hmm... that might be fun. I have stripped and re-glued tubular tires on my bicycle racing wheels. Not sure how similar that is (probably not much)

I get money from work when I buy (or in this case, repair/maintain) shoes, so I'll probably just wait until next year and mail the old ones to Red Wing.

C40's Journal

------------------------------------

MARCH 2013

------------------------------------

SPENDING: $1,282

Home – $679

Food – Groceries - $188

Food – non grocery - $72

Entertainment: $315

Transportation - $25

Non-standard spending:

Home expense includes $115 for safety razor gear (razor, brush, stand, bowl, soap, blades). Haven’t gotten it yet. Hope I like it.

Entertainment includes $240 of fountain pen stuff. This was 4 pens (one of which was stolen after USPS left it), ink samples, and paper. I use a nice leather journal/book for keeping action item lists and various notes. I’m enjoying the pens so far and it is fun experimenting with ink/pen combinations.

I’ve been trying to acquire some more BIFL stuff. This month, the safety razor and pens won’t be saving me much or any money but I think I will enjoy using them more. These are two examples of shifting back to products of older design/technology – back when things were meant to be used for many years rather than discarded quickly.

I tried to find a high quality lunch box (mine is wearing out and failing in 4 places). I couldn’t find much though. The best options I found were this Stanley and this aluminum one but I didn’t think either one looked good enough (the Stanley handle/latch looks flimsy, and I wish the metal one had some insulation… Maybe I should just use a small cooler). Bought a $15 piece of crap from Target instead.

------------ TOTALS YTD --------------

Got my yearly bonus so I like looking at the YTD total numbers.

Income: $22k

Spent: $3k

Saved: $19k

Savings Rate: 87%

Investment increase: $4k (2% YTD)

Net Worth: $225k

Net worth increase YTD: $28k

Net worth in years: 16.4

3.5% SWR: $650/month

SWR Needed @ current spending: 6%

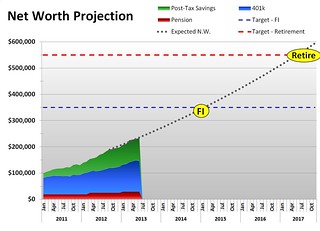

------------ CHARTS --------------

640 days to FI (400 work days)

1200 days to retire (760 work days)

MARCH 2013

------------------------------------

SPENDING: $1,282

Home – $679

Food – Groceries - $188

Food – non grocery - $72

Entertainment: $315

Transportation - $25

Non-standard spending:

Home expense includes $115 for safety razor gear (razor, brush, stand, bowl, soap, blades). Haven’t gotten it yet. Hope I like it.

Entertainment includes $240 of fountain pen stuff. This was 4 pens (one of which was stolen after USPS left it), ink samples, and paper. I use a nice leather journal/book for keeping action item lists and various notes. I’m enjoying the pens so far and it is fun experimenting with ink/pen combinations.

I’ve been trying to acquire some more BIFL stuff. This month, the safety razor and pens won’t be saving me much or any money but I think I will enjoy using them more. These are two examples of shifting back to products of older design/technology – back when things were meant to be used for many years rather than discarded quickly.

I tried to find a high quality lunch box (mine is wearing out and failing in 4 places). I couldn’t find much though. The best options I found were this Stanley and this aluminum one but I didn’t think either one looked good enough (the Stanley handle/latch looks flimsy, and I wish the metal one had some insulation… Maybe I should just use a small cooler). Bought a $15 piece of crap from Target instead.

------------ TOTALS YTD --------------

Got my yearly bonus so I like looking at the YTD total numbers.

Income: $22k

Spent: $3k

Saved: $19k

Savings Rate: 87%

Investment increase: $4k (2% YTD)

Net Worth: $225k

Net worth increase YTD: $28k

Net worth in years: 16.4

3.5% SWR: $650/month

SWR Needed @ current spending: 6%

------------ CHARTS --------------

640 days to FI (400 work days)

1200 days to retire (760 work days)

-

frugaladventurer

- Posts: 118

- Joined: Sat Sep 15, 2012 11:05 pm

So I have my taxes finished. I added them all up (with some like sales tax estimated)

$25k for 2012. It feels like a lot of money. The nice thing is that since they are tied so heavily to income, my taxes will go down a lot in the future.

