Monthly update #30: December and full year 2017

Posted: Thu Jan 04, 2018 10:27 am

Another year has passed and this is already my 30th entry.

The complete embarrassment: monthly goal review

- 20 days no alcohol: 13 days - failed completely, thanks to Christmas parties.

- 12 times sport: 9 times - failed due to laziness

Calories in > calories out, thus I gained 2.5 kgs in just one month. Horrible.

In January I will change the behavior to stick to the goals and eat healthily inside the calory limit.

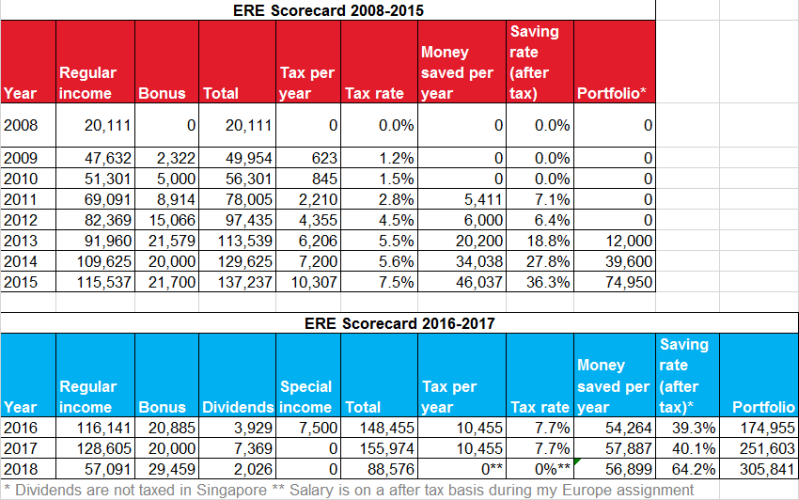

ERE Scorecard:

