@ Secretwealth

It's already in the works. In the next couple of weeks the plan is to mothball one of our two cars. In the next 2 months, we are going to put our son into a regular daycare rather than keeping the full time nanny. These two steps alone will substantially cut down on monthly expenses.

Over the next 1-2 years, we are going to purchase a house with no mortgage. This would effectively eliminate the rent as an expense. Hopefully, we can pull this off.

DebtSlaveNoMore's Journal

-

secretwealth

- Posts: 1948

- Joined: Mon Jun 27, 2011 3:31 am

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

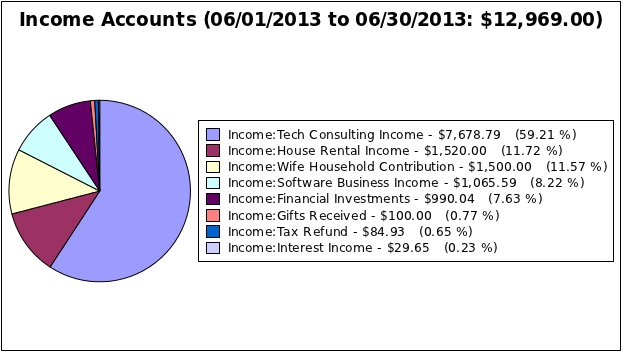

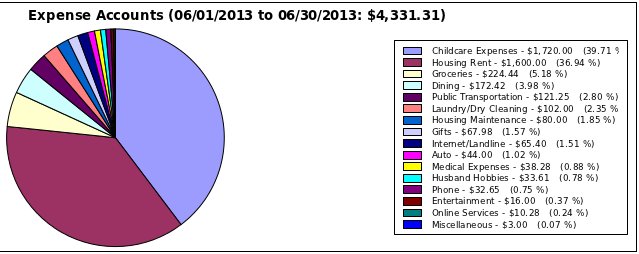

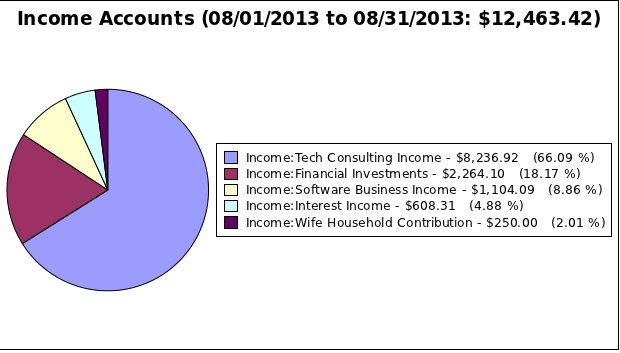

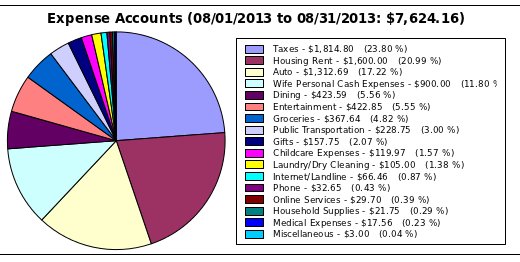

May has come and gone. Here are my numbers for May:

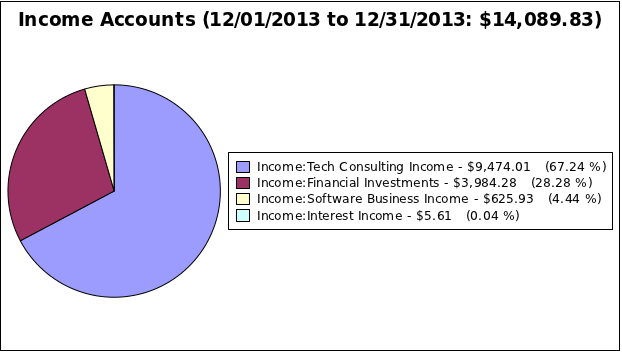

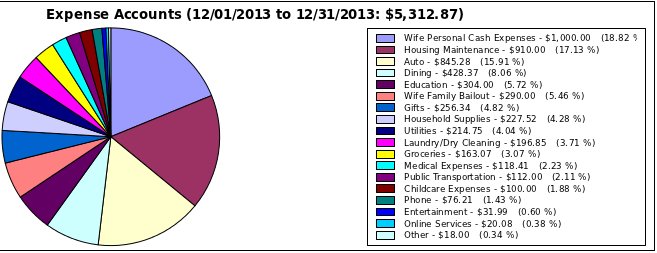

Income: $16,218.31

Expenses: $4,910.92

Monthly Savings Rate: 70.0%

YTD Savings Rate: 53.4%

Months Living Expenses: 99

The Good:

I have successfully mothballed one of our 2 cars. This should save us approximately $200/month in terms of insurance, maintenance, and gas.

The pre-diabetic diet/exercise regime is working out well for me, I have lost approximately 18 lbs in the last 2 months. I'm feeling much better too. The only drawback is that I'm now eating mostly veggies and walking 3 miles every day.

Financial Investments went gangbusters in May for some reason, so money seems to be rushing into my coffers from all corners. I know that this kind of valuation growth cannot last forever.

After much discussion with my wife, we decided to not move to the country side for at least another 5 years. City living has it's drawbacks but we would get to FI much faster if we continued living in our current abode. Because of this decision, I will be investing over 80K of cash(our house fund) into various financial investments over the next several months.

Starting in June, we are putting our toddler son into normal Day care instead of keeping him with a dedicated nanny. If this transition is successful, expenses should be lowered by an additional $500/month.

The Bad:

A water pipe bursted in the basement of my rental house. The tenant was able to contain the leak with the aid of some buckets. But since I was visiting family in Connecticut and could not drive there to fix it myself, I had to call a plumber on Sunday and pay the guy $200 to fix something that I could have done myself for $50 in material costs.