So far in my life I've paid over $200,000 of taxes. Probably more like $250-300k. That seems a like a lifetime's worth to me.

$25k for 2012. It feels like a lot of money. The nice thing is that since they are tied so heavily to income, my taxes will go down a lot in the future.

So far in my life I've paid over $200,000 of taxes. Probably more like $250-300k. That seems a like a lifetime's worth to me.

That's a really nice breakdown of your taxes. I personally can't wait until I enter FI and taxes move into a simpler and lower tax situation.

I heard today on American Public Media a suggestion made by that awesome psychologist from Duke, Dan Ariely, that it would be interesting if we were able to have a say on where a small fraction (say 5%) of our taxes go. I think I would choose education or research.

Btw, I'm starting to read about your power cooking methods. I'm taking some serious notes, thank you for sharing that.

I heard today on American Public Media a suggestion made by that awesome psychologist from Duke, Dan Ariely, that it would be interesting if we were able to have a say on where a small fraction (say 5%) of our taxes go. I think I would choose education or research.

Btw, I'm starting to read about your power cooking methods. I'm taking some serious notes, thank you for sharing that.

------------------------------------

APRIL 2013

------------------------------------

SPENDING: $1,009

Home: $544

Food – Groceries: $122

Food – non grocery: $9

Entertainment: $642

Transportation: $61

Sold stuff: $-360

--------------------------------

It seems like I’m starting to meter my spending up to $1,000 per month. This month my base spending (Home & food) was $670. My Hobby/entertainment spending was $640. I did sell $360 of stuff so the net Entertainment spending was $280

As you can see I've settled in around $1,000 per month. My base expenses have been steady or slowly decreasing, with my entertainment spending going up. Most of my entertainment spending is buying things that I think I’ll be using for many years, so I'm not blowing the money completely (I might make a separate post about BIFL things.)

The problem I have with this is that I’m not challenging myself to reduce my spending further. With many of these BIFL type purchases, I’m being impatient and not acquiring them as cheaply as I could.

I think some of this is actually due to my close monitoring of progress towards FI. I set up a projected plan (FI By End of 2014) and after that I’ve felt like (when it comes to finance) I’m just passing time until then. That’s made me less likely to push further. I have been successful so far lowering my food spending though. I think I just need to stop spending the difference on shiny new things bought new from retail businesses.

--------------------------------

I lost $1,700 on my investment prices in April because of the gold drop. (I use a Permanent Portfolio). For the year I’m still up $3,000. Still on track with the plan I made last summer - but just barely (I'm likely to get behind unless investment returns pick up.)

--------------------------------

A recent work trip and discussions with co-workers has increased my feelings of fitting in less and less with what is now considered normal.

-- Heard multiple people explain why they have TWO separate smart phones (one brand new smart phone paid for by work, and one brand new smart phone that they pay for)

-- Explanations for owning X number of cars (one just for transporting a DOG!)

-- How great of an idea it is to spend $20,000 at work on “jumbotron” TVs to display things at that actually work better to use paper for.

-- $100 for a light lunch for 5 people. $200 for dinner for 5.

-- Got a reminder of how much I dislike flying and hotels. Rental cars. Lines. $12 a day for parking. Violations of privacy and dignity for "safety". Cramming into a small, stuffy airplane (it is nice to see things from up above though)

It is getting more fun to hear jokes like “oh God, we’re still going to be working on this when we retire!”... I get to have a nice little laugh to myself when I’m certain it is true for me.

APRIL 2013

------------------------------------

SPENDING: $1,009

Home: $544

Food – Groceries: $122

Food – non grocery: $9

Entertainment: $642

Transportation: $61

Sold stuff: $-360

--------------------------------

It seems like I’m starting to meter my spending up to $1,000 per month. This month my base spending (Home & food) was $670. My Hobby/entertainment spending was $640. I did sell $360 of stuff so the net Entertainment spending was $280

As you can see I've settled in around $1,000 per month. My base expenses have been steady or slowly decreasing, with my entertainment spending going up. Most of my entertainment spending is buying things that I think I’ll be using for many years, so I'm not blowing the money completely (I might make a separate post about BIFL things.)

