Necessary Expenses

$890 - Rent

$57 - Cell Phone

$304 - Food

$123 - Gas

$18 - Kitchen/Toiletries

$174 - Car Maitenance

$7 - Toll

$43 - Supplements

$936 Personal

$12,539 Taxes

$15,091

Discretionary Expenses

$317 - Restraunts

$130 - Entertainment

$54 - Clothes

$55 - Books

$2,237 - Sports/Gym

$36 - Coffee

$2,828

Total Expenses = $17,917

Restaurant - No Comment

Personal - I'm in the process of making significant changes to my life. One of my focus areas is to remove any clutter or items that don't bring me value. My current mattress needs to be replaced. Instead of purchasing another western style bed, I've decided to purchase a Shikibuton from Japan. Over the next couple of weeks, I'll be selling or throwing out my bedframe, nightstands, and other unnecessary items in my room. Before/after photos coming soon...

Taxes - I was expecting this to be high since I haven't paid any taxes on my side hustle profits.

Gym - I canceled my gym membership and instead purchased a Keiser M series exercise bike. I only used the gym for cardio because of the constant cold weather and rain here in the NW. This was not a cheap purchase, but I will now be able to do cardio in my home along with my yoga and body weight workouts.

January Income

$2,821 - After-Tax Salary

$7,105 - 401K+ Match

$1,129 - Bonus

$35 - AMZ Book

Total Income = $11,091

I received a $4,500 bonus due to my companies performance last year. I dumped it into my 401K so I can take advantage of the Backdoor Mega Roth at the end of the year.

I'm still surprised everytime I get any money for this horribly done kindle book I have on Amazon. I used this book as a test to learn the Kindle process over a year ago and it still produces a small amount of income.

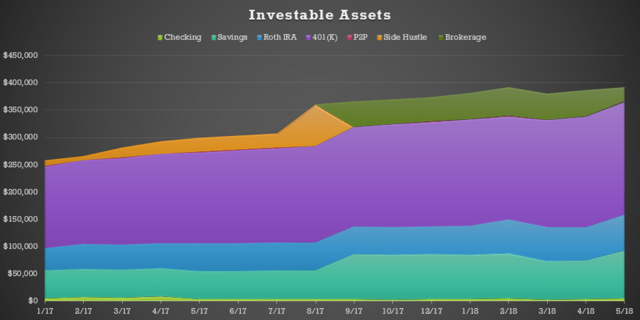

Investable Assets Breakdown

$2482 - Checking

$71,354 - Saving

$61,929 - Roth IRA

$196,200 - 401K

$228 - P2P

46,926 -Brokerage

$150 - Other

$379,274

My assets decreased this month for three main reasons. The value of my gold stocks went down, paying my taxes, and two large purchases.

I've been making a mistake the past 4 years with Capital One. My savings has been sitting in their 360 Savings paying 1% interest which I thought was good. I recently found that their Money Market account pays 1.5% for amounts over $10,000. I made the switch for the fee .5% monthly interest.

Summary

Total Income = $11,090

Total Expenses = $17,919

Investable Assets = $379,274

Savings Rate = Negative

SWR = 56.69%

I really feel like this will be the last expensive month of the year. I see no other obstacles in the near future in terms of expenses. My average spending last year was $2,900, there's no reason why I can't spend below 2,000 going forward.

Wad's Journal

Re: Wad's Journal

Last edited by Wads on Sun Jul 22, 2018 1:51 pm, edited 1 time in total.

Re: Wad's Journal

Necessary Expenses

$890 - Rent

$57 - Cell Phone

$215 - Food

$122 - Gas

$21 - Kitchen/Toiletries

$150 - Home Maitenance

$15 - Supplements

$94 - Personal

$1564

Discretionary Expenses

$385 - Restaurants

$948 - Entertainment

$158 - Shopping

$126 - Books

$83 - Sports/Gym

$29 - Coffee

$1,729

Total Epenses= $3,293

Restaurants ($385) - This has been a major issue for me. I can no longer act on these false signals im getting to eat unhealthy foods. I must recognize where the signal is coming from (animal or rational brain) and act accordingly. I will eat 99% of meals at home next month.

March Income

$6,658 - After-Tax Salary

$3,405 - 401K+ Match

$1,202 - Bonus

$25 - AMZ Book

Total Income = $11,290

- March was a three paycheck month resulting in higher income than normal.