Additionally, I launched my new software product in May. After an initial flurry of sales during the first week, purchases have slowed down a lot. This is really disappointing because the summer is the traditional slow period of this business, and I was really counting on this product to pick up the slack. Assuming that this product doesn't sell well, it means that my software business income is going to be significantly lower in the next 3 months.

Things are very difficult at the day job. The workload is super demanding, and my boss is giving me grief on a daily basis. I suspect that he might be envious of the fact that I have a wife and son while he's in his mid 40s without a family.

The Ugly:

One of my wife's closest friends just left her husband of 9 years. She told my wife that she was entirely dis-satisfied with the "impoverished" life that he(an auto-mechanic) provided for her and their son and thought she could do better. So now this woman is living in a tiny studio apartment in Staten island with her 5 year old son.

Now my wife has been spending large amounts of money on luxury goods these past couple of months. The bulk of the purchases are on designer clothes, handbags, shoes, and a high-end "jumbo" stroller for our son costing over $1000 dollars. She has also donated around $600 to charities in the last month(which I think is great). But she was super public about it, to the point of bragging(which I do not approve of). Now one of my wife's friends have stopped talking to her, and another one has just left her husband. I have this sinking feeling that my DW's consumerism is playing a part in this. But it's her money to spend, and I need to respect that.

Income: $16,218.31

Expenses: $4,910.92

Monthly Savings Rate: 70.0%

YTD Savings Rate: 53.4%

Months Living Expenses: 99

The Good:

I have successfully mothballed one of our 2 cars. This should save us approximately $200/month in terms of insurance, maintenance, and gas.

The pre-diabetic diet/exercise regime is working out well for me, I have lost approximately 18 lbs in the last 2 months. I'm feeling much better too. The only drawback is that I'm now eating mostly veggies and walking 3 miles every day.

Financial Investments went gangbusters in May for some reason, so money seems to be rushing into my coffers from all corners. I know that this kind of valuation growth cannot last forever.

After much discussion with my wife, we decided to not move to the country side for at least another 5 years. City living has it's drawbacks but we would get to FI much faster if we continued living in our current abode. Because of this decision, I will be investing over 80K of cash(our house fund) into various financial investments over the next several months.

Starting in June, we are putting our toddler son into normal Day care instead of keeping him with a dedicated nanny. If this transition is successful, expenses should be lowered by an additional $500/month.

The Bad:

A water pipe bursted in the basement of my rental house. The tenant was able to contain the leak with the aid of some buckets. But since I was visiting family in Connecticut and could not drive there to fix it myself, I had to call a plumber on Sunday and pay the guy $200 to fix something that I could have done myself for $50 in material costs.

Additionally, I launched my new software product in May. After an initial flurry of sales during the first week, purchases have slowed down a lot. This is really disappointing because the summer is the traditional slow period of this business, and I was really counting on this product to pick up the slack. Assuming that this product doesn't sell well, it means that my software business income is going to be significantly lower in the next 3 months.

Things are very difficult at the day job. The workload is super demanding, and my boss is giving me grief on a daily basis. I suspect that he might be envious of the fact that I have a wife and son while he's in his mid 40s without a family.

The Ugly:

One of my wife's closest friends just left her husband of 9 years. She told my wife that she was entirely dis-satisfied with the "impoverished" life that he(an auto-mechanic) provided for her and their son and thought she could do better. So now this woman is living in a tiny studio apartment in Staten island with her 5 year old son.

Now my wife has been spending large amounts of money on luxury goods these past couple of months. The bulk of the purchases are on designer clothes, handbags, shoes, and a high-end "jumbo" stroller for our son costing over $1000 dollars. She has also donated around $600 to charities in the last month(which I think is great). But she was super public about it, to the point of bragging(which I do not approve of). Now one of my wife's friends have stopped talking to her, and another one has just left her husband. I have this sinking feeling that my DW's consumerism is playing a part in this. But it's her money to spend, and I need to respect that.

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

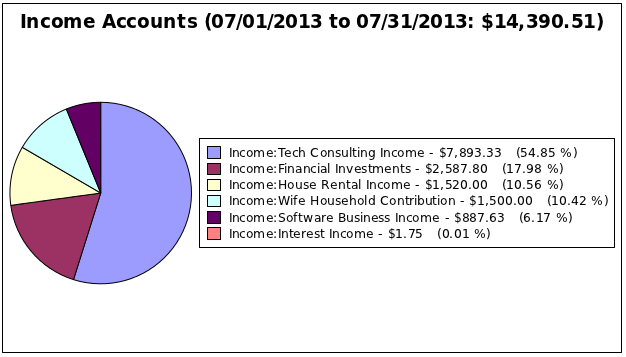

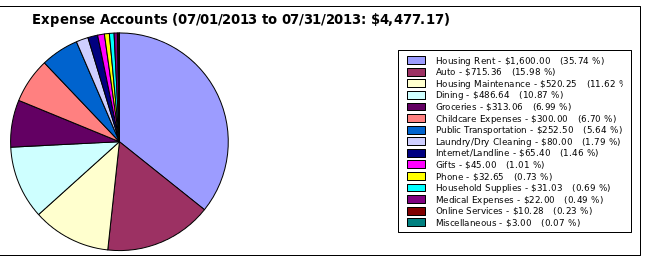

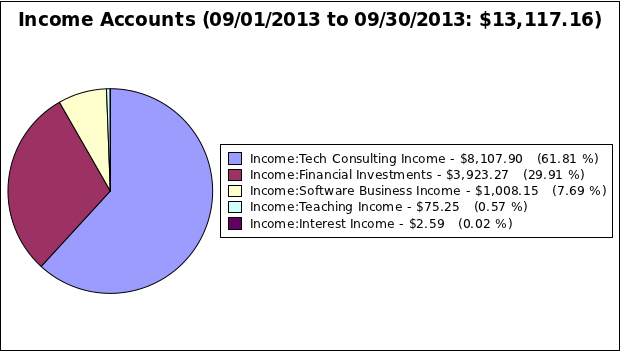

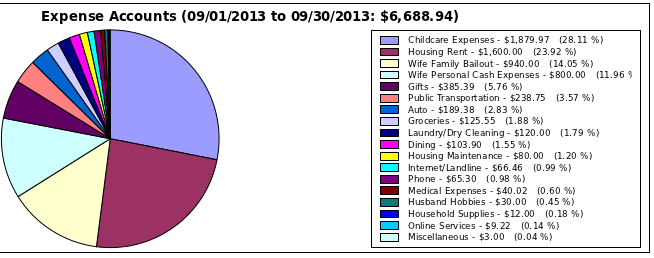

Numbers for June

I've been on vacation down south for the last week, and thus have been a bit tardy with my journal entry. So without further adieu, here are the numbers for June:

Monthly Savings Rate: 66.6%

YTD Savings Rate: 55.6%

Months Living Expenses: 115

The Good:

This pre-diabetic diet is really beginning to take effect. I've lost 25 pounds since beginning this regime and my energy levels are way up! For some reason, a largely vegetarian diet seems to make me calmer. This is having a positive impact on our budget because I'm buying way less red meat and relying on the backyard vegetable garden as a major source of food.

June was a really efficient month, nearly 77% of household expenses were taken up by rent and childcare. For everything else during this month, my family of three spent only $1011. While I know it's still a very lavish budget in the grand scheme of things, it's a new record for my household

I'm noticing something very interesting here. Even a small decrease in monthly expenses can dramatically increase the number of months expenses that I've saved up. So I really need to get cracking in finding ways to reduce monthly costs.

The Bad:

Small business revenue has totally flat-lined in June. Right now we are in the worst time of the year for software/app sales, so I don't anticipate earnings to pick up significantly until about October. With that said however, I am working on a new app that will hopefully launch within the next 2 weeks.

During this month, my son was enrolled into a regular (and much cheaper) day care. Unfortunately he was kicked out after just 3 weeks due to him pushing and biting other children. I have no idea why my 2 year old is acting out, internet searches indicates that it's either a phase or some expression of frustration on his part. In any case, he is back with the nanny at a staggering cost of $1600 a month. Child care has emerged as the single largest expense on our budget, and there is little that I can do to lower this cost.

Our financial investments took a beating in June. The markets dropped a lot and I only "earned" money in this sector because of several dividend payouts and the regular 401K contribution.

The Ugly:

My day job lost a big project, so several more people were suddenly laid off. I survived again, but at this point, I'm saying a small prayer for every paycheck that I get from them.

My wife's parents have an old roof that needs to be replaced, this is going to cost around $12,000. They of course have no savings to speak off and just spent $8000 last year to posh up their backyard. The good thing here is that the cost will need to be split between me/my wife, my sister-in-law/her husband, and my in-laws. But this will still be a huge financial hit in late July or August.

The one car that we are keeping around suddenly developed engine trouble 3 weeks ago. And the fix required a massive tune up at the auto-mechanic's place. Cost ran up to be around $1200, which will need to be paid by August. I hate cars, but I also really need to learn how to fix them!

Monthly Savings Rate: 66.6%

YTD Savings Rate: 55.6%

Months Living Expenses: 115

The Good:

This pre-diabetic diet is really beginning to take effect. I've lost 25 pounds since beginning this regime and my energy levels are way up! For some reason, a largely vegetarian diet seems to make me calmer. This is having a positive impact on our budget because I'm buying way less red meat and relying on the backyard vegetable garden as a major source of food.

June was a really efficient month, nearly 77% of household expenses were taken up by rent and childcare. For everything else during this month, my family of three spent only $1011. While I know it's still a very lavish budget in the grand scheme of things, it's a new record for my household

I'm noticing something very interesting here. Even a small decrease in monthly expenses can dramatically increase the number of months expenses that I've saved up. So I really need to get cracking in finding ways to reduce monthly costs.

The Bad:

Small business revenue has totally flat-lined in June. Right now we are in the worst time of the year for software/app sales, so I don't anticipate earnings to pick up significantly until about October. With that said however, I am working on a new app that will hopefully launch within the next 2 weeks.

During this month, my son was enrolled into a regular (and much cheaper) day care. Unfortunately he was kicked out after just 3 weeks due to him pushing and biting other children. I have no idea why my 2 year old is acting out, internet searches indicates that it's either a phase or some expression of frustration on his part. In any case, he is back with the nanny at a staggering cost of $1600 a month. Child care has emerged as the single largest expense on our budget, and there is little that I can do to lower this cost.

Our financial investments took a beating in June. The markets dropped a lot and I only "earned" money in this sector because of several dividend payouts and the regular 401K contribution.

The Ugly:

My day job lost a big project, so several more people were suddenly laid off. I survived again, but at this point, I'm saying a small prayer for every paycheck that I get from them.

My wife's parents have an old roof that needs to be replaced, this is going to cost around $12,000. They of course have no savings to speak off and just spent $8000 last year to posh up their backyard. The good thing here is that the cost will need to be split between me/my wife, my sister-in-law/her husband, and my in-laws. But this will still be a huge financial hit in late July or August.

The one car that we are keeping around suddenly developed engine trouble 3 weeks ago. And the fix required a massive tune up at the auto-mechanic's place. Cost ran up to be around $1200, which will need to be paid by August. I hate cars, but I also really need to learn how to fix them!

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

Another month has rolled by, here are our numbers for July:

Monthly Savings Rate: 68.9%

YTD Savings Rate: 57.5%

Months Living Expenses: 114

Major happenings:

Lots of things came to a head at the end of July.

1. My wife has entirely exhausted her savings. She has a negative balance in her checking account and 500 dollars in credit card debt due that she can't pay until her next paycheck. What is troubling to me is that when we split our finances 4 months ago, I left her with over $5,000 in her checking account. And she had $1600 a month in spending money from her day job for the last 4 months. So basically, DW spent over $11,000 in 4 months on luxury products and redundant baby supplies.