The problem I have with this is that I’m not challenging myself to reduce my spending further. With many of these BIFL type purchases, I’m being impatient and not acquiring them as cheaply as I could.

I think some of this is actually due to my close monitoring of progress towards FI. I set up a projected plan (FI By End of 2014) and after that I’ve felt like (when it comes to finance) I’m just passing time until then. That’s made me less likely to push further. I have been successful so far lowering my food spending though. I think I just need to stop spending the difference on shiny new things bought new from retail businesses.

--------------------------------

I lost $1,700 on my investment prices in April because of the gold drop. (I use a Permanent Portfolio). For the year I’m still up $3,000. Still on track with the plan I made last summer - but just barely (I'm likely to get behind unless investment returns pick up.)

--------------------------------

A recent work trip and discussions with co-workers has increased my feelings of fitting in less and less with what is now considered normal.

-- Heard multiple people explain why they have TWO separate smart phones (one brand new smart phone paid for by work, and one brand new smart phone that they pay for)

-- Explanations for owning X number of cars (one just for transporting a DOG!)

-- How great of an idea it is to spend $20,000 at work on “jumbotron” TVs to display things at that actually work better to use paper for.

-- $100 for a light lunch for 5 people. $200 for dinner for 5.

-- Got a reminder of how much I dislike flying and hotels. Rental cars. Lines. $12 a day for parking. Violations of privacy and dignity for "safety". Cramming into a small, stuffy airplane (it is nice to see things from up above though)

It is getting more fun to hear jokes like “oh God, we’re still going to be working on this when we retire!”... I get to have a nice little laugh to myself when I’m certain it is true for me.

-

jennypenny

- Posts: 6858

- Joined: Sun Jul 03, 2011 2:20 pm

"A recent work trip and discussions with co-workers has increased my feelings of fitting in less and less with what is now considered normal."

That's hard, and the urge (instinct?) to fit in can be strong. Learn some coping skills now while you have people to practice on . I don't think it gets any easier when you're not working. I haven't worked fulltime in over a year. For me, it's actually a little harder to fit in because a common bond (working) is gone now.

. I don't think it gets any easier when you're not working. I haven't worked fulltime in over a year. For me, it's actually a little harder to fit in because a common bond (working) is gone now.

That's hard, and the urge (instinct?) to fit in can be strong. Learn some coping skills now while you have people to practice on

Jenny - I often prefer to be a bit of an outsider/loner. I usually don't see it as a problem that I have feelings of not fitting in. My urge to fit has never been as high as most people's, and it has decreased quite a lot the last couple years. In most cases when I see these big differences between myself and the sad "normal" I see it as a good sign for myself (I'm noticing the craziness of "normal")

You have a good point about relationships/friendships. I do worry a bit that I'm not making enough new friends (or any at all for long stretches). Work does provide some pretty good relationships - and I'll have to try much harder to make new friends and build social capital when I don't have the work relationships any more. I can still enjoy myself with people. There are a number at work that I have very interesting conversations with and who I might be good friends with outside of work - people who might still spend like normal but who are creative and like to talk about things outside of common small talk. I do believe that the pool of potential friends for me (as a % of all people) has gotten smaller though, and as I've gotten older the exposure to new people has decreased.

You have a good point about relationships/friendships. I do worry a bit that I'm not making enough new friends (or any at all for long stretches). Work does provide some pretty good relationships - and I'll have to try much harder to make new friends and build social capital when I don't have the work relationships any more. I can still enjoy myself with people. There are a number at work that I have very interesting conversations with and who I might be good friends with outside of work - people who might still spend like normal but who are creative and like to talk about things outside of common small talk. I do believe that the pool of potential friends for me (as a % of all people) has gotten smaller though, and as I've gotten older the exposure to new people has decreased.

Have a few things to share, but I want to try to cover it without rambling much.

----------------------------------

I want to challenge myself more.

----------------------------------

I’m happy with thing in my life. Happy (enough) with where. Happy with how I spend my free time. Happy with my spending. Happy enough with work right now. Outside of work my stress level is super low. Nearly zero. I have no crises or dilemmas.

But.. I think I feel a little bit stagnant right now. I feel like I need to challenge myself more and make more improvements such as spending reduction, more side income, better investing, quicker growth in useful skills, more friendships, etc..

