monthly goal review:

- 20 days no alcohol: failed: 19 days

- 12 times sports: achieved: 15 times

Had visitors, was in Southern France, drank copious amounts of wine… not ideal.

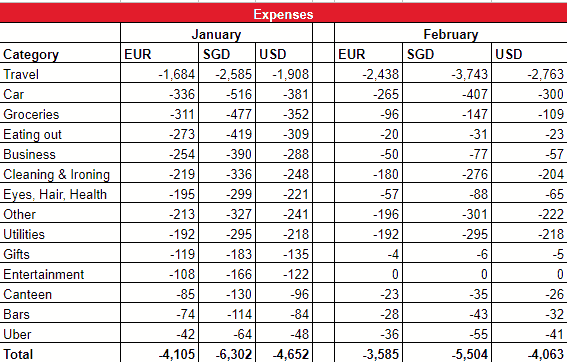

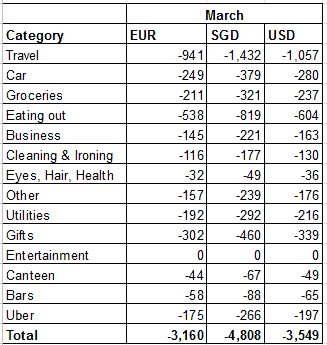

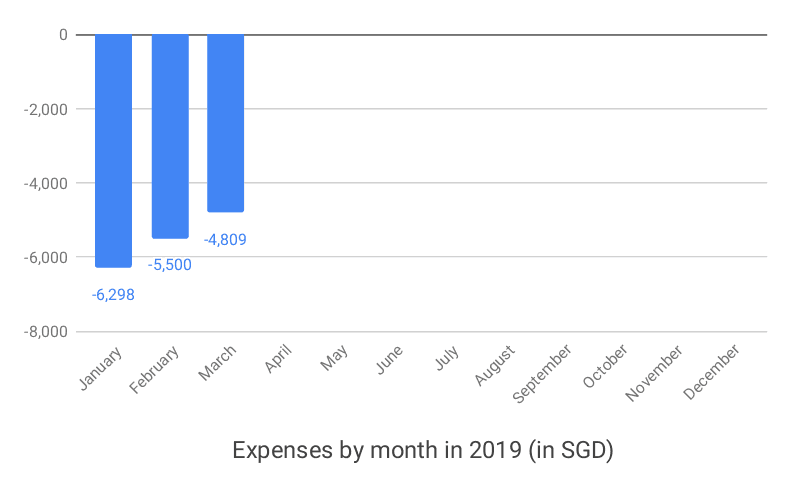

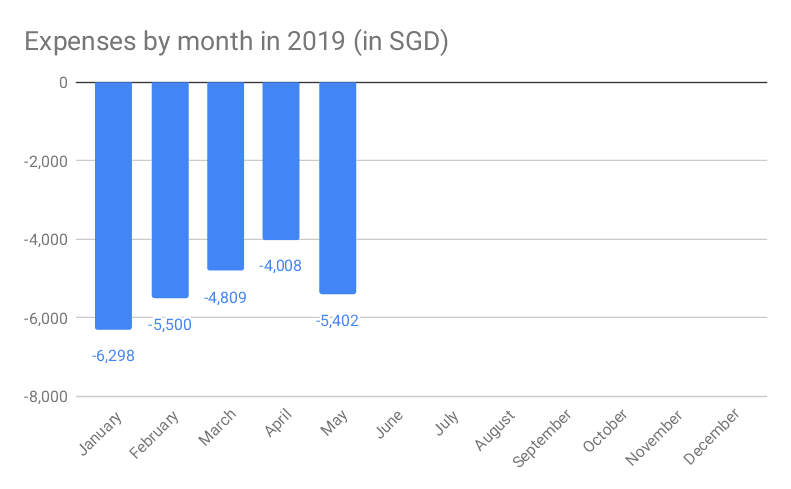

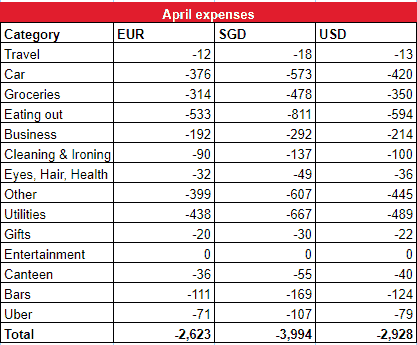

April expense report

I spent

SGD 4,008. Way too much of course. These were the categories for April:

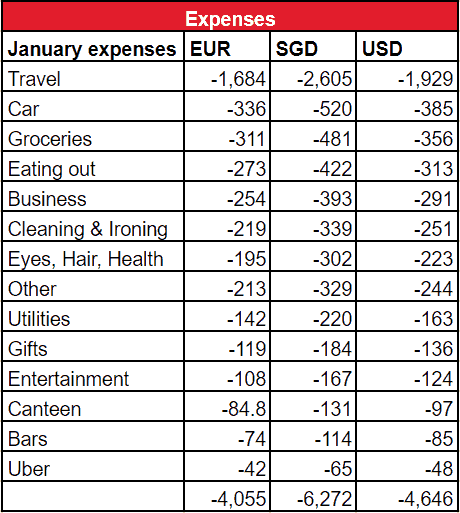

Notable points:

Utilities spending is rather high, as I had to pay the yearly water bill. DW showers recreationally and has childhood trauma of her aunt banging the bathroom door asking her for shorter showers. I could try switching to a more efficient shower head, I guess?

Groceries spending is high, since I forgot my company vouchers and realized at the cashier once.

Bought some unnecessary things, including a limited art print for EUR 129, a laser distance meter to measure a house and so on

I contemplated Bigato’s point to include the company meal vouchers in the calculation, but decided to leave them out because of laziness. They make up <2% of compensation and are complicated to account for, since they cannot be converted to cash and are used mainly by my wife who works near the supermarket (we still keep separate accounts). I also will not count my “free” flat which is paid for by the company.

Overall: Quite embarrassed at the spending level.

I fear that Jacob will ban me at some point for my ERE-unworthy behavior

Only sign of hope:

