Entry #1 October 1, 2013

Hi everyone, time to start my journal covering my journey towards early retirement.

I have just reached an important milestone – SWR 5% - and finished reading Jacob’s book last month, so now seem to be a good time to start the journal.

I’m a 35 old economist who works with accounting/finance for a real estate company. I’m INTJ and have always had the passion for “economic freedom”.

I live in Denmark - English isn’t my first language so please don’t laugh too much of my spelling and grammar errors.

GF (29) and I split all shared costs 50/50 but don’t have joint economy.

We live in a 1,250 sq. feet house – no children jet (we plan for two). Our house is close to family but both of us have to commute. Me 55 miles (public transportation) and GF 32 miles (our car).

A now for the hard numbers (all USD we use DKK but guess nobody knows the value of those..):

Breakdown monthly spending:

Interest mortgage: USD 468

Interest mortgage “savings”: USD -139 *

Savings for repayment mortgage: USD 787 *

Property taxes: USD 229

Property insurance: USD 57

Utilities (heating, water, electricity and waste disposal): USD 436

Property maintenance: USD 90

Auto – gas: USD 377

Auto taxes: USD 50

Auto insurance: USD 55

Auto maintenance: USD 83

Public transportation: USD 266

Household (food etc.): USD 541

Insurance (disability): USD 48

Insurance (household, travel and legal): USD 41

Media taxes: USD 36

Phone and internet: USD 0 (paid by my employer)

Cable: USD 0 (cancelled)

Savings for vacation: USD 180

Saving for misc. new purchases: USD 180

Total shared monthly spending: USD 3,784

Of which we pay 50 per cent each: USD 1,892

Private spending (gifts, entertainment etc.): USD 360

Total monthly spending: USD 2,252

The shared monthly spending is “fixed” at USD 3,784 – any variations will affect the savings for repayment number.

* Our mortgage is interest only loans, but someday we would have to repay.

1. Mortgage - fixed at 2.14% until 2015 – USD 222,342

2. Mortgage – floating 1.1% - USD 83,964

Savings fixed at 3.75% until 2015 – USD -21,586

Saving fixed at 3.00 until 2015 – USD -27,779

Savings floating 1.1% - USD -3,604

Net mortgage: USD 253,337 – house valuation is approx. USD 324,324 (we paid more in 2007).

Income

Taxation in Denmark is really high – tax is by far our highest cost. You really need to plan to avoid taxes being too high – marginal tax for working income is close to 56 per cent!

Breakdown monthly income:

Salary: USD 9,369

Tax: USD -2,928

Retirement savings (equal to 401K): USD -751

Retirement savings (equal to roth): USD -414

Entrepreneur savings (tax deferred): USD -1,654

Net salary: USD 3,623

Monthly savings: USD 1,370

Savings rate: 38%

Savings rate adj. for tax deferred savings: 59%

Savings rate adj. for tax deferred savings and repayment of mortgage: 67%

Total net worth (not including house and car) USD 541,684

SWR: 4.99 %

I hope (and plan) to retire before turning 40 (4 years and 10 months from now). GF will not be able to retire so soon, she is pretty frugal as well but she is younger and finished her education later than me. I will not be including her numbers in this journal.

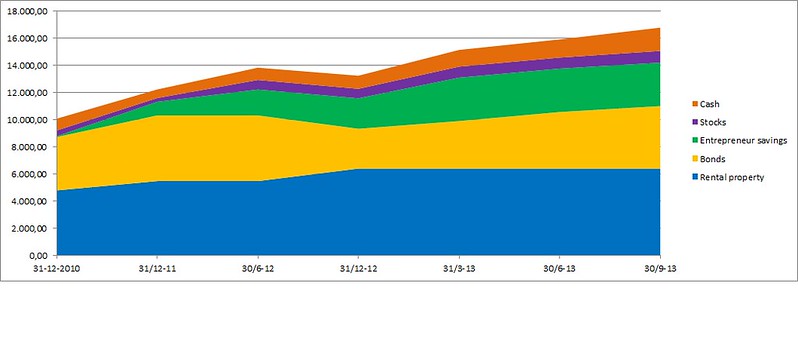

I have been tracking my net worth for many years, but since I started reading the ERE site I have more focused on passive income, here is a graphical view on my progress since 31/12-10:

http://www.flickr.com/photos/103667714@N05/10005563134/

Feel free to comment, ask any question and any good advice would be very welcome as well.

Wizards' journal (ERE in Denmark)

-

almostthere

- Posts: 284

- Joined: Tue Jul 09, 2013 1:47 am

Re: Wizards' journal (ERE in Denmark)

Welcome. Very cool graph. I love the "entrepreneur savings" line.

Re: Wizards' journal (ERE in Denmark)

Thank you, just need to figure out, how to add the image to the post.

"Entrepreneur savings" are tax deductible and since the Danish laws put a cap on the amount you could contribute to retirements saving, I needed to find a new way to avoid paying the marginal tax on my working income.

A 10,000 USD contribution reduce my taxes by USD 5,170 so the real cost of these savings are “only” USD 4,830. The income from the savings (has to be either cash or bonds) are free to be used (minus tax). So this is actually quite an attractive passive income producing option.

Only drawback is that I need to use the principal for a business before turning 67, otherwise there will be tax + penalty tax on the savings.