My spending is starting to bother me a little. It's pretty low but I am not challenging or driving myself. The last few months my base spending has been good (I’ve reduced my food spending), but I have been in the habit of spending on my hobbies right up to around $1,000 total for the month. I’m not completely sure why I’m doing this. I think I’m satisfied with being around $1,000 per month. That’s been a goal for me and for quite a while it was what I looked at to represent having my spending low. Once I got there I haven’t had much desire to go lower. When I think about it, I feel I can go lower without having any negative effect on my life. In fact, sometimes I feel like going lower will be more fun (more interesting, more challenging, more opportunities for ingenuity)

** Here’s one way I’m thinking about challenging myself: I want to transition my hobby/entertainment spending to come only from income from hobbies. My current hobby income is from shirt designs. I also sell stuff here and there but I think that will taper down. I’m going to make a hobby cash jar. I’ll put money that I make from hobbies into it. And take money out for spending on hobbies or entertainment. To start, I will fund the jar with money from my normal income, and I will ramp that amount down over time. Something like this:

June - $200

July - $175

August - $150

…etc.. down to $100 per month. (or zero if I ramp up my hobby income enough) I’m expecting that during this time I will ramp up my shirt income a bit. I feel like this is a gimmick, but maybe it will make my spending reduction a bit more interesting or challenging.

----------------------------------

PROMOTION AT WORK?

----------------------------------

They’re offering me a promotion at work. I’m not sure if I want to take it. I’m leaning towards it. In my current role I work in a location with a few hundred people. My job is mostly coaching and training and setting up systems – working regularly with about 40 people here. Guy at the company headquarters wants me to work for him, and do pretty similar coaching and training as I do now, but for all/some of the different locations. It’d come with an 11% raise and around $10k lump sum for relo (in addition to expenses).

The job would include a LOT of travel. 50-75% of weekdays. This is one of the big things I need to consider. This would reduce my food and travel spending significantly (free food while traveling, and free personal flights from all the miles I’d be racking up)

PROs:

- More money

- Slight reduction in spending due to frequent traveling.

- Possibly more power at work. Much wider influence. I think this would come without an increase in accountability/stress. I might have LESS accountability than right now. I think I’d have less freedom to choose what I do day-to-day though. Some of the times I enjoy most at work currently are with some strategic planning and management stuff - and this promotion would give me a chance to influence a much wider audience on these things. Also, as I hit FI and get close to retirement, this is a position that could be fun to take big changes on driving HUGE changes (without worrying much about consequences when I’m close to retiring)

- Good time to buy a house in the new city. Opportunity to learn renovation skills. Could work out very well if buy a cheap house, fix it up a bit, and get a roommate.

- Warmer climate. I would definitely like the weather.

- Many more opportunities to meet potential girlfriends and friends. I actually have more friends in the new city than I do where I live now. (old friend I used to live nearby in another city 5 years ago who I keep in touch with)

- I’ve been in my current role for 5 years and a change might be nice.

CONS:

- My duties would shift to working more with other people. Sometimes this will be big groups and as an Introvert this can wear on me. Another guy I work with closely who’s been doing a similar job for years is also an introvert, so I’m going to talk to him about it.

- I could get tired of the travel. Currently traveling for work feels like a burden. I don’t like the travelling part much on its own, but I think the main reason I dislike it is because when I travel I’m away from my normal job. If I take this new job, my job is done while traveling so I won’t feel like I’m falling behind. It’s just a question of whether I want to bother with the airports, hotels, and restaurants.

- Can be more politics at headquarters.

- I have a pretty good setup here (nice cheap apartment a couple blocks from work.. cozy town.. very good roads for bicycling) and some of this (cycling roads for sure) would change.

With my last promotion I was 100% sure it's what I wanted. This time I'm not nearly as certain. This is a job that I've always expected I'd do at some point though. I told the guy I’d think about it for a week and a half.

-----------------------------

Still rockin’ and rollin’ on the FI glide path.

This weekend I leave for a backpacking adventure! Five days out in the woods. YAY!

----------------------------------

I want to challenge myself more.

----------------------------------

I’m happy with thing in my life. Happy (enough) with where. Happy with how I spend my free time. Happy with my spending. Happy enough with work right now. Outside of work my stress level is super low. Nearly zero. I have no crises or dilemmas.

