February update

Finances

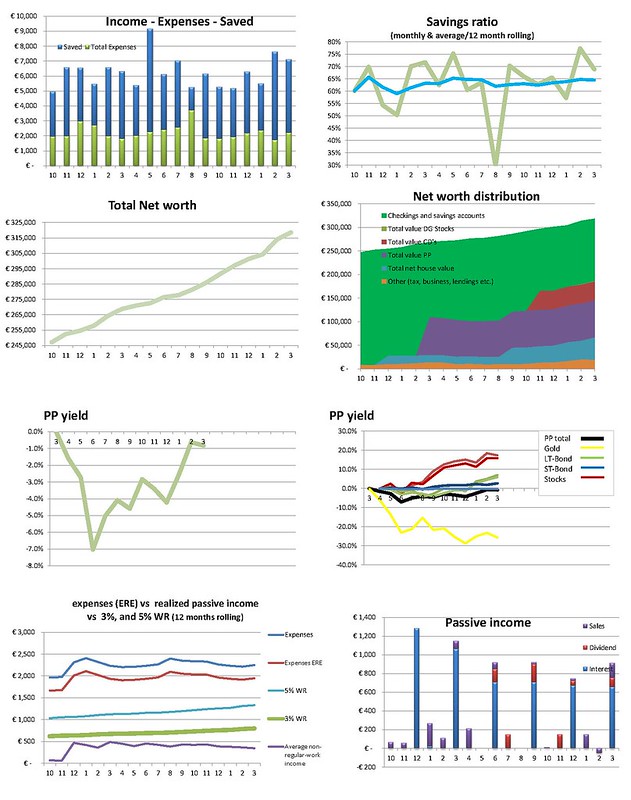

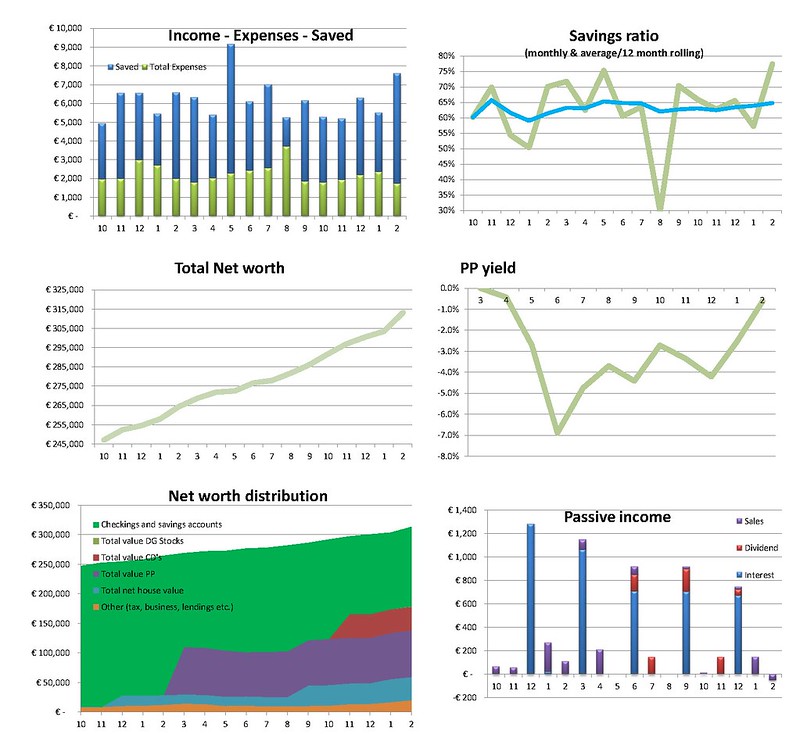

Expenses: 1723

Income 7608 (7658 regular income, -51 CL sales (sales of January had to be split with someone else)

Savings ratio 77% (average 12 months 65%)

Our expenses were the lowest ever

(well, since keeping this journey).

The benefit issue (for using day-care after school) I mentioned earlier, is solved and we received part of the money we were entitled to. The remaining will be settled in the coming months. Also we were reimbursed for some business expenses. That helped to reduce our expenses for this month.

And I got a bonus this month

That helped to achieve our 2nd highest income since starting this journal. Only in May our income was (and will be again) higher, because in May we receive an annual holiday allowance (common in the Netherlands to get it once a year around May-June).

So, we achieved a saving rate of 77%

. That won’t last though…

Still, the average savings rate over 12 months was 62% in November and has increased 1% each month thereafter and we’re now at 65%.

With the changes of the last few months (paying off mortgage partly, needing less day care, little higher income from DW) I hope that we can maintain an average of 65% or even slightly above. Oh, and we paid another few thousand to the principal of our mortgage. We’re now at 74% of the original amount. It will reduce our monthly expenses a little bit further.

Net worth increased with almost 10K, the highest ever also (you see the nice line in the graphic). I wish we could continue this line...

Apart from the high savings rate, the market was good, side business value increased a bit and I already “booked” tax return (see March forecast below).

Side business

Received another order. Not much work, mainly some emails and administration but will increase net worth with a few K during the year.

Other

Working 5 days a week, some social activities in the weekend (birthday party, meeting family etc.) and weeks pass by quickly. That was February.

I did enjoy it most of the part though.

March forecast finances

I mentioned earlier I had to pay additional tax. However, my appeal convinced them it was incorrect. I will receive the already payed tax back again and that will increase the regular income over March a bit. On the other hand, we will have some additional expenses of a similar amount. More about that later in future updates.

Graphics

It’s good to see the diversification of our assets since I started this journal. It used to be almost all in savings account (96%), now it’s down to 43%.

ERE-Finances

ERE-Finances

I am pretty focused on the finance part of ERE, maybe so much I am obsessed by it. I am not afraid about it, I think it will become less in the future, it is not a problem as I can still function normally and I have always been quite keen on keeping track of finances, graphics etc.

Also, I think I can afford to spend time on this as I don’t need to learn a lot about DIY etc. I have always done many things myself, I haven’t paid other people very often to do things for me outside of car maintenance/repairs that I couldn’t do easily myself. I would like to improve on certain other things, growing vegetables, doing all car maintenance by myself, etc. but I simply don’t have the time/energy/priority for that at this moment to dive into that extensively. So for now, it’s okay.

Analogy “becoming FI” – “running a Marathon”

Some people don’t see why they should run a marathon when they are already at the finish

Born with a trust fund

Some people finish a marathon in just over 2 hours

saving rate 85% or more

Some people finish a marathon while using doping in 2-6 hours

not extremely frugal but having a very high income.

Some people enjoy the scenery while walking/running and having a pick nick before they finish the marathon in 1 day

on course for ER, determined, enjoying life* but not extreme

Some people don’t enjoy the scenery, hate walking/running, are complaining constantly and it will take many days before they finish the marathon

Cubicle drones who hate work and save (hopefully enough) to be FI at 65

Some people never finish a marathon

saving rate 0% or negative

Combinations of the above are of course possible...

*I am not saying others are not enjoying life

So far this update, thanks for reading and again: I am enjoying all these other journals (and many other postings) very much.