This thread is for calculating and sharing your Income Robustness Score, or "IR-Score". See below from @jacob for calculating it, from this thread.

Take each source of income, divide it by spending, and if it's >1, make it 1. Add those up. Here's a function for calculating one income source: =IF(ABS(C9/$AA9)>1,1,ABS(C9/$AA9)). c9 is income, aa9 is spending.

Income from w*rk counts.

See discussion in the thread for when it's appropriate to count difference investments as more than one source of income. Footnote your scores if you like.

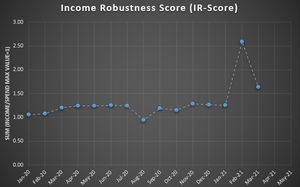

In 2020 my IR-Score was 1.19. (w*rk, stash)

2021 ytd is 1.83, but that's deceptive because I have a whole year in an independent income stream's AR, I just haven't recognized it yet. So I'm actually more like 2.83 ytd.

I'm tracking my IR-score monthly, but I'll post that stuff in my journal and just post yearly updates or milestones here.

Okay, here's a parsimonious suggestion that should be both easy to calculate, hard to game, and more useful than SWR.

To compute, take each independent source(*) of dollar income and divide it by total expenses. If the number is >1, reduce to 1. Add them together.

In my case, my sources are

1) Portfolio * 0.03 (you can pick whatever here as long as it's consistent) / spending > 1

2) ERE book sales / spending > 1.

3) Blog ads / spending ~ 0.75

4) Misc sales of old books, etc. on amazon / spending ~ 0.1

Resulting in an indicator value of 1+1+0.75+0.1 = 2.85

This indicator rewards diversification over concentration because attempts to "go over 1" are not rewarded. By only measuring the demonstrated ability to generate dollar income, it also avoids potential gaming and endless debates/self-delusion about the imputed value of cooking your own dinner as well as the "well if I really would, I bet I could sell my services for $X", etc. Thus the indicator also encourages demonstrated and ongoing ability to produce market value relative to one's [market] expenses.

(*) Obviously a source of debate. For example, should a RE portfolio of two houses be counted as one source or two sources? Similarly, if you split your portfolio, do you get to count it as several independent sources. I'd say that's a discretionary choice. In the spirit of trying to become what we measure, I'd suggest not doing that.

What would be the optimal score? I don't think more is always better, i.e. although '2' is almost always better than '1', a '6' might not be better than, say '3'? Example: someone in their 60's with score of '6' made of something like: 1) state pension 2) company pension 3) stocks portfolio 4) rentals 5) part-time job/consulting 6) some royalties - this person surely overaccumulated and basically wasted years of life working too much? Yes, they are very secure but at what cost? So, is the optimal score somewhere around 2-3 before diminishing returns kick in?

Since I'm working, I'm going to include my job in my Income Robustness Score, to show how generalized it is:

Salarymanning - 1.0

Investments - 0.27

IR-score: 1.27

The goal being to set salarymanning to 0.0 without going below 1.0.

But I have another goal of doing the above also without dropping below 2 sources of income in the chart. Another possibility is something like a modification of the h-index in scientific publishing whereby your IR-score would be

N * I

where N is the number of income sources that produce at least fraction I.

Mine would be 2*0.27 = 0.54. So with this set of value judgements, I have a problem right now, whereas in the first one I don't provided I don't consider my job a problem.

I'll take a stab at this: IR-Score is merely a component of one's overall web-of-goals, and "ideal" can only be evaluated outside of each individual's context. For example, maybe a 2 is optimal for Axel's wog right now. But let's say I become injured, and that "2" was good for me because I know that if I really needed to, I could dig ditches. Now that that fallback is no longer available to me, I'm not comfortable with an IR-Score of 2, and work to bump it up.

It might also be interesting to indicate a level of passivity. Right now I'm IR-Score 1.83, 1.1active, .73passive.

