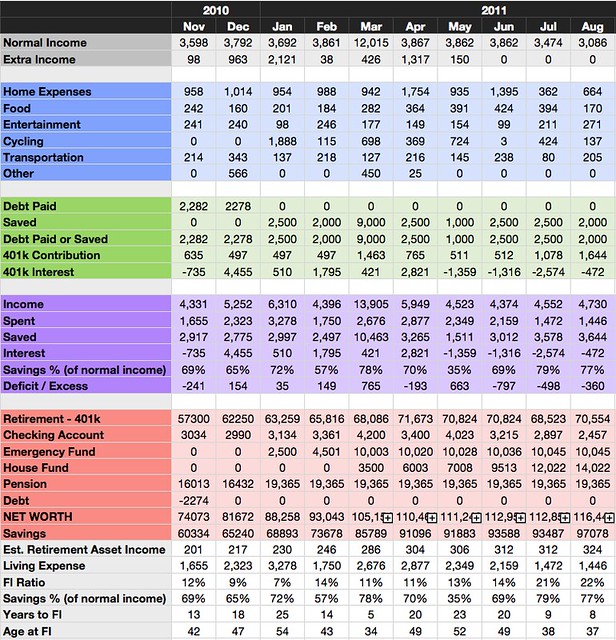

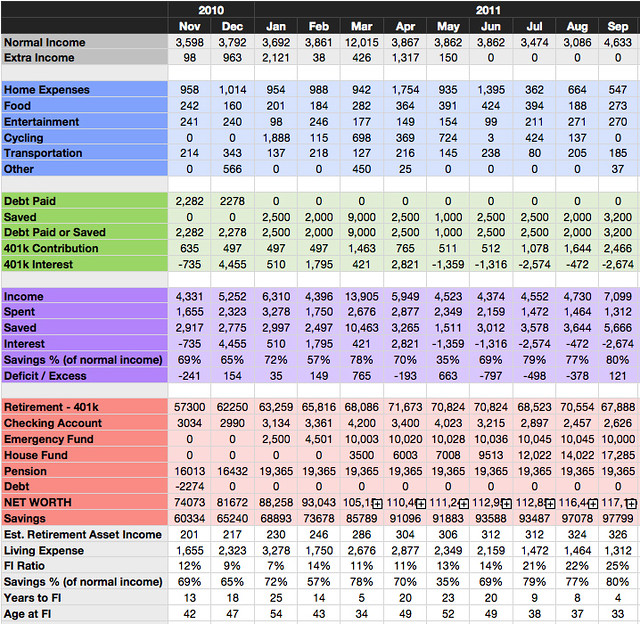

AUGUST 2011

_________________________

TOTALS

TOTAL PAY - $4,730

TOTAL SAVED - $3,644

SAVINGS - 77%

After tax pay: $3,086

401k Contribution: $1,644

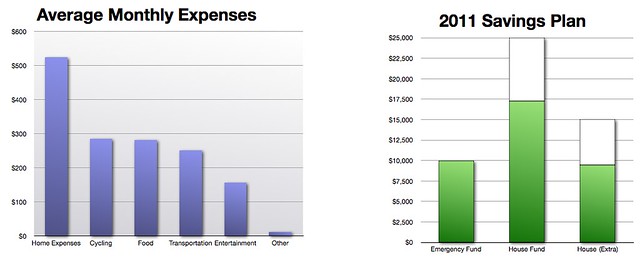

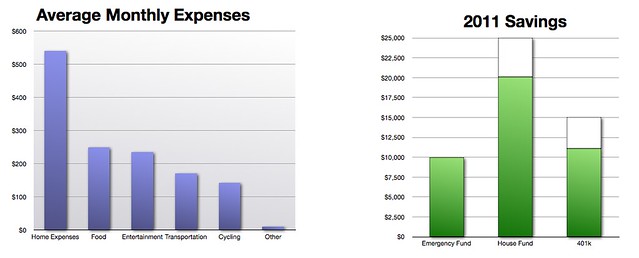

Home Expenses - $664

Food - $170

Entertainment - $271

Cycling - $137

Transportation - $205

Other - $0

Saved, After tax - $2,000

NOTES:

Transportation included 6 months of car insurance, $162. Gas was down to $40 from a pre-move level of about $160.

