I avoid bonds for two reasons, one being my mortgage, which I can prepay in lieu of a bond allocation, the other being extremely low yields in my currency. Americans are getting 3% on the 10-year, we're getting 0.5%, with inflation on par with the US. CDs would be a better option then, you can get 2% on a 5-year or 1.5% on a 2-year. But that's still a real return of 0% or less.

Our bond market is quite underdeveloped for retail investors too, the few funds that exist are a mixed bag of credit quality and maturity. The best "long term" bond fund is a mix of treasuries, munis and mortgage bonds with a weighted maturity of 5 years for example...

Do you have bonds in your portfolio?

Re: Do you have bonds in your portfolio?

I have two bond index funds in my Fidelity IRA, a short term bond index fund (FSBAX) and an intermediate bond index fund (FSITX). I also have a short term brokered CD in my IRA paying 1.95%. I haven't figured out how to buy Treasuries in my IRA.

-

IlliniDave

- Posts: 3869

- Joined: Wed Apr 02, 2014 7:46 pm

Re: Do you have bonds in your portfolio?

ThisDinosaur wrote: ↑Fri Jul 13, 2018 1:05 pm@iDave

But are bonds the best choice for "ballast?" When money is destroyed by tighter credit, cash becomes the rare and valuable asset. All while investable securities are plummeting.

No, stones are, but they don't do much good as an asset.

I'm not familiar with a time when money was destroyed but cash was a rare and valuable asset (seems contradictory). Is that some sort of jargon?

A core holding of intermediate-term US government bonds is pretty stable historically. There may be brief moments in time when cash is marginally more advantageous, but I don't want to surrender all of the opportunity cost over time continually expecting "the big one" to come tomorrow. YMMV.

-

ThisDinosaur

- Posts: 997

- Joined: Fri Jul 17, 2015 9:31 am

Re: Do you have bonds in your portfolio?

@iDave and Mr.I.

"Money is destroyed" isn't a bonfire. Its the effect of rising interest rates in fractional reserve banking.

When QE reverses, the fed sells investment securities into the market. In exchange for dollars from private buyers' accounts. The money is now no longer in circulation, but more securities are. Money is rarer (more valuable) and securities are commoner (less valuable).

Since money is rare, people have less $ to invest. So stock & bond prices drop further with so few buyers. They also have less $ to buy products and services, so corporate earnings drop. Bond prices drop, because the bond supply has increased while demand has dropped. So interest rates are up. Higher interest rates mean its expensive for businesses to borrow money at the same time their earnings are down.

Meanwhile, bond owners trying to sell their bonds take a loss because the few buyers left have higher interest rates available to them.

This is why "cash is king."

"Money is destroyed" isn't a bonfire. Its the effect of rising interest rates in fractional reserve banking.

When QE reverses, the fed sells investment securities into the market. In exchange for dollars from private buyers' accounts. The money is now no longer in circulation, but more securities are. Money is rarer (more valuable) and securities are commoner (less valuable).

Since money is rare, people have less $ to invest. So stock & bond prices drop further with so few buyers. They also have less $ to buy products and services, so corporate earnings drop. Bond prices drop, because the bond supply has increased while demand has dropped. So interest rates are up. Higher interest rates mean its expensive for businesses to borrow money at the same time their earnings are down.

Meanwhile, bond owners trying to sell their bonds take a loss because the few buyers left have higher interest rates available to them.

This is why "cash is king."

-

Mister Imperceptible

- Posts: 1669

- Joined: Fri Nov 10, 2017 4:18 pm

Re: Do you have bonds in your portfolio?

Maybe stones don’t do much good, but what about rounds of .45 Automatic Colt Pistol?IlliniDave wrote: ↑Sat Jul 14, 2018 2:12 pmNo, stones are, but they don't do much good as an asset.