IR: 1 + 0.63 + 0.41 = 2.04. 1 active, 1.04 passive(ish) (<2 hours of work a week). If my active source went away the passive numbers would be higher because of tax stuff. H-IR (@nomadscientist idea) would be 3*0.41= 1.23

I'll take a stab at the family version, as DW and I don't split up our spending (and the kids are solidly in the expense category, at least until DD's candy bar and DS's ice cream businesses turn profitable), and we don't split up our incomes or our retirement accounts and other investing accounts. Both our salaryman incomes could separately cover our family's expenses, so I think that puts us at an IR2* of 2, and as we're not FI yet (and certainly not FI at a 3% WR), our pooled investments/pooled expenses would be a .45. So, IR2 (or whatever) of 2.45?

So, if I lose my job we're OK; and if DW loses hers ditto; but if we both lose our jobs then we better figure out a way to live on 45% of our current spending; which, honestly, would be totally doable as we wouldn't need to live in our HCOL area. We'd rent out our home, pull our kids out of their school, and live in the camper. That alone would cut out more than 55% of our current spending. Also, renting out the house would add another source of income, likely about $1,000 net of mortgage/taxes/insurance/HOA, which would cover a decent chunk of our living-on-the-road monthly spending.

Hmm, the wheels are starting to turn . . . . Perhaps we're more robust than I thought.

IR2 (or 4?), very roughly for family of 4:

20 hr/week work (me) ~ 1

32 hr/week work (de) ~ 1

Rentals ~ 1.4

Interest (mortgages backed loans) ~ 0.35

Other portfolio @3% ~ 0.08

Total ~ 3.83

Expect to drop to 2.82 when dw quits work this summer. Might be replaced partly with irregular income from "something" longer term, but I don't count on it (as long it is not really needed). Portfolio or lending might go a bit up in the future.

IR1(2020) - about 1.9

IR1(2021) - 2.0 (projected)

IR1(2022:2035) - from 2.0 down to 1.7 (projected)

IR1(2036 onward) from 2.7 down to 2.4 or so (projected)

Annuity will start at 1.0 and decline (non-COLA)

Stash will likely stay at 1.0

SS pushes total above 2 somewhere down the road.

I got to thinking that the calculation is closer to what my inner engineer would call redundancy, which is a contributor to robustness, but not the whole story. I spent about two hours last night on a micro-manifesto trying to fit my "iDave Phase III Resource Management System" into the sort of system engineering framework I might encounter at work. It wound up on the cutting room floor because long and too far off topic, but it served as a good reminder that haven't put together adequate definitions to really assess where I stand. Once I get relocated and settled that will be one of my initial contemplative pursuits. Might seem backward to do it after pulling the plug, but work doesn't do much beside add additional excess capacity which I'm confident I don't need. So the anticipated cost of pulling the plug first then addressing breadth is acceptably low.

iDave - would you be willing to post here or in another thread what factors you would look at from a system engineering framework? The redundancy aspect of this model jumps out but I do not have the words/knowledge to know what it should look like though.

Something more useful may be in how well/quickly someone can source new income source if one of theirs were to go poof. That's probably not really quantifiable though.

Something more useful may be in how well/quickly someone can source new income source if one of theirs were to go poof. That's probably not really quantifiable though.

It's kind of like quantifying how long you would have to date in order to get a new boyfriend. You have to do it often enough that you garner statistical data. So, easier to quantify for people likely to be overheard uttering truisms such as "Men are like buses. You miss one, just wait 15 minutes for another to come along."

Also, old rule of thumb for job seekers was something like 1 month for every $10,000 you need/want to make, if and only if you ever previously earned that much. The internet has greatly decreased this interval for employment as well as dating and $10,000 needs to be updated for inflation.

If I wanted either a full-time monogamous BF or full-time employment by other, I am pretty confident that I could get 64, Alec Baldwin build, IQ 120 and some sort of math/teaching related job paying over $30,000 within about 6 weeks. So, maybe people could include what they reasonably believe they could do within a month or two in their number if it doesn't produce time/place/? availability conflict with other sources they are already including in their number? Obviously, pretty much everybody on this forum has enough stash that emergency/transition funds to cover much longer job search inclusive of training (spiffing up your looks/moves resume) and/or investment in own business/endeavor (marriage? my analogy is breaking down...) would be available, so this would be highly conservative estimate.

