Negativity bias plays a big role. We tend to obsess on all the negative shit that could happen and become risk averse that way, driving down the PWR.

My Vanguard Monte Carlo calculation uses age 100 for both DW and I. Really? I don’t need to worry about making it that long … and we still have a 98% chance of success.

How to move the PWR higher? Learn to live in the moment more.

Mark Twain quote that I posted recently elsewhere: “I’ve suffered through some terrible things in my life, some of which actually happened.”

Psychological withdrawal rate

Re: Psychological withdrawal rate

This sounds true to me. We are psychoanalyzing people which is fraught with danger but I think some people want to feel they've won some game.prudentelo wrote: ↑Thu Jan 27, 2022 6:41 pmThat is desire for progression.

With a "runaway portfolio" one can get the feeling of "promotion" over time that often comes with a hierarchical salary job, by increasing the networth passively.

A sense of improving one's condition is important to many people, even if they don't need to do so to satisfy their wants.

This is another good one. I suppose this is why people believe in SWR's. If I just get to 4% then I'll be safe and on it goes.Married2aSwabian wrote: ↑Thu Jan 27, 2022 7:35 pmNegativity bias plays a big role. We tend to obsess on all the negative shit that could happen and become risk averse that way, driving down the PWR.

-

Laura Ingalls

- Posts: 723

- Joined: Mon Jun 25, 2012 3:13 am

Re: Psychological withdrawal rate

@ Ego

I agree that fear goes down the longer you have done this early retirement thing regardless of what it looks like in your specific situation. Part of that is practice and mental transitioning from accumulation mode to either a more subsistence mode or de-accumulation mode.

I tell myself from time to time that if $X was enough money to retire with in 2014 is can surely stomach some market fluctuations now that I am at $2X. I also am almost 8 years older and our offspring have gone from school aged kids to an adult (finishing his degree this summer) and near adult with three semesters of high school left. My resources (social, financial, physical) have less ground to cover now than they did then.

In our situation we have financial reinforcements coming (ie pensions, Social Security and an above average chance of inheritance.)

I agree that fear goes down the longer you have done this early retirement thing regardless of what it looks like in your specific situation. Part of that is practice and mental transitioning from accumulation mode to either a more subsistence mode or de-accumulation mode.

I tell myself from time to time that if $X was enough money to retire with in 2014 is can surely stomach some market fluctuations now that I am at $2X. I also am almost 8 years older and our offspring have gone from school aged kids to an adult (finishing his degree this summer) and near adult with three semesters of high school left. My resources (social, financial, physical) have less ground to cover now than they did then.

In our situation we have financial reinforcements coming (ie pensions, Social Security and an above average chance of inheritance.)

-

Western Red Cedar

- Posts: 1343

- Joined: Tue Sep 01, 2020 2:15 pm

Re: Psychological withdrawal rate

This is, for me, a timely discussion. I've been digging into withdrawal strategies over the last week or two, and finally going through Big ERN's Safe Withdrawal Rate Series: https://earlyretirementnow.com/safe-wit ... te-series/

I've had reservations about a SWR below 4% and always felt like that was much too conservative. But, after reading about a dozen of his posts I'm appreciating why one may want target a 3-3.5% SWR in the current market environment - particularly if you are planning on a 40-60 year retirement. The whole series, which is thoroughly researched and logical, veers towards a low PWR. But for good reason.

Previously, I've gravitated towards SemiERE which really leverages PWR. It requires confidence that things will work out, and that one can easily tap into new income sources or minimize expenses through creativity or flexibility. It requires a mindset of abundance, rather than scarcity.

But this is close to where I'm at now:

viewtopic.php?p=240072#p240072

I've had reservations about a SWR below 4% and always felt like that was much too conservative. But, after reading about a dozen of his posts I'm appreciating why one may want target a 3-3.5% SWR in the current market environment - particularly if you are planning on a 40-60 year retirement. The whole series, which is thoroughly researched and logical, veers towards a low PWR. But for good reason.

Previously, I've gravitated towards SemiERE which really leverages PWR. It requires confidence that things will work out, and that one can easily tap into new income sources or minimize expenses through creativity or flexibility. It requires a mindset of abundance, rather than scarcity.