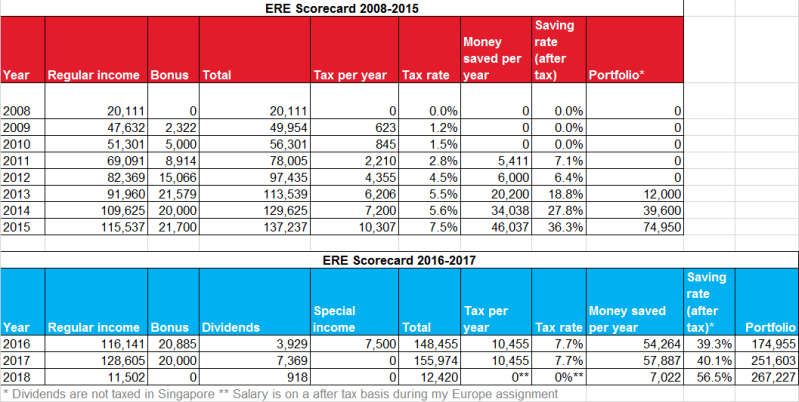

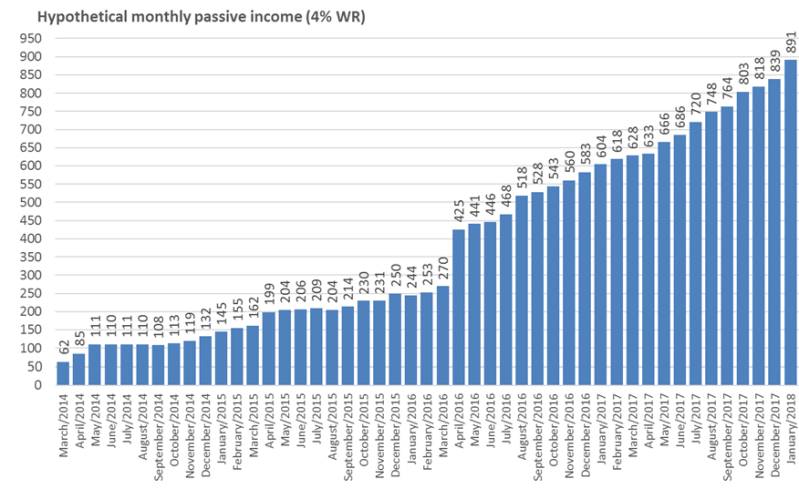

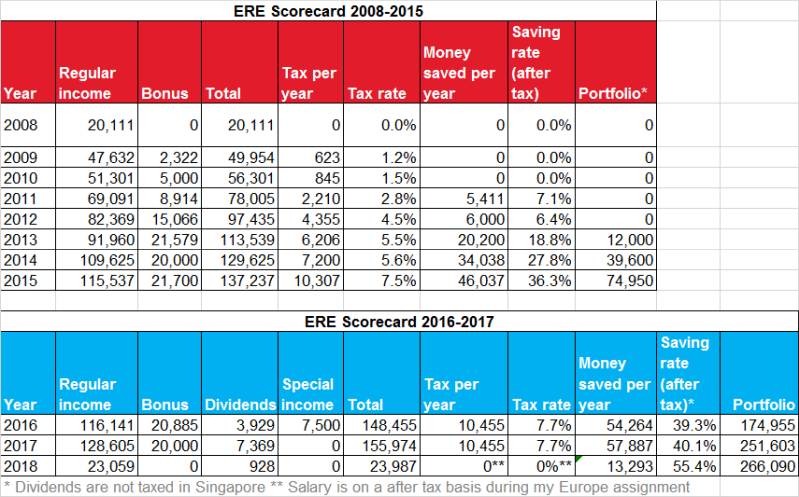

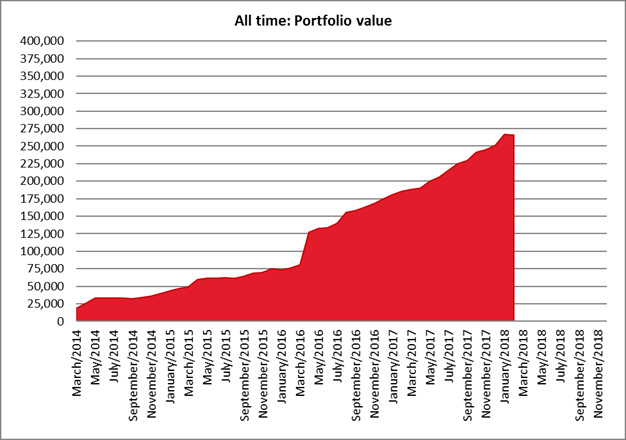

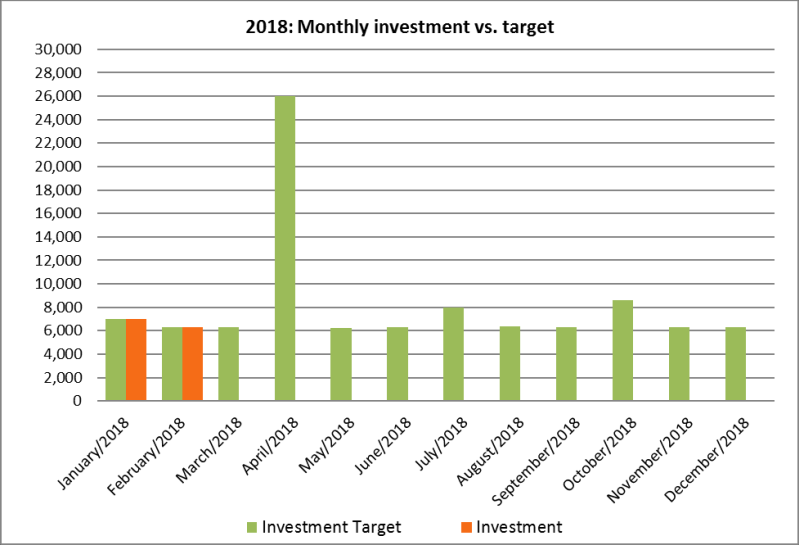