Entertainment included 3 PS3 games ($38) and a used stereo receiver ($100).

I’m going to try to get my expenses below $1,000 for at least one or two months this year. With my current expenses, it’s possible, but it’ll take some focus.

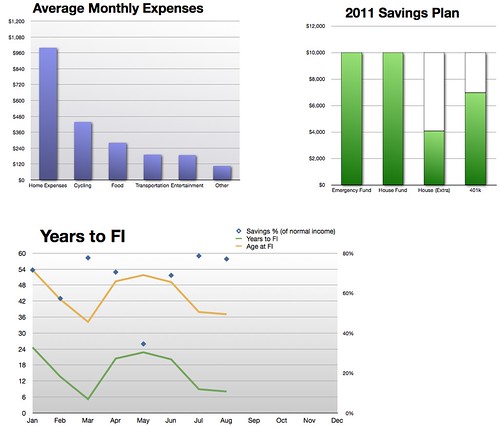

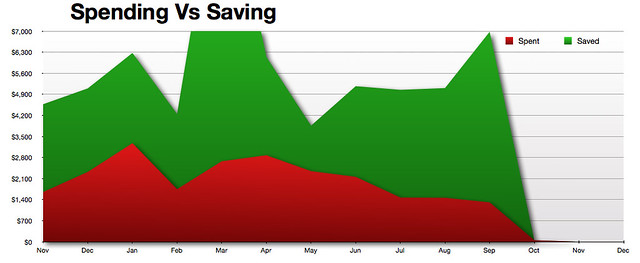

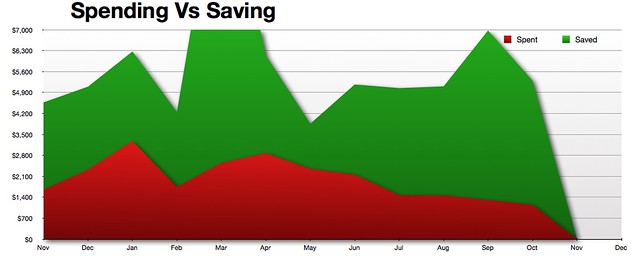

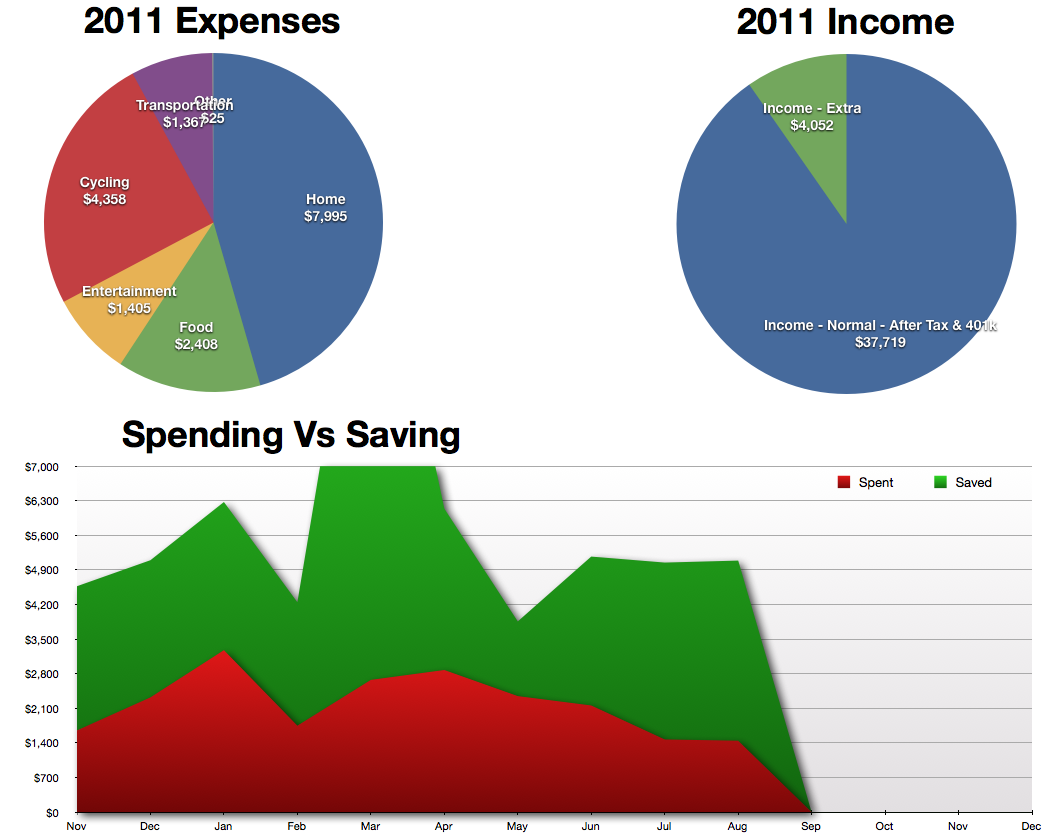

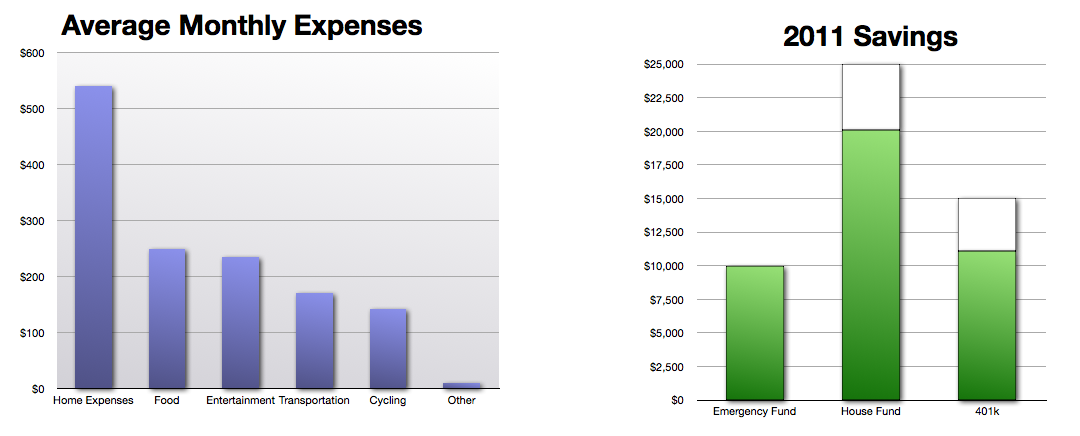

Avg Expenses. Spending Vs Saving:

