Page 5 of 11

Monthly update #23: May 2017

Posted: Thu Jun 08, 2017 2:40 pm

by singvestor

Worst things first:

Monthly goal review:

- 20+ days no alcohol: failed (17 times)

- 12+ days sport: shamefully failed (only 6)

I finally have to reboot the sport program. Things have to improve.

Life & work situation

To be completely honest with you I feel my new job is not a good fit. But then I get paid tremendous amounts and benefits for doing really dull stuff and the colleagues/boss are friendly. I am often desperate about how little stimulation my job offers. Adjusting to

working back to Europe is a struggle after a decade in Asia. I am trying to make the most of it, be in the moment and enjoy the nice parts. Adjusting to

living back in Europe is a breeze. I really enjoy having a fantastic cheese selection and sitting on pavement cafes sipping beers (see also monthly alcohol target failure). So much music and other cultural offerings to take in, huge improvement over Singapore in this regard.

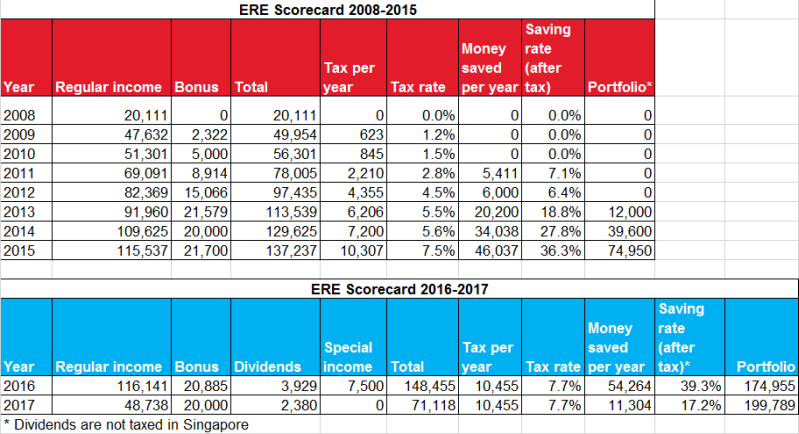

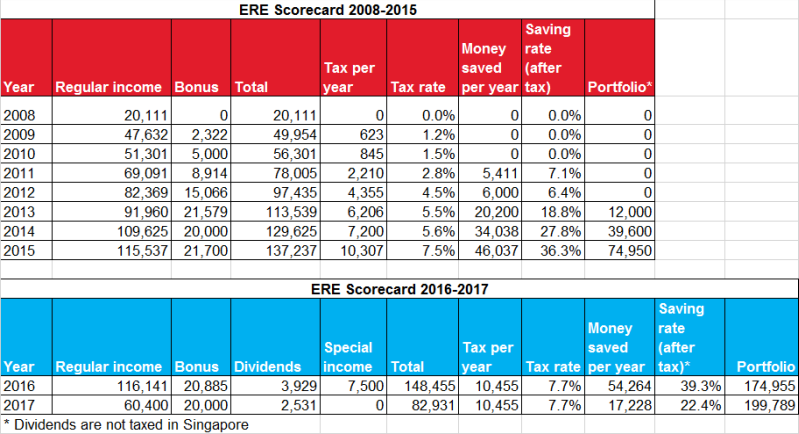

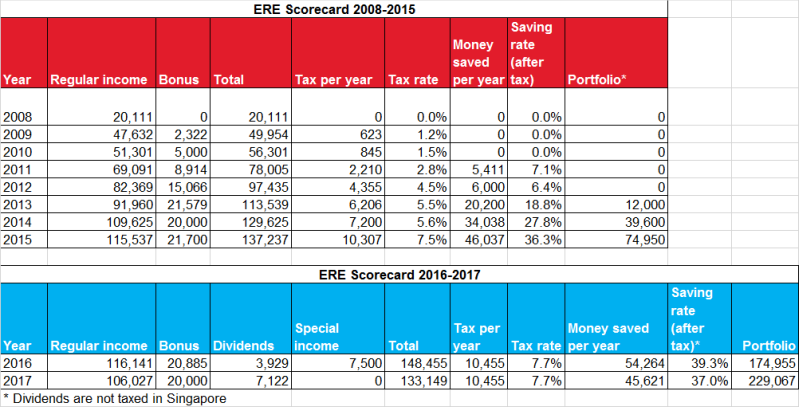

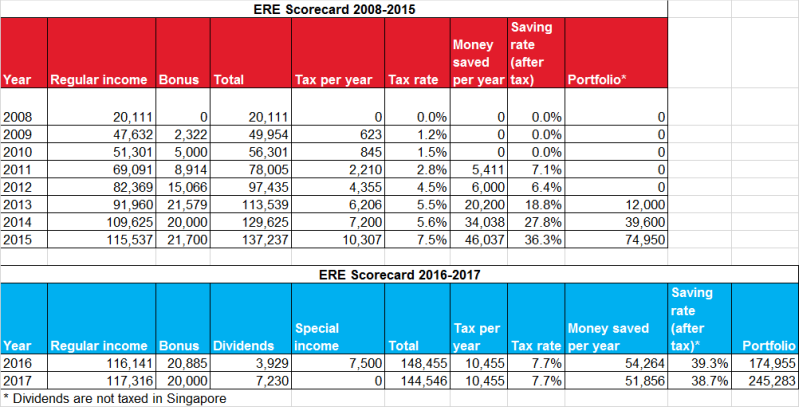

ERE Scorecard

In May I saved

59% of my income. Things are bound to improve now, as most startup costs of the new life are paid and I can reap the benefits of free housing etc.