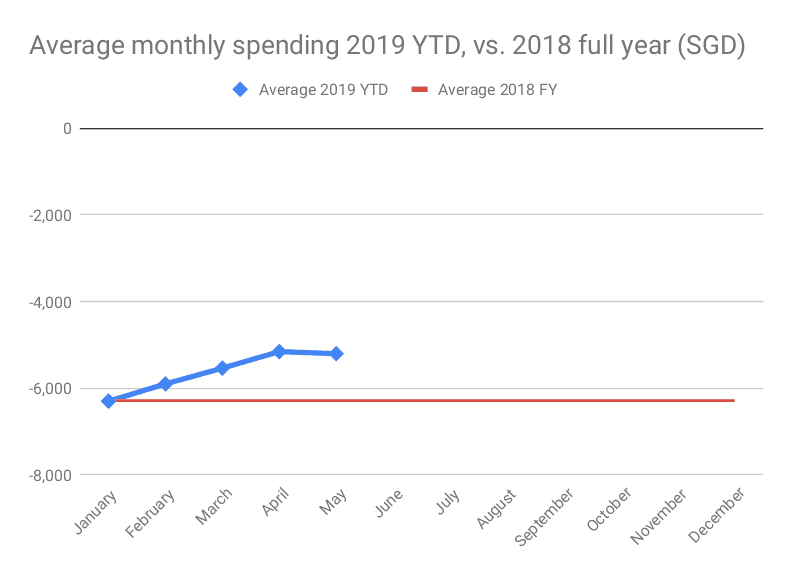

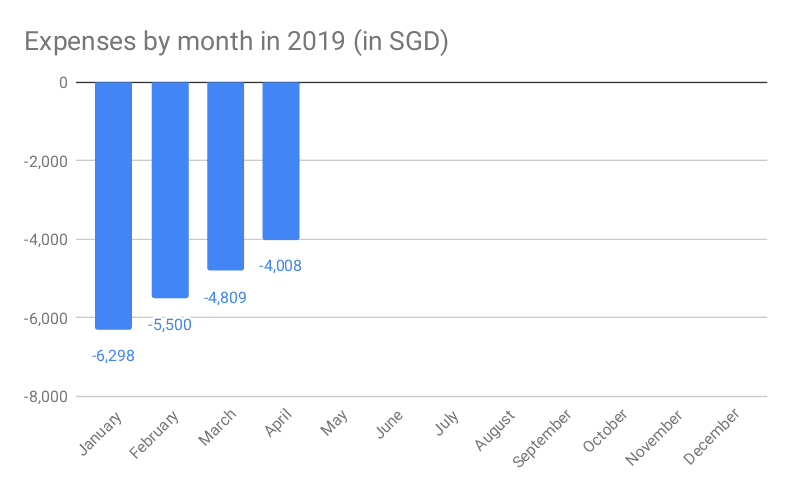

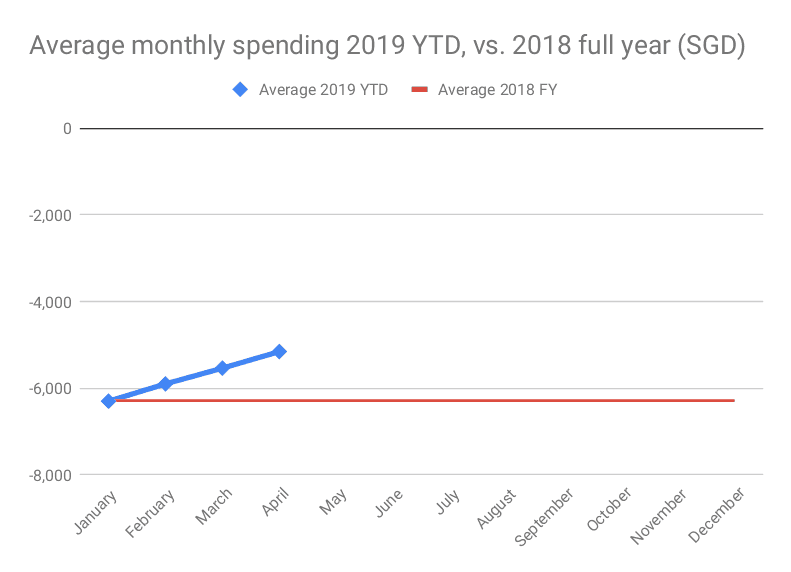

Expense trend is going down slowly:

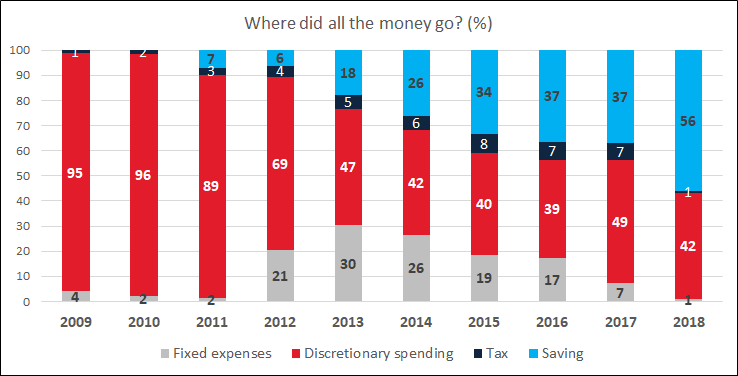

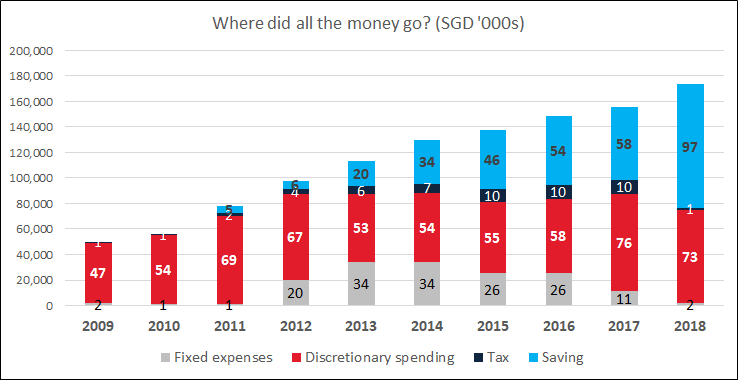

I hope to maintain this trend and reduce spending of vs. last year:

Why did I not focus on expenses the first 5 years of my ERE journey?!