Investable Assets

$74,926- Cash

$62,004 - Roth IRA

$201,205 - 401K

$2230 - P2P

$47,566 -Brokerage

$25 - Other

Total= $385,956

- Not much has changed. I don't like the fact that I have so much cash on hand but feel its best at this time

- I decided value investing is not for me and will go with index funds in the future. I feel I will have better results in the long-term going this route.

April Goals

1- Eat 99% of meals at home

- Reducing these expenses will significantly reduce the amount of money needed for FI.

Monthly Summary

Total Income = $11,290

Total Expenses = $3,293

Investable Assets = $385,956

Savings Rate = 71%

SWR = 10%

- I'm not happy with how high my expenses are. I know why they are so high and will make the changes necessary to get them lower.

$890 - Rent

$57 - Cell Phone

$215 - Food

$122 - Gas

$21 - Kitchen/Toiletries

$150 - Home Maitenance

$15 - Supplements

$94 - Personal

$1564

Discretionary Expenses

$385 - Restaurants

$948 - Entertainment

$158 - Shopping

$126 - Books

$83 - Sports/Gym

$29 - Coffee

$1,729

Total Epenses= $3,293

Restaurants ($385) - This has been a major issue for me. I can no longer act on these false signals im getting to eat unhealthy foods. I must recognize where the signal is coming from (animal or rational brain) and act accordingly. I will eat 99% of meals at home next month.

March Income

$6,658 - After-Tax Salary

$3,405 - 401K+ Match

$1,202 - Bonus

$25 - AMZ Book

Total Income = $11,290

- March was a three paycheck month resulting in higher income than normal.

Investable Assets

$74,926- Cash

$62,004 - Roth IRA

$201,205 - 401K

$2230 - P2P

$47,566 -Brokerage

$25 - Other

Total= $385,956

- Not much has changed. I don't like the fact that I have so much cash on hand but feel its best at this time

- I decided value investing is not for me and will go with index funds in the future. I feel I will have better results in the long-term going this route.

April Goals

1- Eat 99% of meals at home

- Reducing these expenses will significantly reduce the amount of money needed for FI.

Monthly Summary

Total Income = $11,290

Total Expenses = $3,293

Investable Assets = $385,956

Savings Rate = 71%

SWR = 10%

- I'm not happy with how high my expenses are. I know why they are so high and will make the changes necessary to get them lower.

Last edited by Wads on Sun Jan 13, 2019 11:29 pm, edited 3 times in total.

Re: Wad's Journal

The Shikibuton was lost during transit. The shipping service declared the package lost two days ago so the futon company just shipped the replacement. They wanted to make sure they got their insurance claim settled before shipping a new one.

I did donate my bed set, book shelf, and couch to the salvation army. I've been sleeping on the floor with blankets for the past couple of weeks. It took a couple of nights to adjust but I like it now. My bedroom is completely empty and I like the open feeling.

I did donate my bed set, book shelf, and couch to the salvation army. I've been sleeping on the floor with blankets for the past couple of weeks. It took a couple of nights to adjust but I like it now. My bedroom is completely empty and I like the open feeling.

Re: Wad's Journal

But then you don't even need the futon any longer?

Re: Wad's Journal

Yes and no.

It's not needed but it does make sleeping much more comfortable. I did think about canceling the order but at the end of the day, I wanted to try the futon. It's been three weeks now and Im glad I made the switch from traditional bedding.

It's not needed but it does make sleeping much more comfortable. I did think about canceling the order but at the end of the day, I wanted to try the futon. It's been three weeks now and Im glad I made the switch from traditional bedding.

Re: Wad's Journal

Expenses

Necessary

$890 - Rent

$57 - Cell Phone

$282 - Food

$121 - Gas

$7 - Kitchen/Toiletries

$34 - Personal

$1,391

Discretionary

$166 - Restaurants

$200 - Entertainment

$158 - Shopping

$171 - Books

$36 - Sports/Gym

$45 - Coffee

$7 - Toll

$625

Total Expenses = $2,016

I am moving in the right direction overall but still have many areas I need to work on. I can easily (with discipline) cut down an additional $500 from my spending which will put me on at my target of $1,500 per month.

Income

March Income

$3,334 - After-Tax Salary

$2,351 - 401K+ Match

$654 - Bonus

$29 - AMZ Book

Total Income = $6,351

As expected. I did work some overtime this month so I will have an increase of income in next months update.

Assets

Investable Assets Breakdown

$92,324 - Cash

$67,587 - Roth IRA

$204,670 - 401K

$130 - P2P

$25,968 -Brokerage

$29 - Other

Total Assets = $390,708

As expected.