http://farm7.staticflickr.com/6205/6101 ... cd8c_o.png

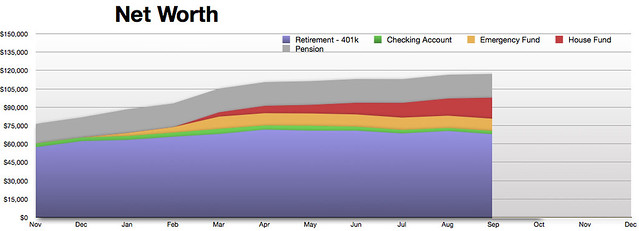

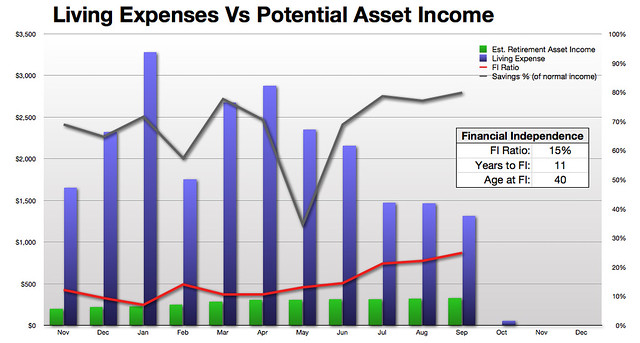

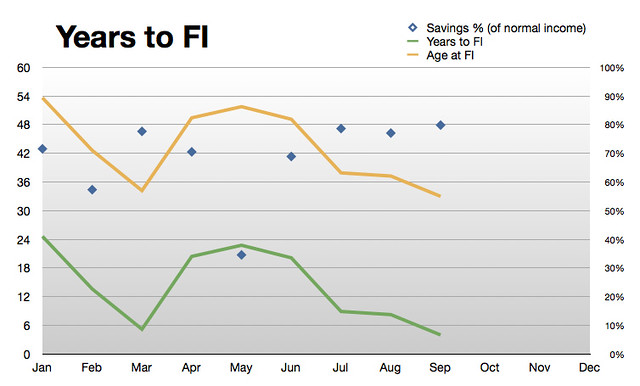

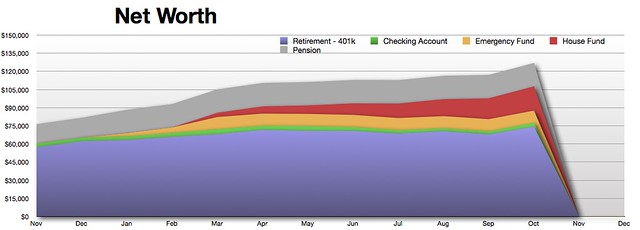