"Entrepreneur savings" are tax deductible and since the Danish laws put a cap on the amount you could contribute to retirements saving, I needed to find a new way to avoid paying the marginal tax on my working income.

A 10,000 USD contribution reduce my taxes by USD 5,170 so the real cost of these savings are “only” USD 4,830. The income from the savings (has to be either cash or bonds) are free to be used (minus tax). So this is actually quite an attractive passive income producing option.

Only drawback is that I need to use the principal for a business before turning 67, otherwise there will be tax + penalty tax on the savings.

-

LiberateMind

- Posts: 206

- Joined: Fri Oct 26, 2012 8:18 pm

Re: Wizards' journal (ERE in Denmark)

Please post in your currency. What actually matters is savings rate , networth increase, ROI , SWR , FI ratio.....

Re: Wizards' journal (ERE in Denmark)

Entry #2, November 1 – Accounting issue, asset allocation and some good news.

First an update on net worth and SWR – net worth is up 1.9% to USD 557,014 and my SWR is now 4.90%.

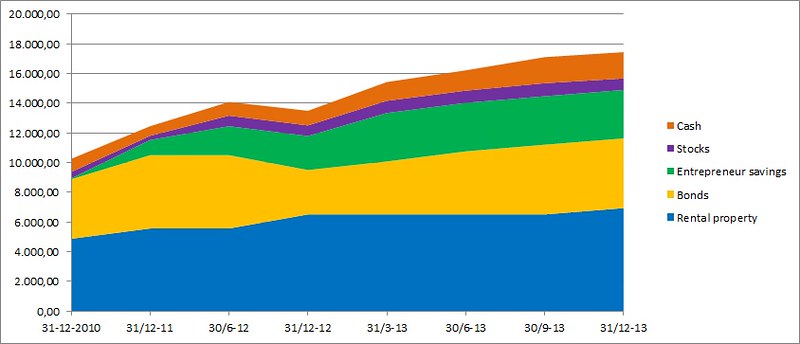

Oh… and I actually learned to post images in the posts – so here is the image of my passive income from Entry #1.

Accounting issue

Regarding my personal spending – I have a small problem with the accounting. The thing is that one of my monetized hobbies is arbitrage gaming, which result in numerous amount of money transfers each month. It is possible to keep an exact account on these, but I came to the conclusion that the time spend on this wasn’t doing me any good. I know each transaction gives profit, and I know that I don’t spend much money besides our joint spending.

Quarterly I do an exact calculation of my private spending – this does however not take the winning from gaming into account – witch result in very low calculated private spending. I actually have a goal to have the winnings pay all of my private spending. Last year and the first three quarters of this year this was actually succeeded (meaning private spending is negative...).

I will keep the budgeted private spending amount in my SWR calculation – because the income/winnings are by no means guaranteed. I need time to do this and most important options to do this might disappear.

Any thoughts on this would be welcome.

Asset allocations

I would like to give an introduction to my investments by presenting my asset allocations (after deferred tax):

Almost like the permanent portfolio except gold/metals are replaced by a rental property…

The cash position is too high I think, however most of the cash do yield a higher return than I pay on my loans, so guess this isn’t too bad after all.

Stocks are mostly individual stocks but I do have some index funds as well. I prefer stocks which pay a nice dividend each year.

Bonds are all corporate bonds – five different companies. Government and mortgage bonds yields are at the moment lower than bank deposit so at the moment this is not attractive.

Good news

Last month GF started to take public transportation to work, it has increased her commute time by approx. half an hour each day – in exchange she gets 1½ hour each day to read in the train. At the moment she is very pleased with this trade. Financial this is win situation as well, as this will reduce our spending by approx. USD 1.000 per year.

Secondly we had our insurances reviewed which gave us a reduction of approx. USD 250 per year.

These savings will not affect my current monthly spending as mentioned in entry #1 this will only mean a higher savings for mortgage repayment. In the long run it will of course mean we can pay of the mortgage quicker.

@LiberateMind: I will keep posting in USD - all the ratios are the same whatever currency used I personally prefer to read journals in USD, GBP or EUR because I know the exchange rates of these currencies and don’t need to look these up. It is no big deal for me to convert from DKK to USD (excel is a fantastic tool

I personally prefer to read journals in USD, GBP or EUR because I know the exchange rates of these currencies and don’t need to look these up. It is no big deal for me to convert from DKK to USD (excel is a fantastic tool  ), so I will keep my numbers in USD. Hopefully this will make it easier for others to relate to my numbers.

), so I will keep my numbers in USD. Hopefully this will make it easier for others to relate to my numbers.

First an update on net worth and SWR – net worth is up 1.9% to USD 557,014 and my SWR is now 4.90%.

Oh… and I actually learned to post images in the posts – so here is the image of my passive income from Entry #1.

Accounting issue

Regarding my personal spending – I have a small problem with the accounting. The thing is that one of my monetized hobbies is arbitrage gaming, which result in numerous amount of money transfers each month. It is possible to keep an exact account on these, but I came to the conclusion that the time spend on this wasn’t doing me any good. I know each transaction gives profit, and I know that I don’t spend much money besides our joint spending.

Quarterly I do an exact calculation of my private spending – this does however not take the winning from gaming into account – witch result in very low calculated private spending. I actually have a goal to have the winnings pay all of my private spending. Last year and the first three quarters of this year this was actually succeeded (meaning private spending is negative...).