@ThisDinosaur

Yes, that’s my argument. US Bonds and Equities will go down together with the reverse of QE and the rising of rates. Since the 1980’s, US long-term bonds in particular have been a safe haven when stocks do poorly. That will not be the case this time. With record levels of sovereign debt, corporate debt, and household debt, the only escape will be to *eventually* flood the market with an increased money supply. Cash will do well in the short term, because it will be in short supply and can be used to purchase distressed assets. Hard assets will eventually have to do well (in nominal terms- the real long term return of gold and real estate without rent is 0%). Gold and real estate defend against currency devaluation but not in a predictable manner, and usually at different times. I would guess real estate would first take a beating and gold would skyrocket, and later when things stabilize, gold will come crashing down like it did in 1980 and 2011 (but never go back down to where it was before) and real estate will skyrocket to new heights. (Not in real terms of course, but nominal terms- but to people unaware of why this is happening, it’s helps perpetuate the idea that “real estate always goes up.” It’s really that the dollar is going down.)

Of course, you have to factor in supply and demand, and mass psychology. How many people in 2010 and 2011 declared gold a great investment and embraced the Permanent Portfolio, only to see gold crash? How many people in 2018 are chasing after real estate and stocks?

“Be fearful when others are greedy, be greedy when others are fearful.”

-

IlliniDave

- Posts: 3869

- Joined: Wed Apr 02, 2014 7:46 pm

Re: Do you have bonds in your portfolio?

Ah, I see. Well, best wishes with that. For my part, I've never made a penny trying to out maneuver the next transient out there in the investable securities world so I'll happily take my 3.3% and reinvest at higher rates if they do go up further using the interest and return of principal from the bonds. I'm confident that will be more than enough ballast for me and that I'll come out ahead over the next 2-3 decades versus sitting on a pile of cash and trying to make a dramatic reentry in a scenario that may not come to pass. To sort of paraphrase Mark Twain: you pays yer money and you takes yer chances.ThisDinosaur wrote: ↑Sat Jul 14, 2018 2:57 pm@iDave and Mr.I.

Meanwhile, bond owners trying to sell their bonds take a loss because the few buyers left have higher interest rates available to them.

This is why "cash is king."

-

Mister Imperceptible

- Posts: 1669

- Joined: Fri Nov 10, 2017 4:18 pm

Re: Do you have bonds in your portfolio?

I didn’t advocate sitting on a pile of cash. Rather, I’m suggesting to use cash, gold, and conservatively-leveraged rental real estate in a low cost of living area, with a smaller allocation to equities. Something Marc Faber would prescribe, with directly-owned real estate instead of REITs (REITs may very well become correlated with the stock market- in a bear market many things suddenly correlate) minus the bonds.

Like so (another appearance by trusty Tyler9K):

https://gyroscopicinvesting.com/forum/v ... php?t=8296

viewtopic.php?f=9&t=8615&start=340#p170010

Like so (another appearance by trusty Tyler9K):

https://gyroscopicinvesting.com/forum/v ... php?t=8296

viewtopic.php?f=9&t=8615&start=340#p170010

-

IlliniDave

- Posts: 3869

- Joined: Wed Apr 02, 2014 7:46 pm

Re: Do you have bonds in your portfolio?

MI, I get what you are saying. Gold just isn't for me. I do own real estate (unleveraged) equal to to 40% of my invested assets (~28% of overall net worth) but only a small fraction of it is rental. I always have cash (if you count a MM, which I believe is largely very short-term notes versus a deposit account), not so much now (maybe 1.5X expenses) but will likely increase that once I disengage to maybe 2.5X expenses--enough to cover more than half of what I anticipate lifetime withdrawals to be so long as the bottom doesn't drop out in a super-historic way. Maybe my comfort with bonds is rooted in having a lot of financial margin such that moderate short-term or even medium-term losses can be shrugged off. And I just can't kick the growth habit. Playing not to lose would put me in a bad psychological state of mind, which isn't good for an old guy's health.