But.. I think I feel a little bit stagnant right now. I feel like I need to challenge myself more and make more improvements such as spending reduction, more side income, better investing, quicker growth in useful skills, more friendships, etc..

My spending is starting to bother me a little. It's pretty low but I am not challenging or driving myself. The last few months my base spending has been good (I’ve reduced my food spending), but I have been in the habit of spending on my hobbies right up to around $1,000 total for the month. I’m not completely sure why I’m doing this. I think I’m satisfied with being around $1,000 per month. That’s been a goal for me and for quite a while it was what I looked at to represent having my spending low. Once I got there I haven’t had much desire to go lower. When I think about it, I feel I can go lower without having any negative effect on my life. In fact, sometimes I feel like going lower will be more fun (more interesting, more challenging, more opportunities for ingenuity)

** Here’s one way I’m thinking about challenging myself: I want to transition my hobby/entertainment spending to come only from income from hobbies. My current hobby income is from shirt designs. I also sell stuff here and there but I think that will taper down. I’m going to make a hobby cash jar. I’ll put money that I make from hobbies into it. And take money out for spending on hobbies or entertainment. To start, I will fund the jar with money from my normal income, and I will ramp that amount down over time. Something like this:

June - $200

July - $175

August - $150

…etc.. down to $100 per month. (or zero if I ramp up my hobby income enough) I’m expecting that during this time I will ramp up my shirt income a bit. I feel like this is a gimmick, but maybe it will make my spending reduction a bit more interesting or challenging.

----------------------------------

PROMOTION AT WORK?

----------------------------------

They’re offering me a promotion at work. I’m not sure if I want to take it. I’m leaning towards it. In my current role I work in a location with a few hundred people. My job is mostly coaching and training and setting up systems – working regularly with about 40 people here. Guy at the company headquarters wants me to work for him, and do pretty similar coaching and training as I do now, but for all/some of the different locations. It’d come with an 11% raise and around $10k lump sum for relo (in addition to expenses).

The job would include a LOT of travel. 50-75% of weekdays. This is one of the big things I need to consider. This would reduce my food and travel spending significantly (free food while traveling, and free personal flights from all the miles I’d be racking up)

PROs:

- More money

- Slight reduction in spending due to frequent traveling.

- Possibly more power at work. Much wider influence. I think this would come without an increase in accountability/stress. I might have LESS accountability than right now. I think I’d have less freedom to choose what I do day-to-day though. Some of the times I enjoy most at work currently are with some strategic planning and management stuff - and this promotion would give me a chance to influence a much wider audience on these things. Also, as I hit FI and get close to retirement, this is a position that could be fun to take big changes on driving HUGE changes (without worrying much about consequences when I’m close to retiring)

- Good time to buy a house in the new city. Opportunity to learn renovation skills. Could work out very well if buy a cheap house, fix it up a bit, and get a roommate.

- Warmer climate. I would definitely like the weather.

- Many more opportunities to meet potential girlfriends and friends. I actually have more friends in the new city than I do where I live now. (old friend I used to live nearby in another city 5 years ago who I keep in touch with)

- I’ve been in my current role for 5 years and a change might be nice.

CONS:

- My duties would shift to working more with other people. Sometimes this will be big groups and as an Introvert this can wear on me. Another guy I work with closely who’s been doing a similar job for years is also an introvert, so I’m going to talk to him about it.

- I could get tired of the travel. Currently traveling for work feels like a burden. I don’t like the travelling part much on its own, but I think the main reason I dislike it is because when I travel I’m away from my normal job. If I take this new job, my job is done while traveling so I won’t feel like I’m falling behind. It’s just a question of whether I want to bother with the airports, hotels, and restaurants.

- Can be more politics at headquarters.

- I have a pretty good setup here (nice cheap apartment a couple blocks from work.. cozy town.. very good roads for bicycling) and some of this (cycling roads for sure) would change.

With my last promotion I was 100% sure it's what I wanted. This time I'm not nearly as certain. This is a job that I've always expected I'd do at some point though. I told the guy I’d think about it for a week and a half.

-----------------------------

Still rockin’ and rollin’ on the FI glide path.

This weekend I leave for a backpacking adventure! Five days out in the woods. YAY!