I will keep the budgeted private spending amount in my SWR calculation – because the income/winnings are by no means guaranteed. I need time to do this and most important options to do this might disappear.

Any thoughts on this would be welcome.

Asset allocations

I would like to give an introduction to my investments by presenting my asset allocations (after deferred tax):

Almost like the permanent portfolio except gold/metals are replaced by a rental property…

The cash position is too high I think, however most of the cash do yield a higher return than I pay on my loans, so guess this isn’t too bad after all.

Stocks are mostly individual stocks but I do have some index funds as well. I prefer stocks which pay a nice dividend each year.

Bonds are all corporate bonds – five different companies. Government and mortgage bonds yields are at the moment lower than bank deposit so at the moment this is not attractive.

Good news

Last month GF started to take public transportation to work, it has increased her commute time by approx. half an hour each day – in exchange she gets 1½ hour each day to read in the train. At the moment she is very pleased with this trade. Financial this is win situation as well, as this will reduce our spending by approx. USD 1.000 per year.

Secondly we had our insurances reviewed which gave us a reduction of approx. USD 250 per year.

These savings will not affect my current monthly spending as mentioned in entry #1 this will only mean a higher savings for mortgage repayment. In the long run it will of course mean we can pay of the mortgage quicker.

@LiberateMind: I will keep posting in USD - all the ratios are the same whatever currency used

-

almostthere

- Posts: 284

- Joined: Tue Jul 09, 2013 1:47 am

Re: Wizards' journal (ERE in Denmark)

Arbitrage gaming? What is it?

Re: Wizards' journal (ERE in Denmark)

@almostthere:

http://en.wikipedia.org/wiki/Arbitrage_betting

Would not recommend this unless you have a high level of experience is the gaming sector, there is plenty of pitfalls.

http://en.wikipedia.org/wiki/Arbitrage_betting

Would not recommend this unless you have a high level of experience is the gaming sector, there is plenty of pitfalls.

Re: Wizards' journal (ERE in Denmark)

Greetings Wizards,

This was a great read!

Regarding your investments - Harry Browne's PP is generally seen as a passive, highly diversified portfolio. How do you reconcile this with investing in only few companies?

Also, do you invest only in Danish companies, or international as well?

I ask because I also come from a small country (Israel) and am curious on how you go about your allocation.

How is the property market in Denmark currently?

Peace

This was a great read!

Regarding your investments - Harry Browne's PP is generally seen as a passive, highly diversified portfolio. How do you reconcile this with investing in only few companies?

Also, do you invest only in Danish companies, or international as well?

I ask because I also come from a small country (Israel) and am curious on how you go about your allocation.

How is the property market in Denmark currently?

Peace

Re: Wizards' journal (ERE in Denmark)

Hi elegant,

Thanks for dropping by - I'm not doing the PP - just happens to be that my asset alloktion is close to the PP (except for the rental vs gold).

I’m not following some specific asset allocation plan, but I try to keep a relatively low risk and adjust to the current market situation.

My tax deferred retirement savings are mostly stocks – because of the long terms on these savings (can’t touch them until I turn 60).

The tax deferred entrepreneur savings are mostly bonds – only bonds and cash are allowed.

The rest of my savings are actually mostly in cash and bonds – I’m trying to increase the stock number but I don’t like buying when prices are high... so not much happening right now…

I like to have cash available to be able to take advantage of great deals when they appear…And secondly the interest rates on my loans (rental and our house) are ridiculously low so I’m not making any repayment at the moment, the money saved on this are deposited in bank accounts which have a higher interest rate than the loans – actually some kind of money printing machine..

As for my stock investment I try to have a diversified portfolio which include both Danish and international stocks, I actually have one Israeli company in the portfolio (TEVA). At the moment I hold positions in 25 different companies + some index funds.

I do spend some time following these companies, but again this is a hobby I enjoy.

Property market in Denmark is recovering, however there is big difference to different parts of the country. Copenhagen residental market is by far doing best. I live in a smaller town 50 miles from Copenhagen, here the prices are still pretty low (relatively speaken). We bought our house when the prices started dropping, but still paid way to much looking at the market now. But we like our house and we have excellent financing, so it's ok. The rental is in another smaller town but closer to Copenhagen where the market is doing better. I bougt this apartment i 2004, so this is a bit better deal

Thanks for dropping by - I'm not doing the PP - just happens to be that my asset alloktion is close to the PP (except for the rental vs gold).

I’m not following some specific asset allocation plan, but I try to keep a relatively low risk and adjust to the current market situation.

My tax deferred retirement savings are mostly stocks – because of the long terms on these savings (can’t touch them until I turn 60).

The tax deferred entrepreneur savings are mostly bonds – only bonds and cash are allowed.

The rest of my savings are actually mostly in cash and bonds – I’m trying to increase the stock number but I don’t like buying when prices are high... so not much happening right now…

I like to have cash available to be able to take advantage of great deals when they appear…And secondly the interest rates on my loans (rental and our house) are ridiculously low so I’m not making any repayment at the moment, the money saved on this are deposited in bank accounts which have a higher interest rate than the loans – actually some kind of money printing machine..

As for my stock investment I try to have a diversified portfolio which include both Danish and international stocks, I actually have one Israeli company in the portfolio (TEVA). At the moment I hold positions in 25 different companies + some index funds.

