An update on my goals:

HEALTH:

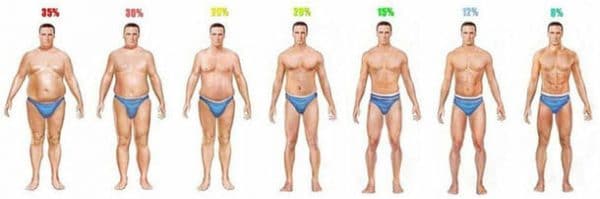

I've been decent at walking and I've followed my regimen to the dot every time I've gone to the gym. I have not averaged 3 times per week, more like 1.5, with a couple of weeks lost due to illnesses. I have to improve in this department, frequency(volume) is the most crucial variable for me. To improve I will plan when to exercise at the start of the week. In general I've seen a decent improvement in body composition. Going by this image:

https://www.healthstatus.com/wp-content ... 00x199.jpg I'm at roughly 15%, down from 20+, with total body weight constant. I seem to have built muscles mainly in my legs and core, reverse disco? My progress has been noticeable, but mediocre, mainly due to low frequency(volume). I feel I am doing the right things, just too little of them. I will start biking to work after the move(see below), upping the light daily exercise a bit.

WORK:

I've become way more independent at work, a necessary transition from a cushy apprenticelike existence that was ultimately very unfulfilling. I've been good at showing up early and have vastly improved my time management, even though I still have a penchant for busywork. I need to work on focus, efficiency and endurance, but I am happy with my progress. Currently I'm quite swamped, hopefully this is transitory.

MENTAL:

I've neglected all of this. At least I'm writing this down. Memento mori happens, though.

SOCIAL:

I've been quite active on the social front, with work, friends and family all. I still strive to develop relationships at work and to up my social skills which are still a bit rough around the edges. My goal is mainly to have a bit smoother interactions, I'm not wired to be a people person but I want to avoid weirdness. If I can manage that, I'll be pleased. A more active social life has helped somewhat, though.

FINANCIAL:

Savings are roughly on target, no major purchases besides some outlays for a planned trip and replacement of a couple of worn out pieces of clothing.

The major event in the financial realm is me having bought an apartment in a

bostadsrättsförening, basically a co-op with a HOA. We found one with low debt, low maintenance, good cash reserves, decent bathroom + kitchen and horrible wallpaper/wall paint within biking distance of both our jobs in a quiet area 20 minutes from downtown, for a decent price. It's a normal size 2-bedroom with an additional small(but very usable) room carved out of the living room, meaning we could raise a family here should the housing market tank, without having to fork out too much extra cash upfront or in monthly fees. We paid 5x net income, which is a lot, but a lot better than I feared. I doubt it'll make us rich, but I feel I can mange the downside. There is some potential specific upside in the exemplary financial state of the co-op(especially since it's likely that new legislation will force real estate agents to advertise debt/square meter and a few other indicators in the prospectus) and in redoing the horrible decor on the cheap. We are thinking about repainting the kitchen cabinets to get a cheap do-over of the kitchen(not more than a few thousand dollars hopefully), since the layout and bones are solid. My goal is to get involved with the co-op, hopefully being able to cut a few costs and influencing the upkeep of the property.

The purchase of course influences my asset allocation. Fixed rate mortgages can only be transfered to a new property under special circumstances, and then only co-op to co-op, not co-op to house. If rates fall, you have to compensate the lender for lost interest if you terminate the mortgage prematurely. Say you get a fixed 10-year and sell after 5. If the rate on a 5-year fixed at that date, + 1 percentage point, is lower than your original 10-year rate, you have to pay the bank the remainder. Eg. original 10-year is 3%, 5-year after 5 years is 1%, then you have to pay 3-(1+1)=1% of the outstanding principal for the remaining five years. In a raising rate environment, the borrower gets no compensation for terminating the mortgage prematurely. Because we'd prefer to move to a house in the medium term, my plan is to go for a 5-year fixed. If we manage our savings rate, and with current assets at almost 2 times net income, that would leave us with 0.5x NI net debt, provided flat returns for our assets. With our student loans, that ratio would be more like 1.5x, but the terms are extremely favourable(current rate 0,34%! and unemployment/illness provisions built in).

We will split our savings 50-50 between principal paydown of the mortgage and investments in securities. Since the mortgage is basically a bond position, and a long one given that I won't pay it down before the term expires, I've excluded bonds from my asset allocation. Since I am massively invested in real estate, I see no reason to overweight REITs, and I've avoided commodities futures in favor of EM. I like gold as a hedge against government/political risk, so it will make up 20% of invested assets. Living in a small, export-oriented country I've decided on a global equity allocation. Currently, basically all of it is in global index funds. I will overweight emerging markets(10% of invested assets), and there's a local mutual fund tracking investment companies(Berkshire, Fairfax etc) to which I will allocate another 10%. I have a few individual stocks I have my eyes on, basically conservatively managed companies which I think have a better shot at surviving the coming storms. 30% of the portfolion will be allocated to 6 stocks at 5% each. I will rebalance if they reach 10% of invested asset value, or if they fall below 2.5% with valuations prohibiting me from increasing my position.

To sum it up:

30% global index(unhedged)

10% emerging markets index(unhegded)

10% investment companies(unhedged)

30% individual stocks(will be mostly large cap, value, likely lower volatility)

20% gold

Basically, the big risk I am taking on is deflation or a massive strengthening of the SEK.

Apart from this we will have 0.5x NI in an emergency fund.

ERUDITION:

Mostly failed, I've been quite bad at keeping up my reading habit, let alone getting started on the other projects(I think I've gotten the gist of J.P so I won't be plowing through all of his lectures). I will decrease time spent on Netflix/blogs and start reading on the tram again(until the move at least).

{kind=link}