Taking the new job could be a way to challenge yourself. You'd have to relocate, get comfortable in the new location, adjust to the new role at work.

To me it sounds like you're leaning in the direction of accepting and it also sounds like the right thing to do. A work challenge shouldn't replace challenges in your personal life, but it could provide some you wouldn't otherwise face.

Would your overall rate of progress towards FI increase? You'd be making more and save some money on food, but also living in a more expensive location.

To me it sounds like you're leaning in the direction of accepting and it also sounds like the right thing to do. A work challenge shouldn't replace challenges in your personal life, but it could provide some you wouldn't otherwise face.

Would your overall rate of progress towards FI increase? You'd be making more and save some money on food, but also living in a more expensive location.

Yeah, I'm leaning towards accepting.

I do think, challenge wise, that this would offer me good timing to buy a house - likely one that could use some remodeling, setting up a big garden - some nice ways to challenge myself.

I'm sure the extra money would offset any increase in spending. If it goes well buying a house, my spending could go lower than it is right now. This would speed up my FI progress, but not drastically.

I do think, challenge wise, that this would offer me good timing to buy a house - likely one that could use some remodeling, setting up a big garden - some nice ways to challenge myself.

I'm sure the extra money would offset any increase in spending. If it goes well buying a house, my spending could go lower than it is right now. This would speed up my FI progress, but not drastically.

I accepted the promotion. I'll be moving to St Louis this summer.

Started looking for homes. I have up to $80k cash to use, and I'm open to different options:

1 - Fixer upper. $30-$70k

2 - Ok. Not brand new or trendy but will work just fine: $50-$100k

3 - Very nice for my standards. $90-$130k

St. Louis is a little a bit tricky and interesting. There are a lot of bad areas. There are some historic and interesting areas (an Irish neighborhood, an Italian, historic and/or trendy spots)

There are also pockets of good and bad neighborhoods. I've taken my bike during visits to town and when I ride through some places it's really nice, but then 2 blocks away, or just across one main st, it's very different. There are 80 small neighborhoods in the official St Louis city area. I looked at data of crime and of race demographics (race was the easiest to find data on), and looked around on google street view at areas I was considering.

The neighborhoods close to work are too dangerous for me (there are a couple nice trendy/historic areas but they are a little more expensive, and they're very close to some really rough spots.) So I've narrowed my current search down to some modest (and I believe safe) neighborhoods that are 4-8 miles from work.

Does anyone on here live in St Louis? I'd love to get more input on what these neighborhoods are like. I do have some friends there and co-workers living there now that I can talk to but it's always good to hear from more - especially from people with similar financial concerns.

Started looking for homes. I have up to $80k cash to use, and I'm open to different options:

1 - Fixer upper. $30-$70k

2 - Ok. Not brand new or trendy but will work just fine: $50-$100k

3 - Very nice for my standards. $90-$130k

St. Louis is a little a bit tricky and interesting. There are a lot of bad areas. There are some historic and interesting areas (an Irish neighborhood, an Italian, historic and/or trendy spots)

There are also pockets of good and bad neighborhoods. I've taken my bike during visits to town and when I ride through some places it's really nice, but then 2 blocks away, or just across one main st, it's very different. There are 80 small neighborhoods in the official St Louis city area. I looked at data of crime and of race demographics (race was the easiest to find data on), and looked around on google street view at areas I was considering.

The neighborhoods close to work are too dangerous for me (there are a couple nice trendy/historic areas but they are a little more expensive, and they're very close to some really rough spots.) So I've narrowed my current search down to some modest (and I believe safe) neighborhoods that are 4-8 miles from work.

Does anyone on here live in St Louis? I'd love to get more input on what these neighborhoods are like. I do have some friends there and co-workers living there now that I can talk to but it's always good to hear from more - especially from people with similar financial concerns.

Congrats C40 with your decision to move. From what I see in Wikipedia, St. Louis is a interesting big city, perhaps it gives you also a reason to study French, if you not already are comfortable with that language.

I will read your journal now with extra interest. For me your journal is the most well kept and presented one in the forum. Wish you all the best.

I will read your journal now with extra interest. For me your journal is the most well kept and presented one in the forum. Wish you all the best.

