"Mind the Gap!, Mind the Gap!" Do you get that stateside? The London tube has an audible warning every time you cross the horizontal gap onto a tube. Not that I'd take the tube in Covid-19 times, and I live in another region of the UK, but when I did work there it always used to tickle me.

I check out this forum regularly and see updates on the SWR milestones thread with interest. However I have my own take and want to share my thoughts and have feedback. I see the "gap" as very important for Fire aficionados, especially for those over 40.

Say you are 45 years (is that too late for ERE), you live in the US and in your working life you have built up a sizable amount in retirement accounts, these are locked until 59 1/2 (is that correct? we are lucky here, in the UK it is currently 55). You are also entitled to some state pension accessible from 67 (is that right also? financed through social security taxes. this is how it works in the UK).

You have studied your locked retirement accounts and social security/pension.

You need to "bridge the gap" from 45 to 59.5, as from then you have enough to live when you unlock your retirement accounts. So in my example the pot you would need in bank, cash, brokerage accounts etc is $7,000 (x1 Jacob) + 50% (adjusted for semi ERE) = $10.5k x 14.5 years = $147,000.

As to my mind 25 x expenditure ($10.5k x 25 = $262.5k) could leave money on the table, as with savvy investment in your brokerage accounts plus growth in your retirement accounts could be left with more when you hit old age. do you agree?

Mind the Gap

Re: Mind the Gap

I'm in Canada, and we don't have any age restrictions on when you can pull money out of your tax sheltered accounts (RRSP, TFSA). If you wait until 65, you can get a pension tax credit for income received out of RRIF (your RRSP can convert to an RRIF, has a minimum withdrawal each other, % based on your age). There may be withholding taxes depending on the particulars that you get a refund for or owe more at tax time.

We have three government retirement income offerings -- CPP, OAS, and GIS. CPP is paid out in accordance with how much you paid in during your working years; if you take it early or late, that will also affect the amount. OAS is only paid out if you lived in Canada while working (more complicated, but that's the gist). It gets clawed back if you earn too much. GIS is a top up to OAS if you are below a certain threshold in total income (likely not applicable).

My plan is not to bridge the gap. That is to say, I consider the value of CPP, OAS, and GIS to be zero in my forward estimates, and need to survive only upon what I have saved. I hope to be wrong . But these programs have been reformed over the years, and it seems prudent to consider them my hedge against inflation, taxation changes, and/or underperforming investments in my golden years (since they are inflation adjusted, at least today).

. But these programs have been reformed over the years, and it seems prudent to consider them my hedge against inflation, taxation changes, and/or underperforming investments in my golden years (since they are inflation adjusted, at least today).

In order to maximize the annual dollar amounts, I would probably defer taking them for as long as feasible. I'm more concerned about outliving my investments than I am about maximize how many dollars I extract from these programs. If I die at 71, the government had the last laugh for sure, since I probably asked for *nothing.*

But I'm an overpaid software engineer, so, easy street for accumulation.

We have three government retirement income offerings -- CPP, OAS, and GIS. CPP is paid out in accordance with how much you paid in during your working years; if you take it early or late, that will also affect the amount. OAS is only paid out if you lived in Canada while working (more complicated, but that's the gist). It gets clawed back if you earn too much. GIS is a top up to OAS if you are below a certain threshold in total income (likely not applicable).

My plan is not to bridge the gap. That is to say, I consider the value of CPP, OAS, and GIS to be zero in my forward estimates, and need to survive only upon what I have saved. I hope to be wrong

In order to maximize the annual dollar amounts, I would probably defer taking them for as long as feasible. I'm more concerned about outliving my investments than I am about maximize how many dollars I extract from these programs. If I die at 71, the government had the last laugh for sure, since I probably asked for *nothing.*

But I'm an overpaid software engineer, so, easy street for accumulation

-

Dream of Freedom

- Posts: 753

- Joined: Wed Aug 29, 2012 5:58 pm

- Location: Nebraska, US

Re: Mind the Gap

You can do a Roth IRA conversion and take out the principal not profit.

Re: Mind the Gap

@slsdly - thanks for the Canadian perspective. I think many FIRE people do not plan to bridge the gap either. But this means you should extra funds in late retirement.

@Dream of Freedom - think the Roth IRA has similarities to the UK Investment ISA, but as different tax regimes not directly comparable. Cheers for the maths point!

@Dream of Freedom - think the Roth IRA has similarities to the UK Investment ISA, but as different tax regimes not directly comparable. Cheers for the maths point!