Re: Do you have bonds in your portfolio?

I have a municipal bond fund in my brokerage account and a TIP fund in my IRA. No bonds in my Roth, HSA, or 401k. About 10% of my total. I also hold REITS, cash, domestic and international equities, utilities, commodities, and an annuity. Domestic equities are the majority of my holdings.

Shotgun approach for me as it's impossible to know what to aim for.

Shotgun approach for me as it's impossible to know what to aim for.

Last edited by OTCW on Sun Jul 15, 2018 1:15 pm, edited 1 time in total.

-

Mister Imperceptible

- Posts: 1669

- Joined: Fri Nov 10, 2017 4:18 pm

Re: Do you have bonds in your portfolio?

@iDave

I’m sure a lot of the comfort level with bonds has to do with investors living their entire investing lives in the Great Bond Bull Market and Plateau without significant correction.

I’m trying for growth too, just how to do so in this bizarro world gets complicated, hence the leveraged real estate. I know JLF loathes mortgages and advises strongly against them, but the companies people own shares of have debt, both standard equities and REITs, so debt somewhere is inescapable and I would rather oversee it myself. I think if you have a cash flush position you can manage it, especially when rates are so near the lower bound. I have over 10 years of mortgage payments in the bank. When I get to 15 or 20, I will start to think about buying a second rental property.

The 30-year-fixed-rate mortgage is one of the greatest wealth building instruments ever, and may not be available forever. I want to take advantage, especially of these low rates. Yes, I am feeding the machine of debt. I did not make the rules. I will short the US Dollar left and right.

I was quite fond of this study posted by @wolf, and what’s of note to me is that the superior risk-adjusted returns from rental real estate identified in this study compared to equities does not even account for leverage:

viewtopic.php?f=3&t=9597

What are the Rothschilds preferred financial instruments? Real estate and gold. I want to emulate them, on a smaller scale.

I’m sure a lot of the comfort level with bonds has to do with investors living their entire investing lives in the Great Bond Bull Market and Plateau without significant correction.

I’m trying for growth too, just how to do so in this bizarro world gets complicated, hence the leveraged real estate. I know JLF loathes mortgages and advises strongly against them, but the companies people own shares of have debt, both standard equities and REITs, so debt somewhere is inescapable and I would rather oversee it myself. I think if you have a cash flush position you can manage it, especially when rates are so near the lower bound. I have over 10 years of mortgage payments in the bank. When I get to 15 or 20, I will start to think about buying a second rental property.

The 30-year-fixed-rate mortgage is one of the greatest wealth building instruments ever, and may not be available forever. I want to take advantage, especially of these low rates. Yes, I am feeding the machine of debt. I did not make the rules. I will short the US Dollar left and right.

I was quite fond of this study posted by @wolf, and what’s of note to me is that the superior risk-adjusted returns from rental real estate identified in this study compared to equities does not even account for leverage:

viewtopic.php?f=3&t=9597

What are the Rothschilds preferred financial instruments? Real estate and gold. I want to emulate them, on a smaller scale.

-

IlliniDave

- Posts: 3869

- Joined: Wed Apr 02, 2014 7:46 pm

Re: Do you have bonds in your portfolio?

MI, sounds cool to me. Hope it works out for you. I'm not trying to evangelize for bonds. The thread started with the OP asking if anyone invests in bonds and if so why, so I responded. And responded a couple times to people challenging my reasoning. If you have a way that feels better to you because this time it's different, that's great. The great thing about investing is that everyone, in theory, can be a winner if their goals are reasonable.

-

Mister Imperceptible

- Posts: 1669

- Joined: Fri Nov 10, 2017 4:18 pm

Re: Do you have bonds in your portfolio?

@iDave

I’m not being even remotely hostile or trying to dog you. (Maybe I need to take cues from Riggerjack about modifying my methods of communication.) I started by saying my allocation to bonds was 0%. And in answering each you and ThisDino, my current investment strategy came out. It’s food for thought, and I would love to hear alternatives to my current strategy.

