C40's Journal

Re: C40's Journal

double post...

Last edited by C40 on Sun Dec 22, 2013 1:26 pm, edited 1 time in total.

-

Standard Staples

- Posts: 37

- Joined: Thu Apr 18, 2013 8:56 pm

Re: C40's Journal

Some solid picks that should do well for you in the long run. I like the even investing in each position, and I'd recommend you throw in some Consumer Staples, Utilities and Financials to balance out. Most utilities offer pretty high yields (4%+), and their growth will be slower than most other categories, but they're pretty safe comparatively speaking. It seems like most REIT's are on sale right now, so you could go after a couple more of them, too. I wouldn't necessarily toss you specific investment advice on this forum, but feel free to PM if you want to bounce any ideas off me. I've recently purchased in all four of these categories.

It has to feel good to lock in 14% of your expenses without having to lift a finger. No hours spent in a cubicle farm, no late night calls about a broken water pipe... just sit back and collect. The great part is, if past performance continues, that % will only grow, since it will handily beat inflation.

It has to feel good to lock in 14% of your expenses without having to lift a finger. No hours spent in a cubicle farm, no late night calls about a broken water pipe... just sit back and collect. The great part is, if past performance continues, that % will only grow, since it will handily beat inflation.

Re: C40's Journal

NOVEMBER

SPENDING: $1,880

- Clothes - $540. ($135 for Red Wings. $400 on clothes!)

- Travel - $424. ($110 Gas, $140 Hotel, $57 out/date, $50 Casino, $50 football ticket)

- Entertainment - $317. ($107 pen, $60 for 7 books, $80 booze/dates)

- Food - $296 ($210 groceries, $60 date, $25 out)

- Home Expenses - $197

- Transportation - $105 ($50 gas, $50 oil/filters)

I’ve spent more this year than I’d like ($18k ytd) but I’m mostly ok with it. I got a raise at work so I’m still saving quite a lot (I’m at $55k YTD and will be very close to my 2013 goal of $60k). Buying a house caused much of the spending increase.

http://farm8.staticflickr.com/7426/1149 ... 4929_c.jpg

http://farm4.staticflickr.com/3735/1149 ... 4a71_c.jpg

http://farm8.staticflickr.com/7298/1149 ... d658_c.jpg

CLOTHES. Lots of clothes.

- Red Wing steel toe boots. Bought a pair when I was in Red Wing, MN for work.

- Work clothes. Pants (3-4 pairs) and shirts (2) for work. I had been buying pants at thrift stores and found some great ones. Got lazy this time and bought new pants.

- Winter coat. Didn’t need this but I wanted a more formal winter coat. I’d seen one I liked at a store a month or two ago and bought it now.

- Also bought a couple ties and a vest. I like to dress more formally sometimes just for fun.

TRAVEL.

- Went back “home” for thanksgiving.

- My old friends were in town so I hung out with them a lot. It’s great seeing them. I don’t have friends like this around anymore. The last few times I’ve seen them it’s driven me to try to build friendships/relationships where I currently live.

- I spent a lot of time with a girl who I’ve known a long time and always had a thing for but never pursued (I had a reason or two at the time but I shouldn’t have let those stop me). I’ve learned over the years that she was always in to me just the same. She lives 1.5 hours away from “home” and has a child, but makes it out to see me most times I go back. It’s always great seeing her, but it also makes me feel a lot of regret and loneliness also.

I’ve written about this before. Moving from the small town I lived in to St. Louis puts me in better position to meet new friends. I’ve been making good progress on the dating/girlfriend side. Need to get better at more actively making friends though. I might make another post on these subjects specifically.

SPENDING: $1,880

- Clothes - $540. ($135 for Red Wings. $400 on clothes!)

- Travel - $424. ($110 Gas, $140 Hotel, $57 out/date, $50 Casino, $50 football ticket)

- Entertainment - $317. ($107 pen, $60 for 7 books, $80 booze/dates)

- Food - $296 ($210 groceries, $60 date, $25 out)

- Home Expenses - $197

- Transportation - $105 ($50 gas, $50 oil/filters)

I’ve spent more this year than I’d like ($18k ytd) but I’m mostly ok with it. I got a raise at work so I’m still saving quite a lot (I’m at $55k YTD and will be very close to my 2013 goal of $60k). Buying a house caused much of the spending increase.

http://farm8.staticflickr.com/7426/1149 ... 4929_c.jpg

{kind=link}

http://farm4.staticflickr.com/3735/1149 ... 4a71_c.jpg

{kind=link}

http://farm8.staticflickr.com/7298/1149 ... d658_c.jpg

{kind=link}

CLOTHES. Lots of clothes.

- Red Wing steel toe boots. Bought a pair when I was in Red Wing, MN for work.

- Work clothes. Pants (3-4 pairs) and shirts (2) for work. I had been buying pants at thrift stores and found some great ones. Got lazy this time and bought new pants.

- Winter coat. Didn’t need this but I wanted a more formal winter coat. I’d seen one I liked at a store a month or two ago and bought it now.

- Also bought a couple ties and a vest. I like to dress more formally sometimes just for fun.

TRAVEL.

- Went back “home” for thanksgiving.

- My old friends were in town so I hung out with them a lot. It’s great seeing them. I don’t have friends like this around anymore. The last few times I’ve seen them it’s driven me to try to build friendships/relationships where I currently live.

- I spent a lot of time with a girl who I’ve known a long time and always had a thing for but never pursued (I had a reason or two at the time but I shouldn’t have let those stop me). I’ve learned over the years that she was always in to me just the same. She lives 1.5 hours away from “home” and has a child, but makes it out to see me most times I go back. It’s always great seeing her, but it also makes me feel a lot of regret and loneliness also.

I’ve written about this before. Moving from the small town I lived in to St. Louis puts me in better position to meet new friends. I’ve been making good progress on the dating/girlfriend side. Need to get better at more actively making friends though. I might make another post on these subjects specifically.

-

jacob

- Site Admin

- Posts: 15996

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: C40's Journal

Your 401k seems to have an extremely smooth ride. What are invested in?

Re: C40's Journal

Jacob - that's hard for me to answer. I don't think I have good records in one place to check. Most of it, most of the time, has been in a US Stock index fund. I've also had the money at times in a Conservative Income fund. I had about $40,000 of PRPFX for a year or so.

Re: C40's Journal

DECEMBER 2013

SPENDING: $3,421 !!

- Entertainment - $2,253

- Home - $690

- Food - $193

- Travel - $189

- Clothes - $63

- Gas - $33

Entertainment spending:

- Computer - $1,600

- Bike trainer - $300

- Nutritional Supplements - $127

- Pen stuff - $77

- Booze - $45

Got a nice laptop computer. Mainly to take with me when I travel for work. I also like being able to use the computer in different rooms. For travel, I'll now be able to use the adobe programs I prefer for Image editing and making shirt designs. It will also be easier to not have to move personal files between my desktop and work laptop. It was expensive - bought a new Macbook pro. I was looking at other laptops but didn't want a Chromebook (can't run programs I want) and didn't want to try Windows 8. I’ve been selling a lot of shirts this year ($1,400). If I increase my efforts I think I could ramp that up. Also, I will probably sell my desktop computer and recoup some of this computer money.

I’d sold my bike trainer and rollers about a year ago, and if I needed to do cardio in the winter I was going to the gym. But now I have my home gym, so I wanted a trainer again. Bought a new one.

Travel out to see my family was fairly cheap. Free air tickets with points from work travel. Paid for parking though. Went out to dinner with my dad and brother and got stuck with the check. This was the 2nd time in a row. Last Christmas we went out, and when they go out, they have a version of check roulette. Each person gives the waiter a credit card and we tell them to pick one. We’ve done this twice – when we went out last year, and again now. I lost last time and it was $115. I lost again this time. Each time I’ve ordered just a meal, while they also get a few drinks. I got kind of pissed off. They knew I didn’t want to go out to eat but went because they wanted to. Whenever I see them it’s because I have spent the money to fly out there. I told them I won’t go out to eat with them in situations like this for a while.

I’ll hold off on posting any charts until my 2013 summary.

RELATIONSHIPS

Dating is going well for now. I met a girl that I get along with well. She’s an ENFP and is opposite from me in many ways. I usually have a great time with her.

She’s annoyed by/doesn’t yet understand my ERE plans and some of my other INTJ behavior. She didn’t ask me to take her out on a dinner date until about the 10th time seeing her though. We agreed on about once per month (I started off basically telling her NEVER. and we met at this). She is fairly frugal. We've hung out something like 13-15 times so far and it hasn't really caused an increase in my spending. Most of the time we're at one of our homes. When we go out, half of the time it's something free like a museum or picnic.

She’s had some rough experiences and prior relationships and is a bit crazy/depressed. I’m all but certain this won’t last long, but we’ll keep going for a now. She helps me improve my relationship skills/behaviors, and it’s good for her to be in a positive, healthy relationship.

SPENDING: $3,421 !!

- Entertainment - $2,253

- Home - $690

- Food - $193

- Travel - $189

- Clothes - $63

- Gas - $33

Entertainment spending:

- Computer - $1,600

- Bike trainer - $300

- Nutritional Supplements - $127

- Pen stuff - $77

- Booze - $45

Got a nice laptop computer. Mainly to take with me when I travel for work. I also like being able to use the computer in different rooms. For travel, I'll now be able to use the adobe programs I prefer for Image editing and making shirt designs. It will also be easier to not have to move personal files between my desktop and work laptop. It was expensive - bought a new Macbook pro. I was looking at other laptops but didn't want a Chromebook (can't run programs I want) and didn't want to try Windows 8. I’ve been selling a lot of shirts this year ($1,400). If I increase my efforts I think I could ramp that up. Also, I will probably sell my desktop computer and recoup some of this computer money.

I’d sold my bike trainer and rollers about a year ago, and if I needed to do cardio in the winter I was going to the gym. But now I have my home gym, so I wanted a trainer again. Bought a new one.

Travel out to see my family was fairly cheap. Free air tickets with points from work travel. Paid for parking though. Went out to dinner with my dad and brother and got stuck with the check. This was the 2nd time in a row. Last Christmas we went out, and when they go out, they have a version of check roulette. Each person gives the waiter a credit card and we tell them to pick one. We’ve done this twice – when we went out last year, and again now. I lost last time and it was $115. I lost again this time. Each time I’ve ordered just a meal, while they also get a few drinks. I got kind of pissed off. They knew I didn’t want to go out to eat but went because they wanted to. Whenever I see them it’s because I have spent the money to fly out there. I told them I won’t go out to eat with them in situations like this for a while.

I’ll hold off on posting any charts until my 2013 summary.

RELATIONSHIPS

Dating is going well for now. I met a girl that I get along with well. She’s an ENFP and is opposite from me in many ways. I usually have a great time with her.

She’s annoyed by/doesn’t yet understand my ERE plans and some of my other INTJ behavior. She didn’t ask me to take her out on a dinner date until about the 10th time seeing her though. We agreed on about once per month (I started off basically telling her NEVER. and we met at this). She is fairly frugal. We've hung out something like 13-15 times so far and it hasn't really caused an increase in my spending. Most of the time we're at one of our homes. When we go out, half of the time it's something free like a museum or picnic.

She’s had some rough experiences and prior relationships and is a bit crazy/depressed. I’m all but certain this won’t last long, but we’ll keep going for a now. She helps me improve my relationship skills/behaviors, and it’s good for her to be in a positive, healthy relationship.

Re: C40's Journal

Congrats on the girl!