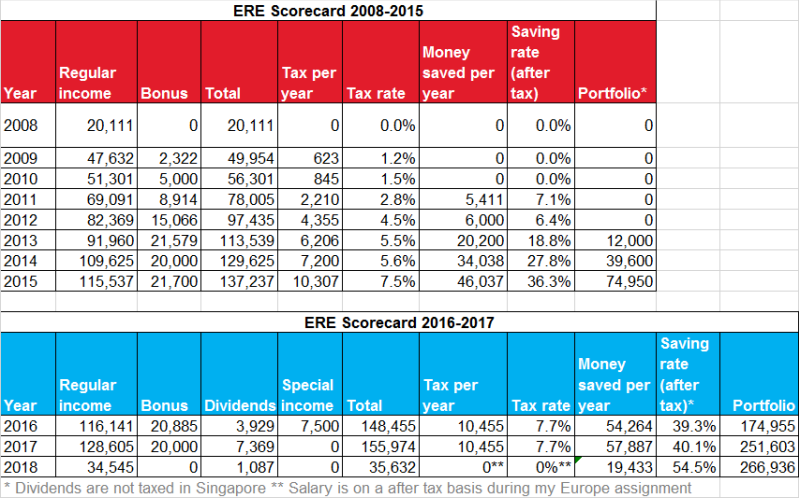

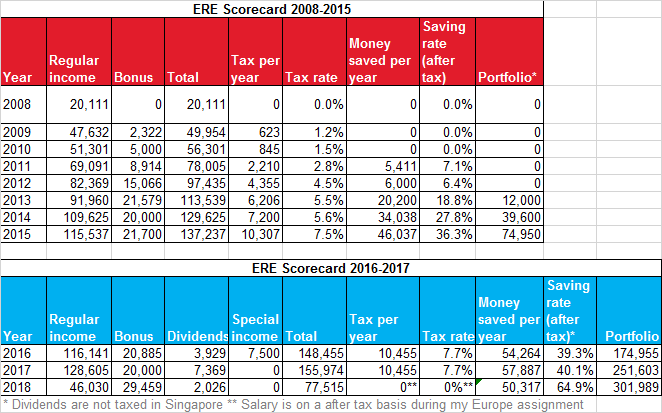

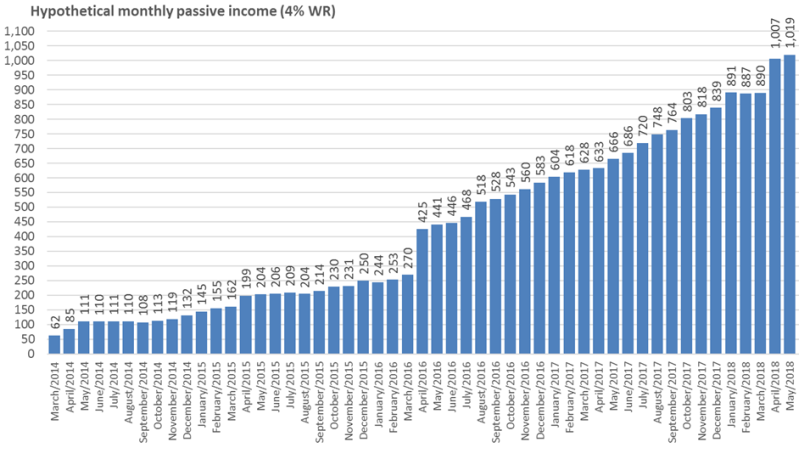

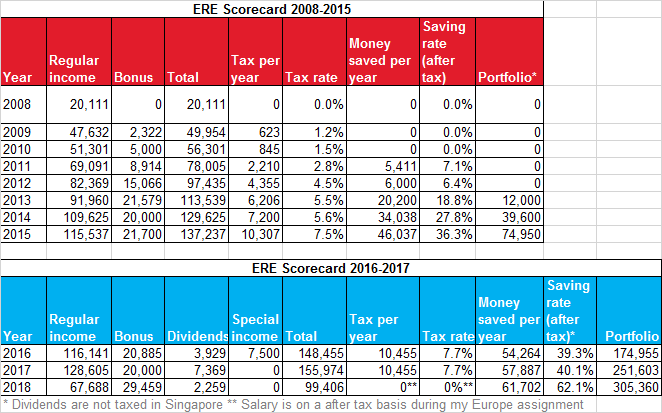

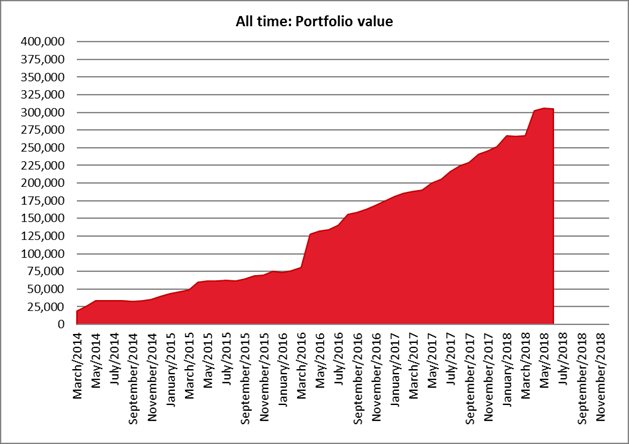

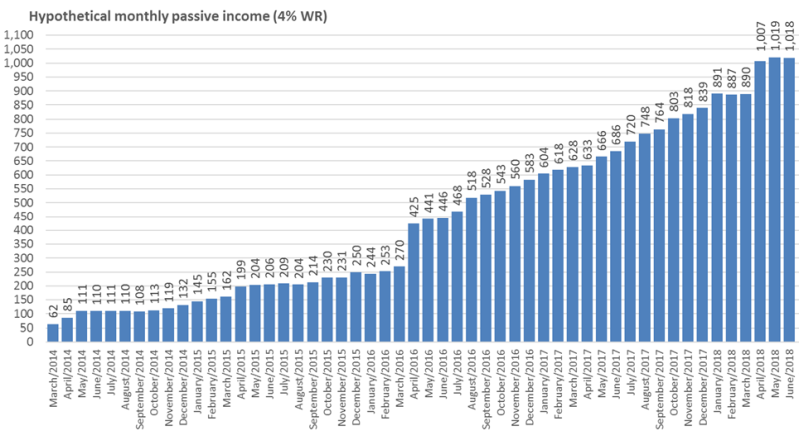