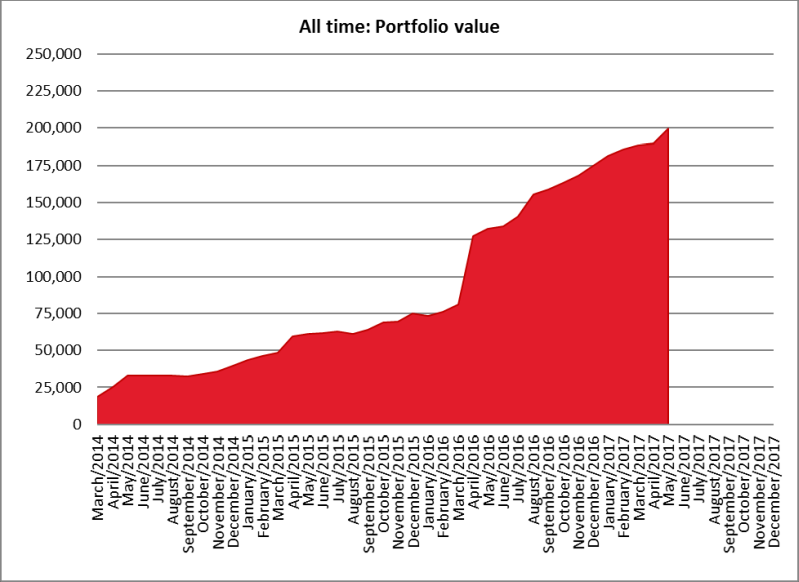

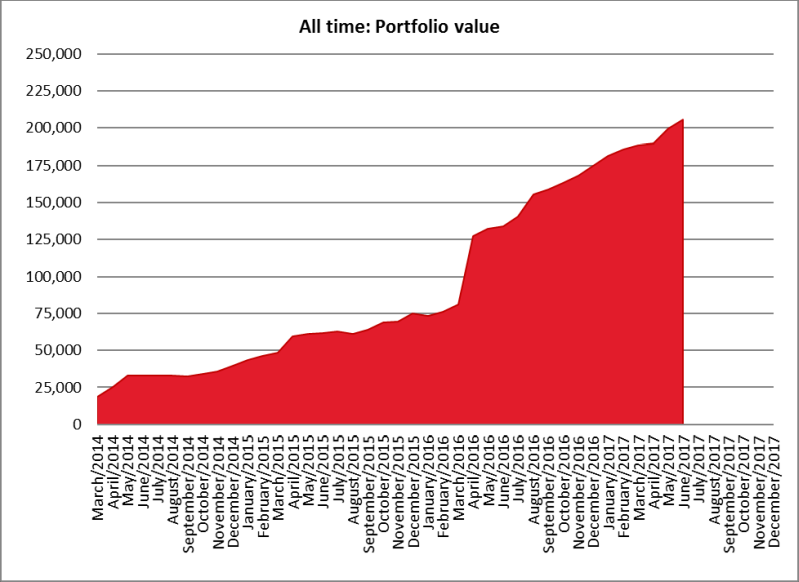

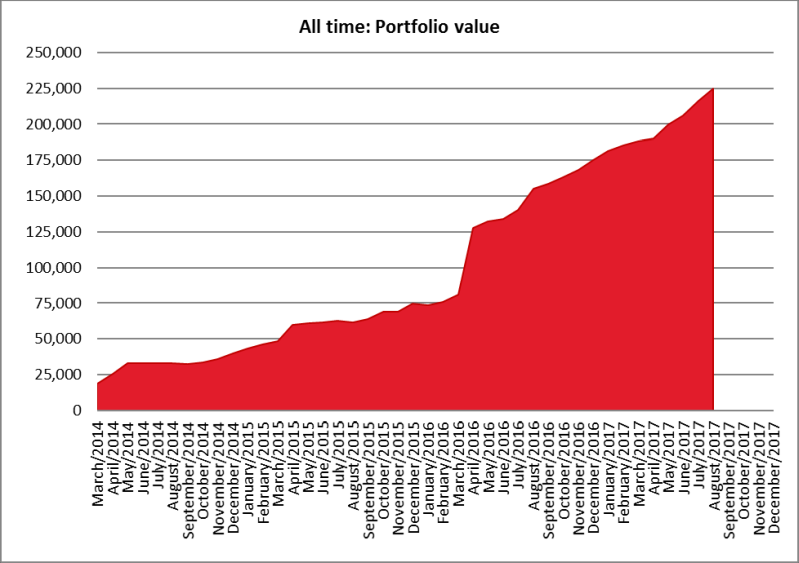

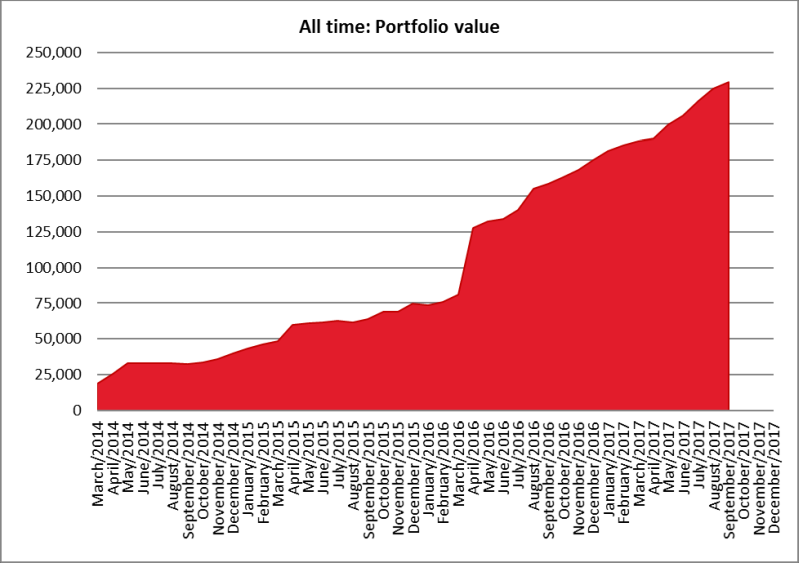

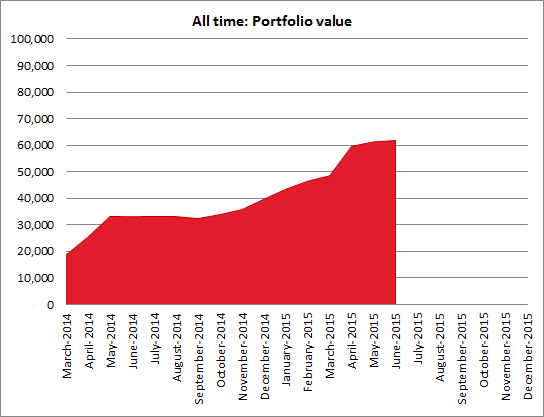

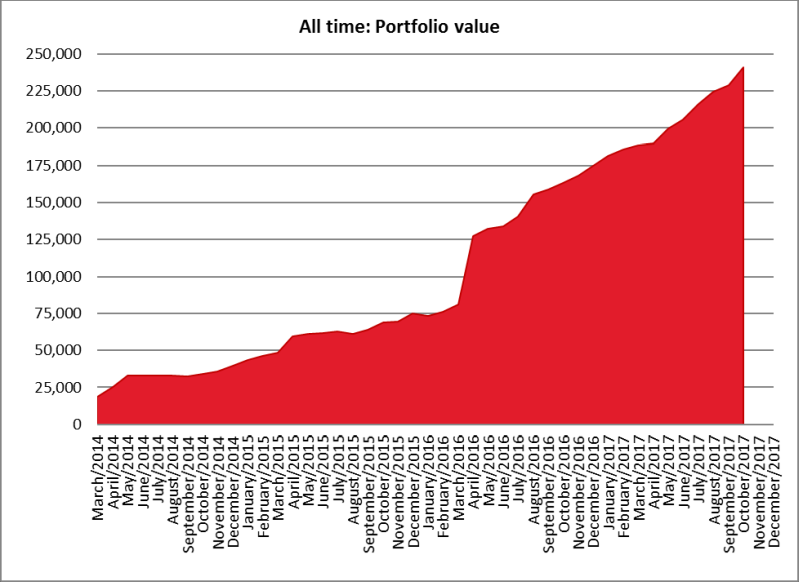

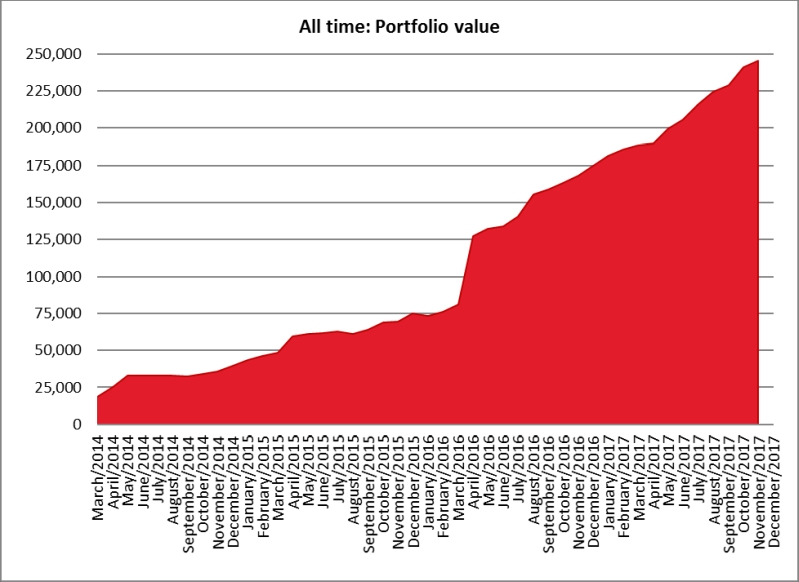

Portfolio update

Portfolio update

In May my portfolio increased by

SGD 9,922 or 5.2% to

SGD 199,789 (=USD 144,627). This gain was made up of capital gains of

SGD 3,930 and

SGD 5,992 of fresh investments.

