This forum is a huge resource even after FI, what other group of INTJ's would answer all of my questions?

How my wife and I saved up $1M by age 30 and became FI!

Re: How my wife and I saved up $1M by age 30 and became FI!

tact?

This forum is a huge resource even after FI, what other group of INTJ's would answer all of my questions?

This forum is a huge resource even after FI, what other group of INTJ's would answer all of my questions?

-

disparatum

- Posts: 61

- Joined: Sun Mar 30, 2014 3:07 pm

Re: How my wife and I saved up $1M by age 30 and became FI!

That's right!! If i had put a smiley at the end of my first post, misunderstandings might have been minimal.Maybe Poe's Law

I am not sure if you are expecting an answer to this questionThis forum is a huge resource even after FI, what other group of INTJ's would answer all of my questions?

Re: How my wife and I saved up $1M by age 30 and became FI!

Congrats on reaching FI so quickly. Costa Rica is a great place, we hope to make it there some day. Pura vida!

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

Hey all, I did some tax analysis and figured out that next year we should be able to completely avoid paying any federal income tax at all (we already pay no state income tax, since we're residents of Nevada). If anyone can poke some holes in this analysis, please let me know!

Here are our current Investment Accounts:

$315,000 - Traditional IRA

$80,000 - Roth IRA

$500,000 - Taxable Investments (Vanguard)

$15,000 - HSA

$95,000 - RRSP (Canada)

$20,000 - LIRA (Canada)

We plan on doing a tax-free Roth IRA Conversion Ladder of $20,600 every year. We're also aiming to live annually on $30,000-40,000 (3-4% of our portfolio).

For our US health care plan, we're aiming for the ‘Gold Plated Silver Plan‘ (200% of FPL with cost sharing subsidies) which will cost us $1,486 for the year and to qualify for it we require a MAGI of $31,460. So our expected income will be:

$20,600 – Conversion of Traditional IRA to Roth IRA (this is counted against our MAGI - but we must wait 5 years for this money)

$10,860 – Capital gains from our Taxable Investment Account

$19,140 – Distributions from our Roth IRA (don’t count towards MAGI).

Ok, this is a lot of information. I'm wondering how many others plan on using their Roth IRA to modify their health care plan costs?

Thanks!

Here are our current Investment Accounts:

$315,000 - Traditional IRA

$80,000 - Roth IRA

$500,000 - Taxable Investments (Vanguard)

$15,000 - HSA

$95,000 - RRSP (Canada)

$20,000 - LIRA (Canada)

We plan on doing a tax-free Roth IRA Conversion Ladder of $20,600 every year. We're also aiming to live annually on $30,000-40,000 (3-4% of our portfolio).

For our US health care plan, we're aiming for the ‘Gold Plated Silver Plan‘ (200% of FPL with cost sharing subsidies) which will cost us $1,486 for the year and to qualify for it we require a MAGI of $31,460. So our expected income will be:

$20,600 – Conversion of Traditional IRA to Roth IRA (this is counted against our MAGI - but we must wait 5 years for this money)

$10,860 – Capital gains from our Taxable Investment Account

$19,140 – Distributions from our Roth IRA (don’t count towards MAGI).

Ok, this is a lot of information. I'm wondering how many others plan on using their Roth IRA to modify their health care plan costs?

Thanks!

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

Hi everyone! It's now been six months since we quit our jobs and started traveling!

When we left the U.S. in March to begin our travels, our portfolio was around $1,030,000. Currently, it’s closer to $960,000, which is a drop of $70,000. Considering we’ve only spent $17,400 in that time, the bulk of the drop has just been the stock markets going up and down. Instead of worrying, we do our best to ignore crazy market behavior and focus on living within our means – keeping our spending low.

Our goal has always been to live on 3-4% of our portfolio, which at $960,000 translates to an annual budget of between $28,800-$38,400. This gives us a monthly budget of $2,400-$3,200.

The good news is that so far during our traveling, we’ve done a decent job of adhering to our budget. Here are our monthly expenses so far:

This overall monthly average of $2,889 represents an annual spend of 3.6% of our portfolio. Not bad – we’re pretty much on target!