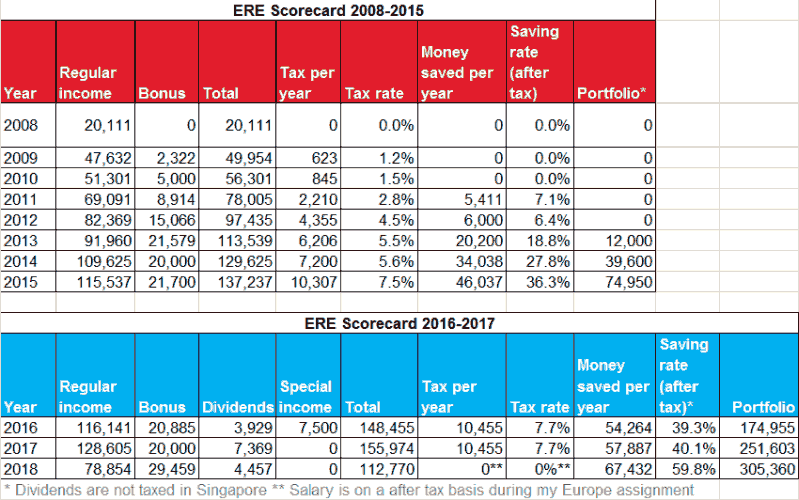

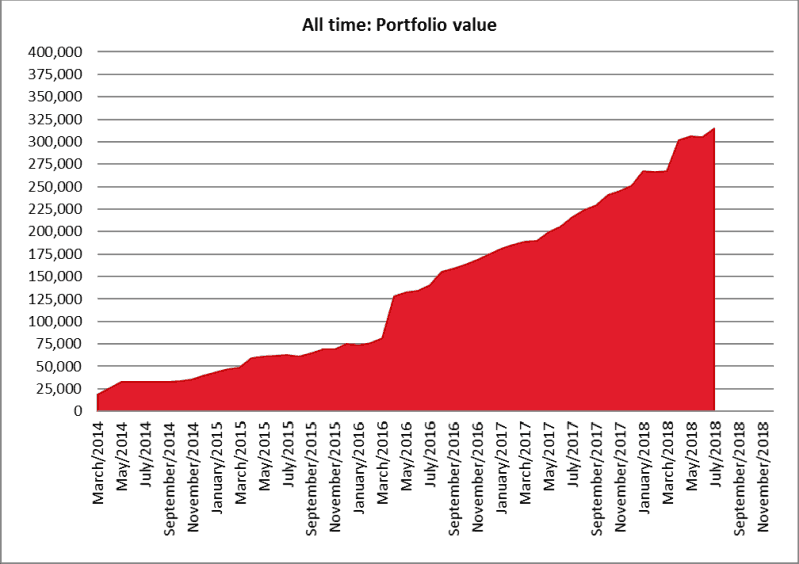

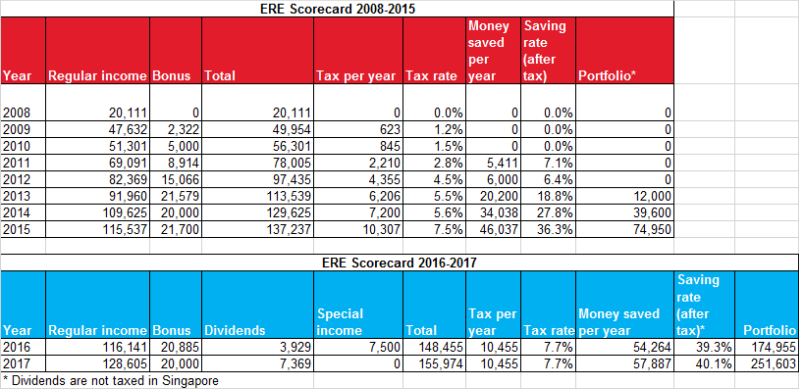

In December I invested 53% of my income, bringing the yearly savings rate to SGD 40.1%.