-

jacob

- Site Admin

- Posts: 17193

- Joined: Fri Jun 28, 2013 8:38 pm

- Location: USA, Zone 5b, Koppen Dfa, Elev. 620ft, Walkscore 77

- Contact:

Re: Mind the Gap

US tax-deferred retirement accounts aren't entirely locked. You can start withdrawing early using something called rule 72(t). Another trick, especially in the leanFIRE world, is to convert IRAs to Roth IRAs (another type) and withdraw the money w/o penality after 5 years.Adamski wrote: ↑Wed Jun 24, 2020 9:37 amSay you are 45 years (is that too late for ERE), you live in the US and in your working life you have built up a sizable amount in retirement accounts, these are locked until 59 1/2 (is that correct? we are lucky here, in the UK it is currently 55). You are also entitled to some state pension accessible from 67 (is that right also? financed through social security taxes. this is how it works in the UK).

Otherwise, it's certainly optimal to see the various "pots" as covering/bridging different age ranges, e.g. taxable savings from now to 59.5. IRAs from 59.5 to 62 or 67 and Social Security from 67 to death. Ideally this is how it should be planned out using a giant spreadsheet that accounts for taxes.

The original 4% rule was intended to estimate what payouts should be in addition to Social Security between e.g. age 62 and death at 92. In the US SS payments are based on the average of your working income over a 35 year career. You get about 90% of your average best monthly income replaced up to $926/month and 32% after that. From an ERE perspective, the payouts are ginormous, but for an average consumer, who will quickly burn through $1000, they need the personal savings to supplement. Another way of looking at it is if you made $1000/month, you'll get ~$900/month from SS and that's close to most of what you already need. If you made $1900/month, you'll get $1200/month from SS and therefore you need additional savings to maintain spending.

The extreme early retirement (E-ER) crowd needs to save enough to guarantee 50-60 years of payouts rather than 30 and they might not pay enough into SS to get that much out or they might not count on SS existing in 2040 (though it probably will). This crowd is divided between the optimists (4% rule) who accept a certain failure rate and the others (pessimists or conservatives) (3% or less) who do not.

Note that E-ER and ERE are not the same although they do have some overlap in the Venn diagram. ERE is just the pursuit of level 7 and it can be achieved at any age. Once there, FI will follow fairly quickly (within 5-10 years).

Re: Mind the Gap

In addition to what has been said above, are you familiar with Monevator? They did a series on how to account for the split of different savings pots (ISAs and SIPPs) to manage the different stages of early retirement (it's a UK based site in case not familiar):

https://monevator.com/tag/ISA-pension-split-series/

Taking the need to bridge to the next level of detail.

https://monevator.com/tag/ISA-pension-split-series/

Taking the need to bridge to the next level of detail.

-

classical_Liberal

- Posts: 2283

- Joined: Sun Mar 20, 2016 6:05 am

Re: Mind the Gap

I think, with semi-ER particularly, there is a huge psychological advantage to minding the gap. I tend to use the term "bucket" instead, borrowed from traditional retirement advice about the certain tax advantaged accounts.Adamski wrote: ↑Wed Jun 24, 2020 9:37 amYou need to "bridge the gap" from 45 to 59.5, as from then you have enough to live when you unlock your retirement accounts. So in my example the pot you would need in bank, cash, brokerage accounts etc is $7,000 (x1 Jacob) + 50% (adjusted for semi ERE) = $10.5k x 14.5 years = $147,000.

If I have enough in my traditional retirement bucket (60 on or whatever), including a realistic amount from underfunded state pensions like SS, then the pressure is off to save for normal "retirement". It's like having a debt you owe to your future self paid. This allows for more risk taking in the interim. This could mean both investing and in life. Because if your 45, how much of a buffer do you really need to make it to 60 in a semi-RE scenerio, particularly if spending needs are 1-2 JAFI's. Almost nothing, if paid work is part of the plan.