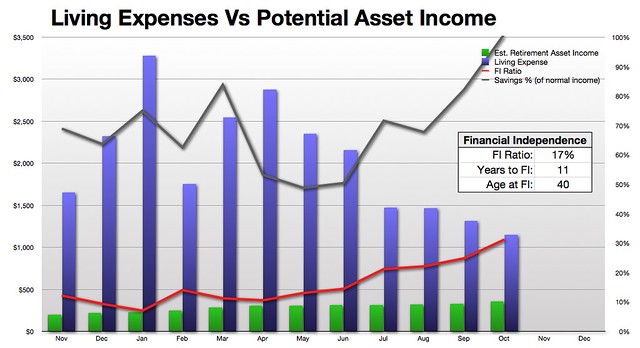

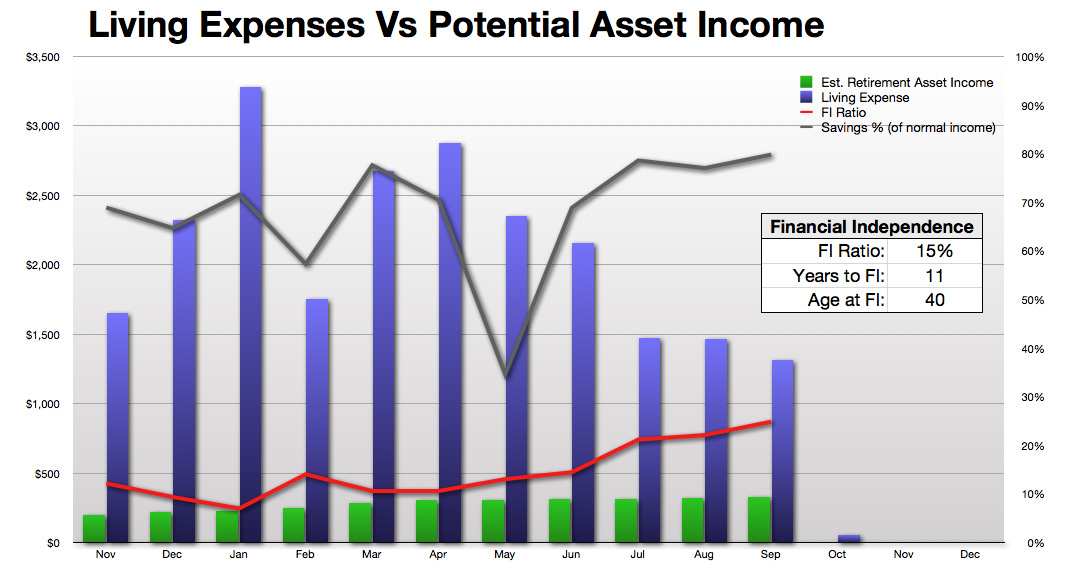

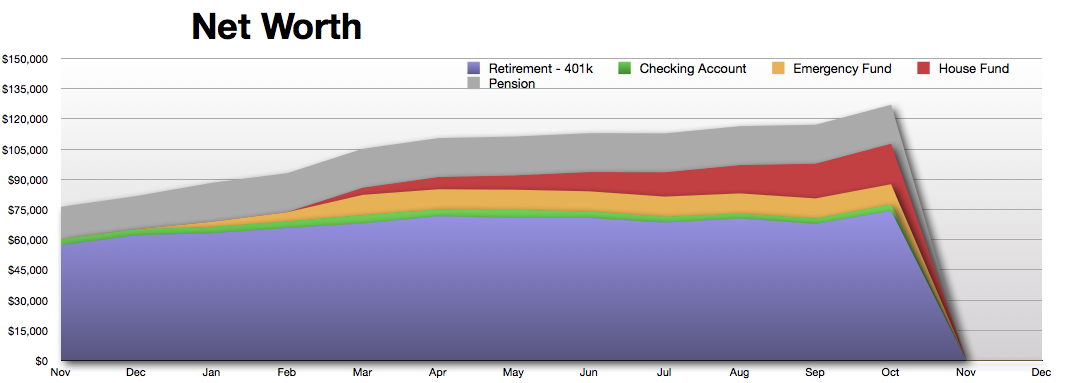

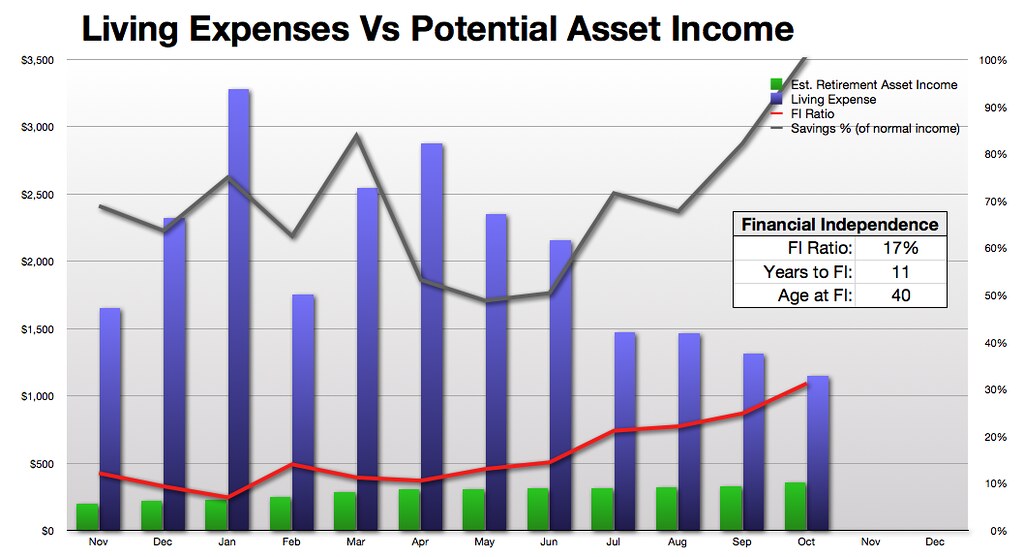

Net Worth. FI Chart.