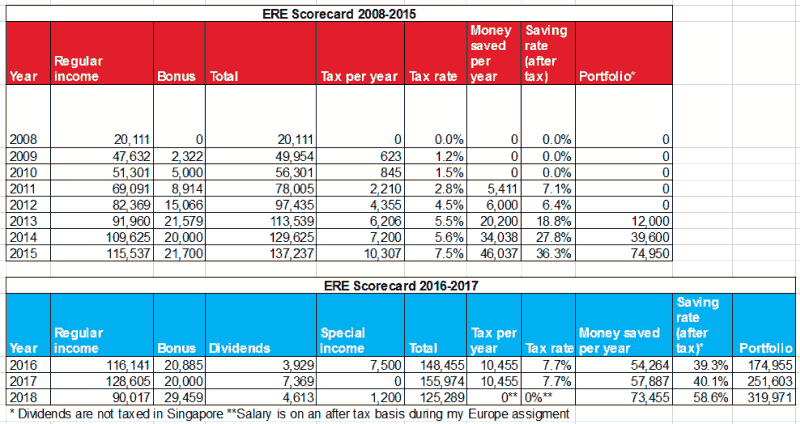

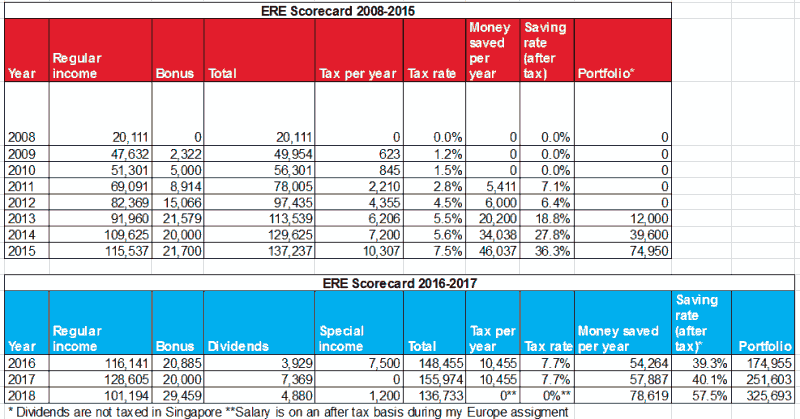

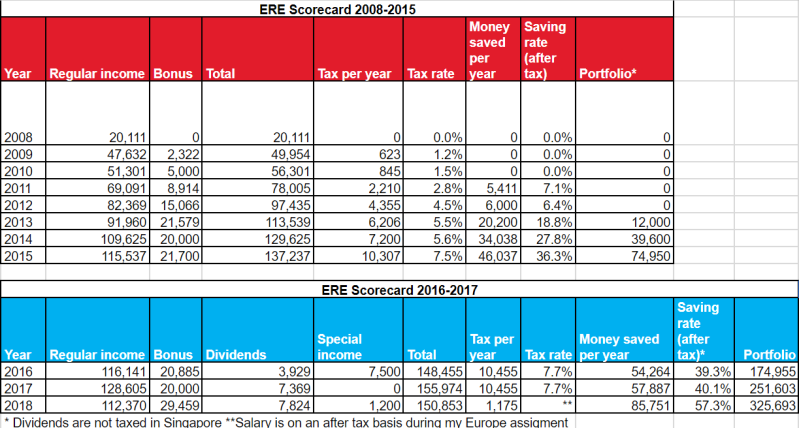

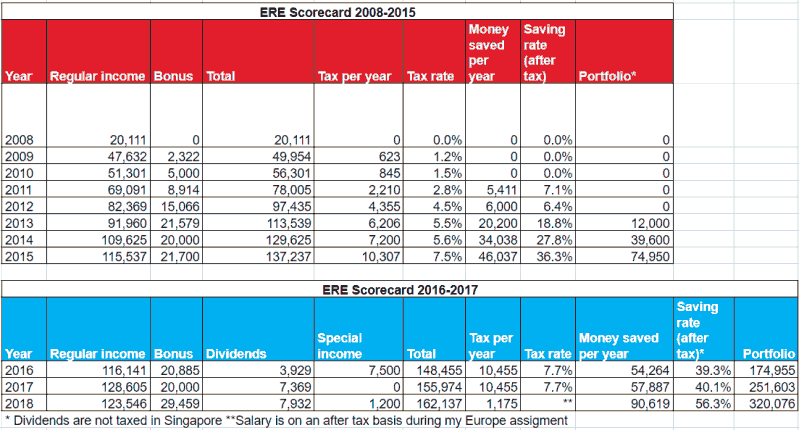

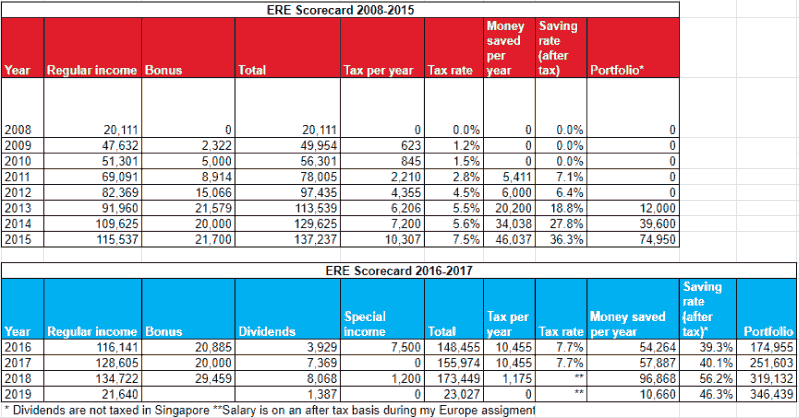

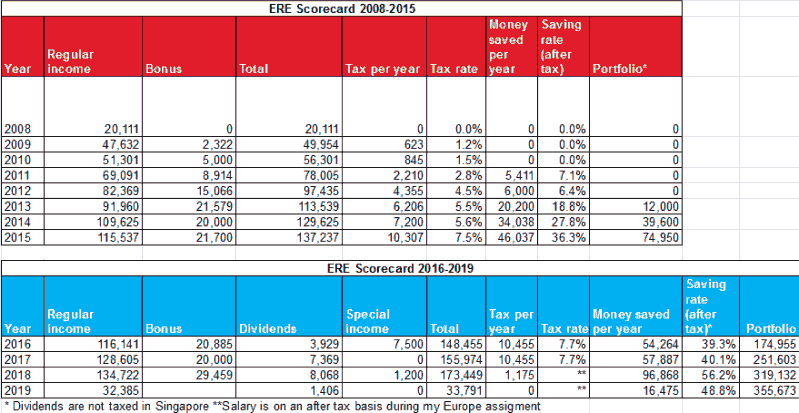

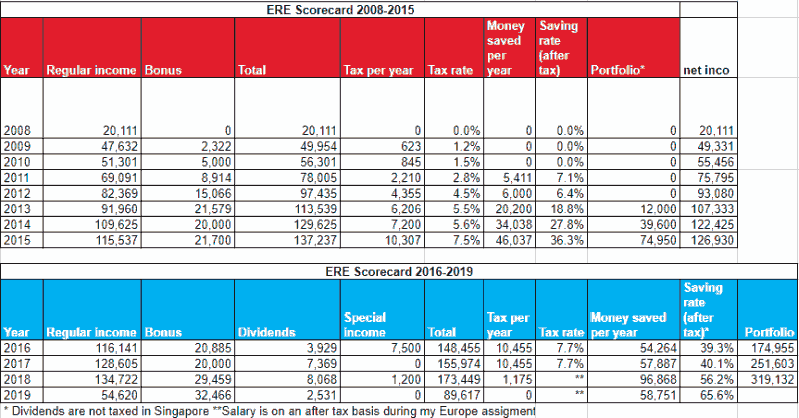

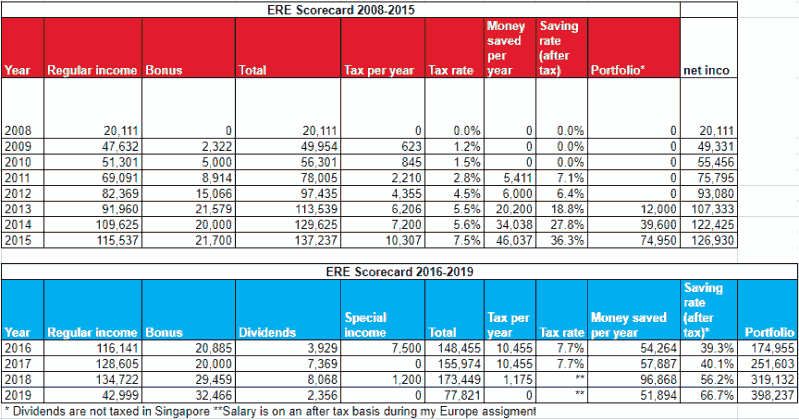

ERE Scorecard

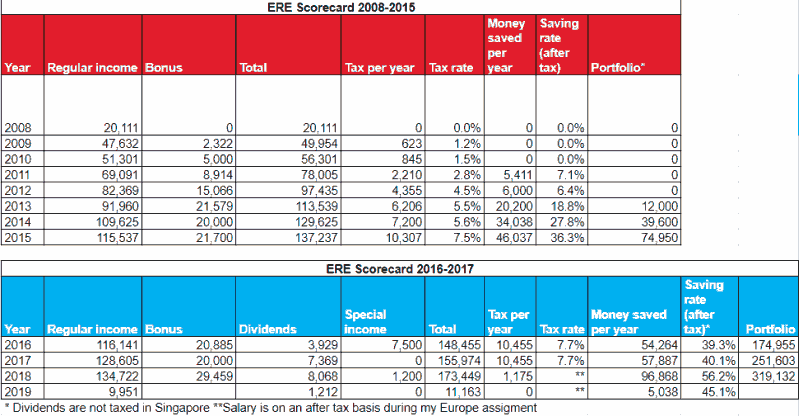

Saving rate in April was

80%. I did not spend all the rest, but buffered some for future months.

April month is bonus month, where many colleagues just spend a lot of money. In Europe this is far less pronounced than in Singapore - I did not hear any discussions on how to spend the bonus as fast as possible. As always I just invested the whole bonus. I received a 30% on top of the normal bonus, because of so called “outstanding performance”. My performance was average in my opinion, but I appreciate the money. It helped, because the company did poorly and normal bonus was lower than last year.