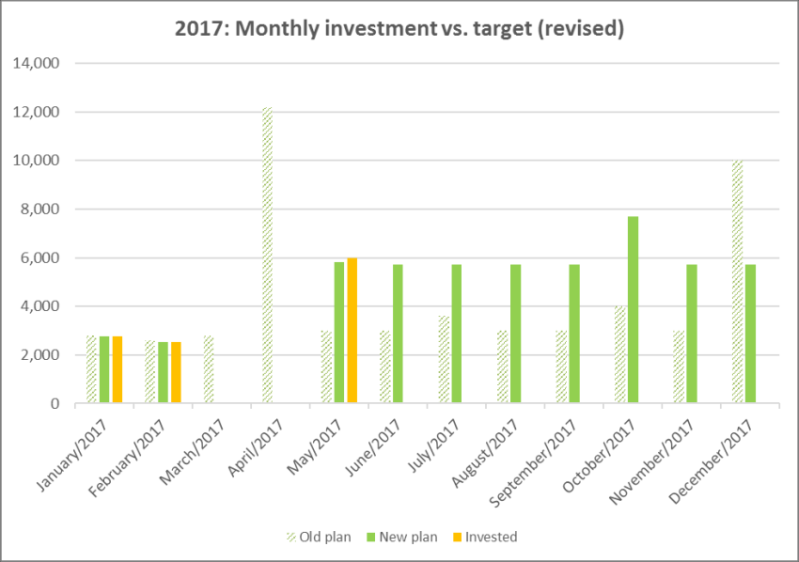

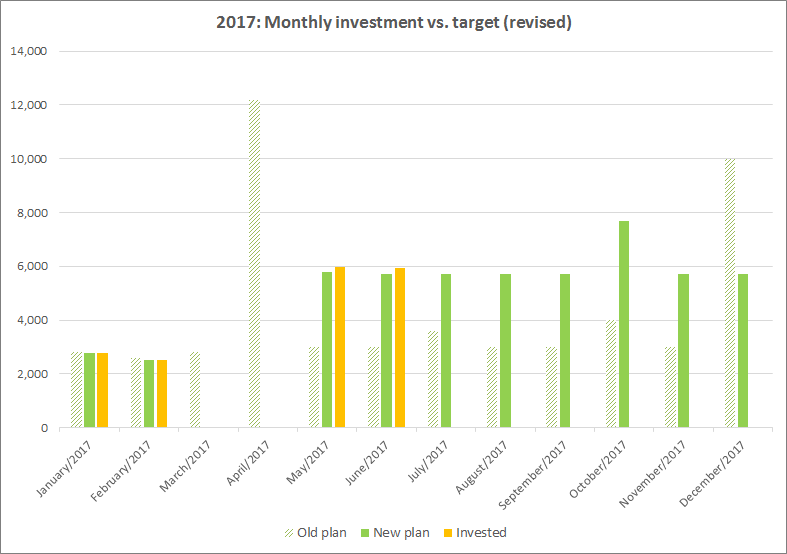

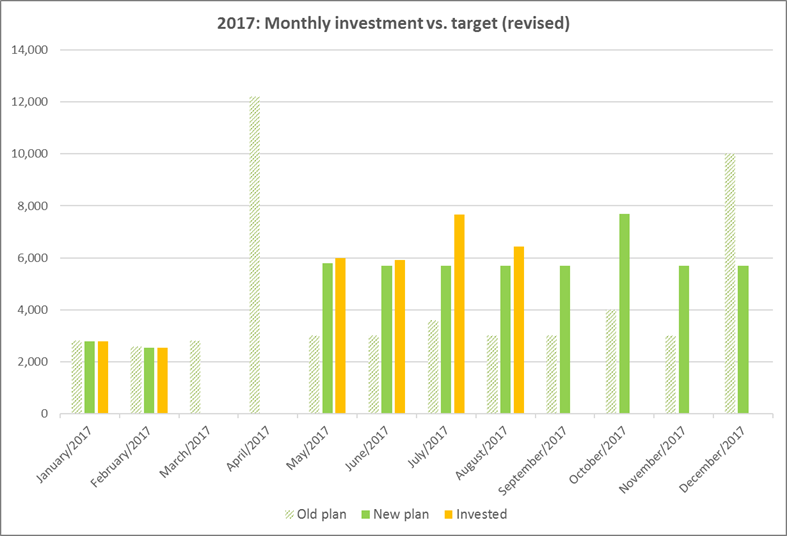

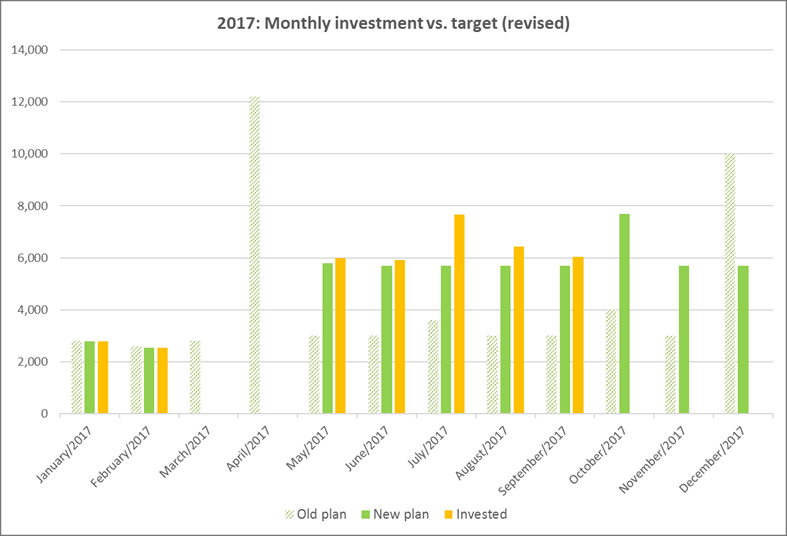

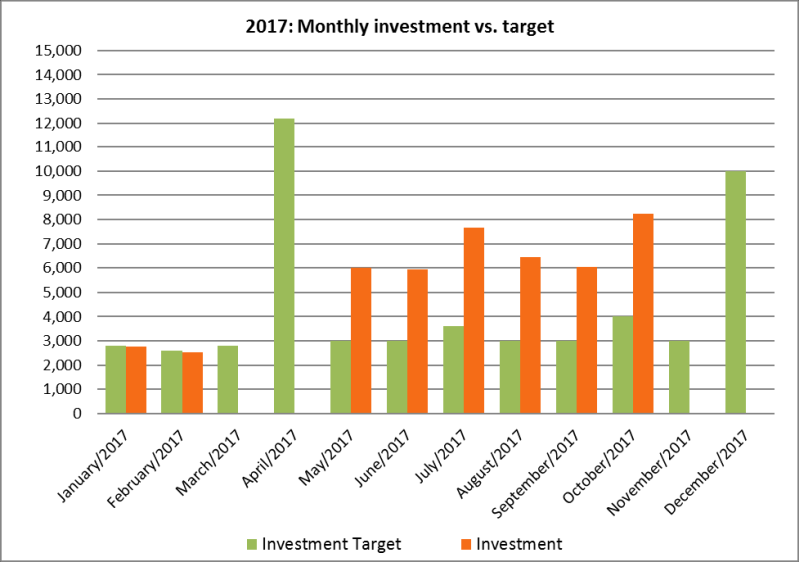

Monthly investment vs. plan

Monthly investment vs. plan

I invested

SGD 5,992 which is slightly higher than the updated plan.

This time I chose to buy some more bonds as stocks seemed pricy and I still had room in my asset allocation. Current yields of around 4.3% for the iShares J.P. Morgan USD Asia Credit Bond Index feel attractive.

I know that timing the market is pointless, but cannot help feeling European and US stocks are really expensive right now. I stick to my asset allocation and there is still room for a few more bonds.