My opinion today is my opinion today. It is not sacrosanct and I am sure I will modify it when I get more data.

I’m not being even remotely hostile or trying to dog you. (Maybe I need to take cues from Riggerjack about modifying my methods of communication.) I started by saying my allocation to bonds was 0%. And in answering each you and ThisDino, my current investment strategy came out. It’s food for thought, and I would love to hear alternatives to my current strategy.

My opinion today is my opinion today. It is not sacrosanct and I am sure I will modify it when I get more data.

Re: Do you have bonds in your portfolio?

This back and forth is a great example of why I love this board.

Two intelligent people politely exchanging points of view.

I (we?) gain nothing from monotonous opinions, so please nobody be discouraged to exchange because of the mostly pointless fear of offending each other.

Most people here are polite adults with enough self confidence: we can disagree without feeling triggered/disrespected.

Thanks to both for the exchange and keep expressing your valuable opinions.

I'll try do so when I feel I have something to say

Two intelligent people politely exchanging points of view.

I (we?) gain nothing from monotonous opinions, so please nobody be discouraged to exchange because of the mostly pointless fear of offending each other.

Most people here are polite adults with enough self confidence: we can disagree without feeling triggered/disrespected.

Thanks to both for the exchange and keep expressing your valuable opinions.

I'll try do so when I feel I have something to say

-

suomalainen

- Posts: 988

- Joined: Sat Oct 18, 2014 12:49 pm

Re: Do you have bonds in your portfolio?

I don’t have bonds in my portfolio per se. At least no publicly traded bonds, whether government or corporate. I do hold private notes (like bonds but with covenants) via a stable value fund through my 401k. As I’m in the industry, I’m very comfortable with the asset class, and I like that the fund is not marked to market. In other words, if interest rates rise, the price of my private bonds stays flat, so no capital losses. On the flip side, no gains either were rates to fall. In that sense it functions like a CD but with a more diverse asset/credit base than simply one bank. In that sense, the opportunity cost is quite low. If rates rise, I could shift into a high yield or investment grade bond fund also available in the 401k. The rub is that there are trading restrictions, so if you are too active, they will freeze your asset allocation until you promise to calm down. Yielding 3% currently, I think, which is a pretty good yield on a cash-like instrument with no real duration risk. Something like 37% of my investable assets are in that. The rest in cash and stocks. Real estate is too much hassle, but I have some exposure via reits.

Re: the @MI and @ID exchange, I can see both sides. There is no one right answer given personal preferences, risk tolerances, horizons, liability matching, etc. You can bet life insurance companies are perfectly comfortable with their extremely heavy bond and mortgage allocations, since they are liability matching and have another lever by adjusting pricing on the policy sale side. There’s room in the market for everyone to get what they want out of their investments because not everyone wants the same thing.

Re: the @MI and @ID exchange, I can see both sides. There is no one right answer given personal preferences, risk tolerances, horizons, liability matching, etc. You can bet life insurance companies are perfectly comfortable with their extremely heavy bond and mortgage allocations, since they are liability matching and have another lever by adjusting pricing on the policy sale side. There’s room in the market for everyone to get what they want out of their investments because not everyone wants the same thing.

-

OrganicRain

- Posts: 32

- Joined: Sun Oct 19, 2014 6:20 pm

Re: Do you have bonds in your portfolio?

I am about to ER and recently added more bonds in my portfolio via an aggregate bond etf. With that I am now at 60/40 allocation.

-

ThisDinosaur

- Posts: 997

- Joined: Fri Jul 17, 2015 9:31 am

Re: Do you have bonds in your portfolio?

As a general rule, if I ever come off as combative, it is only to entice someone to show me where my thinking is wrong. If I tell you that you are wrong about bonds, I'm hoping you will tell me some new piece of information or reasoning that I don't have. I'd much rather be earing a return than sitting on a pile of inert cash.