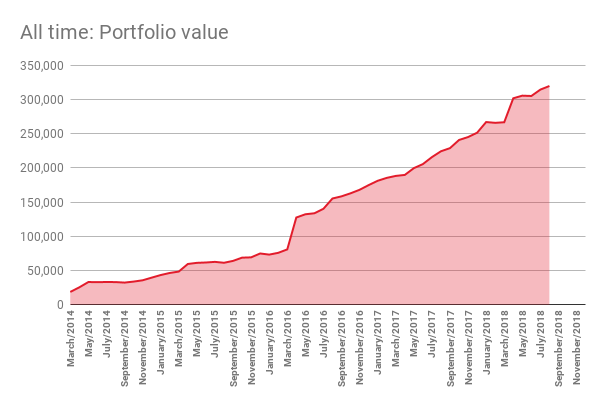

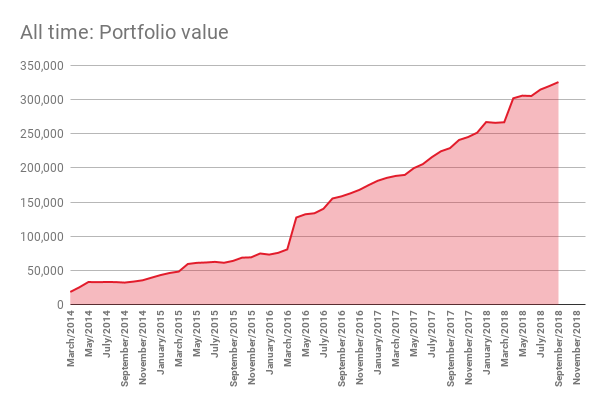

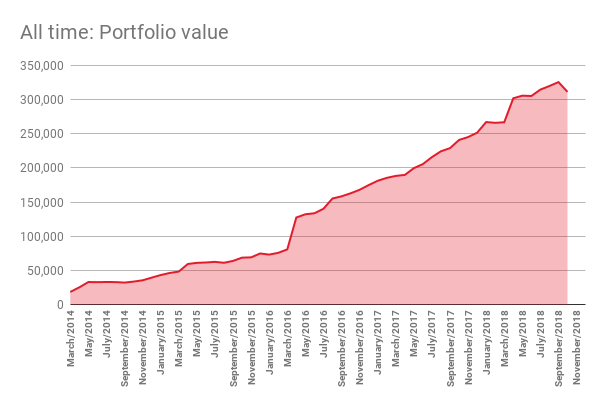

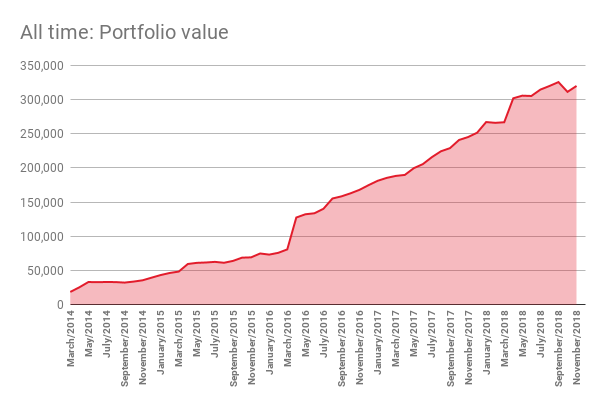

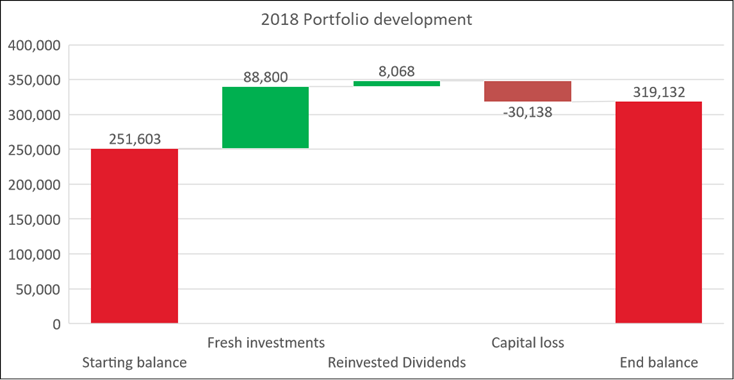

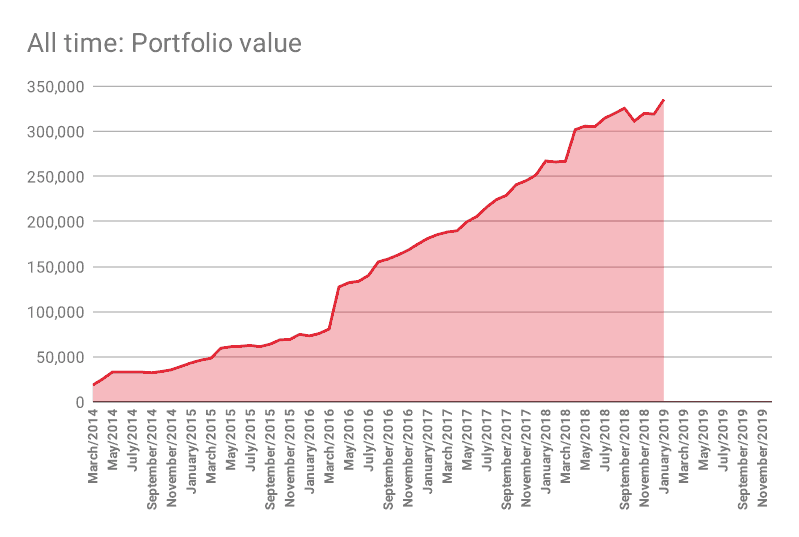

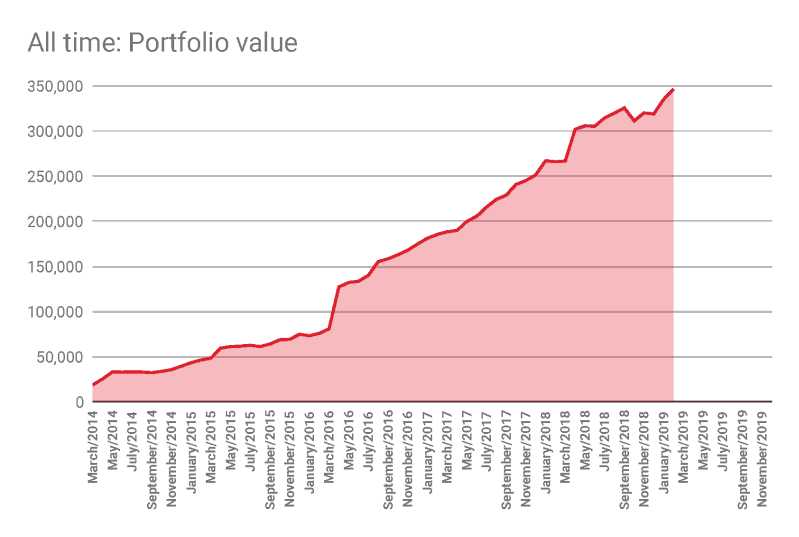

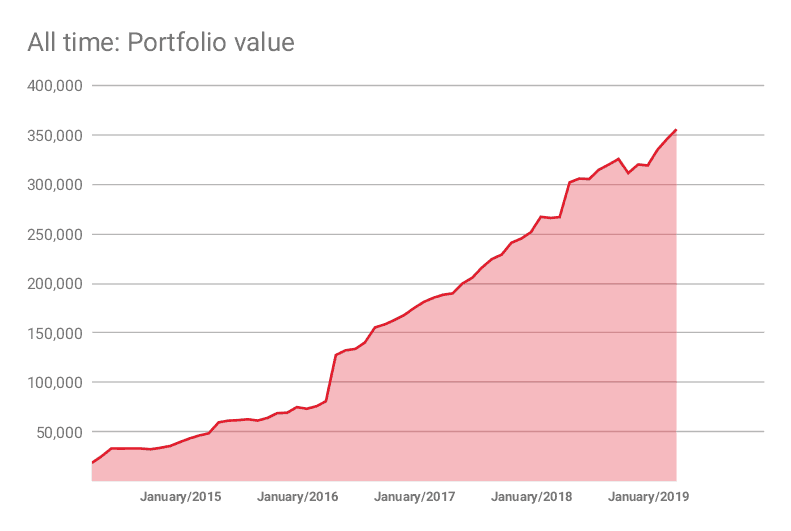

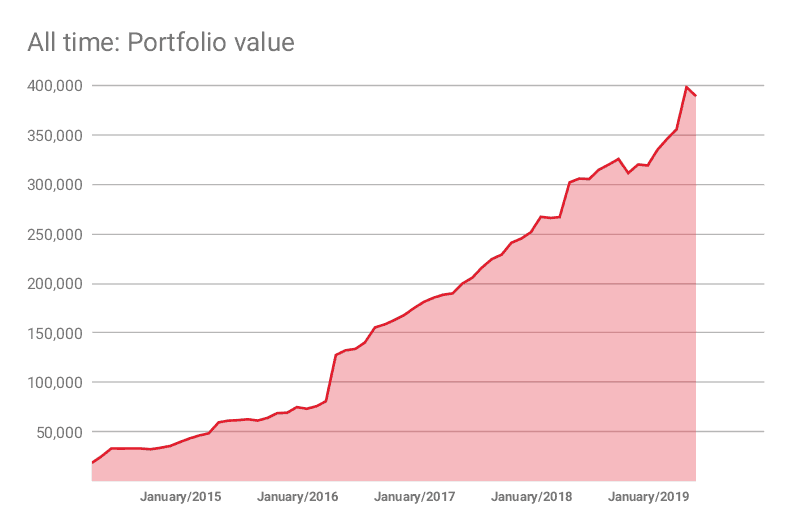

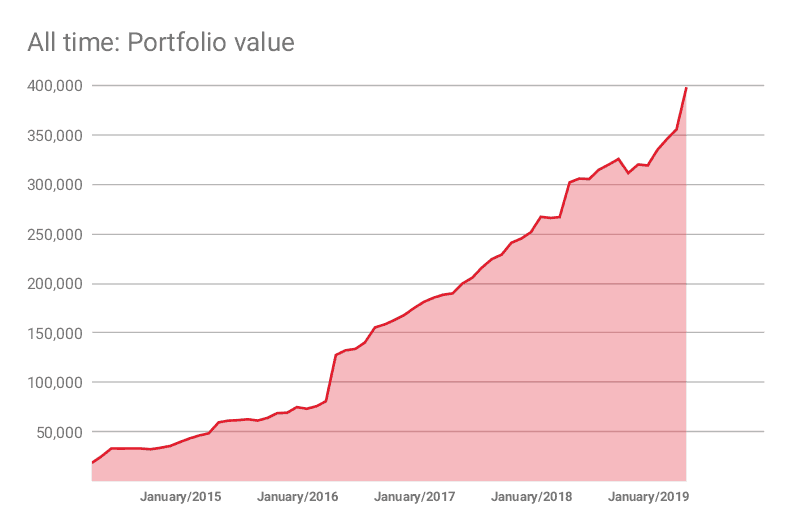

Portfolio update

Portfolio increased by

SGD 42,564 to

SGD 398,237 (USD 292,500). Fresh investments of

SGD

35,419 and gains of SGD 7,145 contributed.