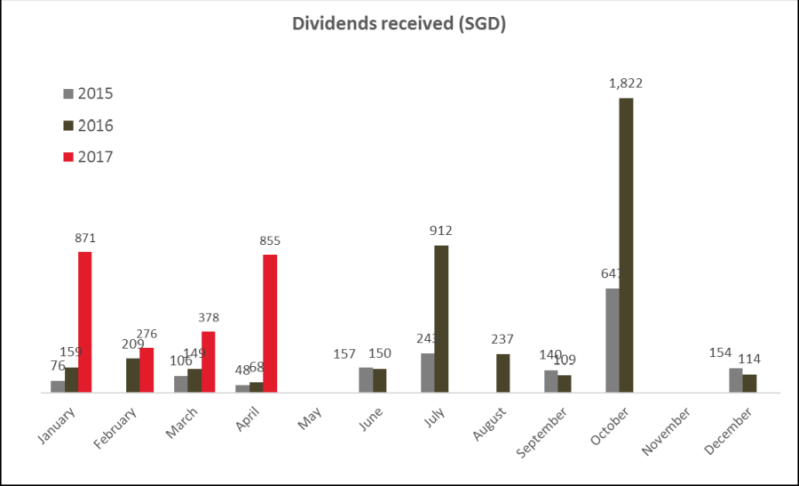

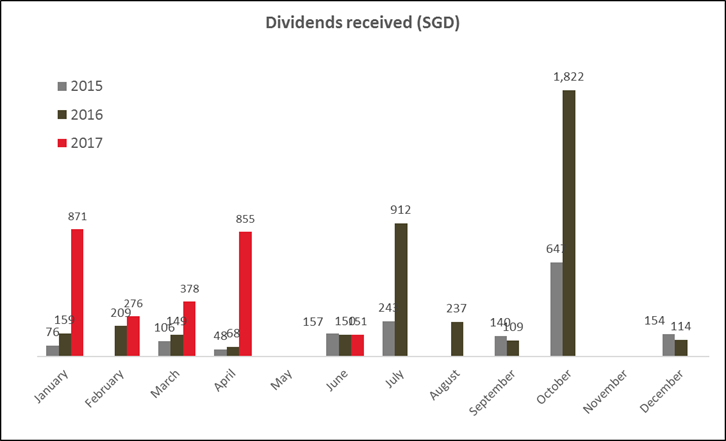

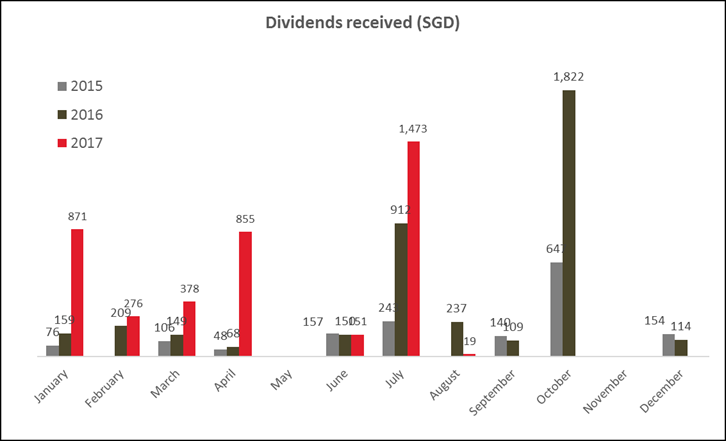

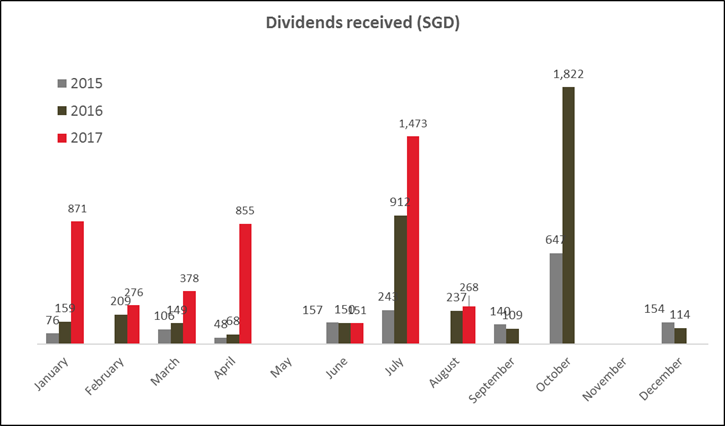

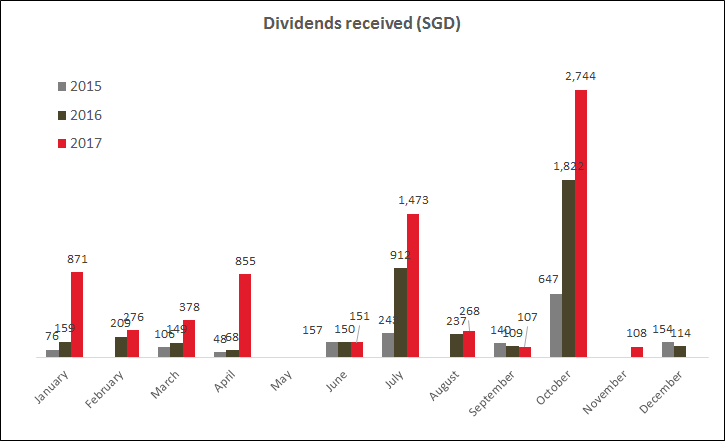

Dividends received

Dividends received

In May I did not receive any dividends.

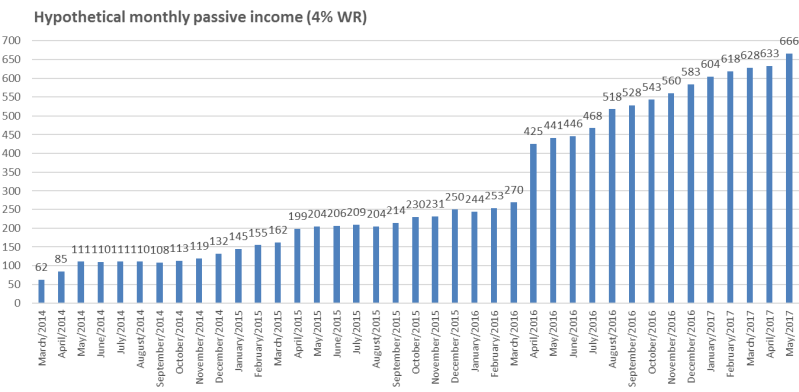

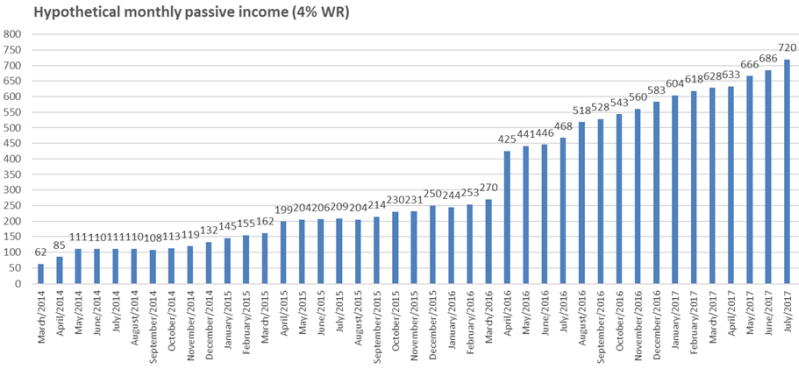

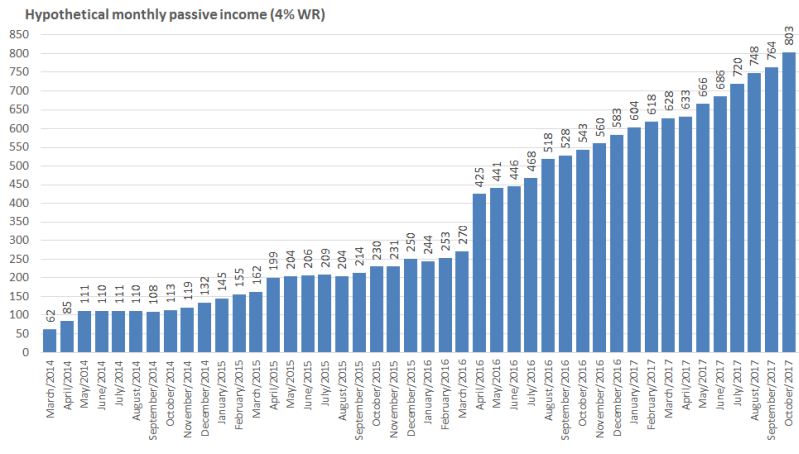

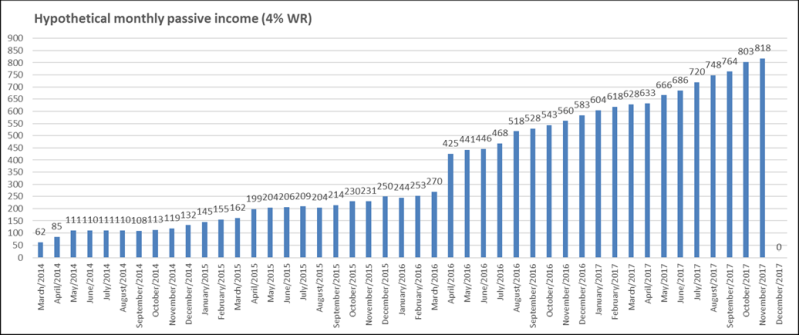

Hypothetical monthly income

SGD 666! Next year at this time it should be in the 4 digit range.

Coast FI age

If I suddenly decided to stop investing, when would I be able to retire based on growth of current portfolio? Assumptions: 6% annual portfolio growth, 2% inflation. May result: I can retire at age 81...

Outlook

Back on track, full steam ahead.

Re: Singvestor's awakening

Posted: Thu Jun 08, 2017 2:58 pm

by singvestor

I realise I forgot to reply to Brute's question. Company credit cards are the norm in my company as well, but unfortunately not available in my current home country/company. Very weird indeed.