ETA:

Oops, my IR is in transition due to Covid and slow-mo household break-up, but if collecting SS and unemployment are considered viable long term or temporary place holder options, I’m at 2 heading towards 3. If my “household” wasn’t in break up mode, it would also be at 2, but only because he could cover me twice. No way in heck I could even cover his child support payments.

iDave - would you be willing to post here or in another thread what factors you would look at from a system engineering framework? The redundancy aspect of this model jumps out but I do not have the words/knowledge to know what it should look like though.

Sure, but it will probably be sometime over the weekend--I deleted what I started and to keep it succinct will take more thought than I usually put into forum blathering.

Something more useful may be in how well/quickly someone can source new income source if one of theirs were to go poof. That's probably not really quantifiable though.

I've told the story in years past, but my journey to ER started when facing the spectre of being a downsizing victim during a time when people in my cohort (midlife mid-level corporate workers) were commonly facing long periods of un- or underemployment (c. 2011). I framed the income gap problem as: assuming I get laid off, how soon to I have to find a new job before I lose my house?" (or how long of a work income disruption would I weather before I lost the house). Even then I didn't think it was a great metric but it was a bone to chew. Outlining some behavioral modifications and playing around with it parametrically (what if I don't get laid off for a month, 6 months, a year?) allowed me to say that if I could hang on to employment for X time I could bridge to retirement. The situation at work improved soon after so I implemented the behavior mods and kept X time in the back of my mind and went on with life.

I'm getting off point, which is that I agree that boiling it down to a single number is probably prohibitively complex, but well worth contemplating. Thinking through the universe of consequences of income disruption and identifying those which are most severe to you personally could suggest "custom" mitigations. For the way I framed my concern there were three pieces of low fruit: significantly reduce spending, pay off the mortgage, and build up a supersized old-school emergency fund. In ere context there are probably more elegant approaches. There may be a way to tease a proxy out of measuring progress to completion of the mitigation steps, but it generally wouldn't be comparable across individuals. And the mitigation steps might chafe against higher-level ere aspirations.

Looking into activities like logistics and supply chain management might suggest some useful tools.

Something more useful may be in how well/quickly someone can source new income source if one of theirs were to go poof.

A careerist would be always working toward lowering the risk of being out of a career rather than lowering risk by having noncorrelated income sources. I am now able to obtain a work income something like 10x my minimum spending in a field that has been in demand for decades, which should still be in demand for decades, and where there will be higher level roles to fill as the boomers in those roles retire, plus the possibility to adapt to technological change in the coming decades (with just a little extra effort and the desire to learn). Yet this "robust" and adaptable 10x income source only counts as a max of 1.0, the same score I'd get if I was working as a cashier with no other skills in a store that was planning to incorporate automated checkout systems.

... Yet this "robust" and adaptable 10x income source only counts as a max of 1.0, the same score I'd get if I was working as a cashier with no other skills in a store that was planning to incorporate automated checkout systems.

Not necessarily in the bigger picture, depending on what you do with the other 9X. If it's funneled into a portfolio, for example, it adds to redundancy. But you are fundamentally correct in that someone who just works a job and saves will top out at IR = 2.0.

Good point, but maybe look at how your plan could fail vs why it should succeed. Also, it seems to me that your advantage over the unskilled cashier is baked into the cake, because you could be buying yourself an alternate source of income every few years with your extreme extra earnings. And, for instance, timberland with cabin would be separate source from 25% of a Rally’s franchise or a share of a Kickstarter desalination system patent etc etc It can be very difficult to uncover shared dependencies or anticipate tail-end risks. For instance, not anticipating that my business partner could lapse into extreme mental illness simultaneously knocked 2 legs out from under my stool a few years ago.