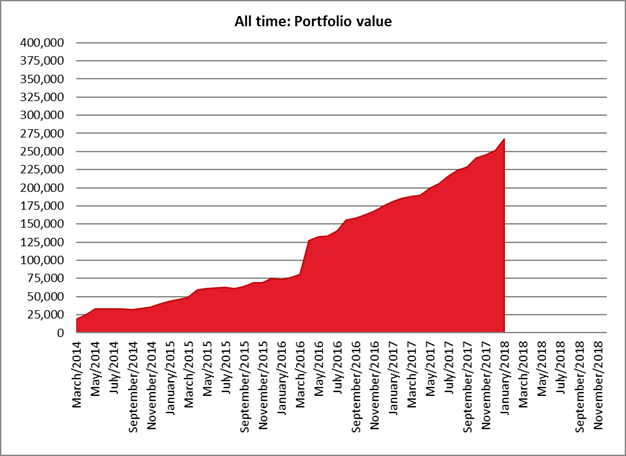

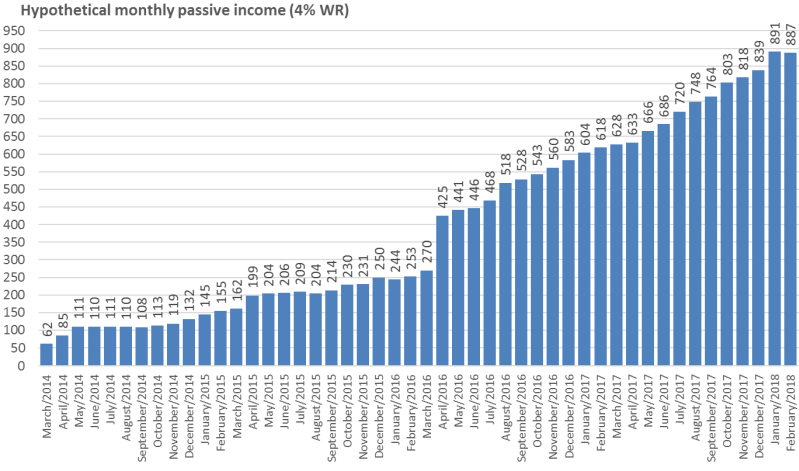

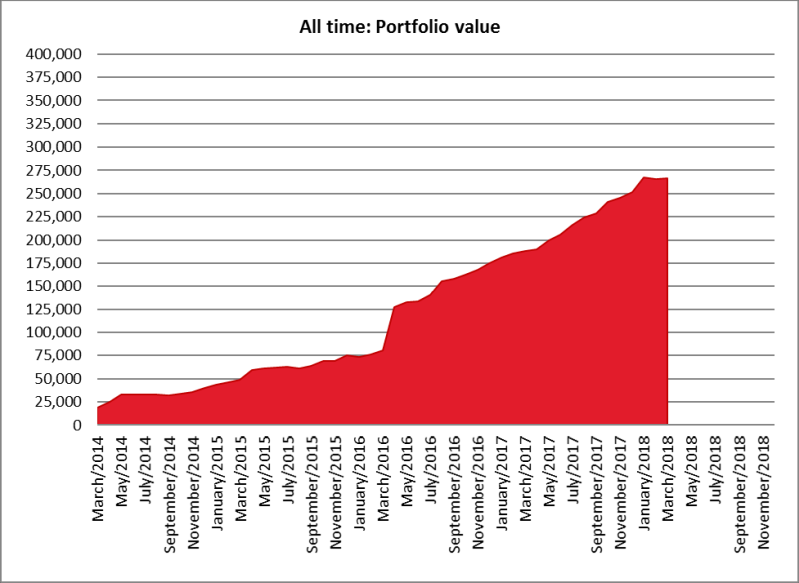

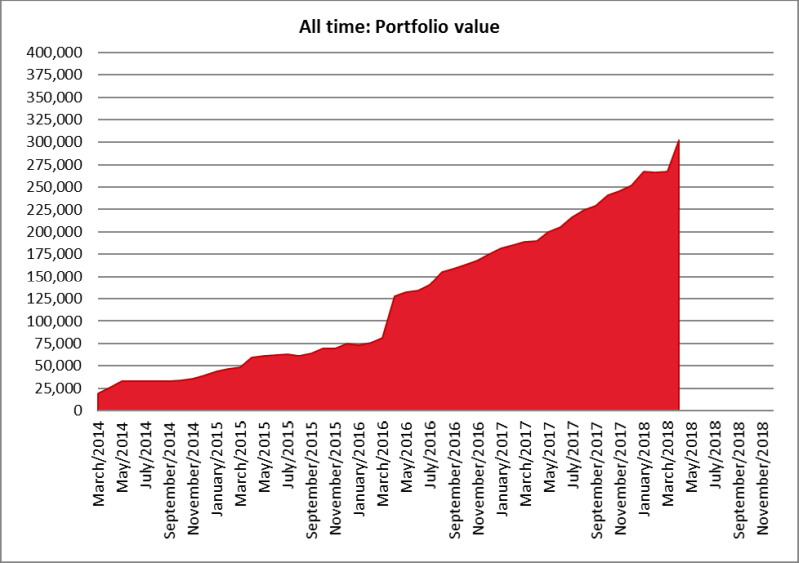

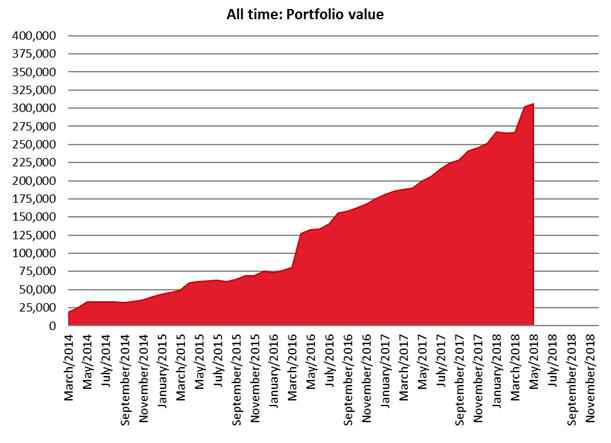

My portfolio ended the year at SGD 251,603 (USD ~189,400), a gain which was made up of SGD 6,035 in fresh investments and paper gains of SGD 289.

_______________________________________________________________________________

Yearly review 2017

I made it!

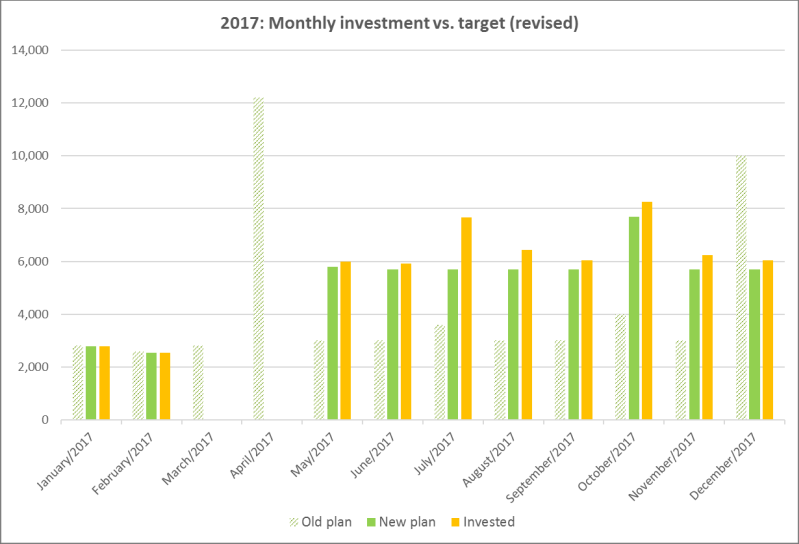

2017 goal: invest SGD 53,000

2017 result: invested SGD 57,887 (+SGD 4,887)

(1 SGD = 0.75 USD)

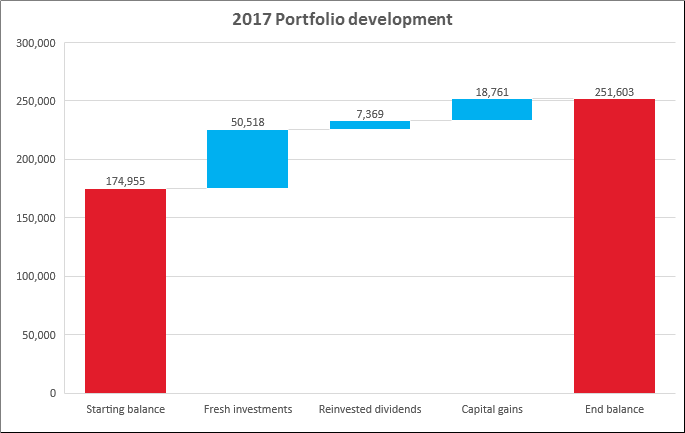

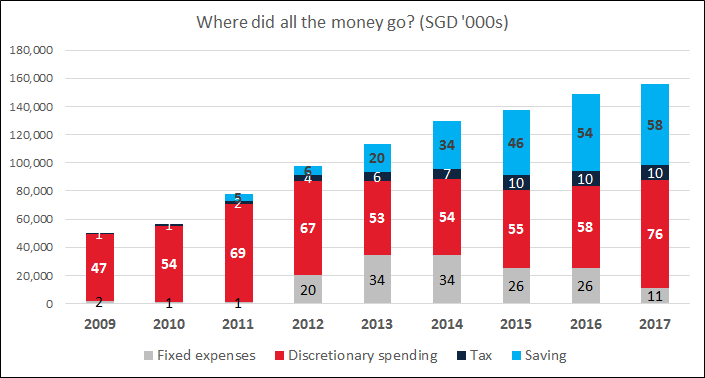

I could not resist creating a waterfall chart:

