Update

2016 is not ended yet, but I don't expect any major changes anymore....

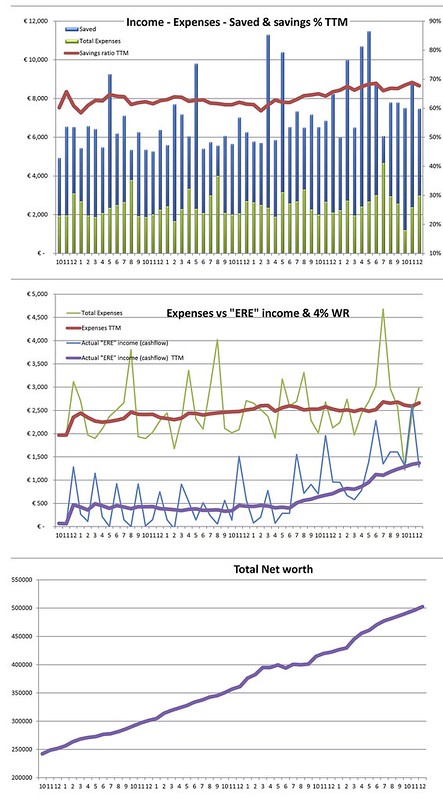

Our average expenses are already 4+ years close to 2500 euro / month and lately getting close to 2600 euro. Probably it is increasing slightly do to the wedding, a new car and growing up kids....we can cut if we want, but this level seems to be okay for all persons in our family

Income has increased due to raises in the last 4+ years and the income from assets (mostly rentals now). We should see another jump next year when we receive the rent of the 3rd rental. This should push our savings rate over the 70%.

With some slight adjustment in appraising the real estate, still quite conservative, NW is now around 500K.

My target date to quit is September 2019 or, if I can stand it it will be March 2020 (6 more months will result in about a 9 month normal pay due to a bonus + tax advantage). We'll see.

Some graphics again after a very long time:

(click for a larger version)

I met my supervisor earlier this month. On my question what I should change or improve he said just keep doing what you are doing. Ok....that is not really pushing me or helping my motivation but I'll take it

I wish everybody in the ERE community the best for 2017! Hope to meet some of you (again) in the (near) future in person.

Thanks for reading.