So DW was panicking again and ultimately, I had to re-gain direct control of her finances. She gave me her credit card, debit card, and check book. And we are going back to the cash-in-envelope system. She agreed to be content with $1200 a month to spend for non-essentials as long as I make her debt problems go away. I feel like this cash-only approach causes a lot of friction between us, but it seems to be the only way to save my wife from herself.

2. Strange things are afoot at my day job. The VP of the company basically offered me a role that would lead to a promotion to tech executive position. If I can handle this challenge, then my day job's income would top 200K. Given this opportunity, I'm disturbed and excited. Effectively, I'm being groomed for the leadership role of an organization that I loathe and entirely do not believe in. Otoh, the challenge is exciting and I could always use more money. So I'm going to make the best of this situation and go for gold!

3. Our living space situation has become intolerable. My son is over 2 years old now and incredibly naughty. Every time we turn our backs, our little man is busy trashing the apartment or peeing over my stuff. 700 square feet is just not enough for 3 people to live in, especially since one is so energetic!!!! So we've decided to buy a house. This will increase commute and saddle us with a small mortgage, but I will do my absolute best to minimize debt and commuting time by picking the right house.

Monthly Savings Rate: 68.9%

YTD Savings Rate: 57.5%

Months Living Expenses: 114

Major happenings:

Lots of things came to a head at the end of July.

1. My wife has entirely exhausted her savings. She has a negative balance in her checking account and 500 dollars in credit card debt due that she can't pay until her next paycheck. What is troubling to me is that when we split our finances 4 months ago, I left her with over $5,000 in her checking account. And she had $1600 a month in spending money from her day job for the last 4 months. So basically, DW spent over $11,000 in 4 months on luxury products and redundant baby supplies.

So DW was panicking again and ultimately, I had to re-gain direct control of her finances. She gave me her credit card, debit card, and check book. And we are going back to the cash-in-envelope system. She agreed to be content with $1200 a month to spend for non-essentials as long as I make her debt problems go away. I feel like this cash-only approach causes a lot of friction between us, but it seems to be the only way to save my wife from herself.

2. Strange things are afoot at my day job. The VP of the company basically offered me a role that would lead to a promotion to tech executive position. If I can handle this challenge, then my day job's income would top 200K. Given this opportunity, I'm disturbed and excited. Effectively, I'm being groomed for the leadership role of an organization that I loathe and entirely do not believe in. Otoh, the challenge is exciting and I could always use more money. So I'm going to make the best of this situation and go for gold!

3. Our living space situation has become intolerable. My son is over 2 years old now and incredibly naughty. Every time we turn our backs, our little man is busy trashing the apartment or peeing over my stuff. 700 square feet is just not enough for 3 people to live in, especially since one is so energetic!!!! So we've decided to buy a house. This will increase commute and saddle us with a small mortgage, but I will do my absolute best to minimize debt and commuting time by picking the right house.

-

WorkingWageWealth

- Posts: 51

- Joined: Sun Aug 18, 2013 5:47 pm

Re: DebtSlaveNoMore's Journal

I really enjoy reading your journal; seeing how you used it to chronicle your challenges and successes was one of the contributing factors to me registering for the site. Your journal is like a mini ERE drama and I am always checking in for updates about weightloss, your wife's conumerism, the day job, etc. Thank you for the motivation. I look forward to new entries.

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

Thanks WorkingWageWealth, I'm glad that this journey is motivating others! I checked out your Journal as well. Best of luck on your debt pay down!

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

Been a little tardy with the updates, too many things are happening in my life at the moment but here is the 1000 ft view of what transpired in August:

Monthly Savings Rate: 38.9%

YTD Savings Rate: 55.2%

Months Living Expenses: 68

Difficulties....

August was a painful month in terms of pretty much everything. I had to pay property taxes on my rental property. My wife has fully switched back onto the cash-only system, but most of her pay checks for august had to be spent paying off the credit card debt that she built up in the previous 4 months where she had full control of her own finances. This arrangement is hardly ideal but thankfully DW is much more accepting of the cash-system now since this is the 2nd time where I had to step in to prevent a total collapse of her finances. The complexity is that there are several thousand dollars of credit card debit that had accrued on 2 credit cards. DW created a 2nd credit line without talking to me about it. In August, we paid off 1 of those cards and promptly cancelled it. There is one more card to pay off in September.

More Difficulties....

August was a rough month for me at the day job. I'm painfully transitioning into this executive position. It entails kissing the bottoms of multiple(not-so-friendly) clients whose money keep the entire account employed. I also seem to get the hardest technical problems to solve, which would normally be fun, except I'm too busy with the clients. So I'm working like a slave, I've been working nights, and every weekend and it sux (_|_)!!! It's so miserable that I had this wonderful, joyous dream about the days of my youth when I worked as a manual laborer on a farm. I woke up and became incredibly depressed that I'm living this life now rather than the the life I had as a teenager. At least back then, I had fresh air and some actual friends at work.

Anyways, I've ranted enough. I simply need to buck up and focus on the tasks at hand and do my best to succeed.

Monthly Savings Rate: 38.9%

YTD Savings Rate: 55.2%

Months Living Expenses: 68

Difficulties....

August was a painful month in terms of pretty much everything. I had to pay property taxes on my rental property. My wife has fully switched back onto the cash-only system, but most of her pay checks for august had to be spent paying off the credit card debt that she built up in the previous 4 months where she had full control of her own finances. This arrangement is hardly ideal but thankfully DW is much more accepting of the cash-system now since this is the 2nd time where I had to step in to prevent a total collapse of her finances. The complexity is that there are several thousand dollars of credit card debit that had accrued on 2 credit cards. DW created a 2nd credit line without talking to me about it. In August, we paid off 1 of those cards and promptly cancelled it. There is one more card to pay off in September.

More Difficulties....