I do spend some time following these companies, but again this is a hobby I enjoy.

Property market in Denmark is recovering, however there is big difference to different parts of the country. Copenhagen residental market is by far doing best. I live in a smaller town 50 miles from Copenhagen, here the prices are still pretty low (relatively speaken). We bought our house when the prices started dropping, but still paid way to much looking at the market now. But we like our house and we have excellent financing, so it's ok. The rental is in another smaller town but closer to Copenhagen where the market is doing better. I bougt this apartment i 2004, so this is a bit better deal

Re: Wizards' journal (ERE in Denmark)

Entry #3, December 2 - Major news, change of plans? And a look back in time.

As usual, I start with an update on SWR and net worth.

SWR down 0.10 to 4.80 %

Net worth up 1.96 % to USD 567,926

Everything right on track, but…

Major news

As stated in Entry # 1 we plan for two kids – and now, after 1½ years of attempts, we finally got lucky, (fingers crossed). GF is pregnant and we should be parents next year (July). I feel very happy and very confused at the same time; this will definitely be a life changing event.

There are a lot of things to consider:

• A room for the child – will most likely be the room we use as “office” – that no big deal, we don’t use our office that much.

• We need to change our wills

• How much maternity leave should we take (Danish rules are above average on this subject)

• And not a least returning to our jobs – childcare?

• How to raise the child

• Name (and surname - as we are not married)

• And a lot more

One thing is sure - without any doubt our costs will go up.

In our long term budget, this is what I use for setting the target day for retirement; I already have included a number for two kids, so it was actually just a matter of time.

The number I have used might seem high, but this is what is considered “normal” in Denmark – USD 900 each month for each child for 20 years…

What I haven’t included is that the Danish government gives a child benefit to all parents until the child turns 18. This benefit starts high and are reduced at age 3 and 7.

And secondly I firmly believe that It should be possible to raise a child on lower than average costs. Please note that almost all health care and education costs are paid for by the government.

Change of plans?

I am currently considering changing the plan I’m currently following. This plan has a retirement date in July 2018, meaning 4 years and 8 months more of 9-5.

Actually if updating our budget with the child benefit it should be possible to retire in July 2017, “only” 3 years and 8 months from now.

But what I’m really considering is to retire even earlier. GF will properly end her paid maternity leave in March 2015. I then have the legally option of taking 32 weeks of maternity leave (without any pay). This way I could get a “free” attempt of having to rely only on investment income (and maybe some freelance income). If this is not working out for one reason or another, I can still return to my current job. Not sure my employer will be excited about this move… but to honest I don’t care – I have a relatively long notice period, so if they would like to go this way, fine by me.

If I choose this second option I will retire in April 2015, 1 year and 4 months from now. Sounds tempting but this will of course come with the consequent effects that my margin of safety will be significantly reduced since I will be missing full time pay for 2 years and 4 months.

Not an easy decision, but still time to consider which move to take.

History - a look back in time

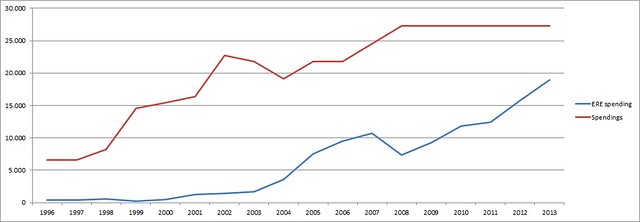

I plan to add some kind of graph/illustration to each entry (some will definitely be repeated).

Since turning 18 I have more of less kept some kind of records of net worth, income and spending. With this data I have constructed a graph showing my actual spending compared to a calculated ERE spending (net worth x SWR 3.33 %).

I’m looking forward to reach the crossover point.

There are a few jumps in the spending:

1998: First real job

1999: Moved away from parents (bought a small apartment)

2002: Bought my first car (new… stupid move)

2005: Sold everything (almost) and moved to Malta

2006: Returned to Denmark, rented an apartment

2008: Bought house with GF (which also effect the ERE spending, since I don’t include our house in net worth)

Feel free to comment, ask questions, give advice etc.

As usual, I start with an update on SWR and net worth.

SWR down 0.10 to 4.80 %

Net worth up 1.96 % to USD 567,926

Everything right on track, but…

Major news

As stated in Entry # 1 we plan for two kids – and now, after 1½ years of attempts, we finally got lucky, (fingers crossed). GF is pregnant and we should be parents next year (July). I feel very happy and very confused at the same time; this will definitely be a life changing event.

There are a lot of things to consider:

• A room for the child – will most likely be the room we use as “office” – that no big deal, we don’t use our office that much.

• We need to change our wills

• How much maternity leave should we take (Danish rules are above average on this subject)

• And not a least returning to our jobs – childcare?

• How to raise the child

• Name (and surname - as we are not married)

• And a lot more

One thing is sure - without any doubt our costs will go up.

In our long term budget, this is what I use for setting the target day for retirement; I already have included a number for two kids, so it was actually just a matter of time.

The number I have used might seem high, but this is what is considered “normal” in Denmark – USD 900 each month for each child for 20 years…

What I haven’t included is that the Danish government gives a child benefit to all parents until the child turns 18. This benefit starts high and are reduced at age 3 and 7.