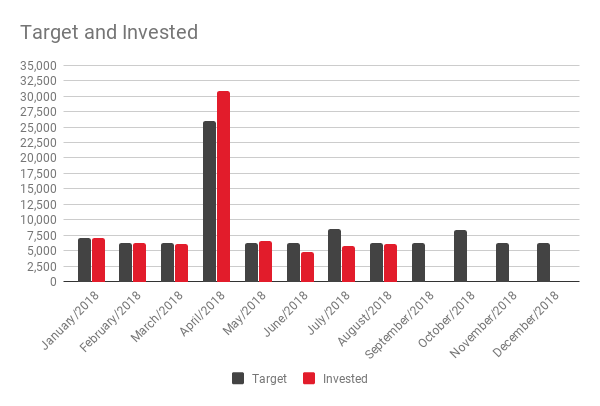

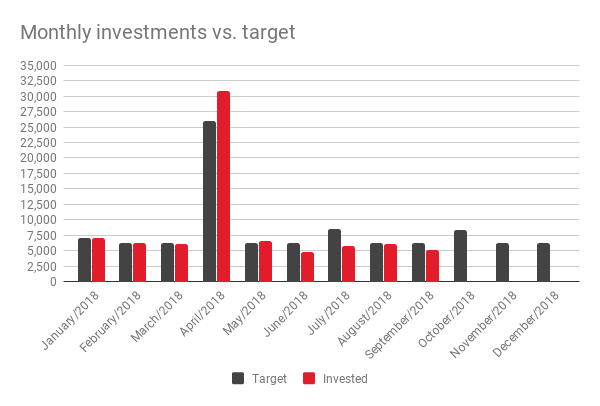

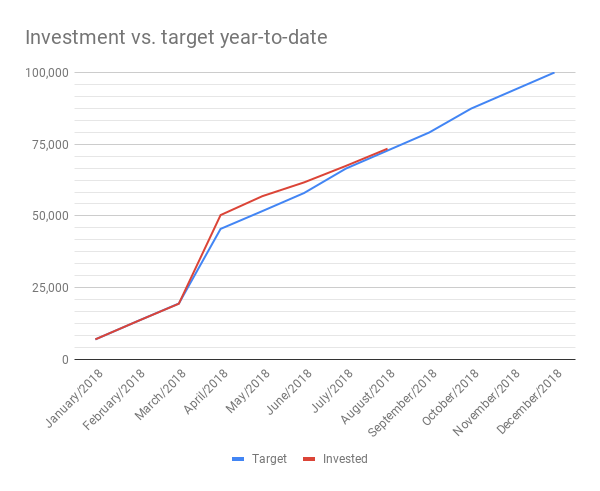

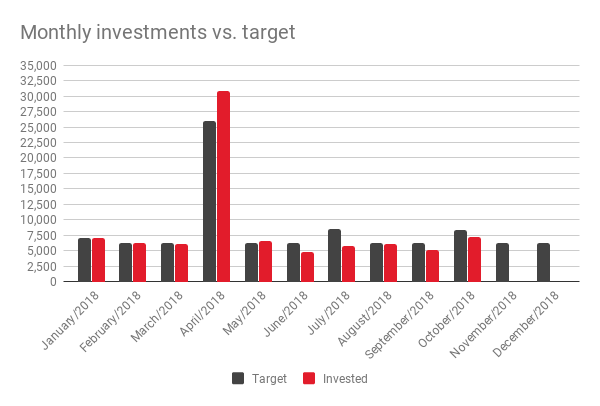

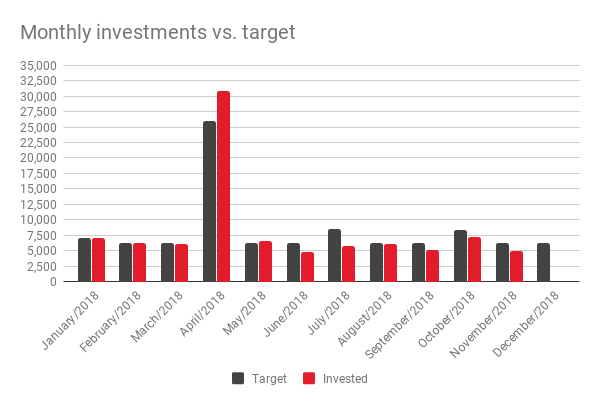

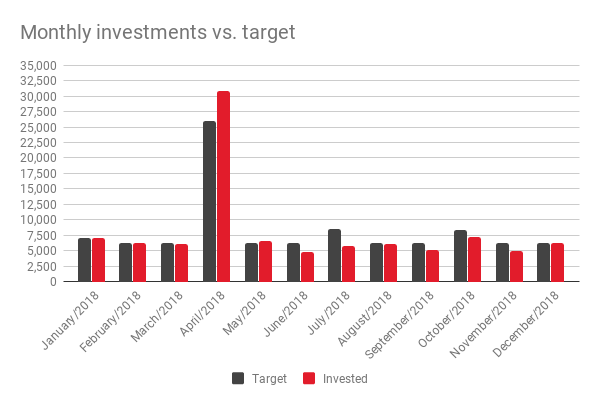

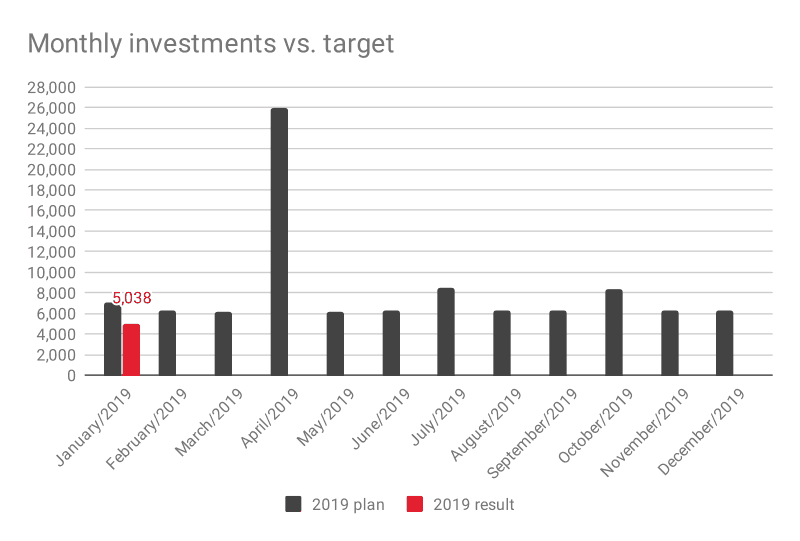

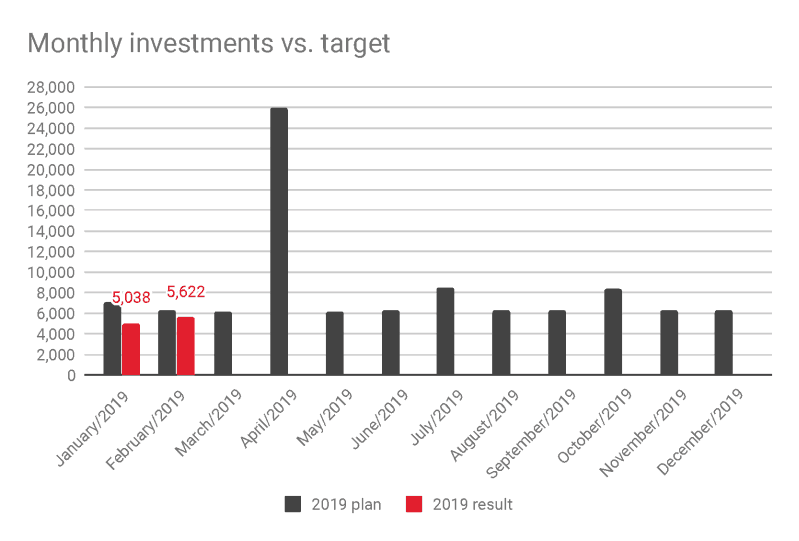

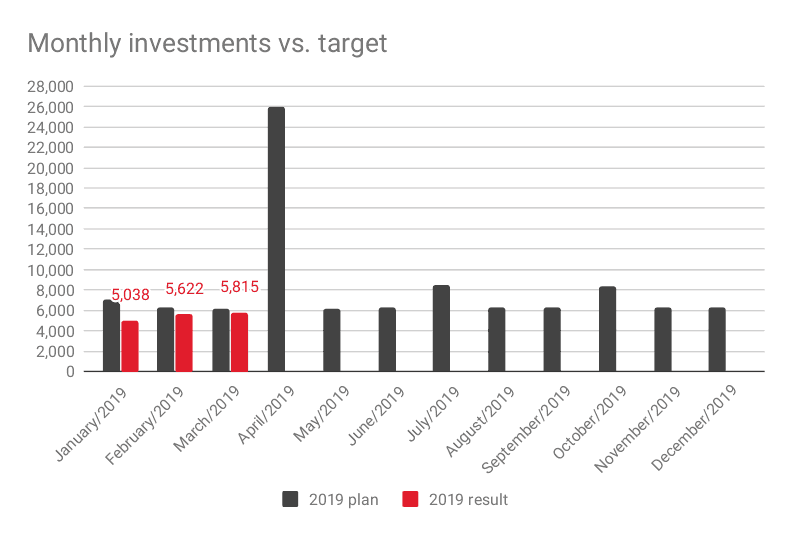

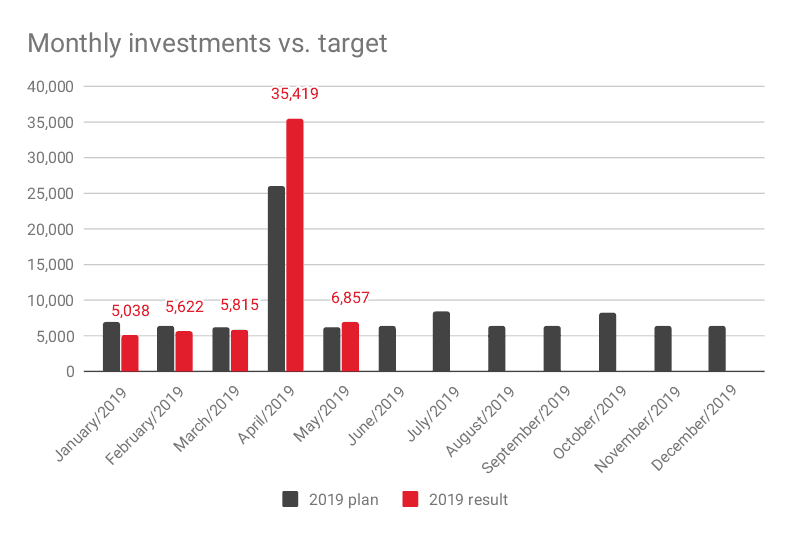

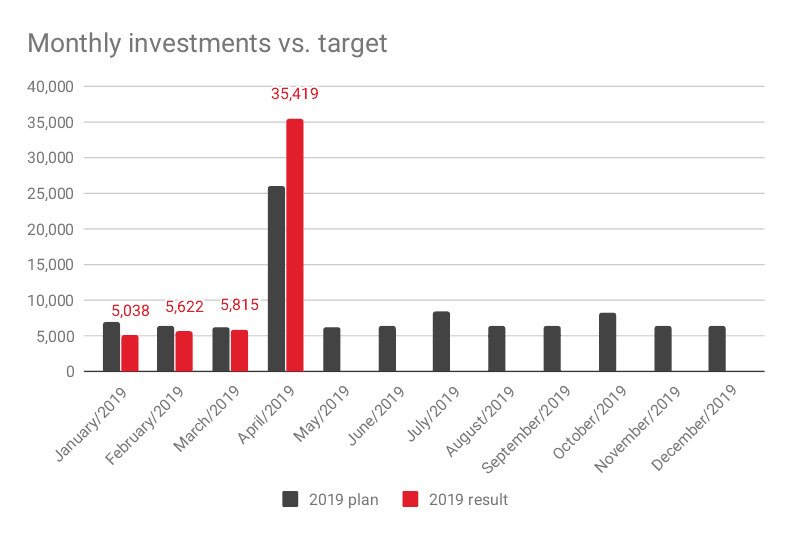

Investments vs. plan

I invested

SGD 35,419 into my portfolio which was quite a bit more than planned (