I thought it was interesting what you said about the personality types and opposites. beyond the 'opposites attract' (except when they don't) cliche, I've wondered if there aren't dynamics between specific personality types like that. If we can say real generally that one aspect of INTJs is liking the challenge of figuring out things, you'd be hard pressed to find anything more challenging to figure out than a strong ENFP. (added bonus: no self-respecting ENFP would ever want to be predictable or figured out, so as soon as you do, she'll change! ) So in the good combos like that, you get a nice feedback loop where both parties are drawn in further, hopefully for the positive.

Now, looking over y'alls star charts..

The going out for dinner thing reminded me of a conversation I had with a good friend in NYC when I was deciding to quit my job and she suggested I'd have more time for dating. But not money for doing it, I told her. Well, as long as you go out for dinner once a month or so, most women should be happy with that, she told me. So sounds like you're doing great!

On the other hand, it's interesting that she came up with exactly the same metric: going out for dinner. Not sure why that is exactly - maybe it's the food, maybe it's being out and seeing and being seen, maybe it's an excuse to dress up and do something fun, maybe it's just the societal measure of what a good 'date' should consist of. One thing that always bugged me is going past good restaurants and seeing a couple out together and both not talking to each other and just looking bored and unhappy, or just giving up on each other and checking facebook on their iphones- here they went to all the trouble of working probably at least half a day to pay for and then the time in going out (maybe because they couldn't cook a microwave pizza with an how-to video from youtube, but ok) and they're not even enjoying it.

my favorite description of a date restaurant I heard from a broker when looking at an apartment near the bronx: "Oh that's the restaurant where all the girls make their boyfriends take them so they can look at each other's shoes."

So there's all the ways to control the dinner spending (nice BYOB places, ordering tactics, etc) but I wonder if there aren't surrogates that feel like you're going out for dinner but don't cost 90 bucks along the way.. like you mentioned museums -- you go to the a museum or gallery for an opening, everybody's dressed up, maybe there'll be wine and cheese, music.. does that feel more like a date? If you see something live instead of a movie, is that somehow date-ier? (asking a girl out for a Spotify date - good luck with that) I dunno.. more things to figure out..

I thought it was interesting what you said about the personality types and opposites. beyond the 'opposites attract' (except when they don't) cliche, I've wondered if there aren't dynamics between specific personality types like that. If we can say real generally that one aspect of INTJs is liking the challenge of figuring out things, you'd be hard pressed to find anything more challenging to figure out than a strong ENFP. (added bonus: no self-respecting ENFP would ever want to be predictable or figured out, so as soon as you do, she'll change! ) So in the good combos like that, you get a nice feedback loop where both parties are drawn in further, hopefully for the positive.

Now, looking over y'alls star charts..

The going out for dinner thing reminded me of a conversation I had with a good friend in NYC when I was deciding to quit my job and she suggested I'd have more time for dating. But not money for doing it, I told her. Well, as long as you go out for dinner once a month or so, most women should be happy with that, she told me. So sounds like you're doing great!

On the other hand, it's interesting that she came up with exactly the same metric: going out for dinner. Not sure why that is exactly - maybe it's the food, maybe it's being out and seeing and being seen, maybe it's an excuse to dress up and do something fun, maybe it's just the societal measure of what a good 'date' should consist of. One thing that always bugged me is going past good restaurants and seeing a couple out together and both not talking to each other and just looking bored and unhappy, or just giving up on each other and checking facebook on their iphones- here they went to all the trouble of working probably at least half a day to pay for and then the time in going out (maybe because they couldn't cook a microwave pizza with an how-to video from youtube, but ok) and they're not even enjoying it.

my favorite description of a date restaurant I heard from a broker when looking at an apartment near the bronx: "Oh that's the restaurant where all the girls make their boyfriends take them so they can look at each other's shoes."

So there's all the ways to control the dinner spending (nice BYOB places, ordering tactics, etc) but I wonder if there aren't surrogates that feel like you're going out for dinner but don't cost 90 bucks along the way.. like you mentioned museums -- you go to the a museum or gallery for an opening, everybody's dressed up, maybe there'll be wine and cheese, music.. does that feel more like a date? If you see something live instead of a movie, is that somehow date-ier? (asking a girl out for a Spotify date - good luck with that) I dunno.. more things to figure out..

Re: C40's Journal

Interesting thoughts. I hadn't really been thinking this way. I replied in the thread below. (it's more directly relevant there and will get more views/discussion)ebast wrote: I wonder if there aren't surrogates that feel like you're going out for dinner but don't cost 90 bucks along the way.. like you mentioned museums -- you go to the a museum or gallery for an opening, everybody's dressed up, maybe there'll be wine and cheese, music.. does that feel more like a date? If you see something live instead of a movie, is that somehow date-ier? (asking a girl out for a Spotify date - good luck with that) I dunno.. more things to figure out..

viewtopic.php?f=7&t=4561&start=25

Re: C40's Journal

------------------------------------------------

2013 REVIEW

------------------------------------------------

This year I moved to another city and bought a house. I set my 2013 goals assuming I’d stay in the same town all year, so the time and expenses related to moving blew many of my goals.

It’s been a good year for me. I’m happy with the progress I made in many areas (finance, skills), and feel ok enough with others (fitness, social). The new position at work is going pretty well. So far, it has been easier (& lower stress) than my previous role. I should be able to do this until when I currently expect to retire (end of 2017 or early 2018). So that’s another year down my path to FI/ERE. I feel I am pretty happy with my life as it is right now. Work is not so bad, I just don’t like all the time and effort I spend there. The fact that I’m saving a lot and progressing to FI helps me to be as content and happy as I am. I’ve made a lot of progress outside of work lately – learning new things through both doing and reading/watching. I’m looking forward to being able to accelerate that when I don’t have to work so much (the INTJ dream?).

I’ve gotten used to spending little now. I truly believe that if I was saving $0 in either scenario, I’d be just as happy right now spending what I am vs spending 2-3 times as much. The only thing that really causes friction is some cases of people close to me expecting me to spend more.

Here are the goals/plans I set at the start of the year, and my results:

-------------------------------------------------------------------------

FINANCE

-------------------------------------------------------------------------

- Spend $13,000 or less. $21,500. Failed.

- Save $60k $58k. Close

- Spend < $3,000 on food. Stretch goal $2,500 $2,591 YAY

Reduce home cost? Options:

- Move to studio in same building? XX

- Move to apartment/rented home with roommate(s) XX

- Buy & renovate a cheap house (+roommates?) XX

Moved to a house. It will cost more than the apartment. If I get a roommate it would cost about the same as my old apartment. It is much nicer than the apartment. (Apartment was $500/mo, and I paid only electricity. House was $105k)

-------------------------------------------------------------------------

SKILLS

-------------------------------------------------------------------------

- Get better at tracking investments. YES - Acceptable progress.

- Get better at image editing software YES – fair progress

- Further home 5S / Minimalism / Optimization YES

- Get better at gardening NO - Failed due to move

- Home renovation skills? NO – Now I have a house with a good number of potential projects.

- Get good at lucid dreaming. ~~ Only slight progress. Very few work dreams though

---------------------------------------------------------------------------

WORK

---------------------------------------------------------------------------

- Get along better with boss & coworkers ~FAIR

- Get better at politics (or avoiding them) ~NO

---------------------------------------------------------------------------

FITNESS

---------------------------------------------------------------------------

- Deadlift 250# x 10+ YES. In the spring. But can’t now

- Stay in good cardiovascular shape – NO. Neglected due to moving

- Get bodyfat low in summer, keep fairly low next winter NO. Neglected due to moving

- Eat healthier. Cut junk food to nearly zero YES

-------------------------------------------------------------------------

SOCIAL

-------------------------------------------------------------------------

- Make more local friends NO. Moved. Time to start again

-------------------------------------------------------------------------

KEY NUMBERS

-------------------------------------------------------------------------

Income: $79k

Spent: $21.5k

Saved: $57.5k

Savings rate: 73%

Net worth, start of year: $197k

Investment growth/income: $14.5k

Net worth, end of year: $269k

Return on total capital: ~ 6%

Buying the house impacted my investing a lot. In a good way and also bad:

- Good that I sold some things before they went down more (esp. gold)

- Bad that I had much of my capital in cash this year (post tax was because I was getting ready to pay cash for a house… Pre-tax I sold my PRPFX- which was about a third of my 401k, got busy with other stuff, and left it in cash the rest of the year)

-------------------------------------------------------------------------

SPENDING DETAILS

-------------------------------------------------------------------------

My spending was similar to last year. The big thing that changed was house-related costs. I got extra income from work to pay for the moving/house expenses. I didn’t keep close tabs on how much extra it was, but it appears it basically covered my extra spending for the year since I was still really close on my savings target. (If I’d just moved to another apartment, I would’ve come out far ahead. But so far I’m happy with the house).

-------------------------------------------------------------------------

CHARTS

-------------------------------------------------------------------------

I’m going a bit overboard with the charts. Many of the information is redundant (it’s basically the same info shown many times in different ways). Rather than pare them down, I’ll just dump them all here.

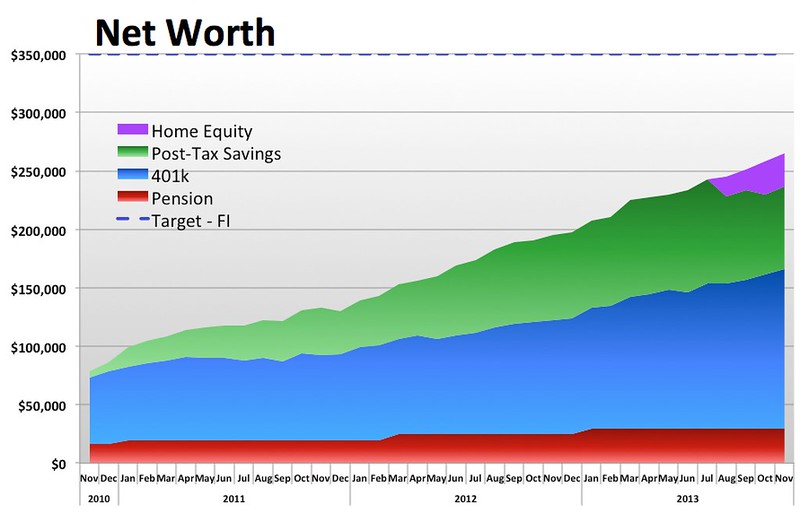

NET WORTH:

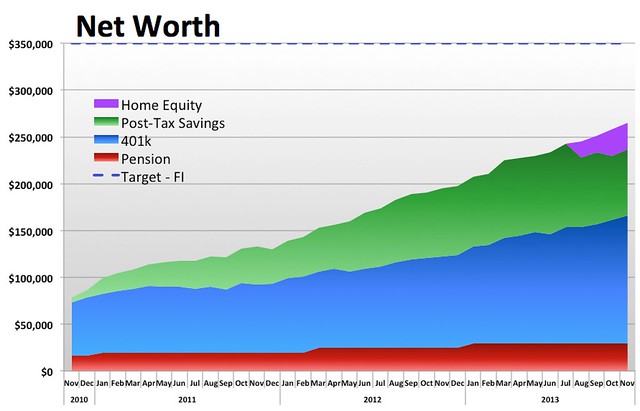

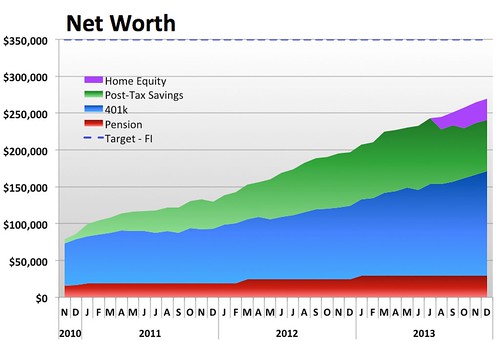

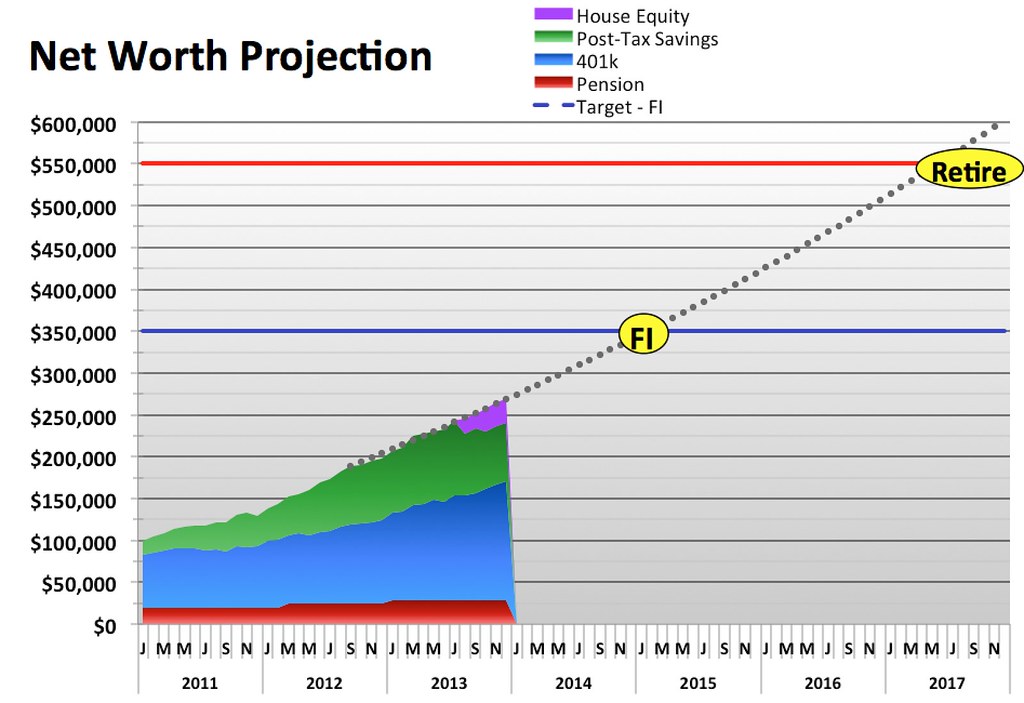

http://farm6.staticflickr.com/5503/1191 ... 9da0_b.jpg

The house is going to suck up $100k of my net worth.

NET WORTH vs PROJECTION

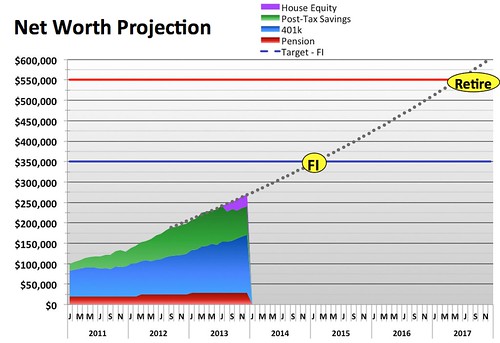

http://farm4.staticflickr.com/3781/1191 ... c56e_b.jpg

I’m on track with this plan. I missed out on a lot of gain from the stock market (related to moving) but if I hadn’t moved I might have stayed in the PP all year and lost rather than gain anything.

NET WORTH IN YEARS

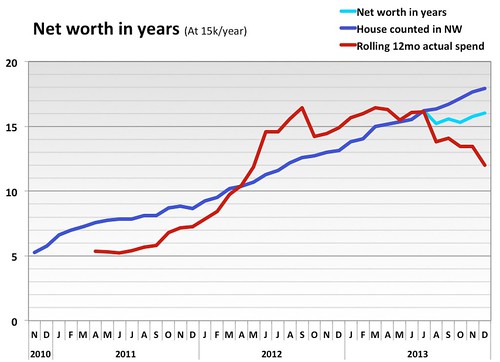

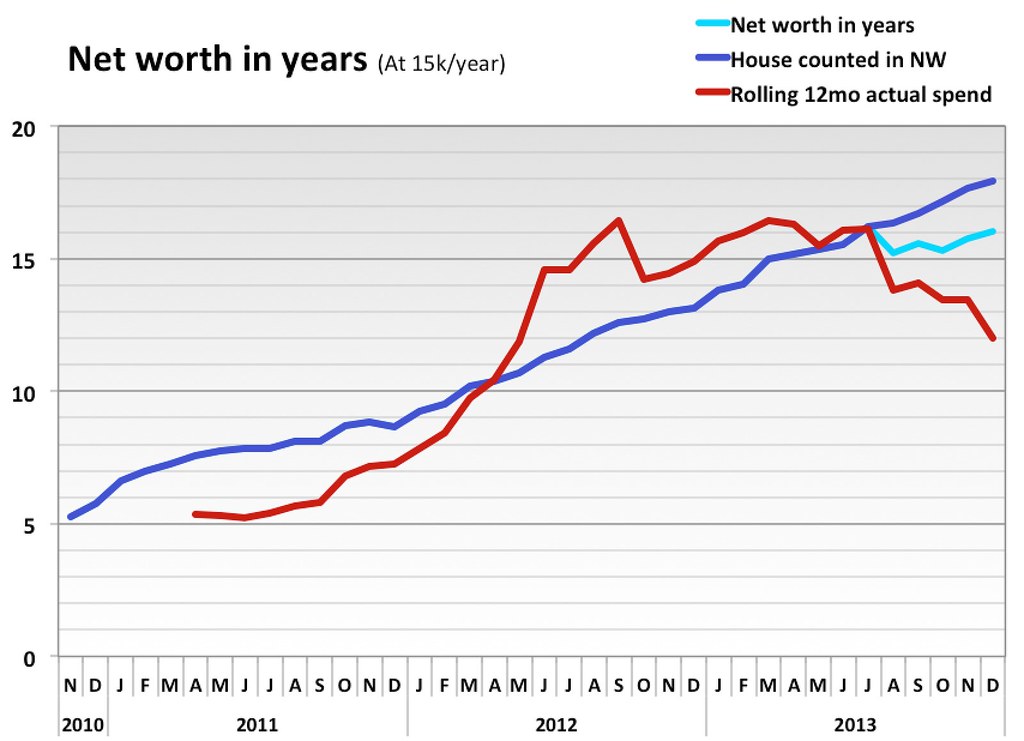

http://farm8.staticflickr.com/7305/1191 ... 0566_b.jpg

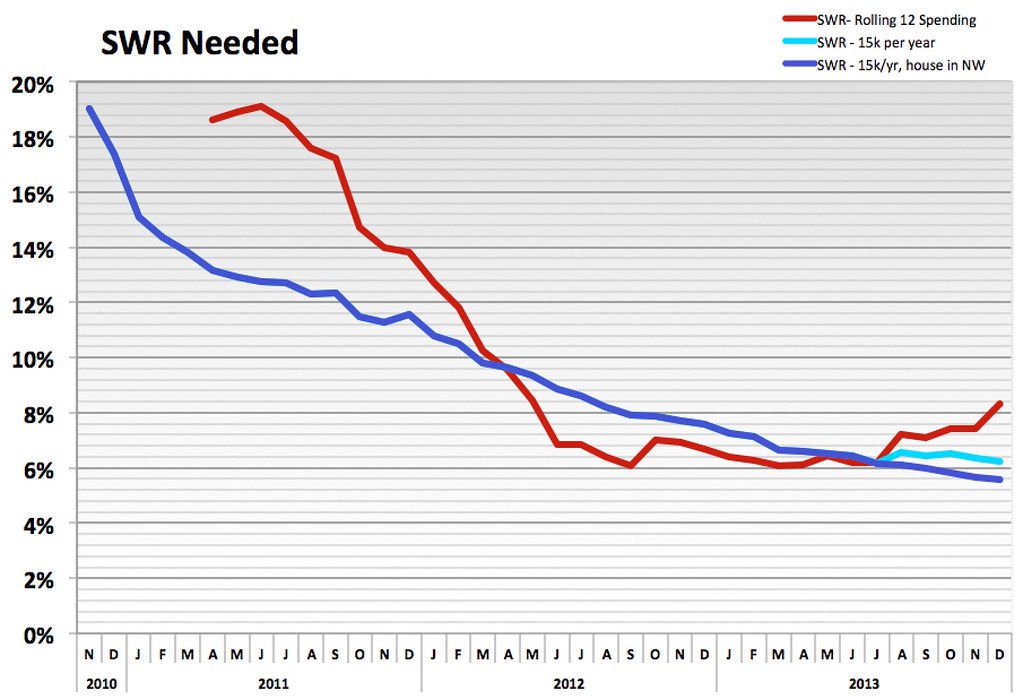

My spending going up has impacted this (and the SWR) chart a lot lately. I don’t think that’s truly reflective of the future spending power of the capital, so I’ve added a couple other lines – both using an assumed $15k of spending. One includes the portion of my net worth tied up in the house (for the scenario of selling the house and renting/traveling) and one does not include the house.