And secondly I firmly believe that It should be possible to raise a child on lower than average costs. Please note that almost all health care and education costs are paid for by the government.

Change of plans?

I am currently considering changing the plan I’m currently following. This plan has a retirement date in July 2018, meaning 4 years and 8 months more of 9-5.

Actually if updating our budget with the child benefit it should be possible to retire in July 2017, “only” 3 years and 8 months from now.

But what I’m really considering is to retire even earlier. GF will properly end her paid maternity leave in March 2015. I then have the legally option of taking 32 weeks of maternity leave (without any pay). This way I could get a “free” attempt of having to rely only on investment income (and maybe some freelance income). If this is not working out for one reason or another, I can still return to my current job. Not sure my employer will be excited about this move… but to honest I don’t care – I have a relatively long notice period, so if they would like to go this way, fine by me.

If I choose this second option I will retire in April 2015, 1 year and 4 months from now. Sounds tempting but this will of course come with the consequent effects that my margin of safety will be significantly reduced since I will be missing full time pay for 2 years and 4 months.

Not an easy decision, but still time to consider which move to take.

History - a look back in time

I plan to add some kind of graph/illustration to each entry (some will definitely be repeated).

Since turning 18 I have more of less kept some kind of records of net worth, income and spending. With this data I have constructed a graph showing my actual spending compared to a calculated ERE spending (net worth x SWR 3.33 %).

I’m looking forward to reach the crossover point.

There are a few jumps in the spending:

1998: First real job

1999: Moved away from parents (bought a small apartment)

2002: Bought my first car (new… stupid move)

2005: Sold everything (almost) and moved to Malta

2006: Returned to Denmark, rented an apartment

2008: Bought house with GF (which also effect the ERE spending, since I don’t include our house in net worth)

Feel free to comment, ask questions, give advice etc.

Re: Wizards' journal (ERE in Denmark)

Is there a reasoning behind the 3.33% or is it just a nice round number?:)

Re: Wizards' journal (ERE in Denmark)

I understand that 4% is the most commonly used rate.

I have chosen to use 30 years x annual spending, equal to 3.33%.

Could also have chosen 3%, but that is perhaps a bit too conservative.

I have chosen to use 30 years x annual spending, equal to 3.33%.

Could also have chosen 3%, but that is perhaps a bit too conservative.

Re: Wizards' journal (ERE in Denmark)

Entry #4, January 1, 2013 done & an update on passive income

Net worth up 0.25 % to USD 574,559.

SWR down 0.01 % to 4.79 %

My income for 2013 has been higher than expected so I had to pay extra taxes this month to avoid penalty taxes for paying late.

2013 - The realized numbers

Without further introduction here are my spending numbers for 2013 (all numbers USD):

Interest mortgage: 5,432

Interest savings for mortgage repayment: -1,224

Saved for mortgage repayment: 13,065

Property taxes: 2,796

Property insurance: 690

Utilities (heating, water, electricity and waste disposal): 5,309

Property maintenance: 0

Auto – gas: 3,811

Auto taxes: 606

Auto insurance: 657

Auto maintenance: 1,677

Public transportation: 3,923

Household (food etc.): 6,697

Insurance (disability): 618

Insurance (household, travel and legal): 499

Media taxes: 447

Vacations: 4,579

Misc. new purchases: -662 (sold some stuff and received some cash gifts)

Total shared spending: USD 48,919

Of which I paid 50 %: 24,460

Private spending: -3,309 (See entry #2 – accounting issues)

Total spending 2013: USD 21,151

Income numbers:

Salary: 117,969

Taxes: -39,902

Retirement savings: -14,239

Entrepreneur savings: -22,613

Net salary: 41,215

Savings: 20,064

Savings rate: 49 %

Savings rate adj. for tax deferred savings: 68 %

Savings rate adj. for tax deferred savings and repayment of mortgage: 73 %

The ratios are better than budgeted (38, 59 & 67).

Still room for improvement, but I’m happy with the numbers.

Passive income

I will finish this entry with an update on my passive income.

My cash position is too high and I currently looking on a few purchases including stocks, bonds and a new rental (might post an update on this one later).

NB: Still considering which plan to follow regarding when to quit the 9-5, not an easy one…

Net worth up 0.25 % to USD 574,559.

SWR down 0.01 % to 4.79 %

My income for 2013 has been higher than expected so I had to pay extra taxes this month to avoid penalty taxes for paying late.

2013 - The realized numbers

Without further introduction here are my spending numbers for 2013 (all numbers USD):

Interest mortgage: 5,432

Interest savings for mortgage repayment: -1,224

Saved for mortgage repayment: 13,065

Property taxes: 2,796

Property insurance: 690

Utilities (heating, water, electricity and waste disposal): 5,309

Property maintenance: 0

Auto – gas: 3,811

Auto taxes: 606

Auto insurance: 657

Auto maintenance: 1,677

Public transportation: 3,923

Household (food etc.): 6,697

Insurance (disability): 618

Insurance (household, travel and legal): 499

Media taxes: 447

Vacations: 4,579

Misc. new purchases: -662 (sold some stuff and received some cash gifts)

Total shared spending: USD 48,919

Of which I paid 50 %: 24,460

Private spending: -3,309 (See entry #2 – accounting issues)

Total spending 2013: USD 21,151

Income numbers:

Salary: 117,969

Taxes: -39,902

Retirement savings: -14,239

Entrepreneur savings: -22,613

Net salary: 41,215

Savings: 20,064

Savings rate: 49 %

Savings rate adj. for tax deferred savings: 68 %

Savings rate adj. for tax deferred savings and repayment of mortgage: 73 %

The ratios are better than budgeted (38, 59 & 67).