SGD 26,000). This helped me catch up with the weak first three months and I am now ahead of my savings plan again.

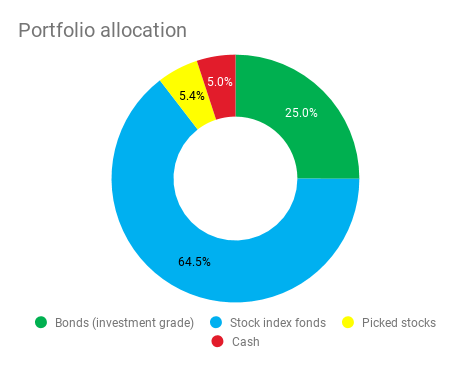

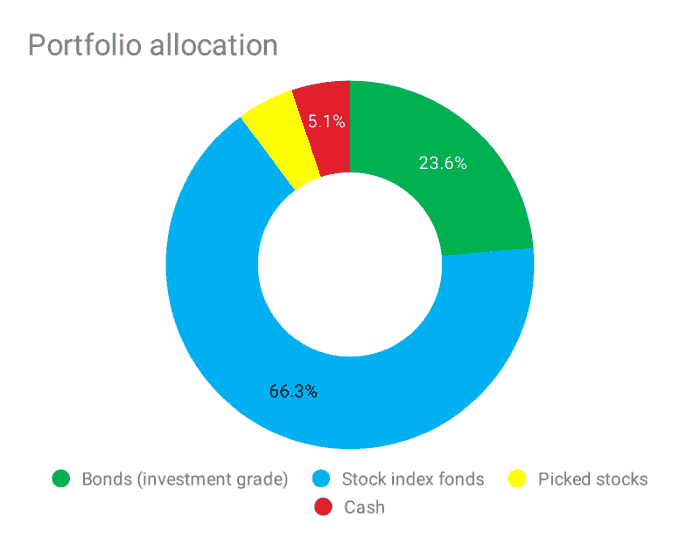

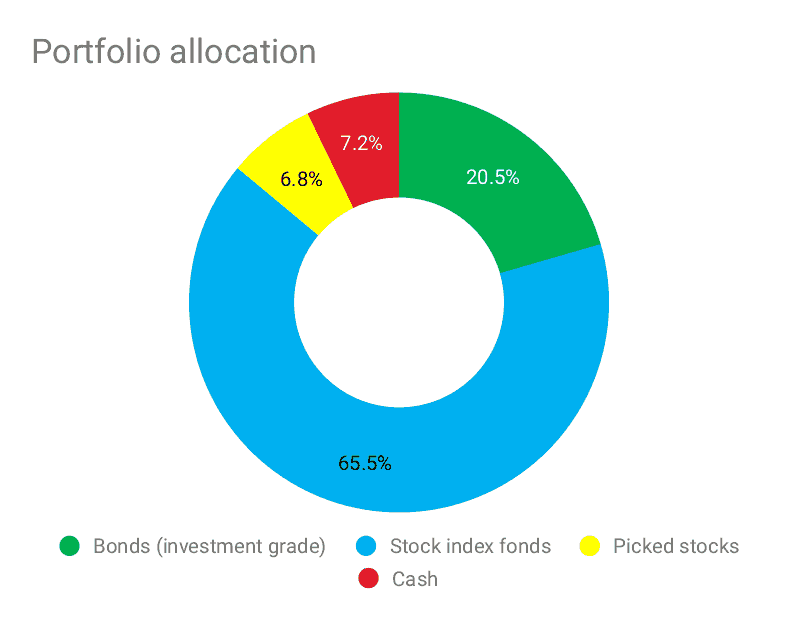

I am a bit worried about the market valuation and optimism in the last few months. Thus I kept some of my new inflows in cash. Asset allocation is currently as follows:

I am also getting light on bonds, which I cannot tax efficiently buy here, because of the EU regulation on PRIIPs. My Singaporean broker does not allow me to buy ETFs anymore, only single stocks and REITs.