Let me know if you have any questions, I'd be delighted to answer!

When we left the U.S. in March to begin our travels, our portfolio was around $1,030,000. Currently, it’s closer to $960,000, which is a drop of $70,000. Considering we’ve only spent $17,400 in that time, the bulk of the drop has just been the stock markets going up and down. Instead of worrying, we do our best to ignore crazy market behavior and focus on living within our means – keeping our spending low.

Our goal has always been to live on 3-4% of our portfolio, which at $960,000 translates to an annual budget of between $28,800-$38,400. This gives us a monthly budget of $2,400-$3,200.

The good news is that so far during our traveling, we’ve done a decent job of adhering to our budget. Here are our monthly expenses so far:

Code: Select all

Month Monthly Spend Comments

April $2,044.39 Traveled through Mexico and Guatemala

May $2,763.59 Traveled El Salvador, Nicaragua, and Costa Rica.

June $4,215.56 Costa Rica living with purchase of flights to D.C.

July $2,684.01 Costa Rica living

Aug $2,800.96 Traveled Costa Rica and Panama

Sept $2,826.01 Traveled Washington, D.C. and NYC

Overall Average $2,889.09 Let me know if you have any questions, I'd be delighted to answer!

Re: How my wife and I saved up $1M by age 30 and became FI!

It's interesting that you have an RRSP and LIRA in the mix.

I'm not familiar with the situation for RRSP's when people move overseas. What is your Canadian situation from a tax perspective? Canada is very aggressive (compared to other first world countries) on residency and collecting taxes on money earned anywhere while you are still a "resident for tax purposes".

I'm not familiar with the situation for RRSP's when people move overseas. What is your Canadian situation from a tax perspective? Canada is very aggressive (compared to other first world countries) on residency and collecting taxes on money earned anywhere while you are still a "resident for tax purposes".

-

IlliniDave

- Posts: 3876

- Joined: Wed Apr 02, 2014 7:46 pm

Re: How my wife and I saved up $1M by age 30 and became FI!

No real questions, but glad to hear you are excited and enjoying life! I have much less wanderlust in me than you, but your travels sound fun. Good luck.

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

Yeah, I'm not really looking forward to pulling money from the RRSP/LIRA.BlueNote wrote:It's interesting that you have an RRSP and LIRA in the mix.

I'm not familiar with the situation for RRSP's when people move overseas. What is your Canadian situation from a tax perspective? Canada is very aggressive (compared to other first world countries) on residency and collecting taxes on money earned anywhere while you are still a "resident for tax purposes".

When we pull from our RRSP in the future, Canada will do a standard 25% withholding tax because we are currently non-residents, but we should be able to get a refund from the Canada Revenue Agency (CRA) at the end of that tax year by filing Non-Resident Income Taxes (Section 217). We would enter all our world income on the Section 217, and apply the Canadian personal exemption of $22,276 for a married couple. For example, if we had world income of $40,000 and applied the exemption, we would need to pay a 15% Canadian tax rate on the remaining $17,724 (which would be total tax of $2,659). Also, we would need to pay US taxes on the RRSP gains since we left Canada in 2008.

Sounds like fun, right?

Re: How my wife and I saved up $1M by age 30 and became FI!

Yeah sounds like a blast! I had a similar situation where I was working for a Japanese company. Canada decided I was still a resident for tax purposes and that I would owe them the difference between the income tax rate in Japan and the Canadian rate which netted out to about 20%. I had to pay my income taxes in one lump sum which sucked.freedomwithbruno wrote:

Sounds like fun, right?

Americans have a better deal from what I understand, it's too bad the money's trapped in Canada but maybe you'll one day move back to Canada for awhile and can start drawing it down at a more reasonable income tax rate.

-

Hankaroundtheworld

- Posts: 470

- Joined: Mon Feb 24, 2014 4:50 am

Re: How my wife and I saved up $1M by age 30 and became FI!

Hi drivingwithbrunoincentralamerica, in your expenses, nothing is around "medical", like insurance, etc... I guess, if you are young, not much is needed, but how do you insure yourself against the none-foreseen big items, like an accident, etc..

cheers, Hank

cheers, Hank

Re: How my wife and I saved up $1M by age 30 and became FI!