Example:

Treasury Bond Principal + Interest is always > or = to Cash

Is this true?

Example:

Treasury Bond Principal + Interest is always > or = to Cash

Is this true?

-

Kriegsspiel

- Posts: 952

- Joined: Fri Aug 03, 2012 9:05 pm

Re: Do you have bonds in your portfolio?

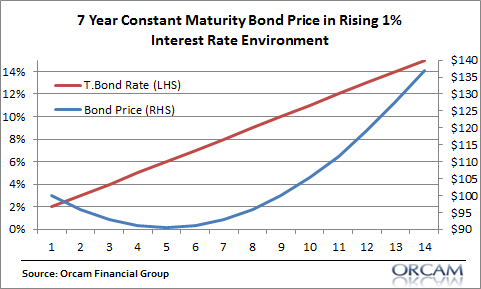

No. Depending on the duration of the bond, it could underperform cash if interest rates rise.ThisDinosaur wrote: ↑Tue Jul 17, 2018 6:59 amTreasury Bond Principal + Interest is always > or = to Cash

Is this true?

For instance:

At the same time as this 7 year duration fund is going down, a 1 year duration fund would be reaping the yearly increases in interest rates because it's principal isn't dropping as much.

The article that chart comes from explains it.

-

Mister Imperceptible

- Posts: 1669

- Joined: Fri Nov 10, 2017 4:18 pm

Re: Do you have bonds in your portfolio?

The only way the inverse could be true would be with an even more massive bout of QE that would drive rates even lower. So you would get a nice one-time capital gain from that if you sell you bonds paying 3% if we end up with Europe or Japan like rates at 1%. But it would be just that, a one-time gain. Who is going to buy 30-year bonds at 0%? Unless the government starts taxing you on deposits and forces you into debt (enslavement) or the purchase of ubertoxic zombie equities.

In such a scenario, the currency will take a beating. Gold, ammunition, solar panels, and other things that are real should far outperform bonds in USD nominal terms.

Real estate is tricky. It would take a beating at first as indebted investors need to sell and overleveraged homeowners are foreclosured on. But as the currency erodes and the government prints money to paper over debts, real estate in places where the economy is robust will *eventually* bounce back in nominal terms. The time it takes to bounce back should be anywhere between 3 and 50 years. Hopefully you are collecting inflation-adjusted rent in the meantime.

In such a scenario, the currency will take a beating. Gold, ammunition, solar panels, and other things that are real should far outperform bonds in USD nominal terms.

Real estate is tricky. It would take a beating at first as indebted investors need to sell and overleveraged homeowners are foreclosured on. But as the currency erodes and the government prints money to paper over debts, real estate in places where the economy is robust will *eventually* bounce back in nominal terms. The time it takes to bounce back should be anywhere between 3 and 50 years. Hopefully you are collecting inflation-adjusted rent in the meantime.

Last edited by Mister Imperceptible on Tue Jul 17, 2018 9:22 am, edited 1 time in total.

-

Mister Imperceptible

- Posts: 1669

- Joined: Fri Nov 10, 2017 4:18 pm

Re: Do you have bonds in your portfolio?

@Kriegsspiel

The author in that article is cheating on his statistics because he is comparing bonds to a 0% bearing cash instrument. See the link to the flat yield curve I posted above.

In the rising rate environment of the 1970’s, T-bills far outperformed long term bonds.

https://portfoliocharts.com/portfolio/bil/

https://portfoliocharts.com/portfolio/ltb/

For comparison, see the 1970’s results for gold and REITs:

https://portfoliocharts.com/portfolio/gld/

https://portfoliocharts.com/portfolio/reit/

No, it won’t happen exactly the same way, but maybe we have a general idea.

The author in that article is cheating on his statistics because he is comparing bonds to a 0% bearing cash instrument. See the link to the flat yield curve I posted above.