August was a rough month for me at the day job. I'm painfully transitioning into this executive position. It entails kissing the bottoms of multiple(not-so-friendly) clients whose money keep the entire account employed. I also seem to get the hardest technical problems to solve, which would normally be fun, except I'm too busy with the clients. So I'm working like a slave, I've been working nights, and every weekend and it sux (_|_)!!! It's so miserable that I had this wonderful, joyous dream about the days of my youth when I worked as a manual laborer on a farm. I woke up and became incredibly depressed that I'm living this life now rather than the the life I had as a teenager. At least back then, I had fresh air and some actual friends at work.

Anyways, I've ranted enough. I simply need to buck up and focus on the tasks at hand and do my best to succeed.

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

September has brought on a whirlwind of change in our household, first the numbers:

Monthly Savings Rate: 49.1%

YTD Savings Rate: 54.5%

Months Living Expenses: 78

Everything happened at once....

In mid September, the tenant of the rental property(in Pennsylvania) abruptly called up and said he was moving out, he gave me a 3 day notice and left the rental house in a terrible condition. He still owes me over a thousand dollars in back rent which he has not paid. I would be very upset by all of this, but the man did pay off half of my mortgage over the years, so net-net it's still a huge gain for me.

At the same time, DW was getting majorly stressed out by all the changes in the public school system where she was working. NYC's public school system is rolling out the "common-core" standards, and the unionized teachers are getting laid off in droves. She did not want to work full time there since the environment is demotivating as hell and she wanted more time with our son. After talking it over, we realized that it actually makes a lot of sense for us to re-locate our family to that rental house in Pennsylvania and have my wife find a part time job there.

Now the final hurdle was my day job. That job is stressing the living hell out of me and as I scheduled a meeting with my boss to talk about the move, I was pretty sure that he was just going to hand me a pink slip there on the spot. Apparently that did not happen. I was able to negotiate a semi work-from-home scheme, where I can telecommute 3 days out of the week, and come into the office the other 2 days. The benefit here is that I get to keep my NYC salary while relocating to semi-rural PA.

With the job secured, the move to PA is now underway. Because I own that rental property free and clear, moving there will eliminate rent and parking ($1700) as a monthly expenditure. Furthermore, because my parents are 5 miles away from the rental property and the local daycare is dirt cheap, we'll be able to shave another $1000 a month in child care costs. Car insurance is less than 1/2 of what it costs in NYC. Food, utilities, and water are all much cheaper as well AND I will have a 300 square feet garden space in the rental house's backyard. So all things considered, we should be able to shave our monthly expenses in half due to this move.

Now for the difficulties

The house needs some serious TLC. The tenant family has 4 kids and they totally trashed the house. The entire house needs to be painted. Most of the carpeting will need to be replaced. Many of the closet doors are broken, and the 2 bathrooms will need to be re-tiled and re-caulked. The entire interior of the house will need contractor work to make it move-in ready.

The backyard was utterly overgrown with thorny bushes, and the fence was in a state of dis-repair. So for the last couple of weekends, I've been driving down to PA to do some of the repairs myself to save money. My father and I cleared out the backyard vegetation, tore down the old fence, and put up a new wooden fence. Then last weekend, I stained the backyard fence and did some concrete work on the house's front and back entrances.

So I've been working ridiculous hours every week, 60 hours a week on the day job, 5 hours a week on my side business, another 10-15 hours a week fixing up the PA house. Still, things are looking up and I'll keep on trucking!!!

Monthly Savings Rate: 49.1%

YTD Savings Rate: 54.5%

Months Living Expenses: 78

Everything happened at once....

In mid September, the tenant of the rental property(in Pennsylvania) abruptly called up and said he was moving out, he gave me a 3 day notice and left the rental house in a terrible condition. He still owes me over a thousand dollars in back rent which he has not paid. I would be very upset by all of this, but the man did pay off half of my mortgage over the years, so net-net it's still a huge gain for me.

At the same time, DW was getting majorly stressed out by all the changes in the public school system where she was working. NYC's public school system is rolling out the "common-core" standards, and the unionized teachers are getting laid off in droves. She did not want to work full time there since the environment is demotivating as hell and she wanted more time with our son. After talking it over, we realized that it actually makes a lot of sense for us to re-locate our family to that rental house in Pennsylvania and have my wife find a part time job there.

Now the final hurdle was my day job. That job is stressing the living hell out of me and as I scheduled a meeting with my boss to talk about the move, I was pretty sure that he was just going to hand me a pink slip there on the spot. Apparently that did not happen. I was able to negotiate a semi work-from-home scheme, where I can telecommute 3 days out of the week, and come into the office the other 2 days. The benefit here is that I get to keep my NYC salary while relocating to semi-rural PA.

With the job secured, the move to PA is now underway. Because I own that rental property free and clear, moving there will eliminate rent and parking ($1700) as a monthly expenditure. Furthermore, because my parents are 5 miles away from the rental property and the local daycare is dirt cheap, we'll be able to shave another $1000 a month in child care costs. Car insurance is less than 1/2 of what it costs in NYC. Food, utilities, and water are all much cheaper as well AND I will have a 300 square feet garden space in the rental house's backyard. So all things considered, we should be able to shave our monthly expenses in half due to this move.

Now for the difficulties

The house needs some serious TLC. The tenant family has 4 kids and they totally trashed the house. The entire house needs to be painted. Most of the carpeting will need to be replaced. Many of the closet doors are broken, and the 2 bathrooms will need to be re-tiled and re-caulked. The entire interior of the house will need contractor work to make it move-in ready.

The backyard was utterly overgrown with thorny bushes, and the fence was in a state of dis-repair. So for the last couple of weekends, I've been driving down to PA to do some of the repairs myself to save money. My father and I cleared out the backyard vegetation, tore down the old fence, and put up a new wooden fence. Then last weekend, I stained the backyard fence and did some concrete work on the house's front and back entrances.

So I've been working ridiculous hours every week, 60 hours a week on the day job, 5 hours a week on my side business, another 10-15 hours a week fixing up the PA house. Still, things are looking up and I'll keep on trucking!!!