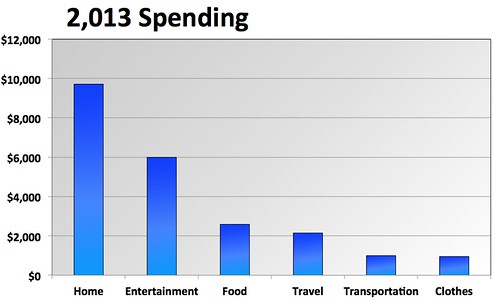

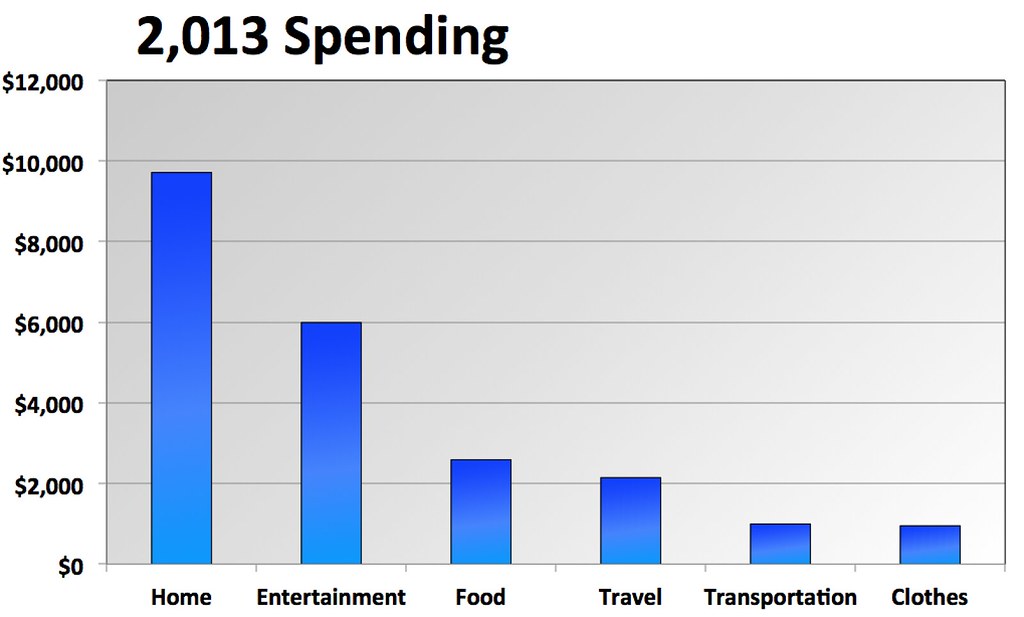

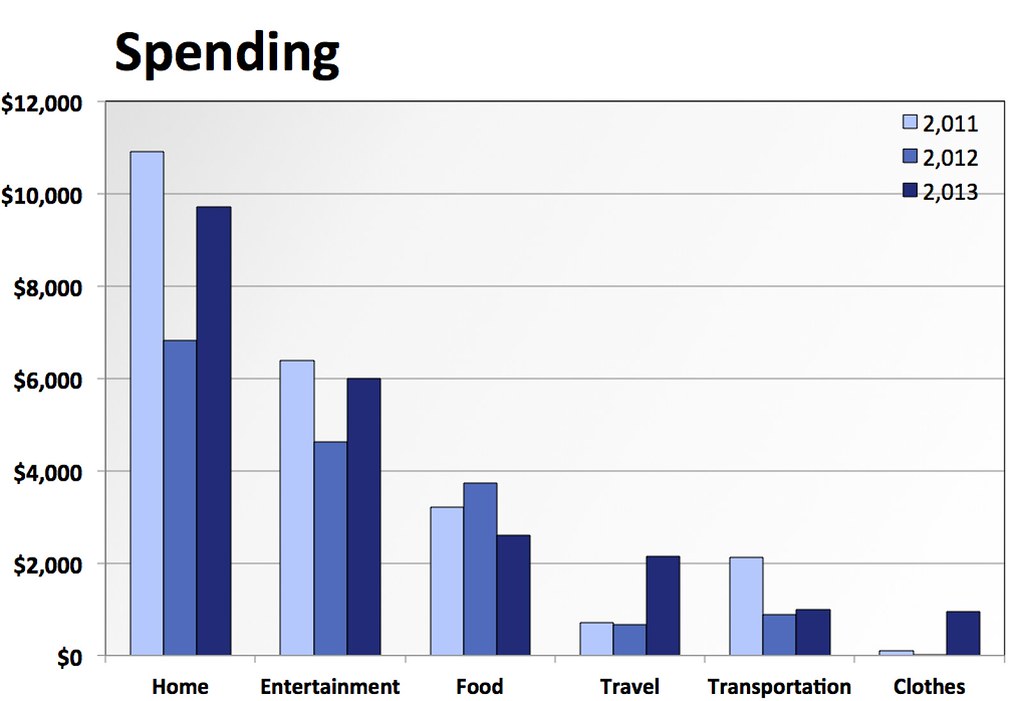

2013 SPENDING PARETO:

http://farm8.staticflickr.com/7431/1191 ... 4bc6_b.jpg

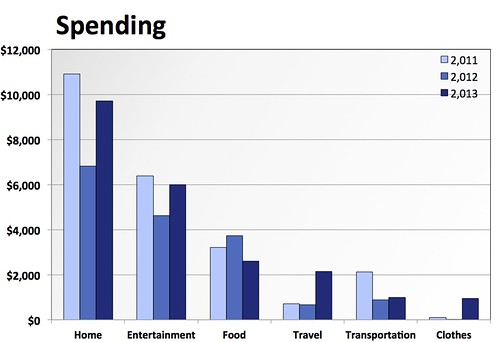

SPENDING PARETO – Last 3 years

http://farm4.staticflickr.com/3785/1191 ... 9769_b.jpg

It’s been pretty consistent. Guess I’m happy with that. Could reduce more but at this point it’s not that high of a priority for me.

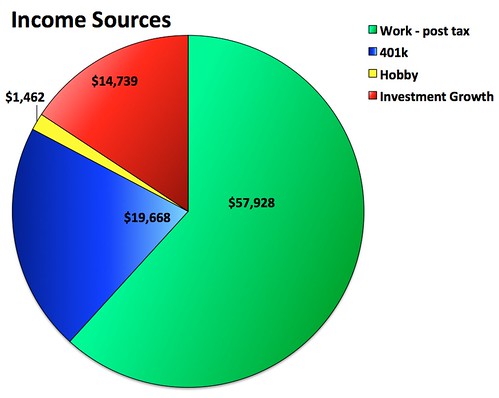

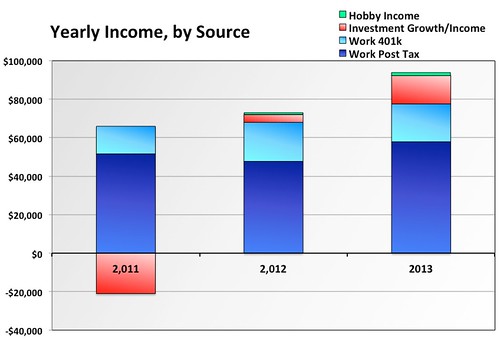

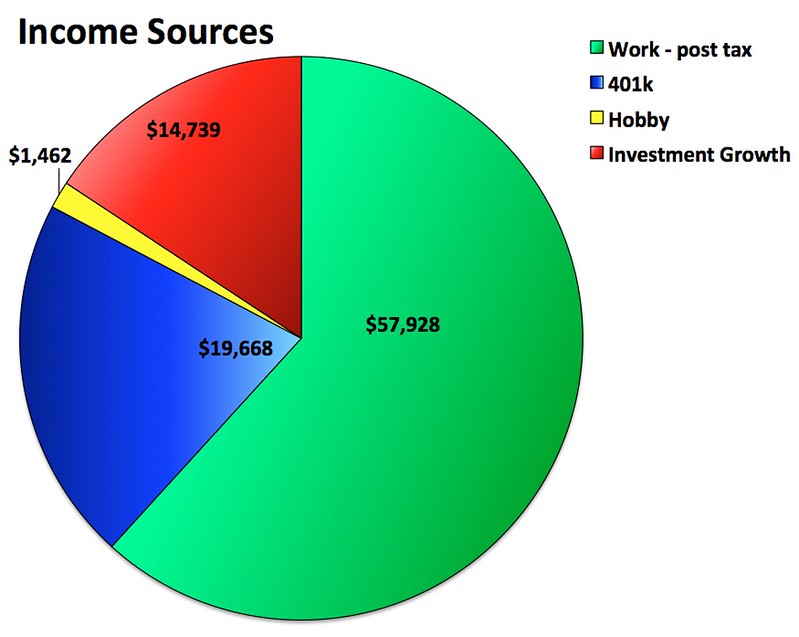

2013 INCOME SOURCES:

http://farm8.staticflickr.com/7392/1191 ... e591_c.jpg

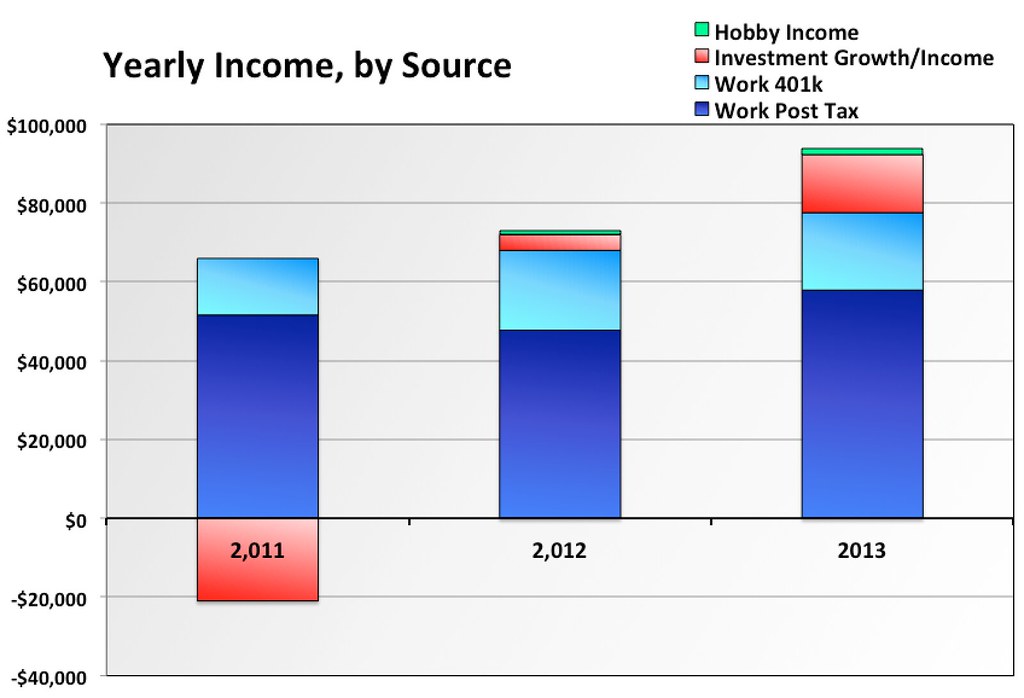

INCOME SOURCES – Last 3 years:

http://farm8.staticflickr.com/7367/1191 ... f834_b.jpg

Work income will be a bit lower in 2014 (Won’t include extra relocation money). Great to see investment returns going up.

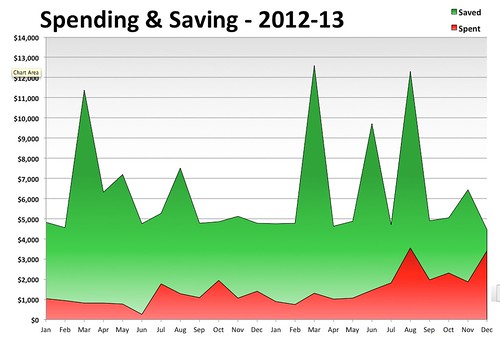

SAVINGS %:

http://farm4.staticflickr.com/3686/1178 ... 191a_b.jpg

http://farm6.staticflickr.com/5479/1191 ... 26fd_z.jpg

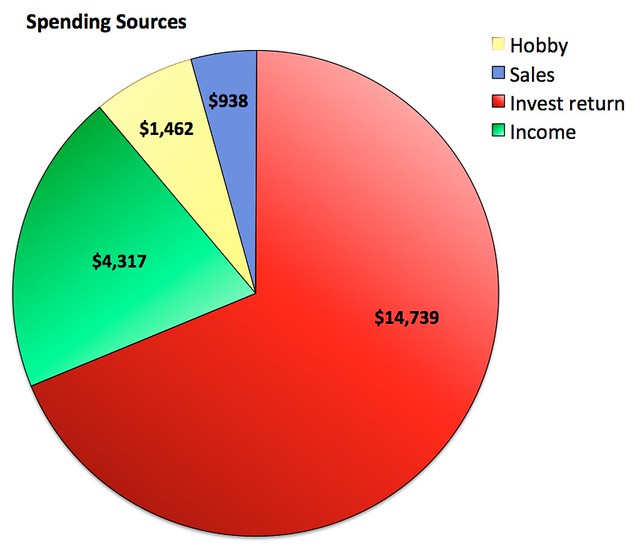

For the money I spent in 2013, this is where it could have come from. (All red = FI)

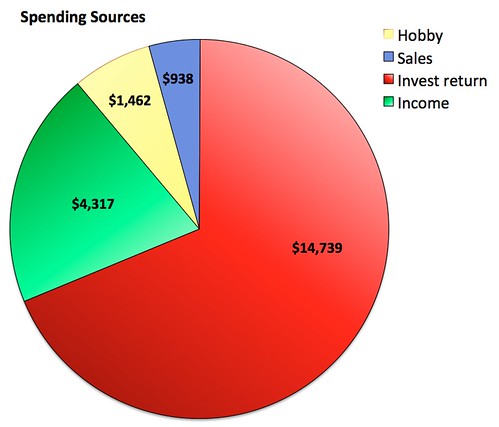

http://farm8.staticflickr.com/7353/1191 ... 2f37_b.jpg

Same information, by year.