But this is close to where I'm at now:

The ERE Wheaton Table helped explain why I'm bouncing back and forth between a 3% SWR and not really worrying about SWR at all (see retirement goal):Lemur wrote: ↑Thu Jan 27, 2022 10:11 amAnother factor effecting PsyWR is where you're currently at in your career or business (salaryman / businessman respectively).

Take for instance the salaryman making above median income or into the 6 figures. They're at a 4-5% SWR right now. Very hard to shut off that money stream when this is all you know! This leads to a feedback loop of being conservative (what if this happens and so on and so forth).

viewtopic.php?p=240072#p240072

If you don't progress beyond WL 5 or 6, you risk falling victim to a low PWR. Money is the easy option to solve your problems. Once you are at WL 7+, you realize that money is just another resource that you can tap into and SWR becomes somewhat irrelevant.prudentelo wrote: ↑Tue Jan 25, 2022 3:10 pmERE should increase PWR, because ERE reduces dependence on money in general, but I see a lot of FIRE and ERE online community have very low PWR. Maybe high PWR people with renaissance skills become entrepreneurs and either become millionaires or blow up.

So PWR might be a bigger barrier to retirement than SWR. What are some techniques for increasing PWR?

Re: Psychological withdrawal rate

I feel this. The ground for security always shifting beneath my feet. I tell myself in part it is because of the Canadian housing market is bonkers. But I know that is only part of the story. After all, it is hard to make money faster than the house prices climb here  . Inflation? No such thing. Move along unlanded peasant.

. Inflation? No such thing. Move along unlanded peasant.

I'm well under 3% withdrawal rate including taxes and fees, and still working. Part of it is I will likely be making financially suboptimal decisions in the near future for love . Burn years of salary on aggressively paying a portion of a mortgage, as my obligation of a yet to be finalized contractual agreement. Lovely. But when it's done, I'm done. For real. I will be under 2% then, and my income tax obligations nil since I won't need the cash flow for rent. At least, that is what I tell myself.

. Burn years of salary on aggressively paying a portion of a mortgage, as my obligation of a yet to be finalized contractual agreement. Lovely. But when it's done, I'm done. For real. I will be under 2% then, and my income tax obligations nil since I won't need the cash flow for rent. At least, that is what I tell myself.

But part of it is I am in a good spot. Make hay while the sun shines. I know from experience this rarely lasts and a natural exit will present itself. I want to enjoy the camaraderie for as long as I still get something besides money from it.

Assuming the TEOTWAWKI doesn't nuke my financial assets (Hello everyone. My name is slsdly and I am a doomer.), I likely will hit my end of days with a mountain of unspent wealth. I'm fine with that. As long as I avoid lifestyle inflation, accumulating more assets is like sequestering carbon dioxide or something. And if the world does drastically change, well, it's not like I have much agency in that aspect. Sometimes the whole town burns down.

I'm well under 3% withdrawal rate including taxes and fees, and still working. Part of it is I will likely be making financially suboptimal decisions in the near future for love

But part of it is I am in a good spot. Make hay while the sun shines. I know from experience this rarely lasts and a natural exit will present itself. I want to enjoy the camaraderie for as long as I still get something besides money from it.

Assuming the TEOTWAWKI doesn't nuke my financial assets (Hello everyone. My name is slsdly and I am a doomer.), I likely will hit my end of days with a mountain of unspent wealth. I'm fine with that. As long as I avoid lifestyle inflation, accumulating more assets is like sequestering carbon dioxide or something. And if the world does drastically change, well, it's not like I have much agency in that aspect. Sometimes the whole town burns down.

-

Married2aSwabian

- Posts: 265

- Joined: Thu Jan 07, 2021 7:45 pm

Re: Psychological withdrawal rate

Having a higher PWR is definitely a matter of perception and letting go.

Last night we watched the live stream of funeral of one of my favorite teachers in mindfulness: Thich Nhat Hanh. RIP.

He summed it up best at 31:20 of this video (it’s just about 2 minutes from there):

https://youtu.be/b5gMJ1BovQ0

I’m working on letting go of more “Cows”.

Last night we watched the live stream of funeral of one of my favorite teachers in mindfulness: Thich Nhat Hanh. RIP.