Monthly Breakdown

Total Income = $6,351

Total Expenses = $2,016

Investable Assets = $390,708

Savings Rate = 68%

SWR = 6.19%

Necessary

$890 - Rent

$57 - Cell Phone

$282 - Food

$121 - Gas

$7 - Kitchen/Toiletries

$34 - Personal

$1,391

Discretionary

$166 - Restaurants

$200 - Entertainment

$158 - Shopping

$171 - Books

$36 - Sports/Gym

$45 - Coffee

$7 - Toll

$625

Total Expenses = $2,016

I am moving in the right direction overall but still have many areas I need to work on. I can easily (with discipline) cut down an additional $500 from my spending which will put me on at my target of $1,500 per month.

Income

March Income

$3,334 - After-Tax Salary

$2,351 - 401K+ Match

$654 - Bonus

$29 - AMZ Book

Total Income = $6,351

As expected. I did work some overtime this month so I will have an increase of income in next months update.

Assets

Investable Assets Breakdown

$92,324 - Cash

$67,587 - Roth IRA

$204,670 - 401K

$130 - P2P

$25,968 -Brokerage

$29 - Other

Total Assets = $390,708

As expected.

Monthly Breakdown

Total Income = $6,351

Total Expenses = $2,016

Investable Assets = $390,708

Savings Rate = 68%

SWR = 6.19%

Re: Wad's Journal

2018 Update

Saving Rate: 56%

NW: $424,000

SWR: 5.6%

Portfolio Breakdown

90% of my assets are in fixed income averaging 2-3%. I've been waiting patiently to get this money into equities and believe an opportunity will finally come in the next 12 or so months. This past year my investing philosophy has changed. For many years I believed that a stock/bond portfolio would be good enough but Portfolio charts made me reconsider this mindset.

Side Hustles

I am no longer pursuing side hustles. I feel like I was using side hustles to form some kind of identity for myself. My income is not the issue, it's my spending. I need to focus on cutting expenses which will pay a lifetime of dividends. One of my goals for 2019 is to use my free time on more fulfilling activities. I always enjoyed working with kids when I coached sports. Im considering mentoring a kid in the Big Brother Foundation this year and see if that is something that will interest me in the future.

Random

I no longer have a cell phone provider. I use google voice for free and love it. I also cut my own hair which looks just as good as the $20 cuts I used to purchase.

FIRE

My original plan was to FIRE asap but this has also changed. I've found that it's not that I dislike my job but rather simply don't like the fact that I have limited control over my situation. FI will give me peace of mind that Im in control and have options, which is what im really seeking. It's possible that once I have achieved FI I may still work for some time. With that said im only 32 and don't see myself working past the age of 40. FIRE will eventually come, but its no longer my priority.

FI Goal

1) Paid off house/condo (I would like to purchase something around $100,000)

2) 600K Invested

I believe I can achieve this in about 5 years. This would provide more than enough and give me unlimited options in my future.

Saving Rate: 56%

NW: $424,000

SWR: 5.6%

Portfolio Breakdown

90% of my assets are in fixed income averaging 2-3%. I've been waiting patiently to get this money into equities and believe an opportunity will finally come in the next 12 or so months. This past year my investing philosophy has changed. For many years I believed that a stock/bond portfolio would be good enough but Portfolio charts made me reconsider this mindset.

Side Hustles

I am no longer pursuing side hustles. I feel like I was using side hustles to form some kind of identity for myself. My income is not the issue, it's my spending. I need to focus on cutting expenses which will pay a lifetime of dividends. One of my goals for 2019 is to use my free time on more fulfilling activities. I always enjoyed working with kids when I coached sports. Im considering mentoring a kid in the Big Brother Foundation this year and see if that is something that will interest me in the future.

Random

I no longer have a cell phone provider. I use google voice for free and love it. I also cut my own hair which looks just as good as the $20 cuts I used to purchase.

FIRE

My original plan was to FIRE asap but this has also changed. I've found that it's not that I dislike my job but rather simply don't like the fact that I have limited control over my situation. FI will give me peace of mind that Im in control and have options, which is what im really seeking. It's possible that once I have achieved FI I may still work for some time. With that said im only 32 and don't see myself working past the age of 40. FIRE will eventually come, but its no longer my priority.

FI Goal

1) Paid off house/condo (I would like to purchase something around $100,000)

2) 600K Invested

I believe I can achieve this in about 5 years. This would provide more than enough and give me unlimited options in my future.