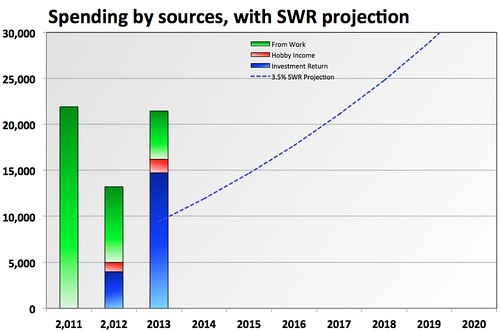

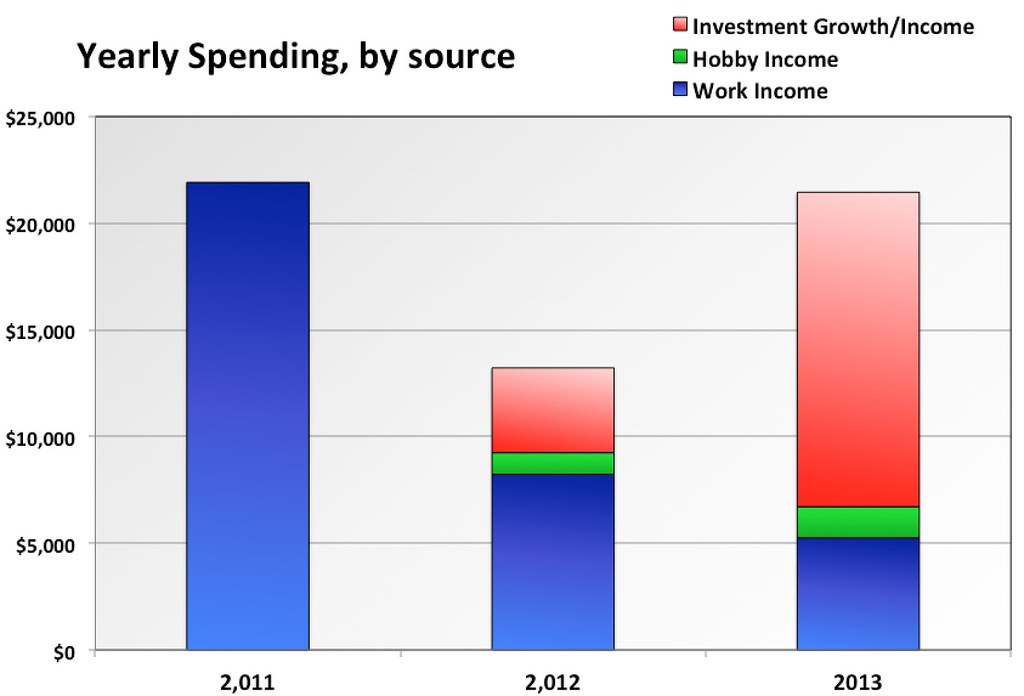

SPENDING by SOURCE – by Year, with projection of capital returns:

http://farm6.staticflickr.com/5496/1191 ... e2f6_b.jpg

I thought this was pretty interesting

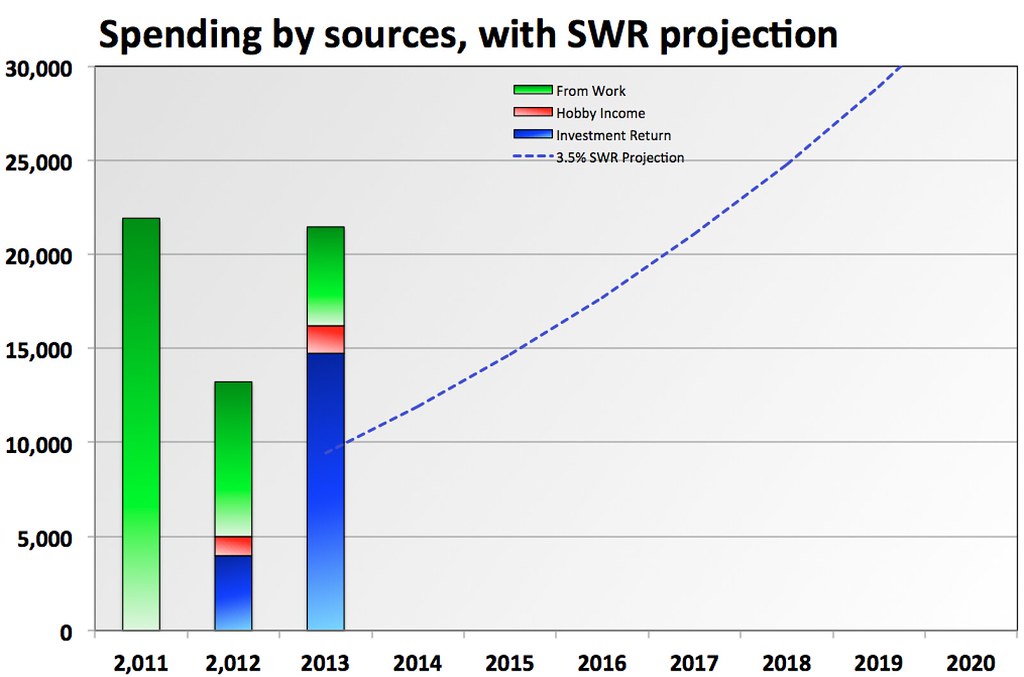

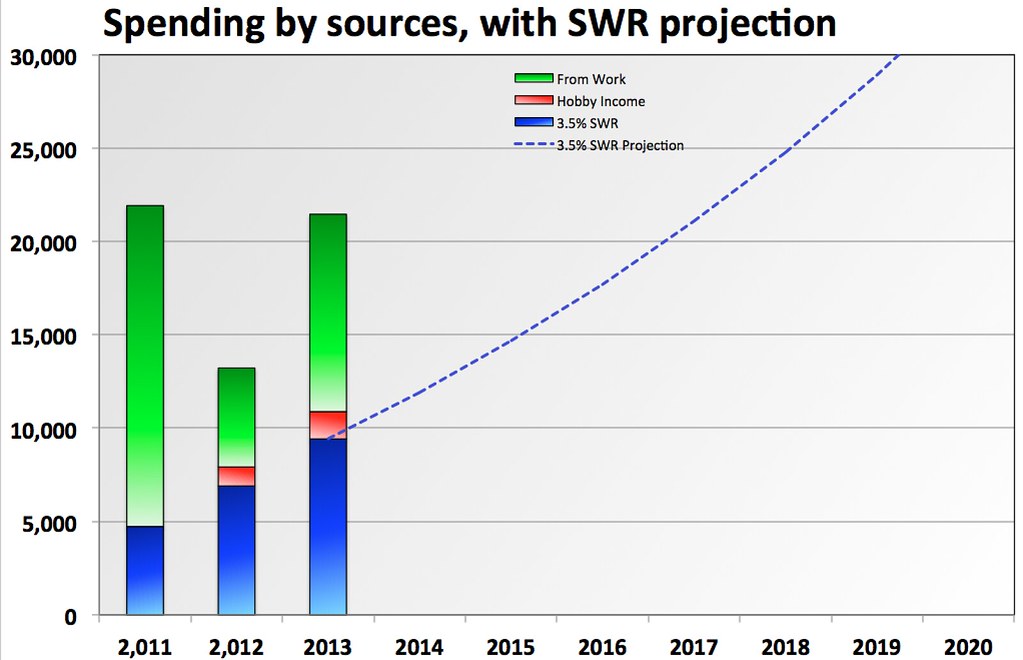

Same thing, but showing only 3.5% SWR instead of actual past returns:

http://farm6.staticflickr.com/5494/1191 ... fdf1_b.jpg

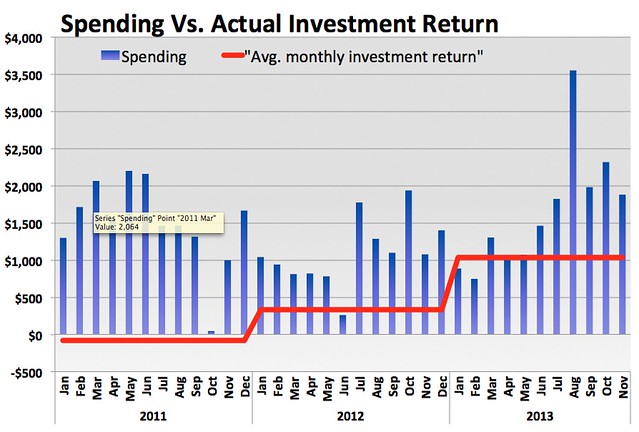

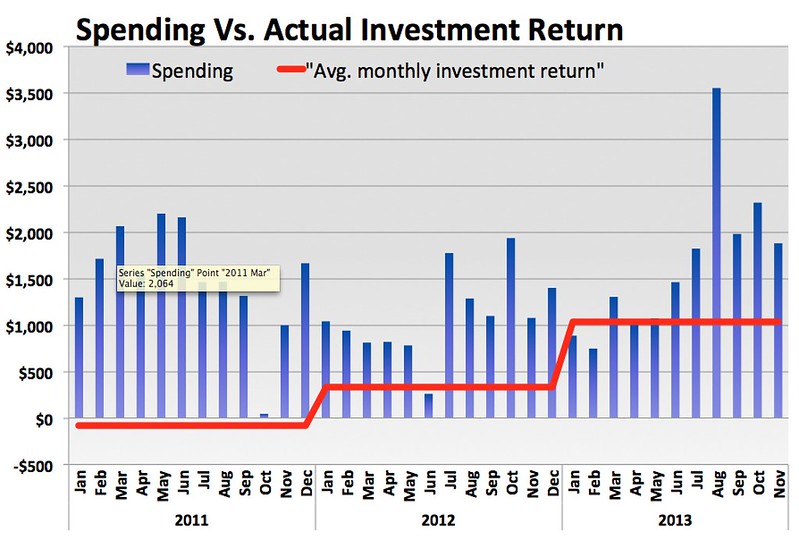

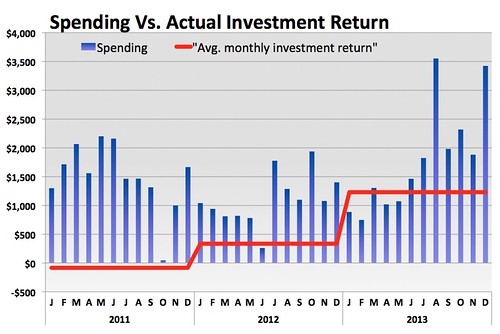

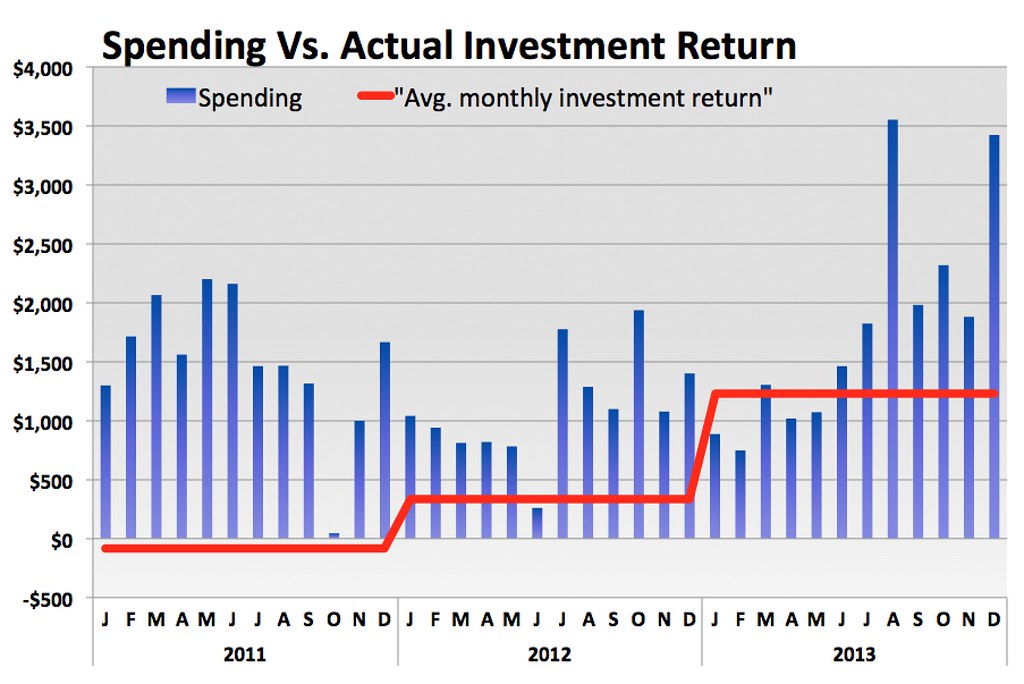

SPENDING vs ACTUAL CAPITAL RETURNS:

http://farm6.staticflickr.com/5476/1178 ... 9c76_b.jpg

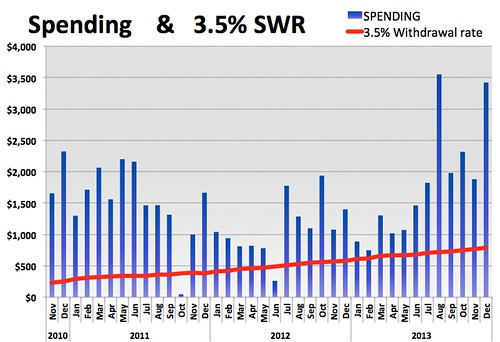

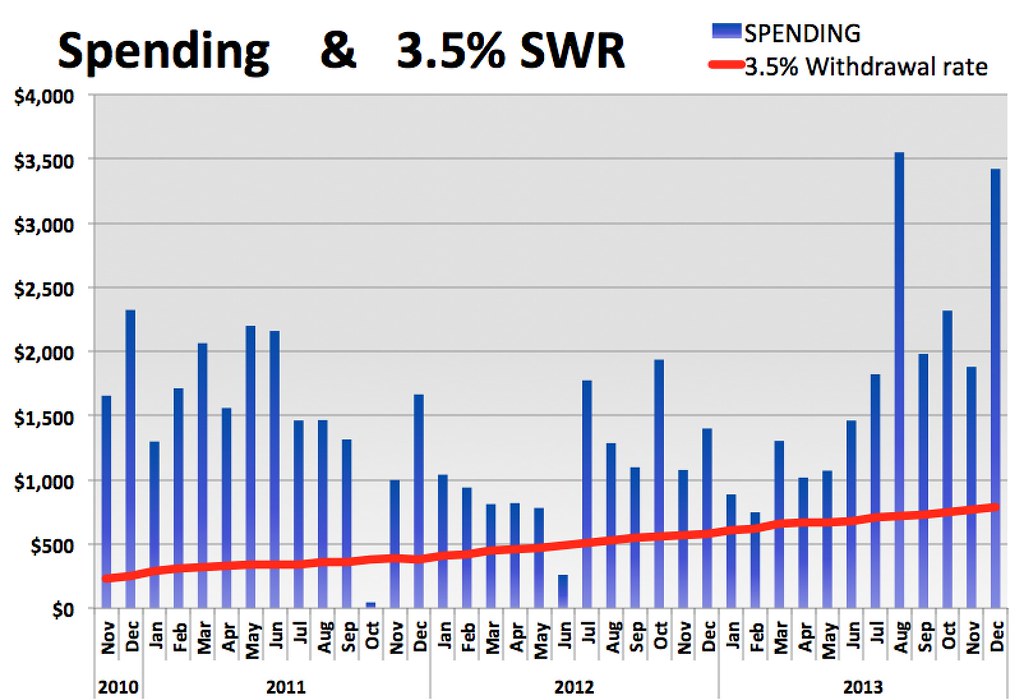

SPENDING VS 3.5% SWR:

http://farm3.staticflickr.com/2845/1191 ... 5c59_b.jpg

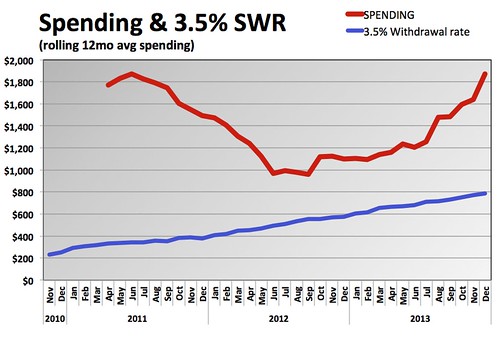

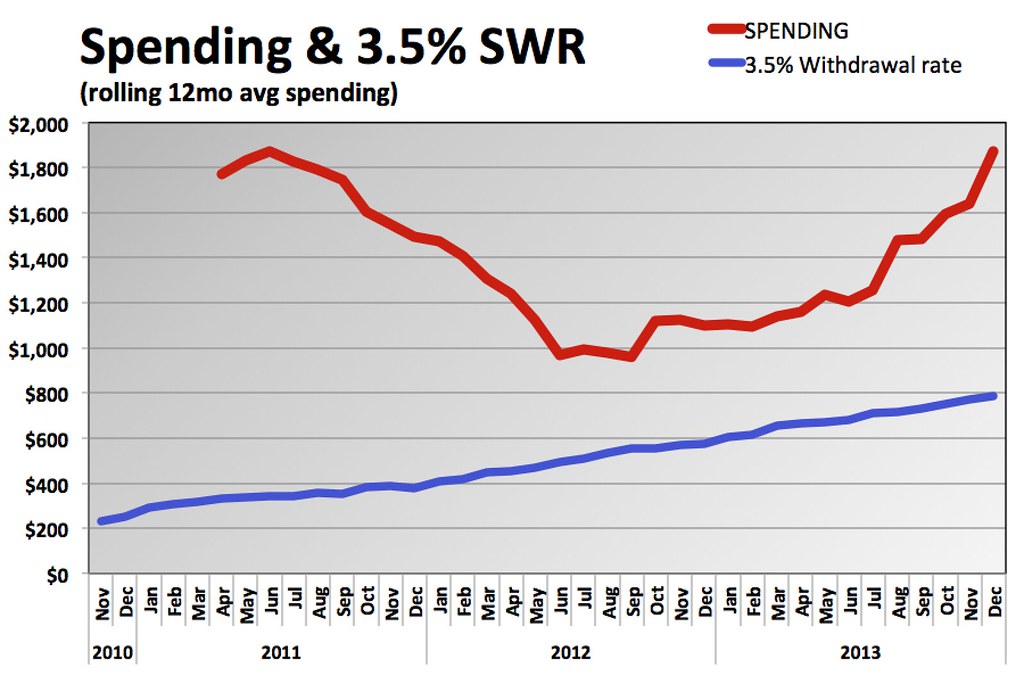

Rolling 12 month avg spending vs 3.5% SWR:

http://farm4.staticflickr.com/3703/1191 ... 7c6a_b.jpg

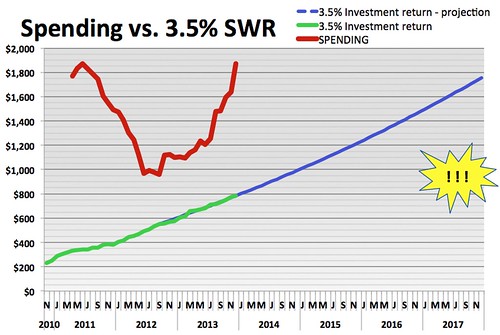

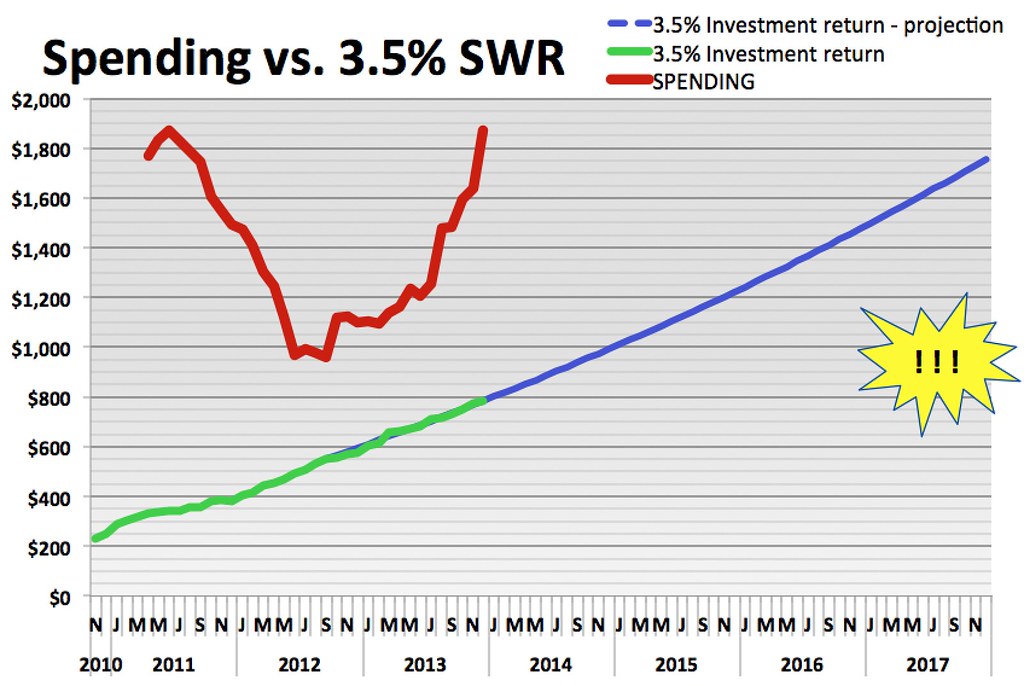

Rolling avg spending vs. 3.5% SWR – with projection

http://farm3.staticflickr.com/2856/1191 ... a142_b.jpg

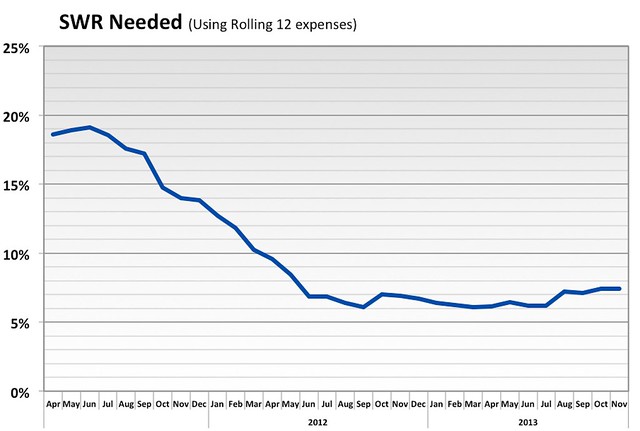

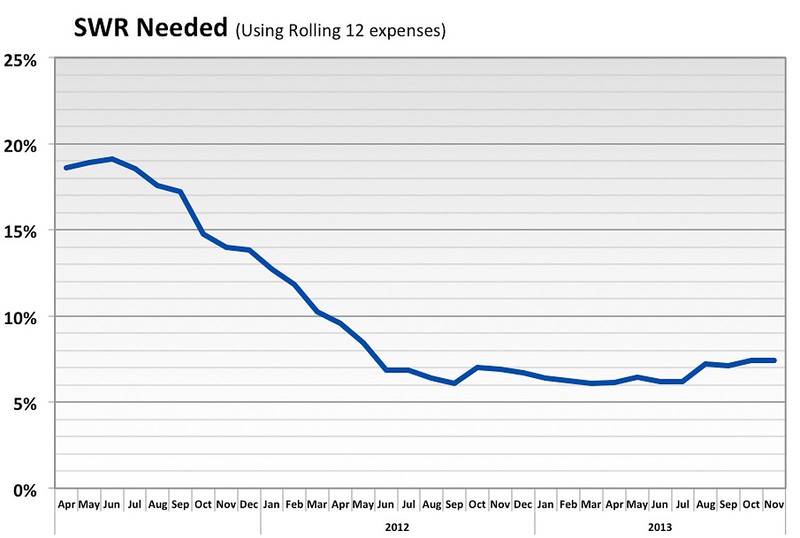

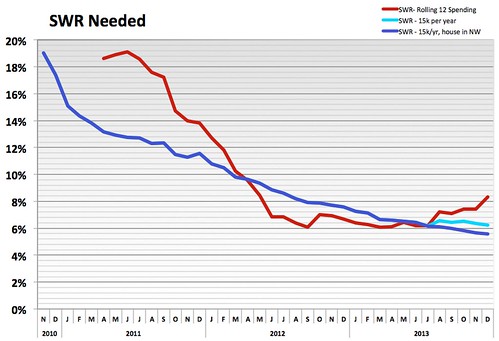

SWR NEEDED:

http://farm6.staticflickr.com/5497/1178 ... c7a0_b.jpg

2013 REVIEW

------------------------------------------------

This year I moved to another city and bought a house. I set my 2013 goals assuming I’d stay in the same town all year, so the time and expenses related to moving blew many of my goals.

It’s been a good year for me. I’m happy with the progress I made in many areas (finance, skills), and feel ok enough with others (fitness, social). The new position at work is going pretty well. So far, it has been easier (& lower stress) than my previous role. I should be able to do this until when I currently expect to retire (end of 2017 or early 2018). So that’s another year down my path to FI/ERE. I feel I am pretty happy with my life as it is right now. Work is not so bad, I just don’t like all the time and effort I spend there. The fact that I’m saving a lot and progressing to FI helps me to be as content and happy as I am. I’ve made a lot of progress outside of work lately – learning new things through both doing and reading/watching. I’m looking forward to being able to accelerate that when I don’t have to work so much (the INTJ dream?).

I’ve gotten used to spending little now. I truly believe that if I was saving $0 in either scenario, I’d be just as happy right now spending what I am vs spending 2-3 times as much. The only thing that really causes friction is some cases of people close to me expecting me to spend more.

Here are the goals/plans I set at the start of the year, and my results:

-------------------------------------------------------------------------

FINANCE

-------------------------------------------------------------------------

- Spend $13,000 or less. $21,500. Failed.

- Save $60k $58k. Close

- Spend < $3,000 on food. Stretch goal $2,500 $2,591 YAY

Reduce home cost? Options:

- Move to studio in same building? XX

- Move to apartment/rented home with roommate(s) XX

- Buy & renovate a cheap house (+roommates?) XX

Moved to a house. It will cost more than the apartment. If I get a roommate it would cost about the same as my old apartment. It is much nicer than the apartment. (Apartment was $500/mo, and I paid only electricity. House was $105k)

-------------------------------------------------------------------------

SKILLS

-------------------------------------------------------------------------

- Get better at tracking investments. YES - Acceptable progress.

- Get better at image editing software YES – fair progress

- Further home 5S / Minimalism / Optimization YES

- Get better at gardening NO - Failed due to move

- Home renovation skills? NO – Now I have a house with a good number of potential projects.

- Get good at lucid dreaming. ~~ Only slight progress. Very few work dreams though

---------------------------------------------------------------------------

WORK

---------------------------------------------------------------------------

- Get along better with boss & coworkers ~FAIR

- Get better at politics (or avoiding them) ~NO

---------------------------------------------------------------------------

FITNESS

---------------------------------------------------------------------------

- Deadlift 250# x 10+ YES. In the spring. But can’t now

- Stay in good cardiovascular shape – NO. Neglected due to moving

- Get bodyfat low in summer, keep fairly low next winter NO. Neglected due to moving

- Eat healthier. Cut junk food to nearly zero YES

-------------------------------------------------------------------------

SOCIAL

-------------------------------------------------------------------------

- Make more local friends NO. Moved. Time to start again

-------------------------------------------------------------------------

KEY NUMBERS

-------------------------------------------------------------------------

Income: $79k

Spent: $21.5k

Saved: $57.5k

Savings rate: 73%

Net worth, start of year: $197k

Investment growth/income: $14.5k

Net worth, end of year: $269k

Return on total capital: ~ 6%

Buying the house impacted my investing a lot. In a good way and also bad:

- Good that I sold some things before they went down more (esp. gold)

- Bad that I had much of my capital in cash this year (post tax was because I was getting ready to pay cash for a house… Pre-tax I sold my PRPFX- which was about a third of my 401k, got busy with other stuff, and left it in cash the rest of the year)

-------------------------------------------------------------------------

SPENDING DETAILS

-------------------------------------------------------------------------

My spending was similar to last year. The big thing that changed was house-related costs. I got extra income from work to pay for the moving/house expenses. I didn’t keep close tabs on how much extra it was, but it appears it basically covered my extra spending for the year since I was still really close on my savings target. (If I’d just moved to another apartment, I would’ve come out far ahead. But so far I’m happy with the house).

-------------------------------------------------------------------------

CHARTS

-------------------------------------------------------------------------

I’m going a bit overboard with the charts. Many of the information is redundant (it’s basically the same info shown many times in different ways). Rather than pare them down, I’ll just dump them all here.

NET WORTH:

http://farm6.staticflickr.com/5503/1191 ... 9da0_b.jpg

{kind=link}

The house is going to suck up $100k of my net worth.

NET WORTH vs PROJECTION

http://farm4.staticflickr.com/3781/1191 ... c56e_b.jpg

{kind=link}

I’m on track with this plan. I missed out on a lot of gain from the stock market (related to moving) but if I hadn’t moved I might have stayed in the PP all year and lost rather than gain anything.

NET WORTH IN YEARS

http://farm8.staticflickr.com/7305/1191 ... 0566_b.jpg

{kind=link}

My spending going up has impacted this (and the SWR) chart a lot lately. I don’t think that’s truly reflective of the future spending power of the capital, so I’ve added a couple other lines – both using an assumed $15k of spending. One includes the portion of my net worth tied up in the house (for the scenario of selling the house and renting/traveling) and one does not include the house.

2013 SPENDING PARETO:

http://farm8.staticflickr.com/7431/1191 ... 4bc6_b.jpg

{kind=link}

SPENDING PARETO – Last 3 years

http://farm4.staticflickr.com/3785/1191 ... 9769_b.jpg

{kind=link}

It’s been pretty consistent. Guess I’m happy with that. Could reduce more but at this point it’s not that high of a priority for me.

2013 INCOME SOURCES:

http://farm8.staticflickr.com/7392/1191 ... e591_c.jpg

{kind=link}

INCOME SOURCES – Last 3 years:

http://farm8.staticflickr.com/7367/1191 ... f834_b.jpg

{kind=link}

Work income will be a bit lower in 2014 (Won’t include extra relocation money). Great to see investment returns going up.

SAVINGS %:

http://farm4.staticflickr.com/3686/1178 ... 191a_b.jpg

{kind=link}

http://farm6.staticflickr.com/5479/1191 ... 26fd_z.jpg

{kind=link}

For the money I spent in 2013, this is where it could have come from. (All red = FI)

http://farm8.staticflickr.com/7353/1191 ... 2f37_b.jpg

{kind=link}

Same information, by year.

SPENDING by SOURCE – by Year, with projection of capital returns:

http://farm6.staticflickr.com/5496/1191 ... e2f6_b.jpg

{kind=link}

I thought this was pretty interesting

Same thing, but showing only 3.5% SWR instead of actual past returns:

http://farm6.staticflickr.com/5494/1191 ... fdf1_b.jpg

{kind=link}

SPENDING vs ACTUAL CAPITAL RETURNS:

http://farm6.staticflickr.com/5476/1178 ... 9c76_b.jpg

{kind=link}

SPENDING VS 3.5% SWR:

http://farm3.staticflickr.com/2845/1191 ... 5c59_b.jpg

{kind=link}

Rolling 12 month avg spending vs 3.5% SWR:

http://farm4.staticflickr.com/3703/1191 ... 7c6a_b.jpg

{kind=link}

Rolling avg spending vs. 3.5% SWR – with projection

http://farm3.staticflickr.com/2856/1191 ... a142_b.jpg

{kind=link}

SWR NEEDED:

http://farm6.staticflickr.com/5497/1178 ... c7a0_b.jpg

{kind=link}

Re: C40's Journal

Impressive charts, thanks for sharing!

May I ask how you calculate your future pension into current net worth?

EDIT: Never mind, I went back to the beginning of your journal and found this:

It's scary how often this gets mentioned on this forum. I'm starting to get this too, as people are beginning to realise it's not just a phase:)The only thing that really causes friction is some cases of people close to me expecting me to spend more.

May I ask how you calculate your future pension into current net worth?

EDIT: Never mind, I went back to the beginning of your journal and found this:

Also, got some good ideas for my own tracking, thanks:)Also note in the Net Worth graph that I added in my work pension value. I never had this on before. I was looking at work retirement stuff and reviewed some Pension information. It seems like they changed how it works within the last couple years. Before, you would use a formula to calculate how much money you can get when you retire. You just do this math with how many years you work and your age and your highest salary, and it spits out a monthly figure. But now when I go look at it, they show a specific value, $19,300, that is supposedly mine. The pension is fully vested, and from the short explanations I've read, that means that they owe me the money, and my employment ends tomorrow, they have to give me that $19,300. So I added that to my net worth total. I was surprised how much they are putting in there - over $5,000 this year, which comes to 7% of my salary. I estimated how much the value would've been for all the months before July, so it shows up on the net worth graph like it was always in there.