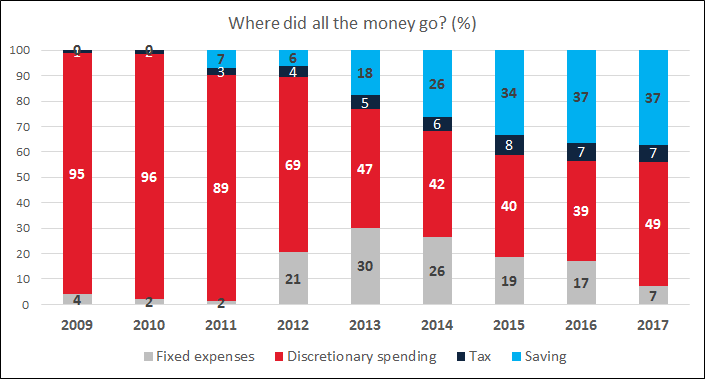

Where did all my money go?

These are by far my favorite charts. Unfortunately, 2017 saw a huge increase in discretionary spending. I spent around SGD 18,000 more than last year! Behind this shocking figure there are a lot of one time costs because of my move to Europe. I bought a lightly used car in cash (SGD 19,400) and spent around SGD 5,400 on furniture and household stuff. Too much!

In 2018 I expect this figure to go down.

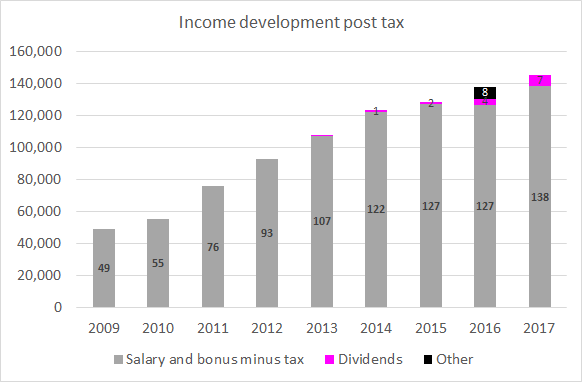

Income development – after tax

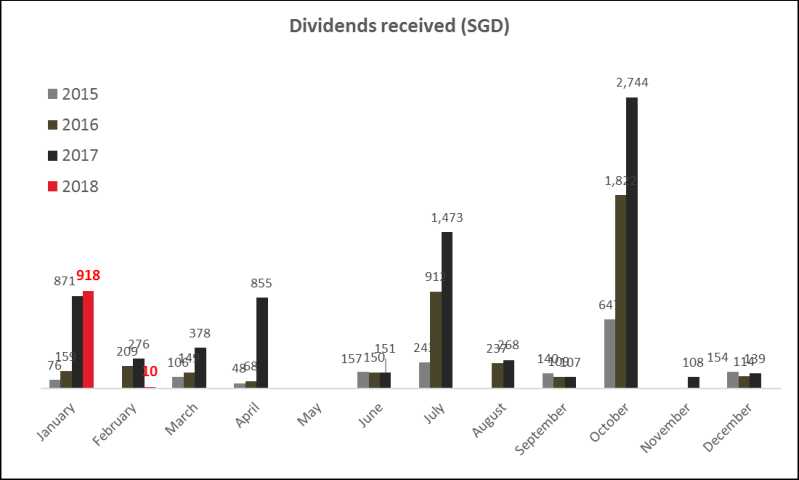

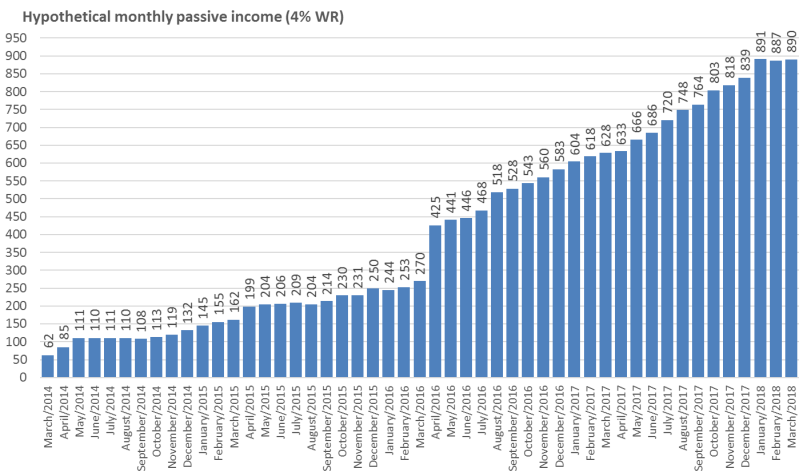

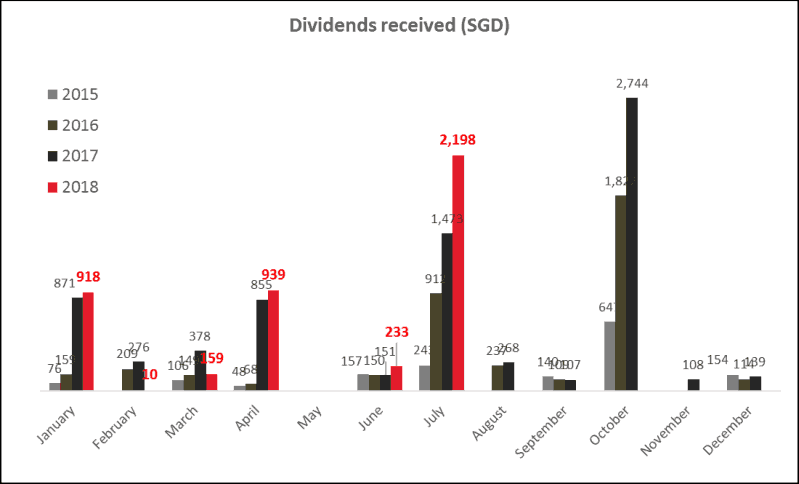

Salary has grown nicely. 2018 is probably going to be a good year, thanks to expat benefits and hopefully a higher bonus. Dividend growth is accelerating and should make up quite a sizeable chunk in a few years or so.