In the rising rate environment of the 1970’s, T-bills far outperformed long term bonds.

https://portfoliocharts.com/portfolio/bil/

https://portfoliocharts.com/portfolio/ltb/

For comparison, see the 1970’s results for gold and REITs:

https://portfoliocharts.com/portfolio/gld/

https://portfoliocharts.com/portfolio/reit/

No, it won’t happen exactly the same way, but maybe we have a general idea.

-

ThisDinosaur

- Posts: 997

- Joined: Fri Jul 17, 2015 9:31 am

Re: Do you have bonds in your portfolio?

@Kriegsspiel

From that article.

you start with equal amounts of cash, short term bonds, and long term bonds. Reinvest all dividends into same asset.

Rates rise over the next several years. Here's what happens:

Cash fund's nominal value stays the same.

Short term bond account nominal value increases. (Minimal loss of principal. Interest yield increasing.)

Long term bond account nominal value initially drops, then rises as interest yield overtakes the drop in principal value.

At the end of the period, the nominal value of all three accounts are long term bond > short term bond > cash account.

We're only comparing "nominal" returns because we are discussing cash vs. bonds. If inflation is high enough, all three will lose purchasing power.

So here's why I'm arguing for cash instead of bonds in a portfolio.

Accumulation phase, rates rise:

Bonds and stocks will decrease in value at the same time. If your portfolio is cash + stocks, you rebalance and buy stocks cheap. If your portfolio is bonds + stocks, they are both down and you get very little from rebalancing.

Distribution phase, rates rise:

Bonds and stocks decrease in value at the same time. If your portfolio is cash + stocks, you have spending money AND can buy stocks cheap. If your portfolio is bonds + stocks, they are both down and you need to reduce spending or your nest egg will take a sequence-of-return hit.

If rates decrease, then stocks, bonds, and gold will all go up. But bonds will rarely go up more than stocks (prosperity) or gold (inflation). Cash's purchasing power goes down here, so its anti-correlated. You rebalance in anticipation of the next rate hike.

I'm arguing that cash is the best diversifier of the other three. Bonds are just watered down stocks wrt how they respond to interest rate changes.

From that article.

This is the scenario;Yes, if rates rise sharply you’ll almost certainly lose purchasing power in your bonds, however, you will also earn a nominal return better than cash if held to maturity

you start with equal amounts of cash, short term bonds, and long term bonds. Reinvest all dividends into same asset.

Rates rise over the next several years. Here's what happens:

Cash fund's nominal value stays the same.

Short term bond account nominal value increases. (Minimal loss of principal. Interest yield increasing.)

Long term bond account nominal value initially drops, then rises as interest yield overtakes the drop in principal value.

At the end of the period, the nominal value of all three accounts are long term bond > short term bond > cash account.

We're only comparing "nominal" returns because we are discussing cash vs. bonds. If inflation is high enough, all three will lose purchasing power.

So here's why I'm arguing for cash instead of bonds in a portfolio.

Accumulation phase, rates rise:

Bonds and stocks will decrease in value at the same time. If your portfolio is cash + stocks, you rebalance and buy stocks cheap. If your portfolio is bonds + stocks, they are both down and you get very little from rebalancing.

Distribution phase, rates rise:

Bonds and stocks decrease in value at the same time. If your portfolio is cash + stocks, you have spending money AND can buy stocks cheap. If your portfolio is bonds + stocks, they are both down and you need to reduce spending or your nest egg will take a sequence-of-return hit.

If rates decrease, then stocks, bonds, and gold will all go up. But bonds will rarely go up more than stocks (prosperity) or gold (inflation). Cash's purchasing power goes down here, so its anti-correlated. You rebalance in anticipation of the next rate hike.

I'm arguing that cash is the best diversifier of the other three. Bonds are just watered down stocks wrt how they respond to interest rate changes.