http://farm7.staticflickr.com/6210/6101 ... 8d6d_o.png

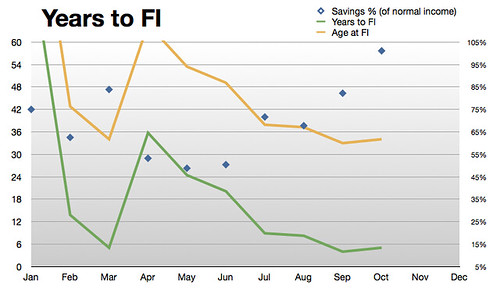

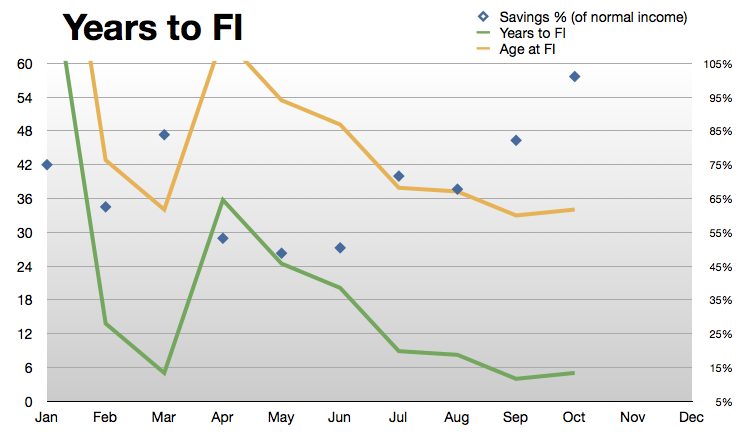

Avg Expenses. Savings. Years left.

http://farm7.staticflickr.com/6083/6101 ... b751_o.png

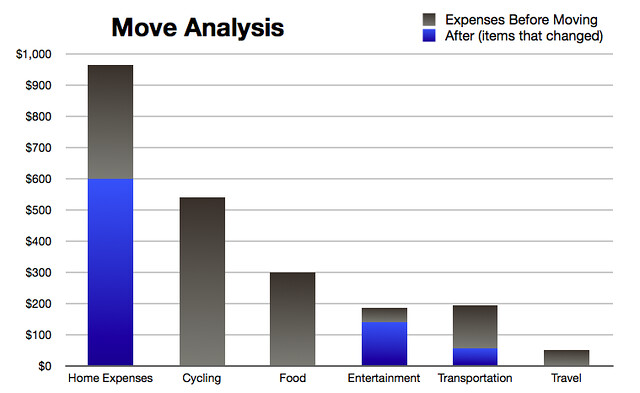

MOVE ANALYSIS:

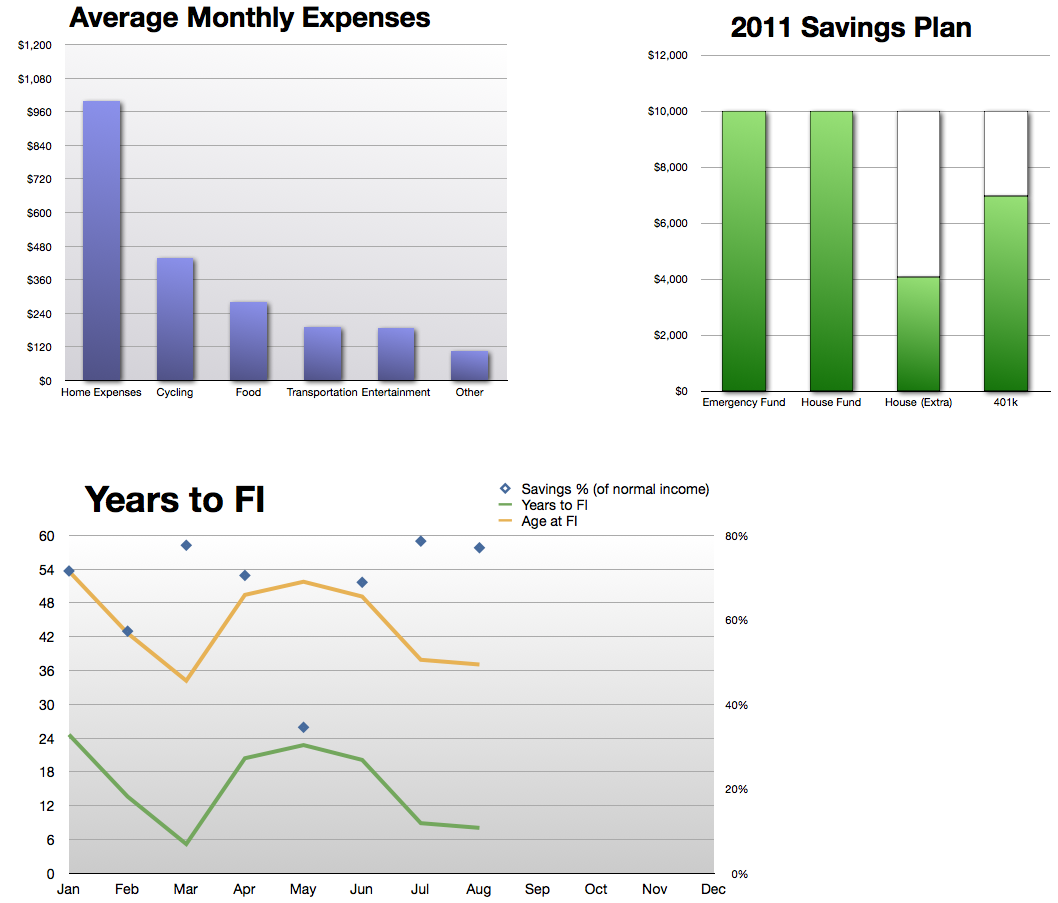

The chart below has a pareto of my expenses. They are not actual numbers but it was easier to use some averages to illustrate. They’re close. The full bars are my expenses before the move. The one’s that reduced have their new values shown in blue. They have an average total monthly expense of $2,220 reduced to $1,660. (a $560, or 25% reduction)

On the other big costs - the $500 per month cycling cost will go down substantially without racing. Maybe to an average of $100 per month or less. Food will probably go down a bit also. To maybe $200 per month. I could have it lower but I want to eat a lot of fruit and vegetables.

I know that It is possible for me to have months below $1,000 expenses (while keeping my current avoidable recurring costs). It would only happen in November this year thought. For September I have already made a trip to Nebraska to visit family (and friends). In October my friends will be coming here and I’ll be spending some for that. December I will probably travel to see family for X-mas. So that only leaves November for this year. The first few months of 2012 will be opportunities.

--------------------------

CYCLING:

--------------------------

I think I’ve gotten my fill of bicycle racing and I’ve decided to stop. I may still race a few times next year depending on whether I feel like it and if I’m still in good enough shape. Maybe I’ll get serious about again in the future. For now I will definitely will not be dedicating such a huge amount of my time to training.

After making this decision, I’ve actually felt at times like I’ve removed a burden. I now have a lot more flexibility with my time and my mental ‘energy’. I think I will perform better at work - I now find myself thinking about work stuff outside of work. Previously it was the other way around - I would think about bike racing while at work.

Some of that physical and creative energy I was devoting to training/racing, I expect I will now devote to more productive things. And for some, I will try to take on other hobbies that are more economical.

I think I had been gradually coming to this decision over the course of the year. My 2 main concerns were safety and the cost. But maybe a turning point was during that 10-day series in June that I was performing poorly. Between some races I stayed with a teammate. He seems to put a lot of thought behind his actions and opinions, and I often listen closely to what he has to say. We were talking about bike racing and he mentioned what everyone knows but either doesn’t care to think about or just doesn’t bring up - that bicycle racing is a very unproductive hobby.

My thoughts:

-- You can’t make any money doing it. It can be pretty expensive

-- You don’t really improve yourself much, or the world in any way by doing it (other than maybe helping to make other people happy.. but the impact is very low compared to effort)

-- It can be very dangerous. It you’re racing frequently, you’re likely to crash a couple times each season. Most of the time you’ll avoid any injury, but you could get a serious injury such as concussions, broken bones, etc. One of my team mates crashed over a year ago and has not completely recovered (and might never). When my brother visited and came to a race, he mentioned afterwords that every guy on my team had scars on the arms/legs from crashing.

The good side of bike racing is that it encourages/requires you to be very healthy and fit. It is also a lot of fun. Winning is great - better than sex, drugs, etc.

Basically, I don’t get enough enjoyment out of it anymore to make it worth all the work. So it’s on to other things now.

I started this thread to get some new ideas:

viewtopic.php?t=1247#post-16369

------------------------------------------------

TRAVEL HOME

------------------------------------------------

I went back "home" - to the state I grew up in mostly and spent about 11 years before moving to where I live now. This was the first time going back since moving up here. I'll discuss it more in another post, but in short, the trip made me realize that for the last few years my life here has been pretty out of balance. I haven't made friends or had any significant relationships here. As comfortable as I may have felt with this, I think I've been missing out on some very important parts of life. I need to make some significant changes on this.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}