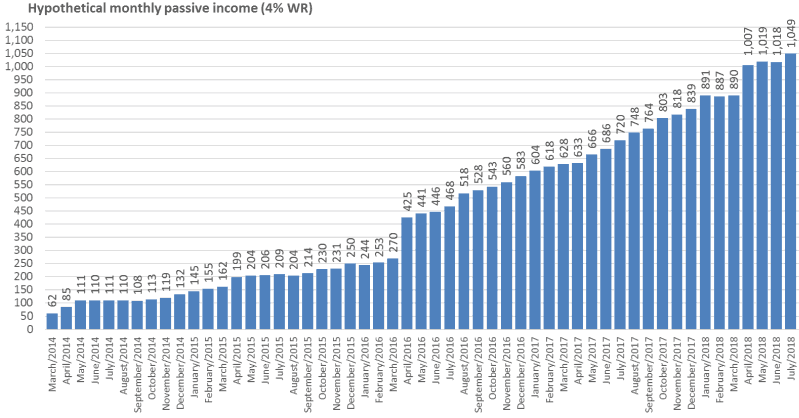

Should I be able to stick it out under current conditions I should be financially independent sooner than I had hoped.

Goals for 2018

It is time to finally commit to the ERE ways and this forum with a proper saving rate goal:

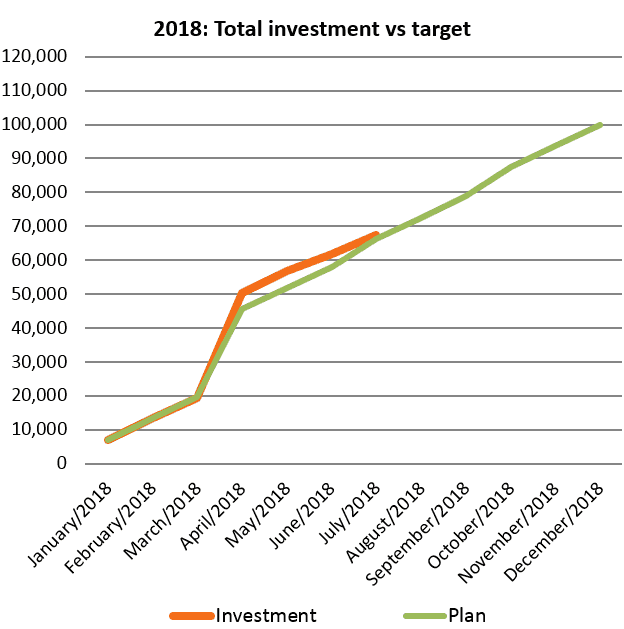

Saving goal: My plan is to save SGD 100,000 (~USD 75,000) this year. This will mean a saving rate of around 60-65%.

Quite a step up from my earlier goals. It will require quite some discipline to get there.

Discretionary spending goal: Discretionary spending should be reduced to below SGD 50,000 (~SGD 26,000 less than this year). I admit it is still ridiculously high, but <insert excuses here>

Life goal 1: Find a new job outside the company I currently work in

Life goal 2: 240 days no alcohol, 144 days sport

Life goal 3: be fluent in French

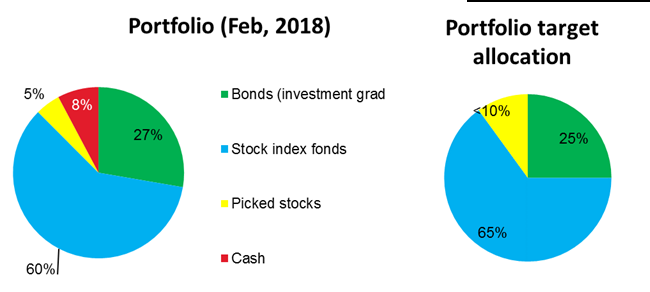

Outlook – freaking out at the markets

Equity prices feel way too high. I know the whole theory about not timing the markets, but cannot help it much.

What will I do to fight this feeling?