Re: Singvestor's awakening

Posted: Thu Jun 08, 2017 9:47 pm

by BRUTE

Re: Singvestor's awakening

Posted: Thu Jun 08, 2017 11:36 pm

by Viktor K

Hello fellow Commander (ENTJ) and Asianite! I have re-found your journal and am catching up. With work being a bit easier/slower, maybe a hobby is in order? Also I really dig your update format, very clear and informative

Re: Singvestor's awakening

Posted: Sat Jun 17, 2017 2:36 pm

by wolf

Great progress. Keep on saving! It brings you step by step toward FIRE.

What are your goals? When would you say you are FI?

Re: Singvestor's awakening

Posted: Sun Jul 02, 2017 10:08 am

by singvestor

@Viktor, thanks for the note! Nice to find another ENTJ here. I am working quite a lot to try and tone down the negative sides of the commander personality, with some success but lots yet to do. How about you?

@MDFire2024: thanks! My retirement goal is SGD 1.2 million (EUR 765,000). My financial independence goal is SGD 750,000 (=EUR 480,000)

Monthly update #24: June 2017

Posted: Sun Jul 02, 2017 11:04 am

by singvestor

Monthly goal review:

- 20+ days no alcohol: failed (17 days)

- 12+ days sport: failed (11 days)

While this is by no means a result to be proud of, I feel that I have successfully restarted the sport program. I exercised a lot in the last 2 weeks of June and really have been enjoying the purpose, relaxation and extra energy.

Also tried cycling to work, which was a full success. We have nice showers in the office and with a bit of planning it was no issue. Arrived in the office in a calm and energetic state.

ERE Scorecard

In June I invested

51% of my income. Not really a great achievement, given the fact that my flat is fully paid for.

Overall I feel that my lifestyle is deflating during my expat assignment which is good. I did not buy a lot of stuff to fill the empty rooms in my oversized apartment and I did not go out to eat a lot. The only big ticket purchase derailing the savings rate was booking a trip to Iceland. A country that is definitely not easily compatible with frugal traveling. Small rooms in guesthouses with shared bathrooms can cost over EUR 100 per night.

July should be a better month with significantly higher savings rate.

Portfolio update

In June my portfolio increased by

SGD 5,908 or 3% to

SGD 205,697 (=USD 149,400). This gain was made up

SGD 5,924 of fresh investments offset by a small capital loss of SGD 16. Just like everyone says, the first SGD 100k was a lot harder than the second.

Monthly investment vs. plan

Monthly investment vs. plan

I invested

SGD 5,924 which is slightly higher than the updated plan.

I bought some more bonds.

Asset allocation

I need to buy a few more of these overpriced stock index funds next month. I would probably not mind bonds up to 30% of the portfolio at this moment, but do not want them to be higher than that.

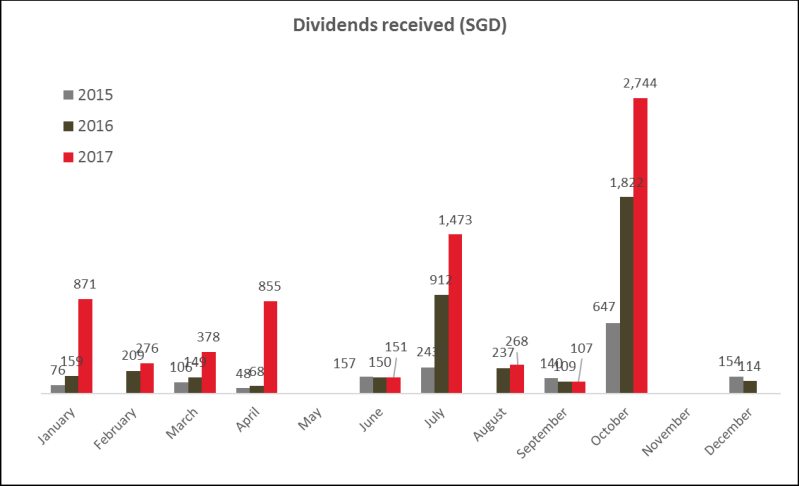

Dividends received

In June I got

SGD 151 in dividends, which are waiting for reinvestment.

Hypothetical monthly income

Hypothetical monthly income

SGD 686

SGD 686

The more I am thinking about it, the more I feel 4% WR is rather high… Will leave the graph intact for consistency.

Coast FI Age

If I suddenly decided to stop investing, when would I be able to retire based on growth of current portfolio? Assumptions: 6% annual portfolio growth, 2% inflation. May result: I can retire at age 80...

Outlook

Things have stabilized in my new life and I am dedicating a lot of my energy to improving my French. My goal is to have my level of French match my English, which needs a lot more classes (paid for by the company) and my own determination and effort. Job is underwhelming, but does not cost much energy, so I can focus on improving my skills.

Focus in July: learning French, meeting sport goal, saving money.

Re: Singvestor's awakening

Posted: Sun Jul 02, 2017 11:09 am

by Viktor K

singvestor wrote: ↑Sun Jul 02, 2017 10:08 am

@Viktor, thanks for the note! Nice to find another ENTJ here. I am working quite a lot to try and tone down the negative sides of the commander personality, with some success but lots yet to do. How about you?

I feel this is an exercise in futility, but a worthy one at that, and of course something I too spend a lot of thought and energy on. If you're anything like me, then you struggle to reconicle your personality type's strengths with its glaring (in your own eyes) weaknesses. I think it is a curse of the ENTJ, but maybe it is me, or maybe it is a human thing. I have a girlfriend who has every strength that I lack. She is caring, compassionate, and sees the good in every person and thing. I feel we are a good match because each of her strengths is something I'm terrible at, so each is something I can respect and admire and strive to be better at. Of course, I constantly fail

Monthly update #25: July 2017

Posted: Mon Aug 07, 2017 10:18 am

by singvestor

Monthly goal review:

- 20+ days no alcohol: failed (18 days)

- 12+ days sport: failed (11 days)

Less than ideal… There are always things interfering with the program, the most common being my own laziness. A 30-minute round of bodyweight exercises should normally always fit in.

ERE Scorecard

In July I invested

59% of my income.

While this sounds good it also means that I spent

SGD 5,280 (EUR 3,320) last month. I had very little discipline and spent too much money. As my flat is paid for by the company this is all discretionary spending on air tickets, presents, groceries and so on. I have decided to track spending more closely from now on.

Overall savings rate for the year is still improving, currently at

28%.

On the bright side I have adjusted from eating out 1-3 times a day in Singapore to just 1-2 times every two weeks in the current country. We are cooking a lot and enjoying it. Better food and improved gym routine contribute to overall better fitness level.

Portfolio update

In July my portfolio increased by

SGD 10,227 or 5% to SGD 215,924 (=USD 158,700). This gain was made up

SGD 7,668 of fresh investments and capital gains of

SGD 2,559.

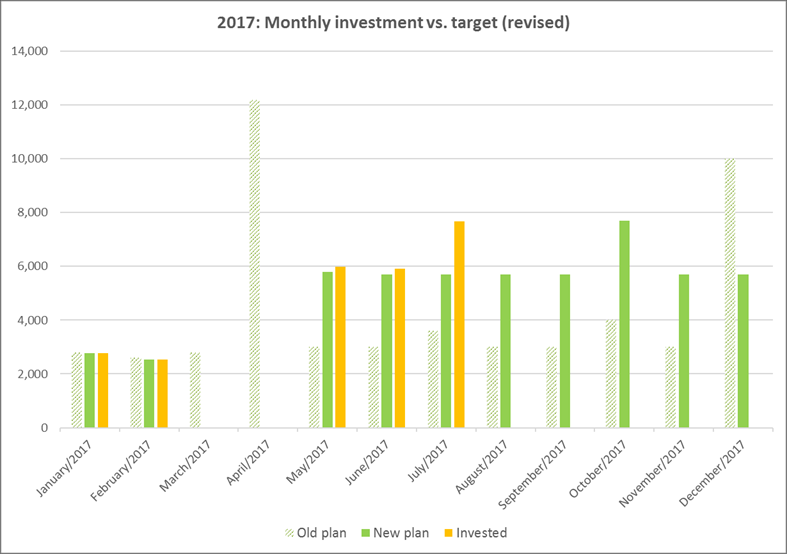

Monthly investment vs. plan

Monthly investment vs. plan

I invested

SGD 7,668 which is about

SGD 2,000 higher than the updated plan.