Still room for improvement, but I’m happy with the numbers.

Passive income

I will finish this entry with an update on my passive income.

My cash position is too high and I currently looking on a few purchases including stocks, bonds and a new rental (might post an update on this one later).

NB: Still considering which plan to follow regarding when to quit the 9-5, not an easy one…

Re: Wizards' journal (ERE in Denmark)

Entry #5, February 2, 2014 Mixed month

Net worth up 1.05 % to USD 575,305

SWR down 0.04 % to 4.75 %

Cash position

In entry #4 I complained about my cash position..

Regarding the new rental the deal didn’t work out. There were to minor issues; the current tenant were (IMO) paying too low a rent + the financing we were able to get wasn’t perfect (margins slightly higher than I wished for plus we needed to put in more equity than expected). The price for the property was actually ok, but I didn’t want to pay full price due to the two issues (I could have lived with one of them). We made an offer with a discount of 3.33%, but the seller wouldn’t accept any sort of discount… (The property is still for sale).

I did manage to buy some new bonds, but others were redeemed, so actually my total bond position was reduced :-/

The stock position was the only one (besides cash) which was increased. One new position bought and two positions were increased.

So I’m still left with too much cash.

Job situation

I managed to get a 9.6 % pay raise, starting next month. So the financial part of work is doing fine. But work’s quite frustrating; we are currently in the need of approx. two more employees in my department, which of course means more to do for the rest of us. At the same time a lot of new stuff is happening due to change in management etc.

Friends tax issue

I’ve spend quite a few hours/days this month helping a friend with a tax issue (he is into online gaming) and this combined with the pressure from work and time spend negotiating the rental has been a bit too much for me. I haven’t really been able to enjoy other parts of life as much as I wish for. In addition (I guess) this has led to a not to healthy month (too much sugar and started drinking coffee again) – a downward spiral I need to relate to.

Child

Last month we broke the news to our parents etc. – they were truly happy. GF had nuchal scan and we have had a meeting with the midwife – and everything goes by the book. Still a lot of unanswered question we need to consider, but as long as the child will be healthy everything else is secondary.

Graph / illustration

I “promised” to include a graph or illustration with each entry, but I’m not being too creative at the moment, and updates on the older ones don’t seem that interesting right now. If I come up with something interesting later this one month, I might post one.

Net worth up 1.05 % to USD 575,305

SWR down 0.04 % to 4.75 %

Cash position

In entry #4 I complained about my cash position..

Regarding the new rental the deal didn’t work out. There were to minor issues; the current tenant were (IMO) paying too low a rent + the financing we were able to get wasn’t perfect (margins slightly higher than I wished for plus we needed to put in more equity than expected). The price for the property was actually ok, but I didn’t want to pay full price due to the two issues (I could have lived with one of them). We made an offer with a discount of 3.33%, but the seller wouldn’t accept any sort of discount… (The property is still for sale).

I did manage to buy some new bonds, but others were redeemed, so actually my total bond position was reduced :-/

The stock position was the only one (besides cash) which was increased. One new position bought and two positions were increased.

So I’m still left with too much cash.

Job situation

I managed to get a 9.6 % pay raise, starting next month. So the financial part of work is doing fine. But work’s quite frustrating; we are currently in the need of approx. two more employees in my department, which of course means more to do for the rest of us. At the same time a lot of new stuff is happening due to change in management etc.

Friends tax issue

I’ve spend quite a few hours/days this month helping a friend with a tax issue (he is into online gaming) and this combined with the pressure from work and time spend negotiating the rental has been a bit too much for me. I haven’t really been able to enjoy other parts of life as much as I wish for. In addition (I guess) this has led to a not to healthy month (too much sugar and started drinking coffee again) – a downward spiral I need to relate to.

Child

Last month we broke the news to our parents etc. – they were truly happy. GF had nuchal scan and we have had a meeting with the midwife – and everything goes by the book. Still a lot of unanswered question we need to consider, but as long as the child will be healthy everything else is secondary.

Graph / illustration

I “promised” to include a graph or illustration with each entry, but I’m not being too creative at the moment, and updates on the older ones don’t seem that interesting right now. If I come up with something interesting later this one month, I might post one.

Re: Wizards' journal (ERE in Denmark)

Entry # 6, March 1, 2014 – Fantastic month moneywise

Net Worth up 2.93 % to USD 603,139

SWR down 0.14 % to 4.61 %

Rental

Last week we signed a deal on the rental I wrote about earlier. The rental will be ours next Friday. GF will have a 25 % part of this one – nice to see her passive income increase.

Apparently the current tenant was paying approx. 7% of the rent to another account… this has been formalized so the rental contract reflects the total payment. This again enabled us to get a better loan offer – almost a 10 % higher loan.

The yield on the property isn’t impressive (~5%) but is a really easy rental to get tenants for, and in a good condition (10 year old apartment). The price is approx. USD 280k and we will pay 25 % in cash.

