TIL I learned a new word: Hypersanity. The concept seems relevant. Here's a short but intriguing article:

https://getpocket.com/explore/item/the- ... ket-newtab

--//--

My thinking about ERE continues to evolve aggressively.

FIRE is presented as the carrot, the bait, to the ERE lifestyle. And, the whole system is presented not as directions but as a map and navigational skills. Here is the swamp of consumerism. Over there is the candy city of entrepreneurship. Through this pass lies the verdant valley of the Renaissance Ideal. Go where thou wilt. etc.

The more I spend time with the material and this community, and the more I reflect upon my relationship with work, the less enticing the well-trod path of traditional FIRE-through-investments becomes. I dislike the idea of working in my current situation for the four to five years it would take me to get to FIRE at 3% at around 1 jafi. I also dislike the idea of investing. We don't even have to get in to the topic of the ethics of an anti-capitalist investing in the stock market; the idea of investing

the time in gaining investing skill is a turn-off for some reason. I respect the idea that in order to do well in the stock market you must invest in your skill in the stock market, and that process is viscerally unappealing to me right now. I have several financial and investing books, and when I pick them up I just put them right back down. Instead of fighting that dynamic right now, I'm choosing to just accept it for the time being. I'd be a pretty crappy investor if I hated every second of it.

This might be in part due to my burnout, my lack of desire to spend one single non-critical second of my short life staring at a computer, the perceived door to stress it opens. But let's set aside the discussion for a moment and just accept that, for now, my emotional and psychological willingness to deal with diving in to the world of investing is extremely low. On top of that, I am concerned that if I 'oversave' or otherwise trad-FIRE, I'll lose motivation to work on the projects I want to. I don't know how overblown that concern is (and I don't know how I would know, without actually doing it).

I

am highly motivated to work, and build skills. There are a million projects I want to work on, all at least somewhat loosely based around a common theme that is in alignment with my vision for my life, and many of which I see a reasonable chance at remuneration. Also many of my projects will (if successful) result in eliminating line items from my expenditures. And, I'm targeting <1 jafi CoL.

I suspect that, once I get up and running (let's say 1-3 years), income from my projects will be bringing in >1 jafi, and I'll actually be enjoying my life, and my stress levels will be dramatically lower. It is entirely reasonable to suspect that somewhere in there, motivation for learning investment skills will flourish, and I can get in to that.

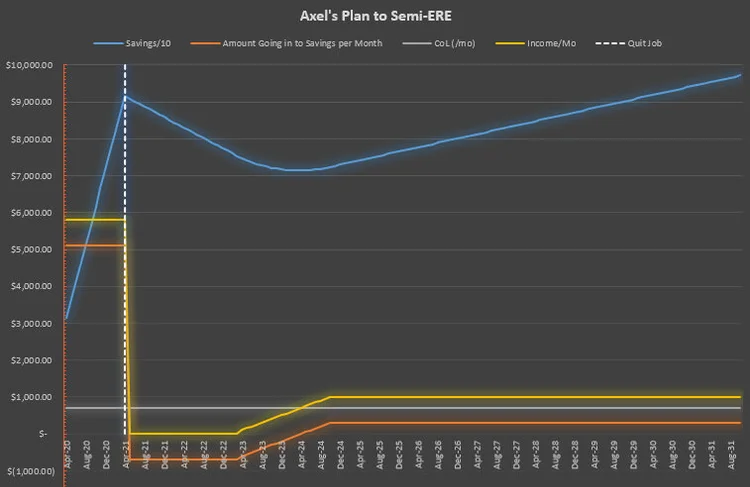

Because this is what I do, here's a graph to illustrate what I'm talking about. To make it read, the blue line representing my savings account is /10. So my savings peaks at $90,000, not $9k.

What this is assuming:

- I save like a madman for a year.

- I keep my expenses to 1 jafi forever (I actually assume I'll be able to spend less than 1 jafi, so this is conservative).

- I quit my job in April 2021.

- I don't earn a single cent for 2 full years.

- Then, I take a year and a half to slowly be generating more income, until I'm making $1k/mo.

- I don't invest anything, I don't make any investment income. (I also suspect that at some point after quitting, I'll gain an ability to invest time in investing).

- I'm ignoring inflation in this, obviously.

- It also assumes that the pay cut we all just got lasts through next year. I could be wrong either way about that - the percentage might increase, or the whole company could implode and I'm out a job.

All this graph is showing that if my assumptions hold true, my savings don't ever dip below 70k. That leaves me with a sizeable enough 'emergency' fund, and it gives me ample time to figure out how to balance my inputs and yields. The size of the stash doesn't matter if you make even slightly more than you spend.

It also has me convinced that if I lose my job sometime this year, I'm not going to scramble for a new one. I'll probably feel more hustle to get working on remunerable skills and be aiming for sooner than 2 years, but this graph gives me some confidence that I'll be able to just skim through a couple year recession.

Why assume no income for 2 years? Well, I figure it's going to take some time to de-scramble my brain and nervous system from 12 years of high stress sedentary work. And maybe I screw around for a while playing with different projects before I hit on some activities that I'm actually stoked to be doing and manage to make money on. And maybe this recessions lasts a while. And it's just conservative. So, I'm guessing it won't take that long. But I like knowing that it'd be fine if it does take that long.

Also, there are various approaches to income. This graph is assuming a very stable monthly income, which is unrealistic. Let's just say that's a yearly average income assumption. There's also a world where after taking a year off, I get interested in investing and go back to some form of high-paid work for a period of time (a year?) to build up a stash of money to invest, and then go back to semiERE/whateverthefuck and manage my money, skills, and adventure time however I see fit.

Thoughts? Criticism? Am I nuts? Is there some major financial/economic dynamic I'm not considering?

{kind=link}