I bought some more bonds and also some “overpriced” (my subjective feeling) stock. Market timing is pointless, but a higher bond allocation feels safer. Still I definitely want to keep the bonds <= 30%.

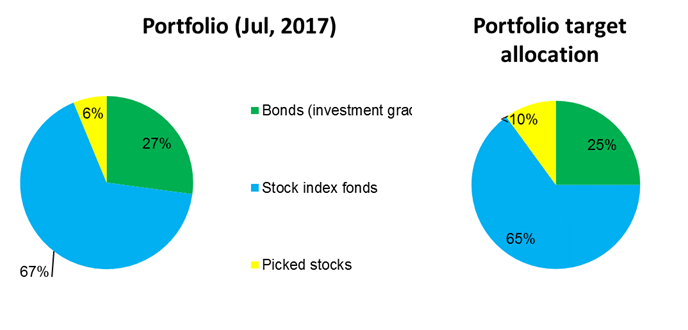

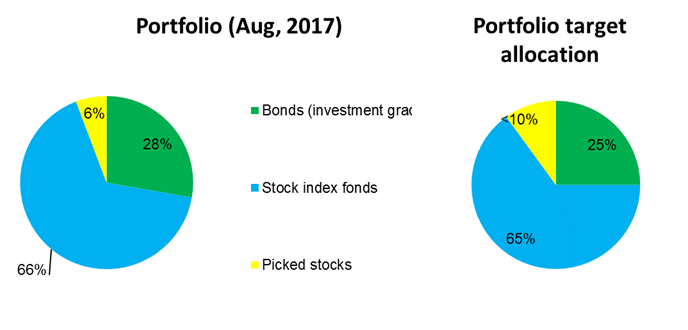

Asset allocation

Bonds slowly creeping up, currently at

28%.

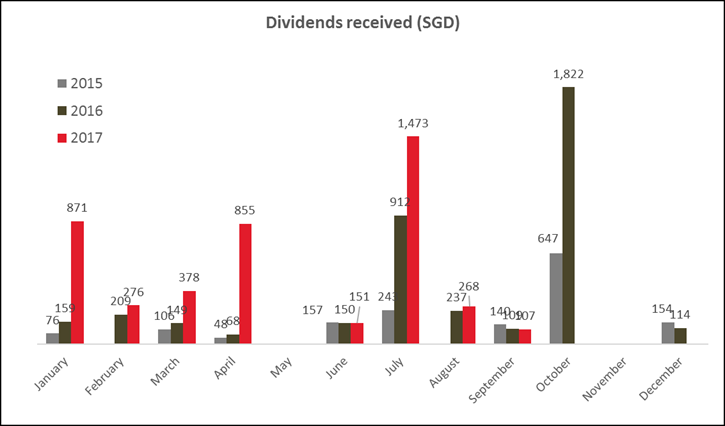

Dividends received

In July I got

SGD 1,473 in dividends, which I reinvested as usual. Dividends are still tax free for me, as my company successfully applied for a tax scheme where I only need to pay for income that I receive in my current country.

Hypothetical monthly income (@4% WR)

Hypothetical monthly income (@4% WR)

SGD 720

SGD 720. The figure is climbing a bit faster these days, thanks to my higher income and increased investments.

Coast FI Age

If I suddenly decided to stop investing, when would I be able to retire based on growth of current portfolio? Assumptions: 6% annual portfolio growth, 2% inflation. July result: I can retire at age 80...

Outlook

In August the wife (still feels weird to type that) and I will travel to Iceland. The most ridiculously priced destination in Europe where basic rooms with shared bathroom can cost EUR 100-150 and above, but we have decided to cut costs as much as possible by buying food from super markets etc.

Re: Monthly update #25: July 2017

Posted: Mon Aug 07, 2017 11:36 am

by wolf

singvestor wrote: ↑Mon Aug 07, 2017 10:18 am

Coast FI Age

If I suddenly decided to stop investing, when would I be able to retire based on growth of current portfolio? Assumptions: 6% annual portfolio growth, 2% inflation. July result: I can retire at age 80...

Outlook

In August the wife (still feels weird to type that) and I will travel to Iceland. The most ridiculously priced destination in Europe where basic rooms with shared bathroom can cost EUR 100-150 and above, but we have decided to cut costs as much as possible by buying food from super markets etc.

Hi singvestor. Great progress so far. Impressive income! I gotta read your journal from the very beginning because I am about your age and I am always interested in reading about people's lifestyles in other parts of the world.

I have been to Singapore once and I liked it there. Very structured and clean city.

Keep on saving! And I also wish you both a nice vacation in Iceland, quite the opposite of Singapore.

Re: Singvestor's awakening

Posted: Sun Sep 10, 2017 6:11 am

by singvestor

Thanks, MDFIRE2024!

Monthly update #26: August 2017

Posted: Sun Sep 10, 2017 6:17 am

by singvestor

Monthly goal review:

- Days without alcohol: failed (17 days)

- 12+ days sports: failed (11 times)

Less than stellar performance I must admit. During the holidays it was difficult not to have a beer here and there and my current home country is full of nice street cafes, live concerts and so on... Have to go to the gym more and to bars a lot less.

Every month I hope I will improve, but similar to weight loss, financial independence and other goals this needs lifestyle change instead of trying the same all over again.

ERE Scorecard

In August I invested 55% of my income. Might have done better, but holiday in Iceland was extremely expensive. Basic hostel rooms easily cost EUR 100 per night. I gave rides to plenty of hitchhikers who managed to travel ERE style by sticking to camping grounds and hitchhiking to make the trip affordable. My wife and I had not been up for it, but we decided to just use a tent during the next trip to such an expensive place.

Re-reading Jakob's book

During my trip I re-read Jakob's book for the first time in a few years. It was quite an interesting experience. The first time I had read it more for the "recipes", to learn about financial independence, the second time I read more the philosophical pieces and the underlying concepts, which I had skimmed through the first time. I also enjoy the humor injected into the book. Parts are repetitive (e.g. the hint to read books on ship provisioning to save grocery costs appears a few times instead just of once), but it definitely inspired me again to re-evaluate priorities and challenged me to do things differently.

Portfolio update

In August my portfolio increased by

SGD 8,556 or 4% to

SGD 224,480 (~ USD 165,400). This gain was made up of SGD 2,121 of capital gains and SGD 6,435 of fresh investments.

Monthly investment vs. plan

I invested

SGD 6,435, which was more than the plan (SGD 5,700).

Dividends received

Dividends received

SGD 268

SGD 268 (which were reinvested)

Hypothetical monthly income

It is taking forever, but at least the portfolio is growing faster these days.

Outlook

September is promising to be an unremarkable month. Let's see!

Re: Singvestor's awakening

Posted: Sun Sep 10, 2017 1:01 pm

by BRUTE

how's the tax situation while Singvestor is living long-term in Europe? doesn't Europe have very high taxes?

Re: Singvestor's awakening

Posted: Sun Sep 10, 2017 1:24 pm

by singvestor

Taxes are insane at around 50%, but the company is paying everything that exceeds the amount I would have to pay in Singapore because of a hypo tax clause in my delegation contract. Thus I only know my after tax salary.

Re: Singvestor's awakening

Posted: Sun Sep 10, 2017 1:27 pm

by BRUTE

oh nice

Monthly update #27: September 2017

Posted: Sun Oct 01, 2017 11:20 am

by singvestor

Worst things first:

Monthly goal review:

- Days without alcohol: failed (17 days)

- 12+ days sports: failed (10 times)

Terrible. Absolutely no discipline and too many social obligations.

Got a standing desk at work. Additional goal for September: stand at least 40 hours while working. Hopefully that will also help me achieve a better posture. Wife has been calling me hunchback lately.

ERE Scorecard

In September I invested

53% of my income. I spent way too much money, mostly on booking various vacations. My wife is still searching for a job which is not as easy in good old Europe as it is back in Singapore/most places in Asia.

My expenses were therefore a bit higher. We cooked most our meals, but went to nice restaurants 3-4 times. This is a huge change from Singapore, where typically we would go to restaurants all the time, sometimes multiple times a day.

Still, as we are living rent free, 70% saving rate should be very comfortable.