-

My_Brain_Gets_Itchy

- Posts: 267

- Joined: Fri Mar 02, 2012 5:29 pm

Re: C40's Journal

------------------------------------

JUNE 2013

------------------------------------

SPENDING: $1,461

- Home: $550

- Home – relocation: $520

- Food – Groceries: $141

- Food – non grocery: $10

- Entertainment: $233

- Transportation: $22

YTD Savings rate: 84%

Days of work left to reach basic FI: ~340

----------------------------------------------------------------

SPENDING DETAILS

The relocation was a home hunting trip to St Louis. I was going to try couchsurfing but my mom and stepdad came up so I got a hotel to make sure we had enough space. The $520 also includes gas and food.

Entertainment – I started a hobby cash Jar. In June I started it off with $200, plus I added $69 from shirt sales and $16 from selling something. I spent $105 from the jar on Pen stuff, backpacking stuff, and a music CD.

----------------------------------------------------------------

RELOCATION

I looked at a lot of houses in 3 days and found 4 that I liked. 1 in particular as it met my list of desires (good space for garden, wood floors, small, safe area, and as a bonus it is near a metrolink train station). Have an offer accepted now so I’m working on inspection and mortgage stuff (going to put 50% down.. don’t have enough cash to buy this one outright). The majority of the houses that I could get for cash had serious issues. Most common was horrible floorplans (many Shotgun houses in STL), or serious flaws that make them not worth fixing (big structural issues, horrible neighborhood, etc.)

----------------------------------------------------------------

CAPITAL

http://farm8.staticflickr.com/7343/9222 ... e611_o.jpg

I’m still on track with my capital building plan, but I received my yearly bonus in March, and got a $5k relocation lump sum in June (another one will come in July). My PP performance has been poor. I sold all my gold and bonds (the gold at a loss) to free up money for the house, so now all I have is cash and stocks. I’m going to learn more about dividend investing and I might shift my investing strategy to include a significant amount of dividend-paying stocks.

I do believe in the Permanent Portfolio principles, but I do feel like there’s a significant amount of speculation within the strategy (that it will work ok, basically – and I’m sure I wouldn’t feel that way if it had been working better). With dividend stocks or something like landlording (or MAYBE REITS), I feel more like the returns are coming from utilization of the money. Returns/growth from non-dividend stocks or from the PP feel more like they come from macro-economic factors and news/propaganda/sheep behavior. It still feels like playing a game.

I’m not highly confident that I won’t feel the same or similar things about dividend stocks after I investigate and start using them. It will of course still feel like a game (actually, much more so when I’m having to pick stocks) but I think I would like the idea of my capital producing returns, rather than the speculation/fear stuff that so directly impacts the PP allocations. Enough rambling – I’m sure with the house stuff coming up, it will be a while before I make big changes.

JUNE 2013

------------------------------------

SPENDING: $1,461

- Home: $550

- Home – relocation: $520

- Food – Groceries: $141

- Food – non grocery: $10

- Entertainment: $233

- Transportation: $22

YTD Savings rate: 84%

Days of work left to reach basic FI: ~340

----------------------------------------------------------------

SPENDING DETAILS

The relocation was a home hunting trip to St Louis. I was going to try couchsurfing but my mom and stepdad came up so I got a hotel to make sure we had enough space. The $520 also includes gas and food.

Entertainment – I started a hobby cash Jar. In June I started it off with $200, plus I added $69 from shirt sales and $16 from selling something. I spent $105 from the jar on Pen stuff, backpacking stuff, and a music CD.

----------------------------------------------------------------

RELOCATION

I looked at a lot of houses in 3 days and found 4 that I liked. 1 in particular as it met my list of desires (good space for garden, wood floors, small, safe area, and as a bonus it is near a metrolink train station). Have an offer accepted now so I’m working on inspection and mortgage stuff (going to put 50% down.. don’t have enough cash to buy this one outright). The majority of the houses that I could get for cash had serious issues. Most common was horrible floorplans (many Shotgun houses in STL), or serious flaws that make them not worth fixing (big structural issues, horrible neighborhood, etc.)