Re: DebtSlaveNoMore's Journal

WOW

I suppose I had missed the finer parts of your journal. Everything has definitely happened at once. You applied a huge crowbar to your situation! After those drastic changes simmer down you are going to be in a great place. I hope your wife is as happy as you are about all this. (I would like to here more about how you guys find a common ground as my wife (and children) do keep me from pulling out the crowbar.) Having your parent's help is huge and I hope she has a good relationship with them.

80 hours weeks devoted to "work" do not bode well for one's health concerning diet, exercise or promotion of mental health. I know this from experience. In part because of my years of working to much, I hold on to negative habits and I still struggle with consistently making the right thing health choices for myself even after ditching my own 80 hour per week problem. I saw your last post did not mention health and wonder if you struggle with the same consistency.

You have a great journal start. You will look back fondly at your progress as your journey continues!

I suppose I had missed the finer parts of your journal. Everything has definitely happened at once. You applied a huge crowbar to your situation! After those drastic changes simmer down you are going to be in a great place. I hope your wife is as happy as you are about all this. (I would like to here more about how you guys find a common ground as my wife (and children) do keep me from pulling out the crowbar.) Having your parent's help is huge and I hope she has a good relationship with them.

80 hours weeks devoted to "work" do not bode well for one's health concerning diet, exercise or promotion of mental health. I know this from experience. In part because of my years of working to much, I hold on to negative habits and I still struggle with consistently making the right thing health choices for myself even after ditching my own 80 hour per week problem. I saw your last post did not mention health and wonder if you struggle with the same consistency.

You have a great journal start. You will look back fondly at your progress as your journey continues!

Re: DebtSlaveNoMore's Journal

Yes, I would say DOUBLE-WOW -- you have really taken a bull by the horns here and wrestled it to the ground.

You wrote:

"In mid September, the tenant of the rental property (in Pennsylvania) abruptly called up and said he was moving out, he gave me a 3 day notice and left the rental house in a terrible condition. He still owes me over a thousand dollars in back rent which he has not paid. I would be very upset by all of this, but the man did pay off half of my mortgage over the years, so net-net it's still a huge gain for me."

The is an excellent and inspirational example of what we have talked about in other threads about expressing gratitude and finding silver linings in clouds. You really turned a potential disaster into a great opportunity to improve your situation.

You wrote:

"In mid September, the tenant of the rental property (in Pennsylvania) abruptly called up and said he was moving out, he gave me a 3 day notice and left the rental house in a terrible condition. He still owes me over a thousand dollars in back rent which he has not paid. I would be very upset by all of this, but the man did pay off half of my mortgage over the years, so net-net it's still a huge gain for me."

The is an excellent and inspirational example of what we have talked about in other threads about expressing gratitude and finding silver linings in clouds. You really turned a potential disaster into a great opportunity to improve your situation.

-

WorkingWageWealth

- Posts: 51

- Joined: Sun Aug 18, 2013 5:47 pm

Re: DebtSlaveNoMore's Journal

Will you also be able to save money on taxes? One of the things I forgot about in my move from a city back to a more rural environment was the lack of city taxes. Will you still have to pay NYC taxes because you work there or will they no longer apply because you don't live there?

In any instance, CONGRATULATIONS, you continue to inspire me.

In any instance, CONGRATULATIONS, you continue to inspire me.

-

RealPerson

- Posts: 875

- Joined: Thu Nov 22, 2012 4:33 pm

Re: DebtSlaveNoMore's Journal

What an amazing and inspiring story. You did wrestle a bull to the ground. Your story goes so fast it almost reads like a thriller.

One suggestion I might make is the spending habits of DW. It seems that they are very dfficult to control. This in turn leads almost to a parent-child relationship, with you taking full control of your DW finances. Clearly, your wife is using big spending as a way to cope with some psychological issue. It may be helpful to her and to your relationship to seek some counseling to help her work through this. It sounds like her parents may be struggling with a similar problem, since you mentioned the cost of the roof replacement issue.

Still an inspirational story. Congratulations.

One suggestion I might make is the spending habits of DW. It seems that they are very dfficult to control. This in turn leads almost to a parent-child relationship, with you taking full control of your DW finances. Clearly, your wife is using big spending as a way to cope with some psychological issue. It may be helpful to her and to your relationship to seek some counseling to help her work through this. It sounds like her parents may be struggling with a similar problem, since you mentioned the cost of the roof replacement issue.

Still an inspirational story. Congratulations.

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

@sshawn, yeah this work pace is killing me. And unfortunately I am stress eating. Hopefully when this move is complete, I can calm down and go back to a more sane diet and exercise pattern.

@Dragline, thanks man! I've found that the only way to keep myself sane sometimes is to hold on to that thin sliver of positivity

@WorkingWageWealth, I am saving heaps of money on taxes. I'll be paying around $1500 in property taxes every year for this house in PA that we're moving to. And it looks like I will no longer have to pay NYC muni taxes!!!!! Woot!!!!

@RealPerson, I've suggested counseling to her so many times already. She just doesn't want to do it, yet my wife can't control herself at all when there is money to e spent. When I first met her, we were both in the same financial boat, but over the years, I've fell out of love with consumerism whereas she has not. So when I cap her spending, I feel bad because I can see that DW feels like she's missing out on life. The money in an envelope system is the only solution that actually works for us. And yes, it really gets annoying for me because it is very much like a parent-child relationship. Her mother is exactly the same, she spends every dime that she has on useless status symbols. I think MIL does this because she never went to college and perhaps always felt inferior to her peers because of it.

@Dragline, thanks man! I've found that the only way to keep myself sane sometimes is to hold on to that thin sliver of positivity

@WorkingWageWealth, I am saving heaps of money on taxes. I'll be paying around $1500 in property taxes every year for this house in PA that we're moving to. And it looks like I will no longer have to pay NYC muni taxes!!!!! Woot!!!!