Portfolio update

In September my portfolio increased by

SGD 4,587 or 2% to

SGD 229,067 (~ USD 168,700). This gain was made up of

SGD 6,036 of fresh investments which were offset by paper losses of

SGD 1,449.

Monthly investment vs. plan

I invested SGD 6,036, which was more than the plan (SGD 5,700).

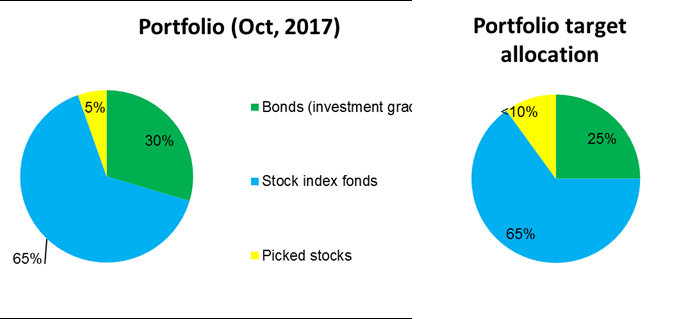

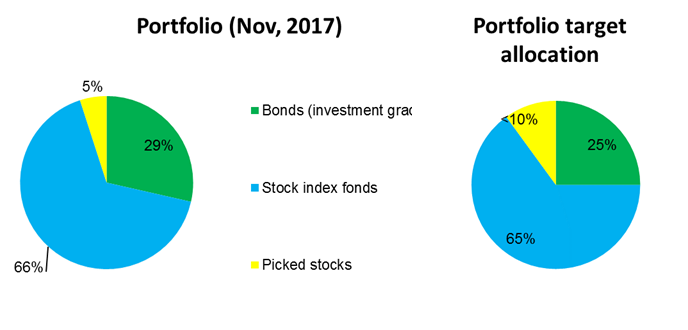

Portfolio allocation

Portfolio allocation

I need to keep the bond portion constant at 30% now, but I am worried about current stock valuations. Still I am forcing myself to buy more stocks, knowing that I cannot time the market.

Dividends received

SGD 107 (which were reinvested)

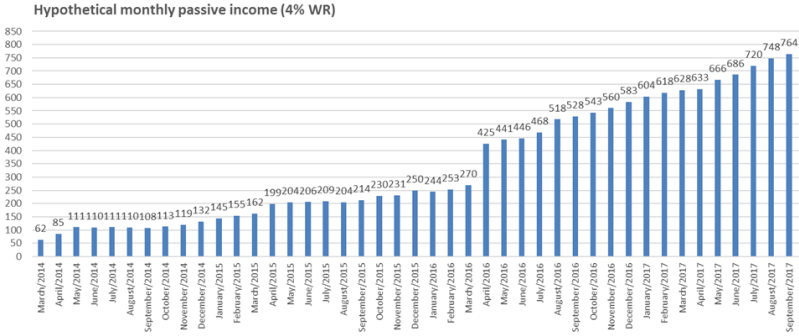

Hypothetical monthly income (4% WR)

Hypothetical monthly income (4% WR)

SGD 764

Outlook

SGD 764

Outlook

Obviously I will be able to save a lot of money during my three year Europe assignment, but I do not have any good options after that. It is time to solve this dilemma, but not sure how. Additional qualifications would be good, but I have no idea what to do.

The obvious plan is to use the three year assignment to save as much as possible. With a bit of discipline I should be able to get to SGD 500,000 which is two thirds of the Lean Financial Independence target.

If my Europe assignment would be extended or (even better) I could get a follow up assignment in a different place then I could comfortably reach the lean financial independence target before the age of 40.

But what then? My dream: work 1-2 days each week or 3-4 days remotely and coast the rest, travel, read, learn more languages.

Re: Singvestor's awakening

Posted: Sun Oct 01, 2017 1:51 pm

by BRUTE

for as long as brute remembers reading this thread, singvestor has failed his fitness goal very narrowly: the goal is always 12 and the actual is always around 10. this isn't what brute would call a failure. it's a 83.3% success rate.

long term dream sounds a lot like brute's dream

Re: Singvestor's awakening

Posted: Sun Oct 01, 2017 3:22 pm

by dagiffy

singvestor wrote: ↑Tue Jul 21, 2015 10:12 pm

Nice to meet all of you!

My name is Singvestor, I am a 33 year old European guy living in Singapore. After some mad years I have been slowly awaking to the reality of my finances and it has been becoming increasingly clear: I want to be FI.

I have not admitted this to anyone before and I hope to find some good feedback and likeminded people here.

My journey so far is quite embarassing, but I want to be brutally honest.

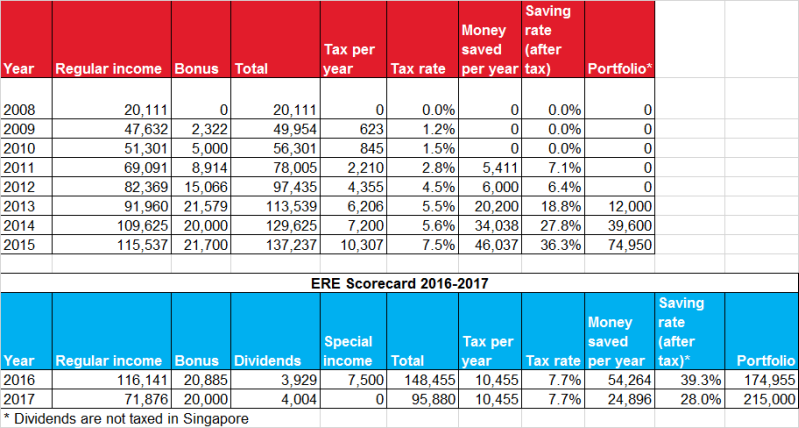

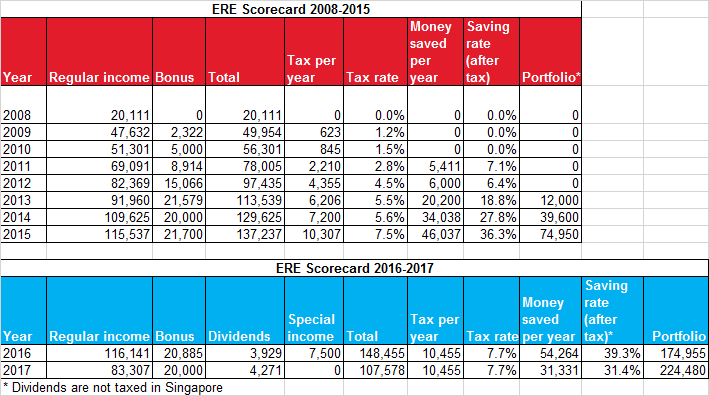

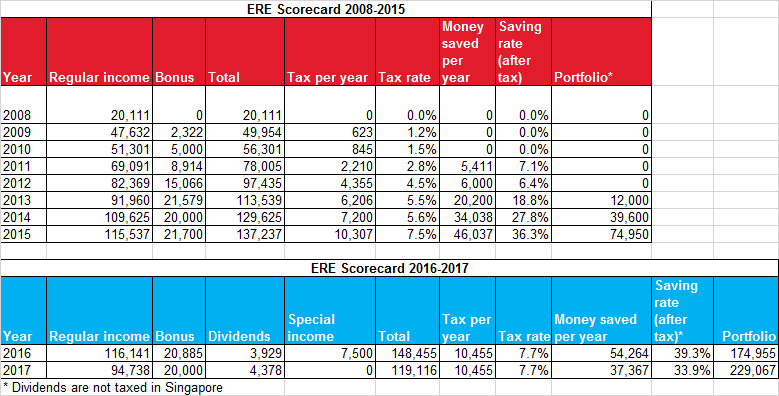

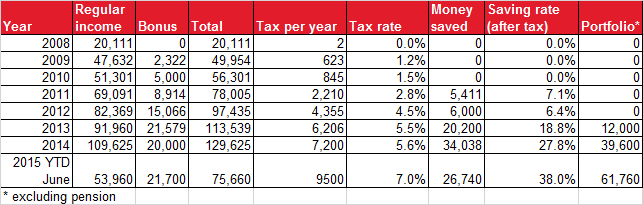

Yearly development of income, savings and taxes

Note: All figures are in SGD. 1 SGD = 0.75 USD.

And this is how I pissed away a quarter of a million Singapore dollars in the first five years of working.

After graduating I earned an okay salary but spent it all immediately and lived recklessly paycheck to paycheck. I had very little expenses but was struggling very much to getting used to working.