Last edited by Wads on Mon Oct 28, 2019 1:45 pm, edited 1 time in total.

-

classical_Liberal

- Posts: 2283

- Joined: Sun Mar 20, 2016 6:05 am

Re: Wad's Journal

At the rate you're going, it should be much less than 5 years. Congrats!

I think you are very wise to look at the big picture (ie the why of FI), before reaching your goals. I have been planning a semi-ERE for awhile now. I passed my original financial marker early last year, then reset goal higher and have now reached it as well. Still, I do not feel ready because I've let other important parts of my life lapse. I do not think FI or Semi-ERE will be a cure-all for what ails me. A wise forum member commented in my journal something to the effect, "money doesn't make you free, you make you free". So 2019 has become OMY, more to learn and understand that comment, than for accumulation of financial assets.

Much like you, I plan to work more in my life as it's a value added activity in ways outside of the income, but want to be free as possible wrt the whens and hows. You've reached a point of FU money where you should be able to leverage it to make your work even more enjoyable, so don't be afraid to use said leverage if you think it'll make life more fulfilling.

I think you are very wise to look at the big picture (ie the why of FI), before reaching your goals. I have been planning a semi-ERE for awhile now. I passed my original financial marker early last year, then reset goal higher and have now reached it as well. Still, I do not feel ready because I've let other important parts of my life lapse. I do not think FI or Semi-ERE will be a cure-all for what ails me. A wise forum member commented in my journal something to the effect, "money doesn't make you free, you make you free". So 2019 has become OMY, more to learn and understand that comment, than for accumulation of financial assets.

Much like you, I plan to work more in my life as it's a value added activity in ways outside of the income, but want to be free as possible wrt the whens and hows. You've reached a point of FU money where you should be able to leverage it to make your work even more enjoyable, so don't be afraid to use said leverage if you think it'll make life more fulfilling.

Re: Wad's Journal

2019 Update

Saving Rate: 63%

NW: $500,060

Portfolio Breakdown

I still have 90% of my assets in fixed income and 10% in gold. I've missed out on most of the gains in the S&P the last couple of years but I have no regrets. I'm in no hurry to FIRE and believe I will have a better opportunity in the future than to buy at these valuations. I understand that this massive bull run may continue for many years but I'm ok with that.

SE Asia

One major change for me this year was the realization that I have no desire to own a home/condo. I am seriously considering moving overseas when I decide to FIRE. There are many pros and cons to such a big move but overall I feel like that lifestyle will fit better with my personality and goals. I convinced my landlord to accept CC payment as rent so now I can start taking advantage of sign up reward points. I plan on making a free trip to SE Asia in 3-4 years as a scouting trip looking at possible FIRE destinations.

Margin of Safety

I plan on having a large margin of safety because I know with only an HS diploma I won't be able to make anywhere near as much money as Im making now once I leave the workforce. 1 million is the end goal. I always prefer to look at the downside risk. In a bad scenario, I would expect my portfolio to drop 40% leaving me with $600,000. At his level, I will still be able to live comfortably on $1,500 - $2,000 each month. With this amount of safety, I will be able to sleep well at night.

Saving Rate: 63%

NW: $500,060

Portfolio Breakdown

I still have 90% of my assets in fixed income and 10% in gold. I've missed out on most of the gains in the S&P the last couple of years but I have no regrets. I'm in no hurry to FIRE and believe I will have a better opportunity in the future than to buy at these valuations. I understand that this massive bull run may continue for many years but I'm ok with that.

SE Asia

One major change for me this year was the realization that I have no desire to own a home/condo. I am seriously considering moving overseas when I decide to FIRE. There are many pros and cons to such a big move but overall I feel like that lifestyle will fit better with my personality and goals. I convinced my landlord to accept CC payment as rent so now I can start taking advantage of sign up reward points. I plan on making a free trip to SE Asia in 3-4 years as a scouting trip looking at possible FIRE destinations.

Margin of Safety

I plan on having a large margin of safety because I know with only an HS diploma I won't be able to make anywhere near as much money as Im making now once I leave the workforce. 1 million is the end goal. I always prefer to look at the downside risk. In a bad scenario, I would expect my portfolio to drop 40% leaving me with $600,000. At his level, I will still be able to live comfortably on $1,500 - $2,000 each month. With this amount of safety, I will be able to sleep well at night.