@RealPerson, I've suggested counseling to her so many times already. She just doesn't want to do it, yet my wife can't control herself at all when there is money to e spent. When I first met her, we were both in the same financial boat, but over the years, I've fell out of love with consumerism whereas she has not. So when I cap her spending, I feel bad because I can see that DW feels like she's missing out on life. The money in an envelope system is the only solution that actually works for us. And yes, it really gets annoying for me because it is very much like a parent-child relationship. Her mother is exactly the same, she spends every dime that she has on useless status symbols. I think MIL does this because she never went to college and perhaps always felt inferior to her peers because of it.

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

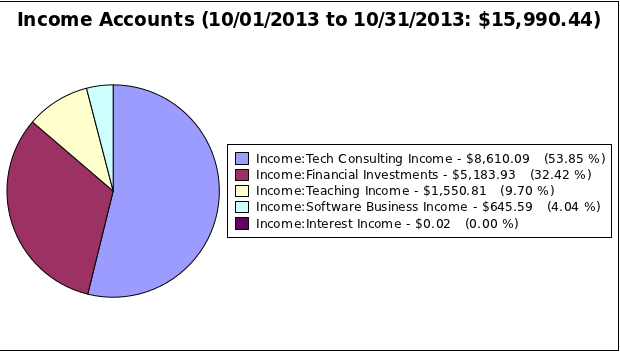

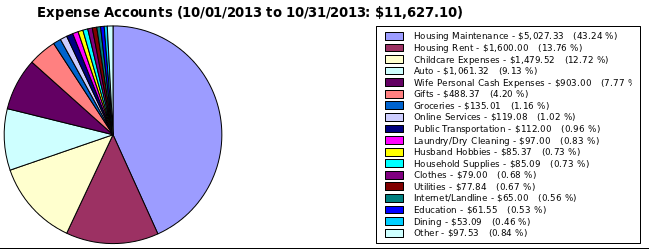

And the numbers are in for October:

Income:

Expenses:

Monthly Savings Rate: 27.3%

YTD Savings Rate: 51.8%

Months Living Expenses: 44 months

The move has finally happened! We are now chillaxing in our new/old house in PA. This has been a crazy time for the family. The house repairs have been enormously costly, and October only shows a small portion of the total costs. In addition to housing repairs, all major appliances in the house had to be replaced. The tenant trashed everything, the refrigerator, washer, dryer, and range are all busted and had to be replaced. When everything is said and done, I will have spent over 26K dollars to fix this place up, but the deed is done

Now that we have moved in, we have to spend several more thousands of dollars to get furniture since our living space has effectively doubled. I am trying my best to get stuff at consignment shops in order to save money. I now have my very own man-cave/workshop while DW has her own art studio!!!! The day job is holding steady, it sux (_|_) but I'm marching onwards. My software side-business earnings are tanking due to neglect, I need to get back onto that bull just as soon as things are settled on the housing front.

In the near term, my numbers are taking a huge hit because of all the housing repairs. Within 6 months, I believe that our family's total monthly spending will drop to around $2,500 per month. This is due to the following major reasons:

1. We no longer have to pay rent or a mortgage. Taxes/insurance on the house is approximately $280/month

2. Childcare costs have now dropped to $500 dollars per month because day care is so much cheaper in PA

3. Auto costs will fall by 50% to $200 a month because insurance/repairs/gas is that much cheaper in PA

As such, I'm anticipating that a minimum state of FI at 4% withdraw rate for my household can be reached by the middle of 2015 if all goes according to plans.

Income:

Expenses:

Monthly Savings Rate: 27.3%

YTD Savings Rate: 51.8%

Months Living Expenses: 44 months

The move has finally happened! We are now chillaxing in our new/old house in PA. This has been a crazy time for the family. The house repairs have been enormously costly, and October only shows a small portion of the total costs. In addition to housing repairs, all major appliances in the house had to be replaced. The tenant trashed everything, the refrigerator, washer, dryer, and range are all busted and had to be replaced. When everything is said and done, I will have spent over 26K dollars to fix this place up, but the deed is done

Now that we have moved in, we have to spend several more thousands of dollars to get furniture since our living space has effectively doubled. I am trying my best to get stuff at consignment shops in order to save money. I now have my very own man-cave/workshop while DW has her own art studio!!!! The day job is holding steady, it sux (_|_) but I'm marching onwards. My software side-business earnings are tanking due to neglect, I need to get back onto that bull just as soon as things are settled on the housing front.

In the near term, my numbers are taking a huge hit because of all the housing repairs. Within 6 months, I believe that our family's total monthly spending will drop to around $2,500 per month. This is due to the following major reasons:

1. We no longer have to pay rent or a mortgage. Taxes/insurance on the house is approximately $280/month

2. Childcare costs have now dropped to $500 dollars per month because day care is so much cheaper in PA

3. Auto costs will fall by 50% to $200 a month because insurance/repairs/gas is that much cheaper in PA

As such, I'm anticipating that a minimum state of FI at 4% withdraw rate for my household can be reached by the middle of 2015 if all goes according to plans.

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

Here are the numbers for November

Monthly Savings Rate: -40.8%

YTD Savings Rate: 43.4%

Months Living Expenses: 21 months

And for December:

Monthly Savings Rate: 62.3%

YTD Savings Rate: 45%

Months Living Expenses: 98 months

Monthly Savings Rate: -40.8%

YTD Savings Rate: 43.4%

Months Living Expenses: 21 months

And for December:

Monthly Savings Rate: 62.3%

YTD Savings Rate: 45%

Months Living Expenses: 98 months

-

DebtSlaveNoMore

- Posts: 57

- Joined: Sat Feb 02, 2013 7:27 pm

Re: DebtSlaveNoMore's Journal

2013 Retrospective

So 2013 has been a very difficult and rewarding year. We have managed to save 45% of our income and closed out the year with 98 months worth of living expenses. Furthermore, we have managed to relocate the family out of NYC and into a significantly lower cost state.