Re: Mind the Gap

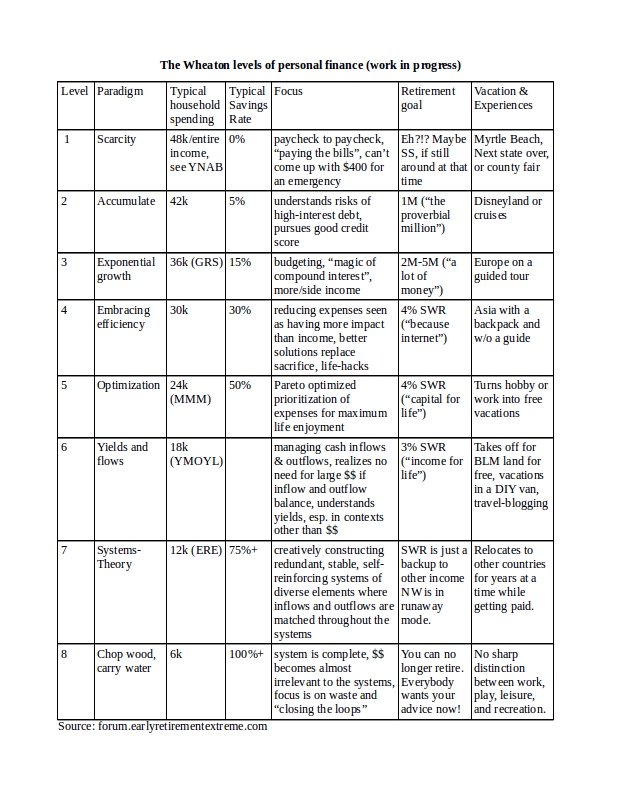

@jacob, thanks for US system perspective and taking time to reply. Love the chart of levels of personal finance.

I'm level 5 MMM on the chart. My spending is not truly ERE and to be honest don't want to take it too frugal. Except to those i know on levels 1 and 2 I'm probably seen as extreme or crazy (or will be when I 'RE and give up a decent paid job very soon).

@egg, yes know, like the monevator site. Great source of info for UK ppl and very well written and balanced.

@classical, thanks. I've not decided on part time work. My latest thinking is a clean break would be better. Then for the gap, will risk it that my funds will last, then return to work, only if investments take a heavy hit (without bounce back) or cash forecast looks like could run out. Cheers and take care

I'm level 5 MMM on the chart. My spending is not truly ERE and to be honest don't want to take it too frugal. Except to those i know on levels 1 and 2 I'm probably seen as extreme or crazy (or will be when I 'RE and give up a decent paid job very soon).

@egg, yes know, like the monevator site. Great source of info for UK ppl and very well written and balanced.

@classical, thanks. I've not decided on part time work. My latest thinking is a clean break would be better. Then for the gap, will risk it that my funds will last, then return to work, only if investments take a heavy hit (without bounce back) or cash forecast looks like could run out. Cheers and take care

-

UK-with-kids

- Posts: 228

- Joined: Tue Oct 09, 2018 4:55 am

- Location: Oxbridge, UK

Re: Mind the Gap

Interesting subject. Of course, those "Mind the Gap" announcements and signs are mainly where train carriages aren't close enough to the platforms, for example when the station was built on a curve. That's the result of the Tube (=Subway) being built in the 19th century when Health & Safety wasn't a thing (the first trains were pulled by steam engines, running underground!)

I stopped focusing so much on SWRs a while ago and made a ladder/waterfall type spreadsheet to help me bridge the gap. I think this is the natural consequence of getting older, looking ahead to the approaching milestones when you can access certain funds and realising that all you need to do is make sure you can get there! My spreadsheet goes from 2020 up until 2047, but to do the calculations you start at the end and work backwards towards the present day.

In 2047 we'll both be getting our state pensions - in the UK it's really easy to meet the minimum entitlement and it's not really impacted by earning too little. I believe the current rate is £175.20 per week or £9,110 per year. So in 2047 we'll have an income of £18,220. If that was all we needed then you can assume remaining savings of zero are ok at that point. One year earlier in 2046 only one of us will have reached pensionable age, and hence we'd have an income of £9,110 and need to fund another £9,110 from our private pension pots (called "SIPPs" in the UK) in order to have the same £18,220. A few years earlier neither of us will have the state pension yet and so we'd need to be funding the full £18,220 from our private pensions until we reach the point where they're all used up. And before that we'd be using our non-pension funds (usually "ISAs" in the UK). And if I keep moving back up towards the present until I've used the whole non-pension ISA assets I eventually get to the age where we'd first be dipping into savings, which means that until that point we'll still need to be earning money. But in my simple example, we'd only need to earn £18,220 between two people, which is part-time burger flipping territory really.

A key risk is having too much in the SIPP (the private pension) and not enough in the ISAs (non-pension assets), because in the UK it's completely impossible to access pension funds early - in my case before age 57. It's only too easy to end up with more money in pensions because a lot of the saving is "automatic" (e.g. deducted from wages) and the funds have longer to compound, whereas the non-pension assets could easily get spent along the way, e.g. to fund a home purchase, and they're more likely to lose value to inflation if held in cash.

Anyway, my spreadsheet has an awful lot of assumptions in it - all in today's terms, assumes state pensions don't get eroded in real terms, doesn't really take account of funds performance, assumes we stay together as a couple and both stay alive... I've also simplified the way I've explained it above because I'm actually aiming for more than £18,220 in annual income at retirement. But to summarise its purpose: I've already saved enough for retirement, and now I just need to get there. Do I have enough savings to get me to 2047, and is my money all in the right buckets? How much longer do I need to continue working and/or how much do I need to earn before I can retire?