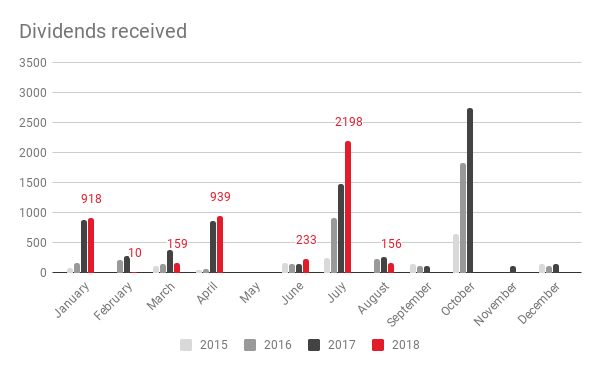

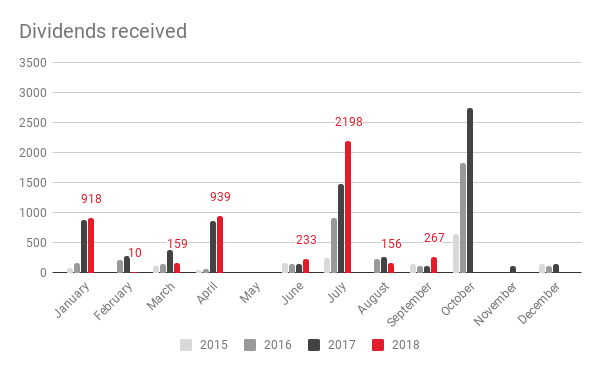

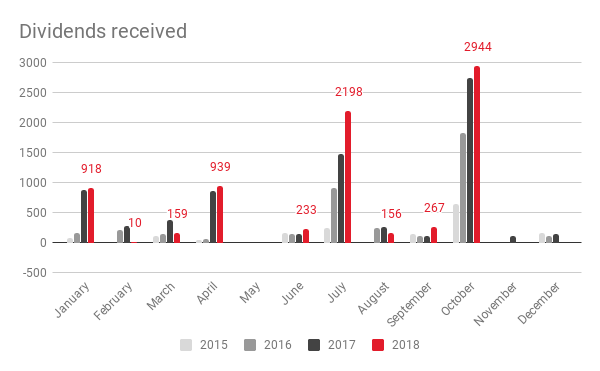

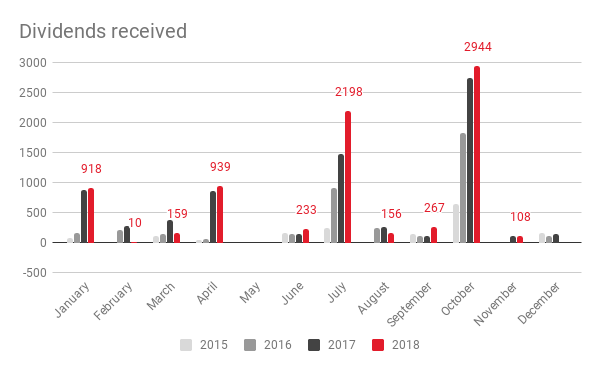

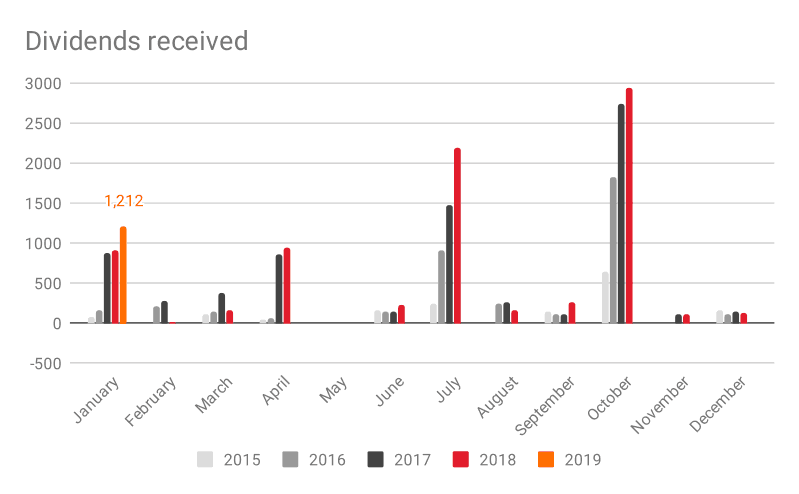

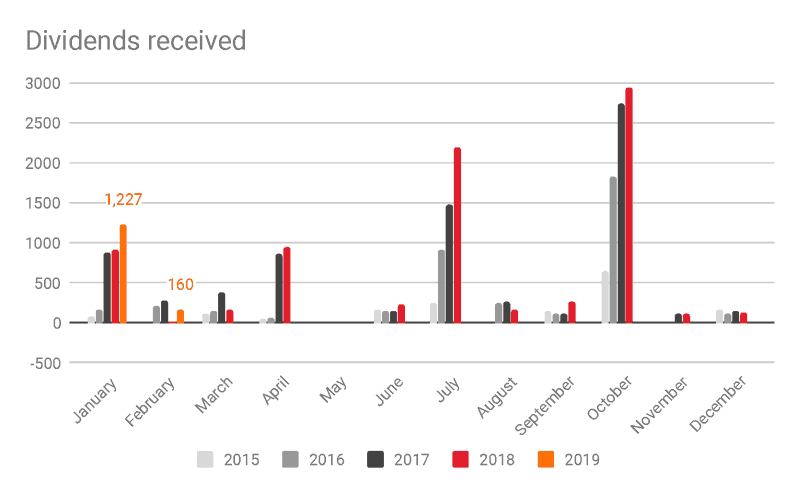

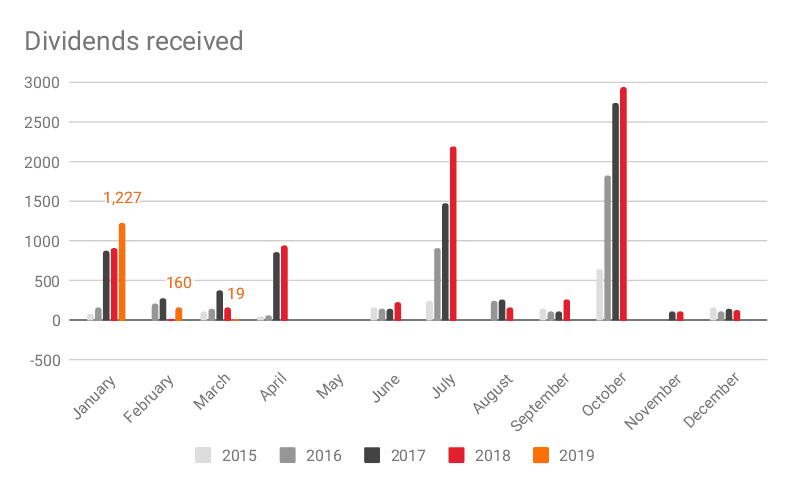

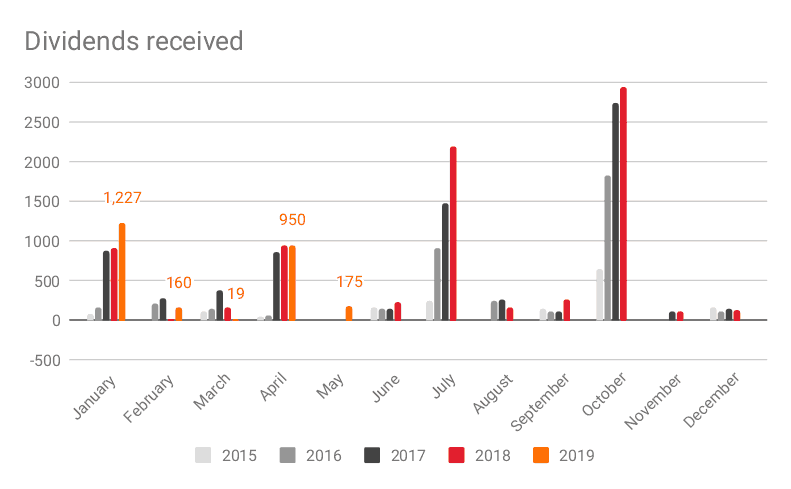

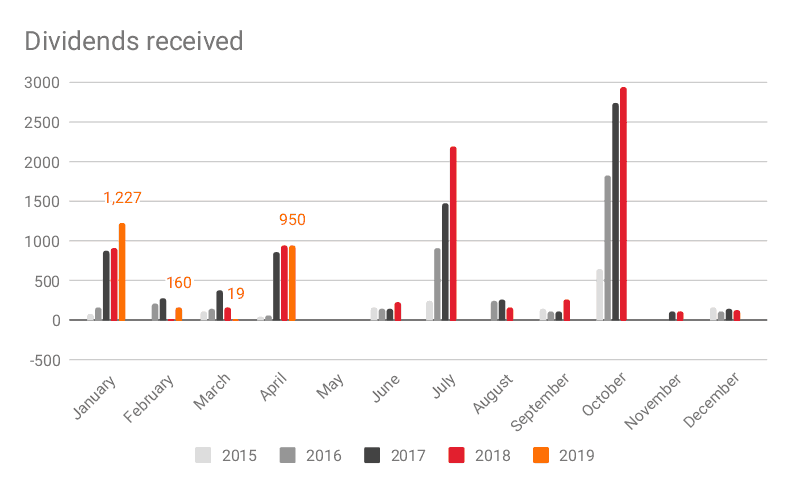

Dividends received

SGD 950.