The loan is super nice – 30 year commitment and amortization, interest adjusted every three years. The interest for the first three years will be decided next Wednesday, looks like it will be at a rate of 1.5 % including margin.

AFTER amortization and tax this will give us a 4 % return on the invested capital, or more than a USD 2k bump on my passive income.

Stock and Bonds

February has been a really good month for my investments. My biggest single stock investment, a small Danish investment company, which was trading at price/book ratio of 0.83, announced the decision to liquidate the company, meaning the stock holders will get a payment close to the book value. I hadn’t expected this; I was just hoping to exit at a price/book ratio of 0.90.

The new bonds I bought last month at price of 74 is now trading at 85 – If I knew what else to buy I might sell these one, but I think is it really hard to find bonds which offer an attractive yield without the risk being too high.

In general the market has been really good last month, which of course has helped as well.

Child

We had been to the final scan, and everything still looks fine, and we now know that it will be a boy. GF is still doing fine (and getting bigger).

Job situation

Still chaotic but we signed contracts with two new full time employees and a student assistant so hopefully it will get better when they start (April).

Health (goals)

Spring is getting near and I hope to be able to start to exercise more. I am considering setting some non financial goals and publishing them here – might serve as an extra motivation…

Did manage to cut back on the coffee, but still need some improvements regarding sugar to be made.

Net Worth up 2.93 % to USD 603,139

SWR down 0.14 % to 4.61 %

Rental

Last week we signed a deal on the rental I wrote about earlier. The rental will be ours next Friday. GF will have a 25 % part of this one – nice to see her passive income increase.

Apparently the current tenant was paying approx. 7% of the rent to another account… this has been formalized so the rental contract reflects the total payment. This again enabled us to get a better loan offer – almost a 10 % higher loan.

The yield on the property isn’t impressive (~5%) but is a really easy rental to get tenants for, and in a good condition (10 year old apartment). The price is approx. USD 280k and we will pay 25 % in cash.

The loan is super nice – 30 year commitment and amortization, interest adjusted every three years. The interest for the first three years will be decided next Wednesday, looks like it will be at a rate of 1.5 % including margin.

AFTER amortization and tax this will give us a 4 % return on the invested capital, or more than a USD 2k bump on my passive income.

Stock and Bonds

February has been a really good month for my investments. My biggest single stock investment, a small Danish investment company, which was trading at price/book ratio of 0.83, announced the decision to liquidate the company, meaning the stock holders will get a payment close to the book value. I hadn’t expected this; I was just hoping to exit at a price/book ratio of 0.90.

The new bonds I bought last month at price of 74 is now trading at 85 – If I knew what else to buy I might sell these one, but I think is it really hard to find bonds which offer an attractive yield without the risk being too high.

In general the market has been really good last month, which of course has helped as well.

Child

We had been to the final scan, and everything still looks fine, and we now know that it will be a boy. GF is still doing fine (and getting bigger).

Job situation

Still chaotic but we signed contracts with two new full time employees and a student assistant so hopefully it will get better when they start (April).

Health (goals)

Spring is getting near and I hope to be able to start to exercise more. I am considering setting some non financial goals and publishing them here – might serve as an extra motivation…

Did manage to cut back on the coffee, but still need some improvements regarding sugar to be made.

Re: Wizards' journal (ERE in Denmark)

Entry # 7, June 6, 2014

It has been quite a while, since I updated this journal

Here are the numbers for the last three months:

March numbers:

Net Worth up 1.81 % to USD 614,056

SWR down 0.09 % to 4.52 %

April numbers:

Net Worth up 1.81 % to USD 625,189

SWR down 0.08 % to 4.44 %

May numbers:

Net Worth up 2.63 % to USD 635,749

SWR down 0.11 % to 4.33 %

The good

Financially this has been three exceptionally good months, of course the current marked has helped, but most part of my finances is running smoothly – however still holding too much cash.

Girlfriend is doing fine and there is only approx. 6 weeks to the expected day of birth of our son.

We have made arrangement for a secret wedding two weeks from now, so will be no major expense – none of us would like a big party, so this feels like the right way to do it.

The bad

Spending has been a bit higher than normal, still within budget, but have some of the spending could have been avoided..

The ugly

a) Really tired of my work, but as I have the right to 2+10 weeks maternity leave, it would be a really stupid move to quit before next year.

b) Need to start doing some sort of exercise, but am in some sort of downward spiral; I'm normally home at 5.30 pm and then it’s time to prepare dinner. So there is only from approx. 7 pm. to 10 pm. and I’m mostly pretty tired at this time of the day – feels like the job is killing me slowly.

It has been quite a while, since I updated this journal

Here are the numbers for the last three months:

March numbers:

Net Worth up 1.81 % to USD 614,056

SWR down 0.09 % to 4.52 %

April numbers:

Net Worth up 1.81 % to USD 625,189

SWR down 0.08 % to 4.44 %

May numbers:

Net Worth up 2.63 % to USD 635,749

SWR down 0.11 % to 4.33 %

The good

Financially this has been three exceptionally good months, of course the current marked has helped, but most part of my finances is running smoothly – however still holding too much cash.

Girlfriend is doing fine and there is only approx. 6 weeks to the expected day of birth of our son.

We have made arrangement for a secret wedding two weeks from now, so will be no major expense – none of us would like a big party, so this feels like the right way to do it.