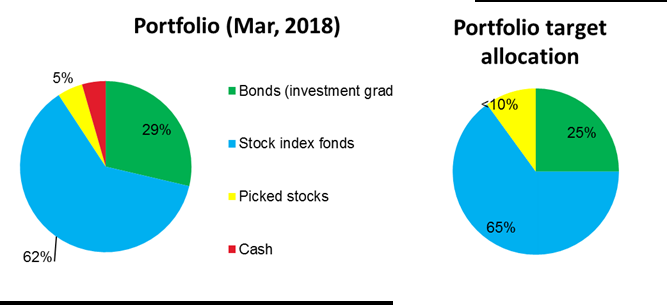

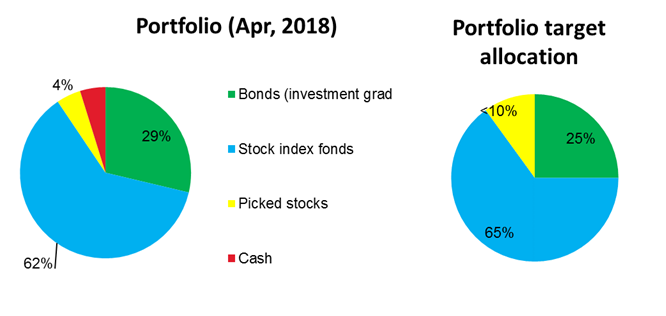

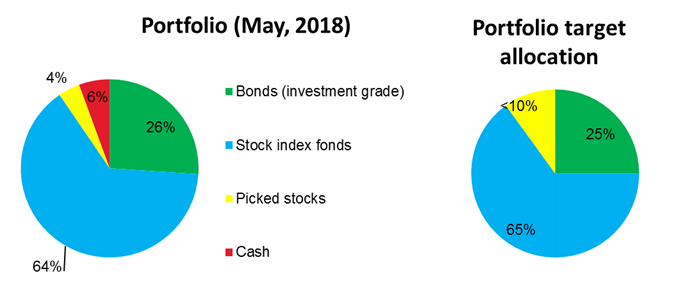

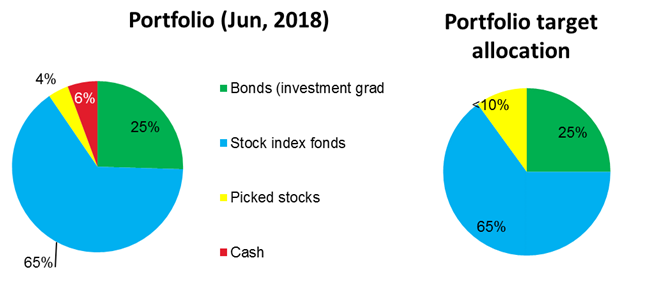

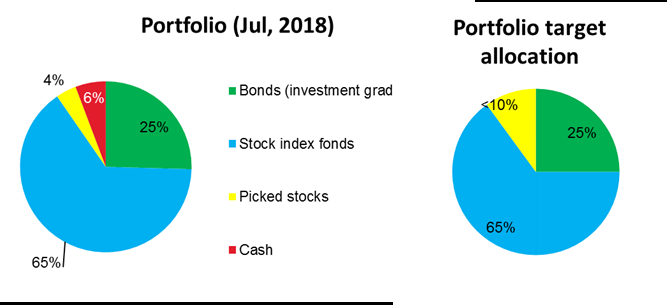

- Increase cash allocation: Currently I have only 0.5% of my portfolio in cash, but will increase this a little bit, to maximum 5-10%.

- Stay the course for the rest of the portfolio

- Eliminate all unnecessary spending and avoid the exuberant mindset that sets in when incomes increase and the mood is good in the company

- Try to use the economic boom phase to find a new job with a better company

- Further reduce clothes and other possessions to reduce stress

The complete embarrassment: monthly goal review

- 20 days no alcohol: 13 days - failed completely, thanks to Christmas parties.

- 12 times sport: 9 times - failed due to laziness

Calories in > calories out, thus I gained 2.5 kgs in just one month. Horrible.

In January I will change the behavior to stick to the goals and eat healthily inside the calory limit.

ERE Scorecard:

In December I invested 53% of my income, bringing the yearly savings rate to SGD 40.1%.

My portfolio ended the year at SGD 251,603 (USD ~189,400), a gain which was made up of SGD 6,035 in fresh investments and paper gains of SGD 289.

_______________________________________________________________________________

Yearly review 2017

I made it!

2017 goal: invest SGD 53,000

2017 result: invested SGD 57,887 (+SGD 4,887)

(1 SGD = 0.75 USD)

I could not resist creating a waterfall chart:

Where did all my money go?

These are by far my favorite charts. Unfortunately, 2017 saw a huge increase in discretionary spending. I spent around SGD 18,000 more than last year! Behind this shocking figure there are a lot of one time costs because of my move to Europe. I bought a lightly used car in cash (SGD 19,400) and spent around SGD 5,400 on furniture and household stuff. Too much!

In 2018 I expect this figure to go down.

Income development – after tax

Salary has grown nicely. 2018 is probably going to be a good year, thanks to expat benefits and hopefully a higher bonus. Dividend growth is accelerating and should make up quite a sizeable chunk in a few years or so.

Should I be able to stick it out under current conditions I should be financially independent sooner than I had hoped.

Goals for 2018

It is time to finally commit to the ERE ways and this forum with a proper saving rate goal:

Saving goal: My plan is to save SGD 100,000 (~USD 75,000) this year. This will mean a saving rate of around 60-65%.

Quite a step up from my earlier goals. It will require quite some discipline to get there.

Discretionary spending goal: Discretionary spending should be reduced to below SGD 50,000 (~SGD 26,000 less than this year). I admit it is still ridiculously high, but <insert excuses here>

Life goal 1: Find a new job outside the company I currently work in

Life goal 2: 240 days no alcohol, 144 days sport

Life goal 3: be fluent in French

Outlook – freaking out at the markets

Equity prices feel way too high. I know the whole theory about not timing the markets, but cannot help it much.

What will I do to fight this feeling?

- Increase cash allocation: Currently I have only 0.5% of my portfolio in cash, but will increase this a little bit, to maximum 5-10%.

- Stay the course for the rest of the portfolio

- Eliminate all unnecessary spending and avoid the exuberant mindset that sets in when incomes increase and the mood is good in the company

- Try to use the economic boom phase to find a new job with a better company

- Further reduce clothes and other possessions to reduce stress