Challenges along the way

During this year, the single biggest drain on resources was the move out of NYC. It has so far set me back by 26K dollars and I will still need to pay more before I'm entirely done with it. This was a painful move, filled with headaches, heartaches, and backaches.... X(. With that said, I don't think I have it in me to move again for at least another 4-5 years. Uprooting has proved to be THAT difficult.

There has been quite a few skirmishes this year with my dear wife over her money management issues. At this point in time, I think we've settled back into the cash in an envelope system. All other options that gave her more control over her own money has been very unsatisfactory, with the last attempt this past summer resulting in a negative balance in her checking account and a massive pile of useless consumer goods. That was a huge setback, with many thousands of dollars was squandered in this effort. So now, we are back to square one, and the cash system is the only method that seems to work.

Dear wife's parents are entering increasingly dire financial straights. As such, we have had to bail them out for the last several months now. I see this becoming a long term trend since they have nothing set aside for their retirement except for the house that my FIL inherited from his parents. This is going to get painful in 2014, I just know it...

Strategic Opportunities for 2014

Ideally, if our household budget could be further optimized to take advantage of the lower cost of living at our new locale, then the time to Financial independence will be halved. The thing that I need to do is revisit the budget and cut every shred of excess out of it. One complication here is that DW and I are trying to have another child, this will increase cost, but it's worth it!

My day job is increasingly evolving into a Executive role. Now I'm directing many separate development teams and flying out to see client executives on a semi-regular basis. I have a secretary and meals at work are increasingly being catered. It is a possibility that I might get promoted into a Executive level position at some point in 2014. I'll have to wait and see. If that becomes a reality, I think I will use this as a spring board to jump to a CTO level position at some point in the near future.

The core money-makers for my side business (smartphone apps and niche sites) are clearly on the decline. Revenue has been falling for the last 6 months. The good news here is that I'm in the process of re-deploying my efforts towards newer technologies such as Wearable apps and Crypto-currencies. These 2 areas have the potential of massive profits and I'm getting into both in a serious way in 2014.

Finally, I sense a major correction in the market coming soon. I don't have enough facts to back it up, but it's just a very strong feeling. Thus, I've begun to scale back on my financial investments and to hoard cash. If the market tanks in 2014, I will be in a good position to pick out valuable ETFs/REITs/MFs at a bargain.

So 2013 has been a very difficult and rewarding year. We have managed to save 45% of our income and closed out the year with 98 months worth of living expenses. Furthermore, we have managed to relocate the family out of NYC and into a significantly lower cost state.

Challenges along the way

During this year, the single biggest drain on resources was the move out of NYC. It has so far set me back by 26K dollars and I will still need to pay more before I'm entirely done with it. This was a painful move, filled with headaches, heartaches, and backaches.... X(. With that said, I don't think I have it in me to move again for at least another 4-5 years. Uprooting has proved to be THAT difficult.

There has been quite a few skirmishes this year with my dear wife over her money management issues. At this point in time, I think we've settled back into the cash in an envelope system. All other options that gave her more control over her own money has been very unsatisfactory, with the last attempt this past summer resulting in a negative balance in her checking account and a massive pile of useless consumer goods. That was a huge setback, with many thousands of dollars was squandered in this effort. So now, we are back to square one, and the cash system is the only method that seems to work.

Dear wife's parents are entering increasingly dire financial straights. As such, we have had to bail them out for the last several months now. I see this becoming a long term trend since they have nothing set aside for their retirement except for the house that my FIL inherited from his parents. This is going to get painful in 2014, I just know it...

Strategic Opportunities for 2014

Ideally, if our household budget could be further optimized to take advantage of the lower cost of living at our new locale, then the time to Financial independence will be halved. The thing that I need to do is revisit the budget and cut every shred of excess out of it. One complication here is that DW and I are trying to have another child, this will increase cost, but it's worth it!

My day job is increasingly evolving into a Executive role. Now I'm directing many separate development teams and flying out to see client executives on a semi-regular basis. I have a secretary and meals at work are increasingly being catered. It is a possibility that I might get promoted into a Executive level position at some point in 2014. I'll have to wait and see. If that becomes a reality, I think I will use this as a spring board to jump to a CTO level position at some point in the near future.

The core money-makers for my side business (smartphone apps and niche sites) are clearly on the decline. Revenue has been falling for the last 6 months. The good news here is that I'm in the process of re-deploying my efforts towards newer technologies such as Wearable apps and Crypto-currencies. These 2 areas have the potential of massive profits and I'm getting into both in a serious way in 2014.

Finally, I sense a major correction in the market coming soon. I don't have enough facts to back it up, but it's just a very strong feeling. Thus, I've begun to scale back on my financial investments and to hoard cash. If the market tanks in 2014, I will be in a good position to pick out valuable ETFs/REITs/MFs at a bargain.

Re: DebtSlaveNoMore's Journal

Very interesting journal. Impressive turnaround in finances, and a successful year. Congratulations!

I feel for you with the financial issues around your wife and her family. I apologise if I'm speaking out of turn, but it does sound like your wife is being somewhat selfish and you're the only one willing to compromise significantly to make the marriage work. I know it's not really my place to comment, all the more because I have zero experience of marriage, but I do know a lot of marriages break down over money, and it's something I think you need to hammer out whether she likes it or not. You have such strong earning ability that you can still drag the whole family into FI pretty quickly, but it's a matter of principle and the issue will just fester if left unresolved.

I feel for you with the financial issues around your wife and her family. I apologise if I'm speaking out of turn, but it does sound like your wife is being somewhat selfish and you're the only one willing to compromise significantly to make the marriage work. I know it's not really my place to comment, all the more because I have zero experience of marriage, but I do know a lot of marriages break down over money, and it's something I think you need to hammer out whether she likes it or not. You have such strong earning ability that you can still drag the whole family into FI pretty quickly, but it's a matter of principle and the issue will just fester if left unresolved.