The bad

Spending has been a bit higher than normal, still within budget, but have some of the spending could have been avoided..

The ugly

a) Really tired of my work, but as I have the right to 2+10 weeks maternity leave, it would be a really stupid move to quit before next year.

b) Need to start doing some sort of exercise, but am in some sort of downward spiral; I'm normally home at 5.30 pm and then it’s time to prepare dinner. So there is only from approx. 7 pm. to 10 pm. and I’m mostly pretty tired at this time of the day – feels like the job is killing me slowly.

Last edited by wizards on Tue Jul 01, 2014 4:23 am, edited 1 time in total.

-

Hankaroundtheworld

- Posts: 470

- Joined: Mon Feb 24, 2014 4:50 am

Re: Wizards' journal (ERE in Denmark)

Sounds good progress, and yes, I guess everyone had some good Months in Net Worth Growth because of growing Stock values. Lots of fun with the upcoming birth of your child, for sure something else on your mind.

Re: Wizards' journal (ERE in Denmark)

@hank - Thanks for dropping by, and thanks - agree, this will defininately change the agenda

Re: Wizards' journal (ERE in Denmark)

Wow...time is running fast - and it doesn't go slower when having a child

Feel like it's time for an update.

I’m now at a WR of 3.61 % and net worth of USD 625,461. My currency (DKK) follows the euro, so if I was to use the same exchange as my last update net worth would be USD 763,177…glad my expenses are in DKK

Breaking news:

Monday I will hand over my resignation. Last day at work will be July 3rd. I could wait almost another month but:

a) I feel like it is fair to give them a longer notice.

b) I might agree to some sort of part time transition if the terms could be as I request, which would be; all work done from home, a right to refuse tasks and a right to decide when the work is done. I will not ask for this option as default, but if they ask if there is a way to make me stay a bit longer I will pitch this idea. If they don’t ask – fine by me.

Why work after “quitting” you might ask – well a few reasons:

1) I would like to reach a SWR of 3.33%

2) I could allocate some funds to my wife so she could retire earlier (she is saving, but isn’t sure she would like to retire at the moment…I did ask her if she would stay home longer with our son as I’m a earning more than she is - but she refused).

3) Set up some “funds” for extraordinary plans (more traveling, charity, supporting start-ups etc.)

4) And well…some of the work I do is quite fun….

Family

My son was born last July – and I am really looking forward to stay home with him. My wife is still on maternity leave, but she will start working again when I quit. It is an amazing thing to have a child – lots of new experiences some more fun than other of course, but I wouldn’t change a thing, other than having more time with him. I did stay a home the first five weeks after he was born and the last 2½ month of 2014 (working 10 hours/week from home) which was really good times

Spending after having a child

I’m glad to report that cost of having a child to a great extent is up to you. It’s definitely not free, but you really don’t need much and at the same time other areas of spending will naturally be reduced.

I will try to make a report on the spending later on (all data is there, just need to figure out how to best display them).

Plans for the last months until the big day

I am beginning to consider how much the days need to be planned – my priorities are:

* My son

* Getting in better shape

* Some home improvement projects

* Read more books

For a start I will properly just ride a long, but I think I will need some structure in the long run

Feel like it's time for an update.

I’m now at a WR of 3.61 % and net worth of USD 625,461. My currency (DKK) follows the euro, so if I was to use the same exchange as my last update net worth would be USD 763,177…glad my expenses are in DKK

Breaking news:

Monday I will hand over my resignation. Last day at work will be July 3rd. I could wait almost another month but:

a) I feel like it is fair to give them a longer notice.

b) I might agree to some sort of part time transition if the terms could be as I request, which would be; all work done from home, a right to refuse tasks and a right to decide when the work is done. I will not ask for this option as default, but if they ask if there is a way to make me stay a bit longer I will pitch this idea. If they don’t ask – fine by me.

Why work after “quitting” you might ask – well a few reasons:

1) I would like to reach a SWR of 3.33%

2) I could allocate some funds to my wife so she could retire earlier (she is saving, but isn’t sure she would like to retire at the moment…I did ask her if she would stay home longer with our son as I’m a earning more than she is - but she refused).

3) Set up some “funds” for extraordinary plans (more traveling, charity, supporting start-ups etc.)

4) And well…some of the work I do is quite fun….

Family

My son was born last July – and I am really looking forward to stay home with him. My wife is still on maternity leave, but she will start working again when I quit. It is an amazing thing to have a child – lots of new experiences some more fun than other of course, but I wouldn’t change a thing, other than having more time with him. I did stay a home the first five weeks after he was born and the last 2½ month of 2014 (working 10 hours/week from home) which was really good times

Spending after having a child

I’m glad to report that cost of having a child to a great extent is up to you. It’s definitely not free, but you really don’t need much and at the same time other areas of spending will naturally be reduced.

I will try to make a report on the spending later on (all data is there, just need to figure out how to best display them).

Plans for the last months until the big day

I am beginning to consider how much the days need to be planned – my priorities are:

* My son

* Getting in better shape

* Some home improvement projects

* Read more books

For a start I will properly just ride a long, but I think I will need some structure in the long run

-

andystkilda

- Posts: 17

- Joined: Wed Jan 28, 2015 10:13 pm

Re: Wizards' journal (ERE in Denmark)

Wow - amazing story and congratulations on your new-found freedom!