Re: C40's Journal

Just wanted to say I look forward to reading your updates due to your charts and aggressive savings. It looks like you are Excel monkey of sorts in your day job like me (I mean that as a compliment). I also like to take the skills I have learned in the corporate world and apply them to the 'business of me'. Great job and keep it up!

Re: C40's Journal

Great journal, love the charts!... I noticed your housing expenses have been a bit erratic post rent; $197 in Nov then $690 in Dec. Is this just payments/investments balancing out?

Fight those monthly utilities mine are about 40% of what they were when I moved in!... What I did:

*disputed taxes (based on my purchase price)

*wrapped my water pipes in insulation and heat-tape (left house unheated thru at least 0, no probs)

*timed/concentrated heat

*got off gas completely (no min monthly)

*checked with 8 insurance companies, finding cheapest/highest reviewed

*partnered internet with neighbor (dd-wrt router/repeater)

*cancelled trash (at first I just kept compressing it into a standard grocery bag, and would dump it discretely when I bought gas).

Congrats on the house, think you'll do really well there.

Fight those monthly utilities mine are about 40% of what they were when I moved in!... What I did:

*disputed taxes (based on my purchase price)

*wrapped my water pipes in insulation and heat-tape (left house unheated thru at least 0, no probs)

*timed/concentrated heat

*got off gas completely (no min monthly)

*checked with 8 insurance companies, finding cheapest/highest reviewed

*partnered internet with neighbor (dd-wrt router/repeater)

*cancelled trash (at first I just kept compressing it into a standard grocery bag, and would dump it discretely when I bought gas).

Congrats on the house, think you'll do really well there.

Re: C40's Journal

Hey C40. I have been a long time fan of your Journal and have been following along practically since its creation. We are similar in age, networth, and spending so it has been easy to relate. I could never come close to your charting abilities, though.

Question for you.. when the day comes when you say you are FI and retire, are you planning on that 3.5% withdraw to be calculated from all of your combined assets even including your pension? That is the area where I'm constantly battling my approach. My current stretch goal is to be retired off my taxable account only but that means having to work a bit longer to achieve. Just curious what your plan for that is at the moment.

Question for you.. when the day comes when you say you are FI and retire, are you planning on that 3.5% withdraw to be calculated from all of your combined assets even including your pension? That is the area where I'm constantly battling my approach. My current stretch goal is to be retired off my taxable account only but that means having to work a bit longer to achieve. Just curious what your plan for that is at the moment.

Re: C40's Journal

Thanks all for the chart/journal compliments!

@Robby152 - Thanks Yeah, I use Excel a lot at work. I'm the guy some people go ask when they can't figure something out in Excel.

@Henrik - Yeah.. I could have phrased that a little better.. It's not so much of a problem that they just expect me to and I do not.. but rather when we're spending time together and what we want to do clashes (which really isn't so bad). My immediate family and close friends are accepting. I think the biggest challenge will be with SOs.

The tricky part with the pension is that I'll have to pay taxes on it. If I recall correctly, I might be able to send it straight to my 401k or maybe an IRA. I haven't worried about it much yet. Maybe to be safe I should only count a portion of it in my net worth.

@JohnnyH - Thanks. I'll have to try some of those, and think of others.. I haven't considered these costs much so far.

1 - Taxes when I retire from my job and get the pension mentioned above.

2 - Taxes when withdrawing 401k money normally

3 - 401k withdrawal penalties if I take it out in a stupid way for some reason

I think it will work out ok for the following reasons:

1 - Safety factor - I'm planning to save significantly more than my basic FI target. So my actual SWR might be quite a bit lower (or I could reduce my spending if needed). Right now my 401k is a huge portion of my net worth, but now 2/3 of my saving is post-tax, so at retirement it won't be such a huge portion.

2 - I'll probably be making some money through hobbies, part time work, sporadic full time work, etc..

3 - There are things like the 401k 72(t) distributions, or the IRA escape ladder (well, that's what I call it...)

@Robby152 - Thanks Yeah, I use Excel a lot at work. I'm the guy some people go ask when they can't figure something out in Excel.

@Henrik - Yeah.. I could have phrased that a little better.. It's not so much of a problem that they just expect me to and I do not.. but rather when we're spending time together and what we want to do clashes (which really isn't so bad). My immediate family and close friends are accepting. I think the biggest challenge will be with SOs.

The tricky part with the pension is that I'll have to pay taxes on it. If I recall correctly, I might be able to send it straight to my 401k or maybe an IRA. I haven't worried about it much yet. Maybe to be safe I should only count a portion of it in my net worth.

@JohnnyH - Thanks. I'll have to try some of those, and think of others.. I haven't considered these costs much so far.

Yes, for now I'm counting 3.5% of everything (except, at times, for the money tied up in the house). There are some potential pitfalls, including:IwantLess wrote: Question for you.. when the day comes when you say you are FI and retire, are you planning on that 3.5% withdraw to be calculated from all of your combined assets even including your pension? That is the area where I'm constantly battling my approach. My current stretch goal is to be retired off my taxable account only but that means having to work a bit longer to achieve. Just curious what your plan for that is at the moment.

1 - Taxes when I retire from my job and get the pension mentioned above.

2 - Taxes when withdrawing 401k money normally

3 - 401k withdrawal penalties if I take it out in a stupid way for some reason

I think it will work out ok for the following reasons:

1 - Safety factor - I'm planning to save significantly more than my basic FI target. So my actual SWR might be quite a bit lower (or I could reduce my spending if needed). Right now my 401k is a huge portion of my net worth, but now 2/3 of my saving is post-tax, so at retirement it won't be such a huge portion.

2 - I'll probably be making some money through hobbies, part time work, sporadic full time work, etc..

3 - There are things like the 401k 72(t) distributions, or the IRA escape ladder (well, that's what I call it...)

Re: C40's Journal

Does your 401k graph include your yearly contribution (my guess is you contribute to the max) an employer match as well? Keep up with your good work!

Re: C40's Journal

mxlr650 - Yes, the 401k portion of the net worth graph includes my contributions as well as fund price changes (growth mostly, I hope!). This is the case for all of the categories on my net worth chart.

Re: C40's Journal

---------------------------------------------------

JANUARY 2014

---------------------------------------------------

SPENDING: $1,380

- Home - $700

- Food - $300

- Entertainment - $170

- Clothes - $120

- Transportation - $54

- Other ~ $30

$174 of food spending was groceries, $127 out.

Costs related to girlfriend:

$85 – Date, restaurant

$36 – Drinks, out

$22 – Date, ice skating

$21 – Ordered pizza

$15 – Gift

$14 – Coffee/Tea, out

2014 GOALS - INTRO

I have a lot in my goals this year. I haven’t went through much prioritization. I've learned at work how important prioritization is (it's critical for alignment and to have a chance at actually achieving them). I don't think it is as important for one person. I won’t be disappointed if I don’t get all of them done. For the skills, home projects, and fitness, I might be happy to achieve half of them. Things ebb and flow throughout a year and this is my starting point. I want to look back to this list fairly often (monthly) to make sure the short term actions I’m planning for myself are aligned.

I use a 5x8 notebook for keeping track of actions. I have it divided into sections (Finance, House projects, reading, to buy, social, chores/misc, hobbies, and a couple specific hobbies). I take the book with me when I travel. It’s medium-duration actions – most of them will be accomplished within a quarter or half a year. Some weekends I make a separate action list for that weekend – which consists of actions from the book, plus more mundane short-term things like laundry, lifting weights, etc.. Each month or so I want to look back at my yearly goals, consider progress, and check my action book to see if the actions I have are aligned.

Anyways, I’m rambling….

-------------------------------------------------------

2014 PLANS

-------------------------------------------------------

FINANCE

- Spend - $16,000

- Save - $55,000

- Net Worth - $340,000

- Invest all available Money

- Dividends – receive $2,500

- Get Roommate. (Girlfriend or Normal)

- Hobby Income - $2,000

SKILLS

- Read 20+ Books

- Investing – Dividend stock analysis and tracking

- Gardening

- Home renovation / repair

- Image editing (Adobe Illustrator use)

- Lucid dreaming

- Cooking

FITNESS

- Squat / Deadlift – at least 250x10

- Cardio – get/stay in good shape

- Bodyweight & Bodyfat (caliper) -- 160lbs, <=10mm

- Limit drinking

- Eat well

- Yoga & Stretching

SOCIAL

- Dating / Girlfriend (Relationship Experience)

- Make some friends in St Louis

- Get to know neighbors / build social capital in neighborhood

- See family twice

- Get close friend to visit

HOME PROJECTS

Have a list of 12. Not shown here.

Re: C40's Journal

Excellent reviews, plans, charts and progress, as usual!

The entertainment number from 2013 jumps out to me as pretty high. I guess it has some pretty useful stuff in there like a computer though. I wonder if you could split that category apart so that things like a computer would'nt be grouped with things like a $10 movie ticket.

I had girlfriend as a line-item in a former wall chart, and one day my girlfriend saw it and was pretty sore about it.

The entertainment number from 2013 jumps out to me as pretty high. I guess it has some pretty useful stuff in there like a computer though. I wonder if you could split that category apart so that things like a computer would'nt be grouped with things like a $10 movie ticket.

I had girlfriend as a line-item in a former wall chart, and one day my girlfriend saw it and was pretty sore about it.

-

Kriegsspiel

- Posts: 952

- Joined: Fri Aug 03, 2012 9:05 pm

Re: C40's Journal

LOL... nice.akratic wrote: I had girlfriend as a line-item in a former wall chart, and one day my girlfriend saw it and was pretty sore about it.

Re: C40's Journal

Yeah, a lot of the time that I was living in my previous apartment, a big portion of my expenses were entertainment and hobbies.. maybe 40% many months. I kind of liked it this way. I'd prefer my spending be on that instead of high rent, gas for commuting, etc.. One problem was that sometimes I just kept spending on hobbies up until I broke $1,000 for the month.akratic wrote: The entertainment number from 2013 jumps out to me as pretty high. I guess it has some pretty useful stuff in there like a computer though. I wonder if you could split that category apart so that things like a computer would'nt be grouped with things like a $10 movie ticket.

A pretty good chunk of my hobby spending is indeed for semi-permanent things. I don't spend much directly on experiences, but rather buy things I'll generally use for quite a while. Computers, cameras, bikes, etc.. A good chunk of my 2013 computer spending will be offset when I sell the old computer. That's the benefit, IMO, of this type of hobby spending, compared to 'experience' spending. When I buy a computer or a bike, a month later I still have and can use it. When I'm done with it, I can sell it and get back some of the money I spent on it (or if I did really well, all or more money than I spent).

When I buy a plane ticket, restaurant meal, or a sporting event ticket, the money and the usefulness are gone as soon as the experience ends.

I end up shaping my hobbies around this concept. I have very rarely had hobbies where I have to pay for each experience, or pay an ongoing rate. [the only ones that come to mind now are when I had a gym membership (which I ended as soon as I had space to make a gym at home), MMO game subscriptions, and when I used to drink at the bars regularly.]

.... I remember after 2,012, for discussion with some of my personal friends/acquaintances, listing all the fun/hobby things I bought/did while still only spending around $13,000. It was quite a lot. I may end up listing those out for 2,013. $6,000 is a pretty good chunk of money.

My girlfriend knows that I track all my spending and make my charts and such. She did ask me if I keep track of how much money I spend with/on her, and she didn't like that I do. She suggested/told me that I should not track it... She wasn't too surprised about her suggestion not going anywhere.akratic wrote:

I had girlfriend as a line-item in a former wall chart, and one day my girlfriend saw it and was pretty sore about it.