Flying to Europe over the long weekend? Why not! New DSLR? Why not? 300 Singapore dollars for a night of partying? Why not!

I wish I could punch younger self in the face.

Between 2009-mid 2011 I lost quite a bit of grip on my life, dating a very difficult person while at the same time travelling for business like a mad man.

Born as an introvert I had to adapt to being highly sociable, leading a small team, travelling all across Asia, meeting new people all the time. I powered through but after a whole day of full-on social interaction with people from various cultures I was exhausted. I had started drinking quite a lot to relax in the evenings and I had gained about 10kg since graduation. Waking up somewhere in China in a hotel room with beer cans on the floor, this type of stuff.

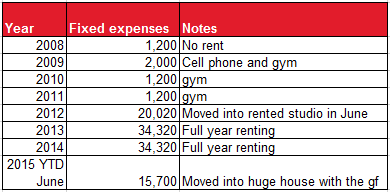

I present you my "table of shame"

As you can see I had no expenses (living rent-free) and still spent all the money.

The awaking begins with some first clueless steps

Somewhere in mid 2012, I realized what had happened to me the last few years. I was fat (1.79m, 82kg) had nothing to show for 4 years of working. I had no goals, but decided to get back in shape, limit beer consumption and not live paycheck to paycheck. I moved into my own appartment which is expensive as hell in Singapore and stopped spending money aimlessly.

Early 2013, I finally made a plan and rediscovered my deep love for Excel and graphs.

I decided to save SGD 100,000 which seemed like an impossibly high number at this time.

Clueless about investing I opened an online trading account and bought some shares of companies that I found promising. And had a very messy portfolio by end-2013.

Life changer: Discovering FI

End of 2013 marks a big change in my life when I finally discovered proper financial planning. It all came at once: Mr Moneymoustache, ERE, Bogleheads, A Random Walk Down Wallstreet and especially Your Money or Your Life.

I was intrigued. I started using taxis less, biked to the train station, lost the excess weight and replaced some silly expenses (SGD 1,200 / year gym) with cheaper alternatives (SGD 5 per entry gym)

Needless to say I was very pissed at younger self. Living in a low tax country with no capital gains or dividend taxes and wasting all my money. What an idiot I was.

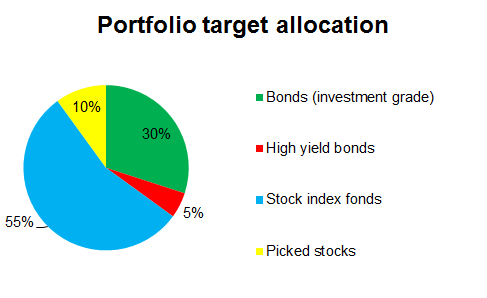

I created a new target allocation:

and moved money into index funds.

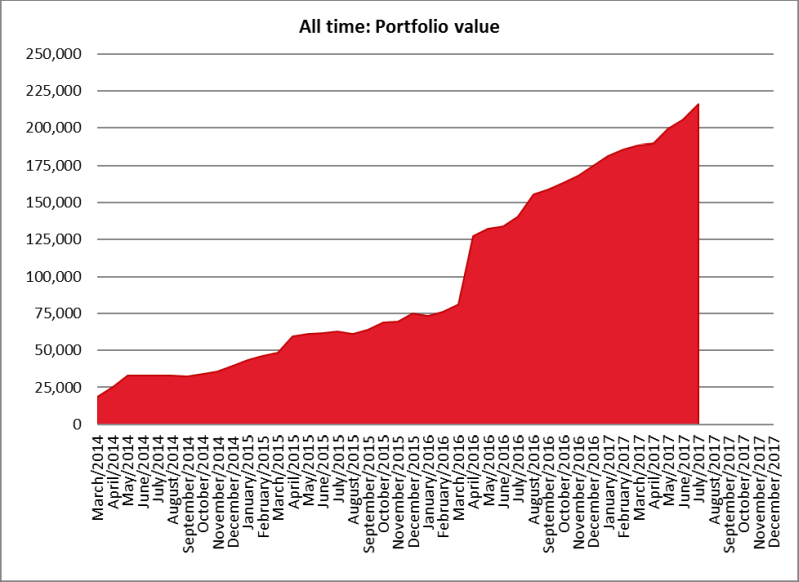

It was a painful journey, but slowly the portfolio is growing.

After trucking along in 2014 and the first half of 2015 I realized that I am not badass enough. I discovered the relationship of saving-rate and speed to retirement.

I realized I need to be a lot more badass to get out of the corporate 9-5.

And so it begins! Let's get this journal started!

This is one of the greatest first posts I've ever seen. Whatever impresses Brute, even in the least, impresses the socks off of me. Well done.

Monthly update #28: October 2017

Posted: Sat Nov 04, 2017 12:09 pm

by singvestor

Monthly goal review:

•

20 Days without alcohol: failed

(17 days)

•

12+ days sports: failed (7 times)

•

40 hours stand at desk: failed (20? hours)

While this is not very good some of the effects came from a nine day trip to Portugal where I drank copious amounts of red wine, but also walked 96 km according to the wife’s fitness tracker. This was in addition to the 7 times sport.

Portugal

If you ask me: a pretty ideal location for those who have retired. Low costs, good food, weather very pleasant all year round… Access to mountains, sea… How much better can it get?

Nós ossos que aqui estamos pelos vossos esperamos

We bones that here are, for yours await

Visited a chapel which was stacked to the ceiling with old human bones and the above motto written over the entrance. Got reminded that I need to accelerate financial independence efforts.

Photo from the inside of the chapel:

Judging from the

Wikipedia page of the chapel the two skeletons used to hang from ropes, but now have been placed into these glass boxes...

ERE Scorecard

In October I invested

59% of my income. This is not really enough, but things should improve because:

Wife got a job

The dear wife got a professional full-time job in Europe starting next week and we can therefore return to the glorious DINK life. She is a lot more financially responsible & frugal than me and likes investing her salary. We are still keeping finances separate for convenience sake, so all the numbers in this journal are only from me. Maybe my wife should start her own journal

Portfolio

In October my portfolio increased by

5.2% or

SGD 11,922 to

SGD 240,989 (=USD 176,500).

This gain was made up of

SGD 8,254 of fresh investments and

SGD 3,668 of capital gains.

Stock valuations are getting higher and higher and I am not really comfortable with the price levels, but then I started work in 2008 and so tough economic times are all I am familiar with. The economy in Europe seems to be doing quite well now.

Investment vs. plan

In October I invested

SGD 8,254 which was more than the plan (

SGD 7,700).

Asset allocation

Asset allocation

More or less in line with the plan.

Dividends

In October I received a bumper crop of dividends:

SGD 2,744 made it to my account. Dividend income is increasing strongly and should be a significant part of my income in a few years, provided that I can continue to receive them tax free.

Hypothetical monthly income (4% WR)

SGD 803.

Outlook

SGD 803.

Outlook

Now that the wife has a new fulltime job my spending will be reduced a bit. I am also committed to the sport program and will give it my best in November. Work is a bit surreal for me, I have to do very little and mostly quite basic work, at the same time I am overpaid for the job. I keep worrying that someone will realize what a waste of money this is and that will be the end of the gravy train and expat life. I guess I have to enjoy it while it lasts…

Monthly update #29: November 2017

Posted: Sun Dec 03, 2017 12:25 pm

by singvestor

Monthly goals

•

20 Days without alcohol:

failed (17 days)

•

12+ days sports:

achieved (13 times)

•

40 hours stand at desk:

failed (20? hours)

ERE Scorecard

In November I invested 55% of my income. Not ideal as usual. I spent a week in the Spanish Canary Islands to escape work. At least I could manage the sport challenge, thanks to lots of free time during the short holiday.

Portfolio

Portfolio

In November my portfolio increased by

5.2% or

SGD 4,294 to

SGD 245,283 (=USD 182,100).

This gain was made up of SGD 6,235 of fresh investments which were offset by a decline in portfolio value by SGD 1,941.

Investment vs. plan

In November I invested SGD 6,235 which was more than the plan (SGD 5,700).

Dividends

Dividends

SGD 108

SGD 108 were received from my small holding of HSBC stocks.

Hypothetical monthly income (4% WR)

SGD 818.

Outlook

SGD 818.

Outlook

Work is not going too well, but I know I should not complain so much given my fortunate circumstances.