I stopped focusing so much on SWRs a while ago and made a ladder/waterfall type spreadsheet to help me bridge the gap. I think this is the natural consequence of getting older, looking ahead to the approaching milestones when you can access certain funds and realising that all you need to do is make sure you can get there! My spreadsheet goes from 2020 up until 2047, but to do the calculations you start at the end and work backwards towards the present day.

In 2047 we'll both be getting our state pensions - in the UK it's really easy to meet the minimum entitlement and it's not really impacted by earning too little. I believe the current rate is £175.20 per week or £9,110 per year. So in 2047 we'll have an income of £18,220. If that was all we needed then you can assume remaining savings of zero are ok at that point. One year earlier in 2046 only one of us will have reached pensionable age, and hence we'd have an income of £9,110 and need to fund another £9,110 from our private pension pots (called "SIPPs" in the UK) in order to have the same £18,220. A few years earlier neither of us will have the state pension yet and so we'd need to be funding the full £18,220 from our private pensions until we reach the point where they're all used up. And before that we'd be using our non-pension funds (usually "ISAs" in the UK). And if I keep moving back up towards the present until I've used the whole non-pension ISA assets I eventually get to the age where we'd first be dipping into savings, which means that until that point we'll still need to be earning money. But in my simple example, we'd only need to earn £18,220 between two people, which is part-time burger flipping territory really.

A key risk is having too much in the SIPP (the private pension) and not enough in the ISAs (non-pension assets), because in the UK it's completely impossible to access pension funds early - in my case before age 57. It's only too easy to end up with more money in pensions because a lot of the saving is "automatic" (e.g. deducted from wages) and the funds have longer to compound, whereas the non-pension assets could easily get spent along the way, e.g. to fund a home purchase, and they're more likely to lose value to inflation if held in cash.

Anyway, my spreadsheet has an awful lot of assumptions in it - all in today's terms, assumes state pensions don't get eroded in real terms, doesn't really take account of funds performance, assumes we stay together as a couple and both stay alive... I've also simplified the way I've explained it above because I'm actually aiming for more than £18,220 in annual income at retirement. But to summarise its purpose: I've already saved enough for retirement, and now I just need to get there. Do I have enough savings to get me to 2047, and is my money all in the right buckets? How much longer do I need to continue working and/or how much do I need to earn before I can retire?

Re: Mind the Gap

Well, I am currently 52 and a bit and I can get my UK pension pots at 55 - that gap is currently 32 months, but who is counting...

It turned out that I had a lot of money in pensions but not much outside of that.

I decided to a bit of creative accounting and remortgage my house. a very competitive rate of 1.6% interest.

The loan is enough to live on without major frills - however, the option/prospect of work is still there if I want to dive in.

That is another option if your have enough equity in your property...

It turned out that I had a lot of money in pensions but not much outside of that.

I decided to a bit of creative accounting and remortgage my house. a very competitive rate of 1.6% interest.

The loan is enough to live on without major frills - however, the option/prospect of work is still there if I want to dive in.

That is another option if your have enough equity in your property...

-

UK-with-kids

- Posts: 228

- Joined: Tue Oct 09, 2018 4:55 am

- Location: Oxbridge, UK

Re: Mind the Gap

Interesting idea. Was this a conventional mortgage then? I read on your 2020 thread that you were doing salary sacrifice and also that you quit your job. Did you arrange the mortgage before any of that started? It feels like the mortgage option would be most easily available while you don't need it because you have an income from a salary, but if you lose your job and you're trying to bridge the gap then it might be hard to get a loan.

Re: Mind the Gap

Yes, I arranged the mortgage before I quit - banks are rather narrow mindedUK-with-kids wrote: ↑Tue Jun 30, 2020 9:09 amInteresting idea. Was this a conventional mortgage then? I read on your 2020 thread that you were doing salary sacrifice and also that you quit your job. Did you arrange the mortgage before any of that started? It feels like the mortgage option would be most easily available while you don't need it because you have an income from a salary, but if you lose your job and you're trying to bridge the gap then it might be hard to get a loan.

The house was paid off, with this remortgage they have loaned me 35% the value of the house with a standard repayment mortgage.

The fixed period is 5 years at 1.6% which is very reasonable.

By the time the fixed period ends, I have access to my SIPPs... So I can pay the remaining off in a lump.

Also, I have a lodger and the rent pays the lions share of the mortgage.