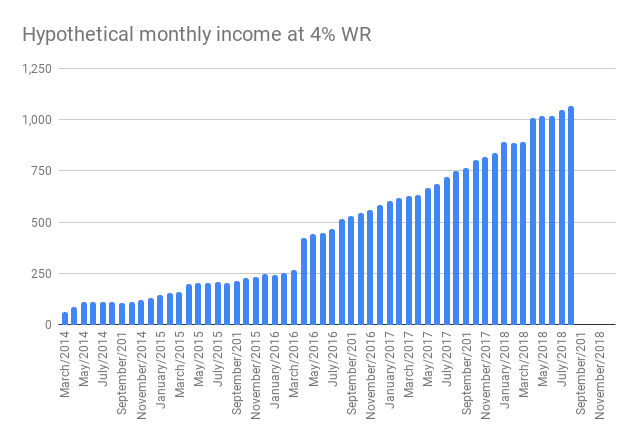

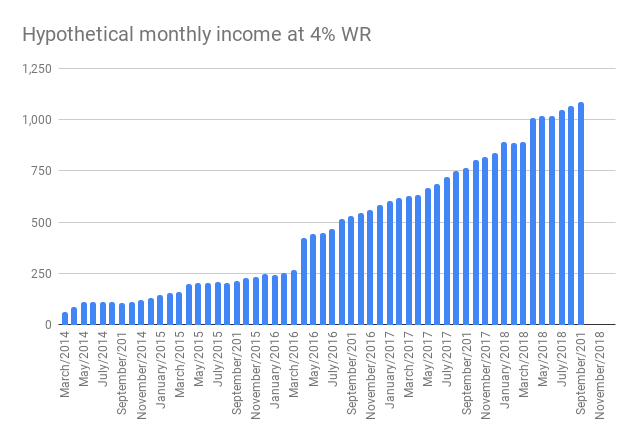

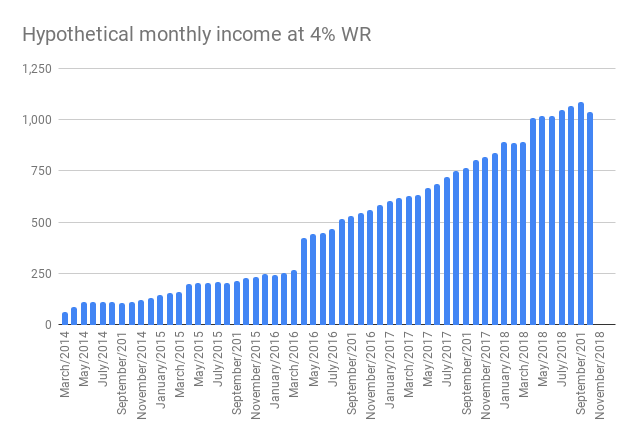

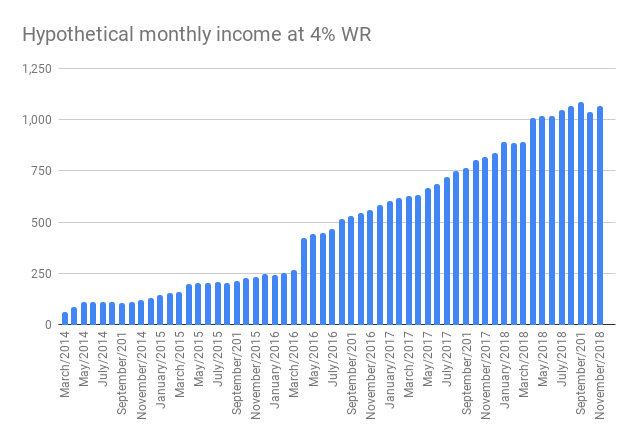

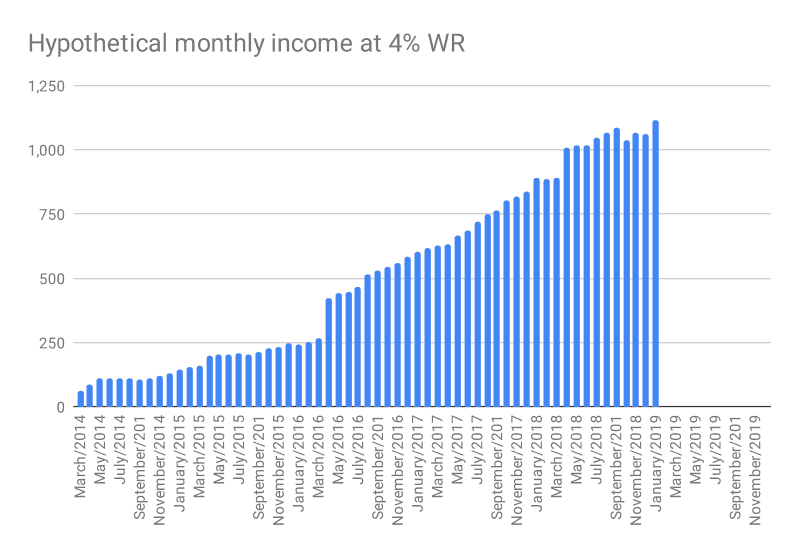

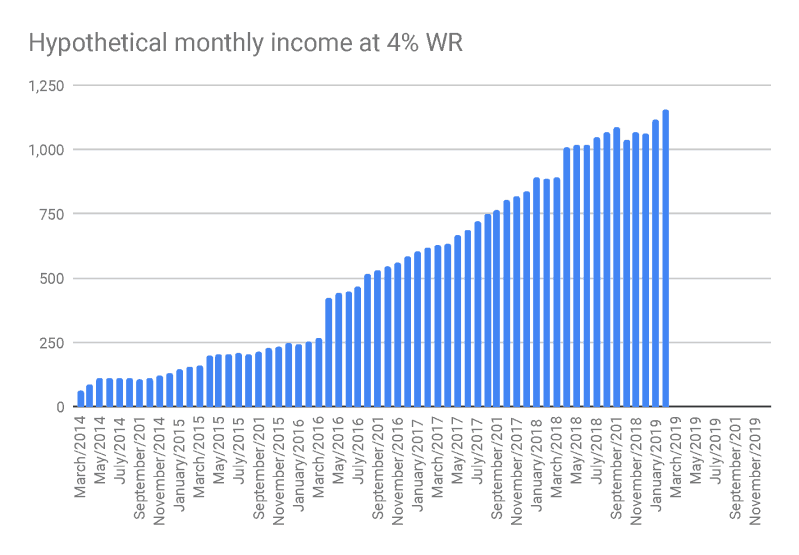

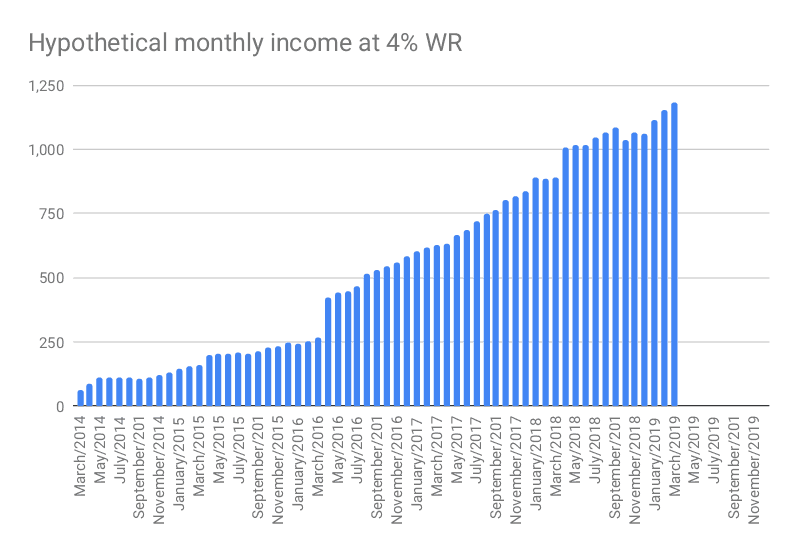

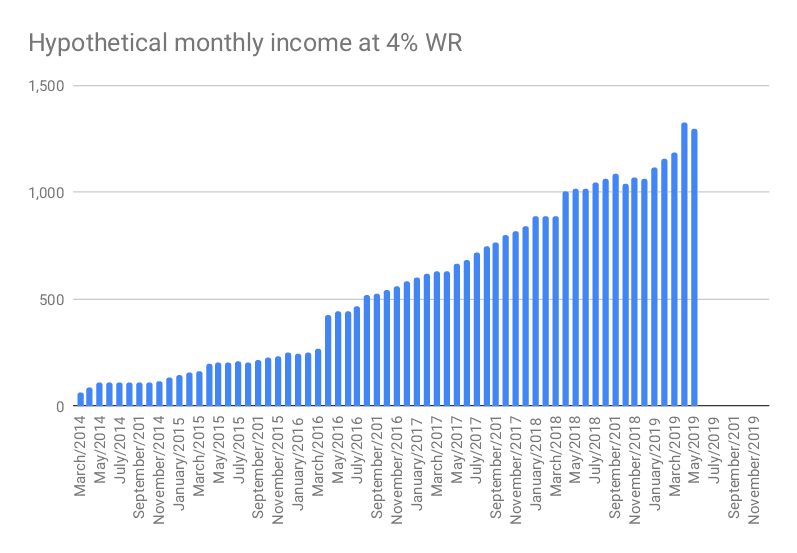

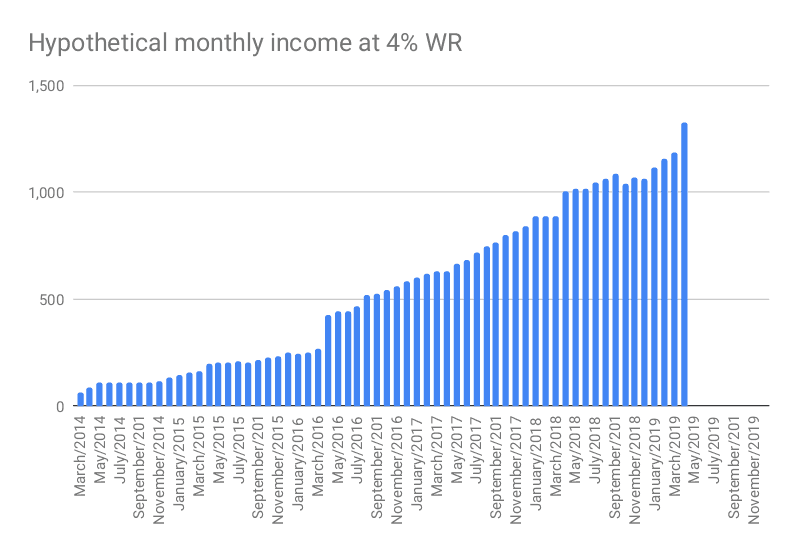

Hypothetical monthly income

SGD 1,372.

SGD 950.

Hypothetical monthly income

SGD 1,372. Getting closer and closer to the magical EUR 1,000 mark (SGD 1,530)

Early retirement: funding secured!

Early retirement: funding secured!

Assuming an annual growth of current portfolio of 6% and inflation at 2% per year I could retire at the age of 66. German official retirement age is 67 so I have officially paid for my somewhat early retirement

Feels like quite a big deal!

Moreover my portfolio would support monthly income of EUR 2,500 in today’s Euros. Someone who always paid into the German state-run retirement scheme while working non-stop for 45 years would only receive EUR 1,400 before tax. So my early retirement would be quite cushy.

Outlook

It seems like I got a bit of salary increase - not sure how much, but it seems like about EUR 300 / month or so. Will see in May. Needless to say, lifestyle inflation will be avoided!