Hello,

Just wanted to say that it's wonderful that you guys manage to live this.

Of course we do not have the same risk profile and priorities, but with your earnings power, I would have considered working a few years more to reach the $2M mark, for a few reasons:

- Reaching a 2% real return (after inflation, ie between 3% and 5% nominal return) is definitely safer than a 4% real return (which after inflation will mean between 6% and 8% nominal return: there's no guarantee that equities will be able to sustain that growth rate)

- Being able to work and resume your lucrative career today doesn't mean you'll be able to do that tomorrow

- Need to plan for the unforeseen big item, as the previous poster mentioned

I do believe that the way you're going might be sustainable, but with my risk profile I'd definitely have pushed hard for another 5 years to get that extra safety margin and not have to wonder about it.

Another remark is that a lot of your investments seem to be managed by Vanguard - I would have sliced these into two $250K tranches and have these tranches managed by 2 different asset managers just in case one of them defaults (because if that happens the Federal insurance will kick in and guarantee the whole $500K, however in the present situation you could lose $250K because only the first tranche would get covered - assuming all your investments are made in the same assets category https://en.wikipedia.org/wiki/Federal_D ... orporation).

Just wanted to say that it's wonderful that you guys manage to live this.

Of course we do not have the same risk profile and priorities, but with your earnings power, I would have considered working a few years more to reach the $2M mark, for a few reasons:

- Reaching a 2% real return (after inflation, ie between 3% and 5% nominal return) is definitely safer than a 4% real return (which after inflation will mean between 6% and 8% nominal return: there's no guarantee that equities will be able to sustain that growth rate)

- Being able to work and resume your lucrative career today doesn't mean you'll be able to do that tomorrow

- Need to plan for the unforeseen big item, as the previous poster mentioned

I do believe that the way you're going might be sustainable, but with my risk profile I'd definitely have pushed hard for another 5 years to get that extra safety margin and not have to wonder about it.

Another remark is that a lot of your investments seem to be managed by Vanguard - I would have sliced these into two $250K tranches and have these tranches managed by 2 different asset managers just in case one of them defaults (because if that happens the Federal insurance will kick in and guarantee the whole $500K, however in the present situation you could lose $250K because only the first tranche would get covered - assuming all your investments are made in the same assets category https://en.wikipedia.org/wiki/Federal_D ... orporation).

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

Currently we do not have health insurance coverage, but once we're back in the US we'll be signing up for an ACA Health Plan. If we have any issues while traveling in Central America, we'll pay cash for health services.Hankaroundtheworld wrote:Hi drivingwithbrunoincentralamerica, in your expenses, nothing is around "medical", like insurance, etc... I guess, if you are young, not much is needed, but how do you insure yourself against the none-foreseen big items, like an accident, etc..

cheers, Hank

For now, we're happy with $1M in savings. In the future, will we regret not saving more? Maybe, maybe not. I'm not much for regret, and I'm confident we can make things work living on $40k/year.julien wrote:...I do believe that the way you're going might be sustainable, but with my risk profile I'd definitely have pushed hard for another 5 years to get that extra safety margin and not have to wonder about it.

Another remark is that a lot of your investments seem to be managed by Vanguard - I would have sliced these into two $250K tranches and have these tranches managed by 2 different asset managers just in case one of them defaults (because if that happens the Federal insurance will kick in and guarantee the whole $500K, however in the present situation you could lose $250K because only the first tranche would get covered - assuming all your investments are made in the same assets category https://en.wikipedia.org/wiki/Federal_D ... orporation).

Good suggestion regarding Vanguard, although everything I've read indicates that they are a stable, well-run company. I'll look into it a bit more.

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

Hey everyone! Just wanted to provide another followup update on our travels (if anyone is interested). We're alive and well, and we successfully drove our 4Runner all the way up from Costa Rica, through Mexico and now we're back in the US. So far so good! Everyone we've met along the way has been extremely friendly and helpful, and we've had no problems with corrupt police officers or anything. Maybe we've just had good luck?

As we've been driving through the US, we're currently searching for where our next home should be. If anyone is curious, we just made a blog post describing the cities we compared: http://freedomwithbruno.com/hunting-bes ... ment-city/ We think we might settle in Asheville, NC.