----------------------------------------------------------------

CAPITAL

http://farm8.staticflickr.com/7343/9222 ... e611_o.jpg

{kind=link}

I’m still on track with my capital building plan, but I received my yearly bonus in March, and got a $5k relocation lump sum in June (another one will come in July). My PP performance has been poor. I sold all my gold and bonds (the gold at a loss) to free up money for the house, so now all I have is cash and stocks. I’m going to learn more about dividend investing and I might shift my investing strategy to include a significant amount of dividend-paying stocks.

I do believe in the Permanent Portfolio principles, but I do feel like there’s a significant amount of speculation within the strategy (that it will work ok, basically – and I’m sure I wouldn’t feel that way if it had been working better). With dividend stocks or something like landlording (or MAYBE REITS), I feel more like the returns are coming from utilization of the money. Returns/growth from non-dividend stocks or from the PP feel more like they come from macro-economic factors and news/propaganda/sheep behavior. It still feels like playing a game.

I’m not highly confident that I won’t feel the same or similar things about dividend stocks after I investigate and start using them. It will of course still feel like a game (actually, much more so when I’m having to pick stocks) but I think I would like the idea of my capital producing returns, rather than the speculation/fear stuff that so directly impacts the PP allocations. Enough rambling – I’m sure with the house stuff coming up, it will be a while before I make big changes.

Re: C40's Journal

I love the charts, it looks like you are on track to retire early with that trend line.

It is interesting that you see the PP as a game but dividends and REIT's as more businesslike. Would you feel comfortable watching your dividend portfolio drop 50% in a short period , even if you knew the business was sound and that the dividends would continue to flow and grow in the foreseeable future? The thing about the PP is that even though it is down this year , I don't think it is nearly as variable as something like a dividend growth portfolio. Even if gold gets cut in half or to a third of where it is now there is still three other equal sized components in the portfolio so it won't impact you too harshly.

It is interesting that you see the PP as a game but dividends and REIT's as more businesslike. Would you feel comfortable watching your dividend portfolio drop 50% in a short period , even if you knew the business was sound and that the dividends would continue to flow and grow in the foreseeable future? The thing about the PP is that even though it is down this year , I don't think it is nearly as variable as something like a dividend growth portfolio. Even if gold gets cut in half or to a third of where it is now there is still three other equal sized components in the portfolio so it won't impact you too harshly.

Re: C40's Journal

Bluenote -- on the PP / investing.. I think it's mainly that the PP depends more directly on public OPINION, and dividend payment depend more-so on actual business/behaviors. I'm sure I wouldn't be happy if I had dividend stocks and the price of the stocks dropped a lot. I might be comforted some if the dividends are still coming and not getting cut though.

At this point I haven't made any decision - just that I want to learn about dividend investing. Maybe once I learn more, I won't feel any better about them than the PP.

At this point I haven't made any decision - just that I want to learn about dividend investing. Maybe once I learn more, I won't feel any better about them than the PP.

Re: C40's Journal

House buying -- it's getting stressful...

- Found a nice house at a list price that I think is fair.

- Seller wouldn't come down on price.. appears to be completely broke (previous foreclosure & bankruptcy)

- Inspection didn't go too bad.. Mostly just stuff I expected or already saw.

- Appraisal was WAY lower than my offer... (19% lower than original offer... 16% lower than what I'm trying to get with inspection concessions).. It won't mess up my loan at all as I was already putting way more down than the difference.

So I'm nervous about the appraisal and if I might be overpaying. I looked pretty close at comps before making the offer and I thought it was an ok price. After getting the appraisal, I looked in detail at the appraisal method used and his adjustments.. I think he made some bad decisions. When I make adjustments that I think are right, I come out much closer...

- Found a nice house at a list price that I think is fair.

- Seller wouldn't come down on price.. appears to be completely broke (previous foreclosure & bankruptcy)

- Inspection didn't go too bad.. Mostly just stuff I expected or already saw.

- Appraisal was WAY lower than my offer... (19% lower than original offer... 16% lower than what I'm trying to get with inspection concessions).. It won't mess up my loan at all as I was already putting way more down than the difference.

So I'm nervous about the appraisal and if I might be overpaying. I looked pretty close at comps before making the offer and I thought it was an ok price. After getting the appraisal, I looked in detail at the appraisal method used and his adjustments.. I think he made some bad decisions. When I make adjustments that I think are right, I come out much closer...