Re: Wad's Journal

Hello Wads, I always love reading of someone who's killing it and doesn't fall into a standard white-collar massive-income field. I'm a plumber so not really that similar to aerospace mechanic, but perhaps extremely similar when juxtaposed to an office job.

I have a cousin close to graduating high school who wants to be a mechanic. He's really into cars, of course, but my common understanding is mechanics in specialized fields, such as yourself, earn more than say a Mercedes mechanic, which is his current direction of choice. Do you any have quick advice or insights I could give to someone in his situation?

I have a cousin close to graduating high school who wants to be a mechanic. He's really into cars, of course, but my common understanding is mechanics in specialized fields, such as yourself, earn more than say a Mercedes mechanic, which is his current direction of choice. Do you any have quick advice or insights I could give to someone in his situation?

Re: Wad's Journal

I'm not sure I can provide any insights or advice for your cousin. I know a couple of guys who went to those Auto mechanic institutes with the same desire to work at Mercedes/Lexus/BMW. They found that its a very competitive niche and ended up at low-end dealerships with little pay.

For my situation, the key was hiring onto a large company with a strong union at 18. If I were to do the same job outside of my union, my pay would be around $20-$25/hr which is about 50% less than my current base salary and the working conditions would be horrible. In addition to wages, we get great health care, 401K matches, defined pension benefit, and severance if I were to get laid off. None of this is available outside of my company to those in the same field. To be honest, I got lucky.

So I guess my advice to anyone who doesn't want to pursue college would be to find a union job. There are still many good ones out there. Here is the benefits of a good union. This is a breakdown of my salary from the first 6 years at the job from age 18-24.

2006 - $41,458

2007 - $41,851

2008 - $41,523

2009 - $50,713

2010 - $55,034

2011 - $64,285

2012 - $127,000 < Lots of OT

For my situation, the key was hiring onto a large company with a strong union at 18. If I were to do the same job outside of my union, my pay would be around $20-$25/hr which is about 50% less than my current base salary and the working conditions would be horrible. In addition to wages, we get great health care, 401K matches, defined pension benefit, and severance if I were to get laid off. None of this is available outside of my company to those in the same field. To be honest, I got lucky.

So I guess my advice to anyone who doesn't want to pursue college would be to find a union job. There are still many good ones out there. Here is the benefits of a good union. This is a breakdown of my salary from the first 6 years at the job from age 18-24.

2006 - $41,458

2007 - $41,851

2008 - $41,523

2009 - $50,713

2010 - $55,034

2011 - $64,285

2012 - $127,000 < Lots of OT

Re: Wad's Journal

Thanks for confirming my general understanding of the field. He's got his sights pretty set on a particular Mercedes school right now, but still has a little bit to make up his mind. As many good critiques there are of unions as organizations the good ones really are great for the workers. There's no way I'd be plumbing if I wasn't making union scale. I'll be looking into mechanic union information for his area and passing it on, thank you.

Re: Wad's Journal

2020 Update

Age:33

Savings Rate:52%

NW:$662,000 (Increase from $500K on 1/1/20)

Portfolio Breakdown (60/30/10)

S&P500 - 25%

VXUS - 18%

VTV - 11%

BRK.b - 5%

SRG - 2%

Gold - 9%

Stable Value - 15%

Money Market - 15%

After many years of waiting on the sideline, I finally had an opportunity to purchase stocks during the march downturn. I currently have a value tilt in my equity position. I did purchase two individual stocks (BRK.B @ $178 & recently Seritage Growth Properties @ $12.8). I like how I'm currently positioned. I still hold gold and lots of cash. I have enough offense to reap the rewards if this crazy market continues but also have enough defense to take advantage of a significant correction.

SE Asia

Made good progress this year with reward points. I believe I have enough for a free trip to Asia in search of my future Homebase. I've been watching lots of youtube channels learning from expats who have made similar moves. One of my favorites is Nomad Capitalist.

Health & Fitness

I've been hitting the gym three days a week since October. I'm finally starting to see the work payoff. I have found that fitness has really improved my mental health. At this pace, I believe I will be in the best shape of my life within the next 3-6 months.

Expenses

I still have work to do. I'm going to make a change this year to make sure I hit my spending goal. My goal is $2,000 or less monthly. My fixed cost are $1,600. I will now take out $400 cash each month to use towards discretionary spending. I can use it however I wish, but once it's gone I'm done.