If anyone has any questions, I'd be more than happy to answer!

As we've been driving through the US, we're currently searching for where our next home should be. If anyone is curious, we just made a blog post describing the cities we compared: http://freedomwithbruno.com/hunting-bes ... ment-city/ We think we might settle in Asheville, NC.

If anyone has any questions, I'd be more than happy to answer!

Re: How my wife and I saved up $1M by age 30 and became FI!

How expensive was it to travel on the road in South America? Did you buy a van? Apologies if you have already told us this

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

No problem! We bought a 2000 Toyota 4Runner, fixed it up, and drove down to Costa Rica from California, rented a house for a few months, then drove back up to the US. Overall, cost of living was pretty reasonable while we were traveling. We spent around $2,800/mo on our way down, which included a lot of Airbnb stops.Did wrote:How expensive was it to travel on the road in South America? Did you buy a van? Apologies if you have already told us this

Re: How my wife and I saved up $1M by age 30 and became FI!

thanks. much scope for free camping?

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

Well, we usually stayed at real campsites, since we wanted working bathrooms with water. But if we had a more self-sustaining camping vehicle, we could have done a lot more free nights!Did wrote:thanks. much scope for free camping?

-

freedomwithbruno

- Posts: 15

- Joined: Thu May 21, 2015 2:12 pm

- Contact:

Re: How my wife and I saved up $1M by age 30 and became FI!

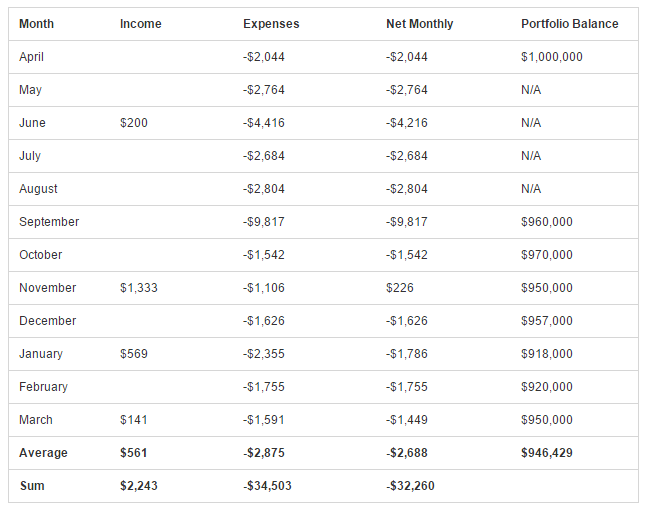

Hey everyone, it's now been more than a year since we quit our jobs, and at the end of each month we've been keeping track of our expenses and our portfolio balance. Here’s what the last twelve months have looked like:

In total, we spent $32,260 of our portfolio as expenses over the year. Dividing this by an average of our portfolio balance, we get an overall Withdrawal Rate for the year of 3.4% ($32,260/$946,429). Our target for the year was a very conservative 3%, so we’re reasonably happy with this!

All in all, it’s been a hell of a year. The freedom that Amanda and I have had in the last year has allowed for experiences and joy unlike anything I have experienced before. If anyone is on the fence about early retirement, don't delay - you won't regret it!

In total, we spent $32,260 of our portfolio as expenses over the year. Dividing this by an average of our portfolio balance, we get an overall Withdrawal Rate for the year of 3.4% ($32,260/$946,429). Our target for the year was a very conservative 3%, so we’re reasonably happy with this!

All in all, it’s been a hell of a year. The freedom that Amanda and I have had in the last year has allowed for experiences and joy unlike anything I have experienced before. If anyone is on the fence about early retirement, don't delay - you won't regret it!

Re: How my wife and I saved up $1M by age 30 and became FI!

Sounds cool, though I'd be a bit taken aback by declining the principal from 1M to 950k in just a year. Four percent smorpercent, that's a lot! Maybe that's why I don't like the total return approach, preferring instead to spend dividends and leaving the principal alone. How have you handled seeing the portfolio decline by 50K (~5%) in one year from mostly expenses?