: $4,496,865

Re: MedSaver's Journal

It doesn't really make sense. The reported categories are a vestige of when I first started this journal. The "other" category is so large and undefined because actually tracking a lot of the underlying items is hard to do and I don't have the time to do it. Our finance tracking software does a pretty good job, but it incorrectly categorizes enough items that I would find it annoying and spend hours trying to fix it all.2Birds1Stone wrote: ↑Sun Mar 02, 2025 10:50 pmThose sound like some of the bigger ticket items when broken down, no? You're tracking $150/month in gas and and $85/month on internet separately but lumping $7,500 worth of stuff together? I guess that's why it didn't make sense to me -_-

Re: MedSaver's Journal

Our retirement spending goal is around $200k. It sounds like a lot, but my wife makes around $200k and wants to work longer than I do. So even after taxes, our portfolio should be fine.DutchGirl wrote: ↑Mon Mar 03, 2025 5:38 amYour expenses are high compared to others here on the forum (including me). If you want to keep spending $250k per year, you'd have to reach a net worth of $6.3 million to likely be able to continue to cover your expenses from your investments.

...but you will easily reach that amount in a couple of years, even with now slightly reduced income (you did go for that new part time role, right?). And your expenses are probably low compared to other people in your direct vicinity - so keep them in check.

Maybe it's a good thing to know that with your current net worth a good lifestyle can also be had. You would have to make some adjustments if all income streams suddenly dried up and you would have to "make do" - ahem - with $4.8 million, but you would definitely still be comfortable, and be able to have a lot of fun.

How is the new role?

And are you donating to charities in a tax-efficient way? Have you looked into donor-advised funds?

Unfortunately, our candidate fell through at the last minute, which means that not only will I not be going part time, I'll be working (and earning) more than planned in 2025. I expect gross income above $1 million.

Re: MedSaver's Journal

Sounds like it's time to start up the hiring process again? Or is this a thing that only works in January for some reason?

Oh by the way, the market downturn means that your net worth decreased. It happens. Hurray for being able to buy some more stocks at (slight?) discounts...

Oh by the way, the market downturn means that your net worth decreased. It happens. Hurray for being able to buy some more stocks at (slight?) discounts...

Re: MedSaver's Journal

April 2025 Update

Assets:

IRA/Brokerage/403b/457/cash: $4,225,670

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $648,738 @ 2.75% fixed

Net: $4,776,932

Assets:

IRA/Brokerage/403b/457/cash: $4,225,670

Estimated Home Worth: $1,200,000

Liabilities:

Mortgage: $648,738 @ 2.75% fixed

Net: $4,776,932

Re: MedSaver's Journal

Yes, we have (re)started our hiring. I do believe that we finally have a good candidate who plans to start with us in Jan '26. We have also been able to find some locums providers (hired guns) that can offload some of our work until then. This is a very lucky turn of events as our specialty is in a historic shortage and good candidates are rare. My fingers are crossed that I will be able to go part time at the end of the year.DutchGirl wrote: ↑Fri Apr 04, 2025 2:26 amSounds like it's time to start up the hiring process again? Or is this a thing that only works in January for some reason?

Oh by the way, the market downturn means that your net worth decreased. It happens. Hurray for being able to buy some more stocks at (slight?) discounts...