Personal

I find myself still searching for something else to fill my time. Reading, exercise, cooking, and watching documentaries/youtube/sports isn't cutting it. I do golf with friends when the weather is good but I need something else. This is a concern for me going forward. I think dating/having a GF would fill the void but I have no desire to date a western woman so that must wait until I leave for Asia. It's not that I dislike American women, but I do not agree with our Family Law system and think it is significantly flawed.

I hope you all have a happy and healthy 2021!

Age:33

Savings Rate:52%

NW:$662,000 (Increase from $500K on 1/1/20)

Portfolio Breakdown (60/30/10)

S&P500 - 25%

VXUS - 18%

VTV - 11%

BRK.b - 5%

SRG - 2%

Gold - 9%

Stable Value - 15%

Money Market - 15%

After many years of waiting on the sideline, I finally had an opportunity to purchase stocks during the march downturn. I currently have a value tilt in my equity position. I did purchase two individual stocks (BRK.B @ $178 & recently Seritage Growth Properties @ $12.8). I like how I'm currently positioned. I still hold gold and lots of cash. I have enough offense to reap the rewards if this crazy market continues but also have enough defense to take advantage of a significant correction.

SE Asia

Made good progress this year with reward points. I believe I have enough for a free trip to Asia in search of my future Homebase. I've been watching lots of youtube channels learning from expats who have made similar moves. One of my favorites is Nomad Capitalist.

Health & Fitness

I've been hitting the gym three days a week since October. I'm finally starting to see the work payoff. I have found that fitness has really improved my mental health. At this pace, I believe I will be in the best shape of my life within the next 3-6 months.

Expenses

I still have work to do. I'm going to make a change this year to make sure I hit my spending goal. My goal is $2,000 or less monthly. My fixed cost are $1,600. I will now take out $400 cash each month to use towards discretionary spending. I can use it however I wish, but once it's gone I'm done.

Personal

I find myself still searching for something else to fill my time. Reading, exercise, cooking, and watching documentaries/youtube/sports isn't cutting it. I do golf with friends when the weather is good but I need something else. This is a concern for me going forward. I think dating/having a GF would fill the void but I have no desire to date a western woman so that must wait until I leave for Asia. It's not that I dislike American women, but I do not agree with our Family Law system and think it is significantly flawed.

I hope you all have a happy and healthy 2021!

Re: Wad's Journal

2021 Update

Age:34

Savings Rate:36% (down from 52%)

NW:$783,000 (Increase from $662K on 1/1/21)

Portfolio Breakdown (60/30/10)

S&P500 - 40%

BRK.b - 20%

Gold - 10%

Stable Value - 20%

Money Market - 10%

- I'm moving some of my emergency funds into I-bonds. I purchased $10,000 last year and another $10,000 today at 7.12%.

SE Asia

- Still plan on moving overseas. Once covid issues decline I'll start my initial visits looking for a new "home".

Health & Fitness

- My gym routine has continued throughout 2021. For myself, having a solid morning routine sets the foundation for the day. Working out has had a huge impact on my life. I feel so much better and confident. For the first time in my life, I'm actually proud of the person I look at in the mirror.

Expenses

- My expenses increased this year. I'm not concerned because I know it was due to wasteful spending and being lazy. Sometimes I feel like the higher my NW goes, the less I care about FIRE. I lose focus often, but the good news is I'm more focused on activities I find fulfilling and not the FIRE number.

Life is good right now and I have no complaints. I hope you all have a happy and healthy 2022!

Age:34

Savings Rate:36% (down from 52%)

NW:$783,000 (Increase from $662K on 1/1/21)

Portfolio Breakdown (60/30/10)

S&P500 - 40%

BRK.b - 20%

Gold - 10%

Stable Value - 20%

Money Market - 10%

- I'm moving some of my emergency funds into I-bonds. I purchased $10,000 last year and another $10,000 today at 7.12%.

SE Asia

- Still plan on moving overseas. Once covid issues decline I'll start my initial visits looking for a new "home".

Health & Fitness

- My gym routine has continued throughout 2021. For myself, having a solid morning routine sets the foundation for the day. Working out has had a huge impact on my life. I feel so much better and confident. For the first time in my life, I'm actually proud of the person I look at in the mirror.

Expenses

- My expenses increased this year. I'm not concerned because I know it was due to wasteful spending and being lazy. Sometimes I feel like the higher my NW goes, the less I care about FIRE. I lose focus often, but the good news is I'm more focused on activities I find fulfilling and not the FIRE number.

Life is good right now and I have no complaints. I hope you all have a happy and healthy 2022!