He summed it up best at 31:20 of this video (it’s just about 2 minutes from there):

https://youtu.be/b5gMJ1BovQ0

I’m working on letting go of more “Cows”.

-

prudentelo

- Posts: 173

- Joined: Sat Jan 22, 2022 8:55 am

Re: Psychological withdrawal rate

@steveo73

"This sounds true to me. We are psychoanalyzing people which is fraught with danger but I think some people want to feel they've won some game."

I can only say, this is one factor for myself. (To keep progressing, not to "win" - for me, the end is not as important as the journey).

I am not sure it is negative or positive. Or both.

It is negative in that there may be other games we are not playing, because we may be stuck mentally inside this one.

"This sounds true to me. We are psychoanalyzing people which is fraught with danger but I think some people want to feel they've won some game."

I can only say, this is one factor for myself. (To keep progressing, not to "win" - for me, the end is not as important as the journey).

I am not sure it is negative or positive. Or both.

It is negative in that there may be other games we are not playing, because we may be stuck mentally inside this one.

Re: Psychological withdrawal rate

In my case, I don't think it's negativity, but an approach to ambiguity and uncertainty (create a larger buffer). If one is responsible for themselves and don't have children/relatives who can buffer COL variability, PWR may be low, but is just adjusting for the uncertainty of a long duration estimate. But worrying about all the events that could destroy and plan without balancing it dreaming about all the events that could make it a reality is illogical and probably not healthy. We could all just buy a Tesla personal robot who can take care of us from cradle to grave. A good heuristic is if you're worried about X happening and ending your FIRE plans, keep working or cut spending.Married2aSwabian wrote: ↑Thu Jan 27, 2022 7:35 pmNegativity bias plays a big role. We tend to obsess on all the negative shit that could happen and become risk averse that way, driving down the PWR.

My Vanguard Monte Carlo calculation uses age 100 for both DW and I. Really? I don’t need to worry about making it that long … and we still have a 98% chance of success.

How to move the PWR higher? Learn to live in the moment more.

Mark Twain quote that I posted recently elsewhere: “I’ve suffered through some terrible things in my life, some of which actually happened.”

-

prudentelo

- Posts: 173

- Joined: Sat Jan 22, 2022 8:55 am

Re: SWR milestone record

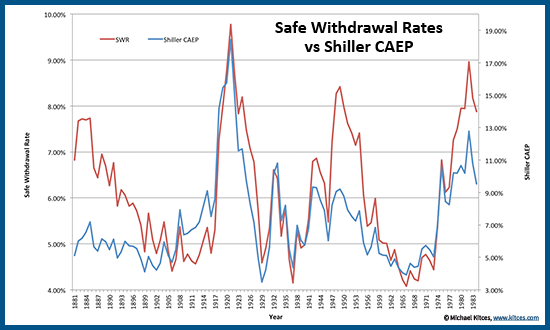

An optimally efficient WR should be upwardly volatile from the 3/4% 'minimums':

There is also a trade-off between efficiency and reliability.

There is also a trade-off between efficiency and reliability.

-

jacob

- Site Admin

- Posts: 16290

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: Psychological withdrawal rate

Shiller CAEP = 1/CAPE is currently (2022) at 2.7%.

-

prudentelo

- Posts: 173

- Joined: Sat Jan 22, 2022 8:55 am

Re: Psychological withdrawal rate

Yes, you are right. SWR back testing logic assumes that the worst historical scenario is worse than the worst possible future scenario. That is not true.

---

EDIT: BTW I wanted to clarify that "PWR" is logically separate from "rational estimate of lifetime SWR."

A PWR is a point where you're willing to pull the plug without a plan. Of course guy with 3 months savings in the bank doesn't rationally estimate he can live on it for life. He is just willing to pull the plug without a plan anyway.

SWR is a fact (or "fact") of the universe. PWR is a psychological comfort level with not being currently employed.

---

EDIT: BTW I wanted to clarify that "PWR" is logically separate from "rational estimate of lifetime SWR."

A PWR is a point where you're willing to pull the plug without a plan. Of course guy with 3 months savings in the bank doesn't rationally estimate he can live on it for life. He is just willing to pull the plug without a plan anyway.

SWR is a fact (or "fact") of the universe. PWR is a psychological comfort level with not being currently employed.